Editor’s Note: This is not an investment article but an article about macro economic modelling. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

Readers know that we distinguish between “Macro” and “Micro” views of the Indian economy. We have always been and remain bullish of the micro story in India, the story of Indian businesses, the story of hardworking Indians, the story of the Indian entrepreneurial class. We celebrated it last week in our article Sensex at All-Time Highs – A Diwali Celebration. In that article, we discussed how financial technology helps in investing in Indian financial assets like stocks and Rupee.

We have been negative on the “macro” story in India and rightly so. The Indian Rupee has suffered 3 collapses in the past two years. The Indian economy is going through a period of slowing growth and rising inflation, an awful combination that is overriding the entrepreneurial drive and hard work of Indians. This happens partly because of the utter incompetence of the current government and the total focus of the political class on getting immensely wealthy via corruption.

But this condition is also due to the ignorance and intellectual arrogance of the “Educated Indian” class. We have been reading articles about the Indian economy by Indian economists and Indian think-tankers in US. These articles are, almost without exception, focused on minutiae and fail to provide a model for sensibly thinking about the Indian economy.

So we describe below a macro model that we use in our own thinking. A macro model is a framework that helps you understand the environment, the forces that drive it and, above all, helps you to successfully benefit from it. Our model helped us in suggesting a strategic exit from Indian assets in 2011 and in a tactical entry in late August 2013.

Recently, a reader wrote to us about the excellent & now famous macroeconomic model put forth by Ray Dalio, one of the most important investors in the world. This 31-minute presentation titled How The Economic Machine Works is a must watch by every reader.

But how can this Dalio model be applied to India, our reader asked. We responded with a quick email and he encouraged us to write in detail about our model of Indian economy being governed by 2 different Central or Reserve banks. So here it is.

1. The Role of Credit

According to Dalio,

- “Credit” is the most important part of the economy and the least understood. It is the most important because it is the biggest and the most volatile part. … when credit is available, you have growth and when credit is unavailable, you have a slowdown”.

But Credit is different from money. As Dalio says, “most of what people call money is credit”. And he makes the difference crystal clear with:.

- “The total amount of credit in the US is $50 trillion and the total amount of money is only about $3 trillion.” (minute 09:55 of the clip below)

In other words, the amount of credit available in the USA is 16 times the amount of money in the USA. And the US has the financial system to generate and absorb this amount of credit (something India lacks, by the way). This is why Robert Shiller, a 2013 Nobel prize winner, teaches that the economic growth of a country is proportional to the size of its financial system.

But is this availability of credit good? Dalio says:

- “Credit is bad when it finances over-consumption & when you can’t pay it back,”

- “Credit is good when it efficiently allocates resources and produces income so you can pay back the debt”

We all saw the bad side in America in 2003-2007 when ample cheap credit created the bubble that bust in 2008. Emerging markets went through their own bubble from 2004 to 2011 and they are undergoing the bust now. But look at the respective currencies during the busts. The US Dollar remained strong while the Rupee and other EM currencies have fallen fast and big. The simple reason is America’s deep, liquid and mostly efficient financial system of markets. But more on that later.

Dalio also teaches that “increased productivity is the only way for growth” and that “productivity matters the most in the long run”. Those “who were inventive and hard working raise their productivity and living standards faster” in the long run. But that doesn’t matter in the short term:

- “Productivity matters the most in the long run but credit matters the most in the short run. This is because productivity growth doesn’t fluctuate much. So its not a big driver of economic swings.”

- “… swings … are not due to how much innovation of hard work there is, they are primarily due to how much credit there is“

These short term (5-8 years) swings are called “cycles” and these cycles are controlled via monetary policies that increase credit during slowdowns and curtailing credit during high growth cycles.

And who controls this creation-reduction of Credit? The Central/Reserve Bank.

2. The Central/Reserve Bank that governs credit in India

The Indian economy is highly responsive to credit growth. When credit is easily and cheaply available, Indian economy grows fast and spreads prosperity. But when credit growth stalls, as in 2008 or now, Indian economy slows down quickly.

India doesn’t generate the credit it needs internally. Forget generating credit. India suffers from a huge current account deficit meaning India needs inflows from foreign investors just to pay its bills. As a result, the Indian economy is critically dependent on foreign investors for credit growth. So credit growth in India is mainly governed, at least at the margin, by the level of risk appetite of global investors.

And what entity governs the risk appetite of global investors? The U.S. Federal Reserve and its chairman Ben Bernanke. When Bernanke eases monetary policy, he increases risk appetite of global investors and that risk appetite gets translated into investments in high growth areas of the world which results in inflows and credit growth in India.

Conversely when Bernanke began talking about curtailing his easy monetary policy,

interest rates in the US shot up. That immediately reduced the risk appetite of global investors and they began selling their risk assets. This created outflows of capital from India and credit growth in India slowed to a virtual halt.

Remember the quotes of Ray Dalio in section 1 above. The short term swings (5-8 years) in an economy are entirely due to swings in credit or what is known is the short term credit cycle. And who governs the short term credit cycles? The Central Bank.

So you put these two paragraphs together and what logical deduction do you get?

- That the primary Central Bank for the Indian economy is the U.S. Federal Reserve and not the Reserve Bank of India.

Yes, we know and understand that this is difficult to swallow. Yes, it feels like colonial British rule again when the fate of Indians was dependent on policy set in London. But macro models are meant to reflect reality and not dreams. And macro models are used to suggest actions to benefit from reality.

This model is why our case for a tactical entry into Indian stocks & rupee in late August was partly based on our call for lower interests in the USA. And that model also shows why this week Indian stocks fell hard and the Indian rupee began weakening. Why? Because interest rates in US went up this week on expectations of more hawkish monetary policy in the December meeting of the US Federal Reserve.

3. Vagaries of Indian Monsoon & Food Infrastructure

This dependence of the Indian economy on the US Federal Reserve reminds us of the old problem in Indian agriculture. For decades and centuries, Indian agriculture and rural economy have been critically dependent on monsoon rains. Years of plentiful rains would result in large crops and economic growth while years of weaker monsoon would create hunger, famine and curtail economic growth. Even years of strong monsoon created problems due to flooding.

Yet, India did very little and continues to do little to protect itself from the vagaries of monsoon. India has not built enough reservoirs to store water or build an interconnected canal network to distribute water across the country.

The same story applies to agriculture. The cycles of good harvest and drought have been a part of Indian economy for decades. And even good harvests don’t help because, 30-35% of food production reportedly rots and becomes useless. India has not bothered to build climate controlled granaries to store food grains as strategic reserve. And India has ignored building a network to distribute food from agricultural regions to consuming regions.

This pattern is evident in the Indian financial system.

4. Why doesn’t the US have India’s problems?

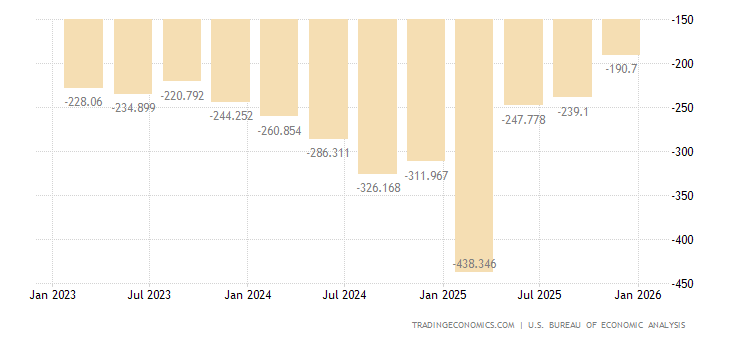

The US runs a very high current account deficit just as India does. In fact, the US current account deficit is higher than India’s as a ratio of GDP. And it was far worse in 2008-2009 as the chart below shows:

And the US economy showed the same signs of over-consumption in 2006-2007 that Indian economy showed in the past couple of years. So why didn’t the US Dollar collapse in 2008-2009 the way the Indian Rupee collapsed in 2011-2012?

The answer is the deep, liquid, interconnected system of financial markets in the US. So capital runs to the USA whenever there is a problem in the world while capital runs out of India. The primary financial reservoir in the US is the Treasury market, the market for trading U.S. Government issued bonds. This reservoir is linked to other functional or regional reservoirs like the Corporate Investment Grade bond market, the High Yield or Junk bond market, the Municipal or local State & City bond market. Continuous financial innovation in these markets keeps them efficient and liquid.

It is this massive financial infrastructure is what makes the U.S. Federal Reserve the predominant central bank in the world, the ultimate arbiter of increase & decrease in global risk capital.

In contrast, the Reserve Bank of India is virtually powerless because India lacks even the most rudimentary level of financial infrastructure. So capital flows into India in good times like a bountiful monsoon and evaporates in bad time creating a credit drought in the Indian economy.

5. The Reserve Bank of India

The Reserve Bank of India (RBI) is itself responsible for many of its problems. The RBI leadership only understands the science of economics. No one at the RBI has ever understood technology of markets. In fact, in their academic intellectual arrogance, the RBI establishment has looked down on “speculators”, their word for traders. They have never understood that speculators make markets at the margin and without speculative traders markets can never attain liquidity or depth. And because they don’t understand markets, they get petrified at the thought of losing their control over policy.

This is why the Indian Rupee trades in Singapore and not in India. Yes, the RBI has refused to permit trading of the Indian Rupee, its national currency, in India, its own bailiwick. How dumb is this? Now you understand how powerless the RBI is influencing its own currency?

To be candid, the RBI is a small insignificant powerless institution when compared with major central banks and global markets. But their ignorance and resultant arrogance are actually making the RBI more insignificant than they should be.

This is a key reason why the Reserve Bank of India has been unable to protect the Indian economy from ravages of high inflation, weak credit growth and emerging stagflation. This is a key reason why India is a story of cyclical excesses, extreme optimism about India’s great future and deep pessimism about India’s pathetic macro present.

This is why the Reserve Bank of India is only a minor Central Bank for the Indian economy, the primary or major central bank being the U.S. Federal Reserve. And that will continue until they help build liquid, deep bond markets in India.

This is our dual central bank macro model for thinking about investing in India.

Editor’s PS:

- Today’s English-Educated Indians have forgotten Artha Ev Pradhan or अर्थ एव प्रधान:

from Artha-Shaastra, the science of Money, that governed Indian thinking from the beginning of time. It was in 4rd century BCE when Vishnu-Gupt Chanakya wrote his treatise on Money, a collection of great Indian thinkers of antiquity about monetary policy; yes thinkers who represented antiquity to him in 4th century BCE. - The clip of Ray Dalio is a must watch in our opinion. We include it below:

Send your feedback to [email protected] Or @MacroViewpoints on Twitter