Editor’s Note: In this series of articles, we include important or interesting tweets, articles, videoclips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. “what was good for last several weeks is not good right now”

said Rick Santelli on Friday morning. And he was absolutely right. He was speaking about this week’s reversal in trades that have worked until now. Last Friday morning saw a spike in Treasuries and Gold. This week, there was a reverse spike.

Last week, our article discussed the flattening in the 30-5 year yield curve and the fall in the 30-10 year yield spread, our favorite indicator. Remember that the flattening in the 30-5 year accelerated and became directional with Dr. Yellen’s “6 months” comment in March. The combination of the new sooner rate rise prospects and the steady removal of easing led to the relentless flattening in the Treasury curve.

Did that change or at least pause as the tweet below suggested on Wednesday late morning?

- Jack Rodeghier @glarustrading – US5-30 re-steepening underway?Yellen msg too low for too long -> FV > consol band: use US call spds to fund FV calls pic.twitter.com/AxQnXaiygS

Wednesday also featured a strong 10-year Treasury auction. So long Treasuries appeared to be in a Panglossian world on Wednesday afternoon and Thursday morning. Then came the 30-year Treasury auction on Thursday 1 pm and watch the immediate vertical fall in TLT & the spike in volume below

Our friends on CNBC Power Lunch didn’t notice the fall because it took place in the bond market. Had it been an equivalent vertical fall of 146 points in the Dow, they would have devoted the entire show to it. The 30-year auction was atrociously weak and a fall in the 30-year bond was rational. But not this kind of a fall. Yes, most of the curve steepeners were liquidated last week (perhaps creating last Friday’s spike in long Treasuries) and that position squaring might have made the 30-year bond technically vulnerable. (We focus on the 30-year because it was the only on-the-run Treasury to close down on Thursday.)

But still, the vertical nature & the volume spike do suggest a change in the macro sentiment. Remember the 30-year T-bond is vulnerable to increased or additional QE and that the up move in 30-year yields really began with Draghi’s promise to whatever needed in August 2012.

And what happened on Thursday morning? Draghi became dovish and the Euro-USD fell. The markets took it seriously and the bounce in the U.S. Dollar vs. Euro demonstrates it. This change in macro sentiment and the surprise of weak demand in the 30-year auction led to the vertical fall, we think.

Look where the 30-10 year spread closed on Thursday:

- J.C.Parets @allstarcharts – Here’s your curve: 30yr T-Bond Yields $TYX minus 10yr Yields $TNX – testing major trendline support http://stks.co/q0Inb

This spread steepened a bit more on Friday but not enough to break the support above, we argue. Chair Yellen has been trying valiantly without success to steepen the 30-5 yr curve ever since her comments in March. And Draghi did it with a mere hint on Thursday morning. Shows who’s the boss, right? And why are markets so focused on QE in Euroland?

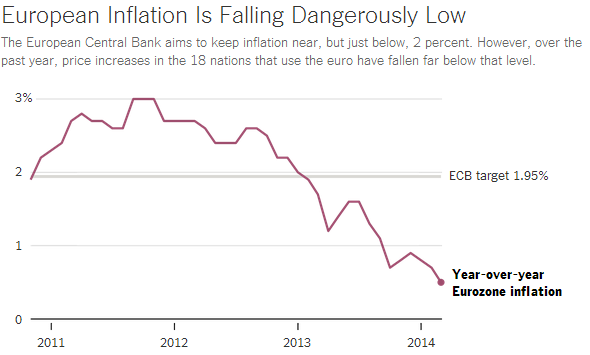

- Justin Wolfers @JustinWolfers – The chart that terrifies everyone except the European Central Bank: www.nytimes.com/2014/05/09/upshot/why-caution-is-risky-for-europes-central-bankers.html?rref=upshot … pic.twitter.com/ZsBwnZXzd4

The European stock markets seemed to take Draghi at his hint of QE, according to the tweet below on Friday afternoon.

- ETF Godfather @ETFGodfather – ECB QE play: huge volume in $DBEU to close the week #ETFs pic.twitter.com/LLfkl2IQmO

Now if the markets really expect a QE from Draghi, then the Euro has to weaken and the Dollar should strengthen, right? That is what J.C. Parets argued on Friday:

- J.C. Parets @allstarcharts – an explosive US Dollar rally here would catch so many people off guard. It would be so awesome $DX_F $UUP a lot of dollar haters out there!

- J.C. Parets @allstarcharts – after hitting 2yr lows, US Dollar Index reversed & went out at highs. Weekly candle also beautiful. Is this beginning of epic squeeze? $DX_F

Is the above a major macro change or is it simply be a head fake driven by a correction in the major trends in the Dollar and the Treasury yield curve? We don’t know but Draghi has served notice, we think.

2. U.S. Bonds

The 30-year yield jumped by 10 bps this week, mainly due to the spike on Thursday and Friday. The 10-year yield went up by about 5 bps while the 5-year & 2-year yields fell by 4 bps. A major steepening indeed. The European sovereign bond markets continue their bull run as in the born-again “yield convergence” type appetites of 1993 with the Spanish 10-year yield breaking below 3% (2.92%). The U.S. Corporate bond market also acts very well. This led to:

- Tuesday morning – Gluskin Sheff @GluskinSheffInc – David Rosenberg: Is that CAT 50-year bond a sign that issuers see that the lows in yield…. are in?

Jeff Gundlach took a more nuanced position on Treasuries at these levels in his comments on CNBC FM 1/2 on Monday:

- “It would seem to me without having too much economic weakness,or without too much difficulty in the world we could probably see the 10-year make it down to 2.50, 2.47, type of zone. It’s getting kind of close. My viewpoint is to get through that level you would need some kind of psychological shift and some sort of macro event to make investors really want a flight to safety. The investment value down in the low 2s is pretty dubious.”

- “so you really need it to be an alternative away from other risky things. so maybe a really hard slowdown in China could cause a change in attitudes and deflationary fears. maybe hotter situation in Ukraine could cause those types of fears. maybe just the GDP that came out at basically nothing in the first quarter”

- “Treasuries are under-owned and there’s a lot of shorts against it in unconstrained bond funds and ETFs. If those shorts get pulled, you could see a real scramble to Treasury rates. And who knows? Maybe we actually take out the unthinkable – the low of 2012,” he said. “I said at the time it was a 90 percent chance that that was the low in bond yields in July 2012. I still think it was, but I think now it’s only a 70 pct chance. I think the chances have gone up that we go lower in yield because of the massive under-positioning in the Treasury market“

Frankly, the worst sentiment news for the Treasury market is bullishness from confirmed stock bulls like say, Ed Yardeni:

- Urban Carmel @ukarlewitz – Yardeni: US Treasury yields of 2.5%-3% must be very attractive given how low rates have fallen in the Eurozone $ZN pic.twitter.com/Zfjejrovxt

3. U.S. Equities

3.1 Divergences

If the Dollar begins a rally, if the yield curve begins to re-steepen perhaps in a corrective/bear mode, what sector of the S&P might face the headwind from these moves? The Consumer sector, we think. And like the short Dollar and Long Treasuries trades, XLP has substantially outperformed the S&P which itself has viciously outperformed the Nasdaq & Russell 2000.

Interestingly enough, Carter Worth of CNBC Options Action argued for a 10% correction in the XLP on Friday after the close. His main point is mean reversion of the “epic period of outperformance” which he explains via persuasive charts in the clip. His supporting argument is that the major components of XLP sport average PE of 21.5 with 0% average earnings growth.

The second divergence is obvious and best explained by below:

- The Street @TheStreet – The Only Chart You Need to Understand the Market Right Now: http://trib.al/eh2YxU1 pic.twitter.com/3QURAZ87QG

The 3rd and perhaps most important divergence is the tremendous under-performance of the Russell 2000 small cap index. It held an important support level this week but barely:

- C J @Marketrend – Russell testing today huge support last 6 months pic.twitter.com/AjbcwjVG1f

3.2 Final Top?

Tom DeMark spoke with Rick Santelli on Thursday and in his typical fashion stated the proximity of a final top of this rally.

- “I think downside. we have modest move upcoming this week and then the market should top finally. finally. … what’s happening, each market is topping out individually; you got the march peak in the Russell and the Nasdaq — excuse me — and now we’ve got the upcoming peak in the S&P and the New York Stock Exchange composite. the Dow Jones Average effectively made the high as I predicted on the air with you on December 31st. We’re coming up for a secondary move on that high, and all we need is 16,660 possibly within the next couple of days, and that should top that market out, finally.”

DeMark is well known for his trend exhaustion indicators. Unfortunately for him, this Fed-QE driven market has been like the Energizer bunny. This is one reason why indicators like DeMark’s failed in 2013. Given the steady and determined taper by Chair Yellen and the high probability of the end of QE in 2013, his exhaustion indicators stand a higher chance of being proven correct. And we won’t have to wait long. DeMark, in his usual fashion, says the stock market should top in the next couple of days, meaning next week. At least, that is what we think he said to Rick Santelli because DeMark’s prediction seems conditional on hitting 16,600 – at least that’s how he put it.

A supportive view came from the tweet below:.

- Minyanville @Minyanville Jason Haver: S&P, BKX, USB – A Terminal Pattern in Equities?http://www.minyanville.com/

business-news/ markets/articles/Jason-Haver253A- … @PretzelLogic pic.twitter.com/DfB6t8FbmWS2526P-500-BKX-USB/5/6/2014/ id/54830

But then we have a more conditional tweet from the same source:

- Minyanville @Minyanville – The S&P 500 is Either Forming a Topping Pattern or a Large Basing Pattern http://www.minyanville.com/

special-featur es/from-the-buzz-banter/articles/The- … pic.twitter.com/mcJrpidmthS2526P-500-Is-Either-Forming/ 5/9/2014/id/54921

A similar view came from:

- Robert Kelly @robertknyc – The S&P has either just completed a bullish triangle that yields a last hurrah on the upside, or top is already in. 1891 and 1860 are key.

3.3 Directional.

Marc Faber is nothing of not decisive and emphatic. He was both on CNBC Squawk Box on Thursday morning:

- “now I believe the next test will be stocks and bonds will go down at the same time. the most under-appreciated asset is cash. nobody likes cash. cash for the next 10 years you earn precisely zero. in fact you will lose money because Ms. Yellen is a money printer like all the others. and she will make sure that the dollar continues to depreciate in real terms. for the next six months cash is the most attractive. I’m saying for the next six months opportunities will come along for a long time“

Remember the key BlackRock statement from their 2014 outlook was that stocks and bonds will be much more correlated in 2014. Marc Faber’s prediction seems to echo that.

Jay Jordan of the Jordan Companies told CNBC Squawk Box that he had sold his stocks a few months ago. He added:

- “the marks are so robust,in the technical sector, even in the private sector we deal in, liquidity globally. it’s a little scary to me. I tend to be a bit of a bear right now, because thing are going too well. you’ at the banking sector if financing the private equity firms are doing the same thing they did in the mid-2000s. this lite loans, PIK-toggles, we’re starting to see that again. I’m thinking, don’t these folks ever learn? you can make an argument for a bubble building in the markets again, it won’t be as difficult the markets are not as leveraged.”

Could we find a bull? The closest was the tweet below:

- Minyanville @Minyanville Todd Harrison: Keep in Mind the Bull Case for the S&P 500 http://www.minyanville.com/

special-featur es/from-the-buzz-banter/articles/Todd- … pic.twitter.com/U1BcMyS6cxHarrison253A-Keep-in-Mind-the/ 5/7/2014/id/54886

Featured Videoclips:.

1. David Einhorn with Erik Schatzker and Stephanie Ruhle on BTV Market Makers – Monday, May 5

Such detailed interviews are what BTV does best and Erik Schatzker & Stephanie Ruhle are probably the best pair for such interviews. The following is a subset of the excellent transcript provided by BTV PR.

Key Point:

- On a March 26 dinner conversation with Bernanke, Einhorn said: “I got to ask him all these questions that had been on my mind for a very long period of time, right? And then on the other side, it was like sort of frightening because the answers weren’t any better than I thought that they might be. I asked several things. He started out by explaining that he was 100 percent sure that there’s not going to be hyper inflation. And not that I think that there’s going to be hyper inflation, but it’s like how do you get to 100 percent certainty of anything?“

Einhorn said he was keeping an “open mind” about new Fed Chair Janet Yellen. “I would love to see if she had a better reason for rates to remain at zero at this stage of the economy.”

Summary of the clip:

ERIK SCHATZKER: Valuations out of control. David, you wrote in your letter to investors for the first quarter that you see some of these stocks dropping by 90 percent. So good businesses

SCHATZKER: So what’s in — you’ve taken a different approach than perhaps the conventional route, which would be pinpointing, identifying overvalued single-name stocks and shorting them and instead gone for a basket approach. What’s in the basket?

EINHORN: Well, a whole number of stocks. Probably many of the ones on your list. We identified one yesterday as an example. I don’t really want to get into all the different ones that are in the basket, but I think it’s — I think people can more or less sort these things out. Certainly we’re not saying like Apple is a short or Micron is a short. We’re long those things.

SCHATZKER: But is Twitter a short, for example? Twitter’s a company that people, as you know, have raised many valuation concerns about and it shows up on my list.

EINHORN: Yeah. Well here’s the thing. Like when we put out this letter, half the people were very upset that they thought we were talking our book. And the other half of the people were upset that we weren’t telling them all the names. So you really couldn’t please anybody. So I thought I’d bridge this yesterday by giving out one, by giving out one.

EINHORN: I think adding information to the market so that people can sort these things out, I think it’s constructive and that’s why we tend to sometimes share our thinking.

RUHLE: You want to talk about Athena?

EINHORN: Sure.

EINHORN: Sure. Look, I think Athena is — is a very good example of this. This is a good business with a good strategy and a good product and a good management that’s doing good things for the world, but it stock is just at the wrong price and it’s really as simple as that. And what happened was is a few weeks ago Morgan Stanley came out with this conventional DCF valuation where they projected out the results until 2030 and we just looked at that and said, wow, how are you going to get from a 10 percent margin before stock comp to a 30 percent margin? And we thought about the business, and we just don’t think that the assumptions that they’re using there are plausible.

RUHLE: Well you say — or you said in your presentation they weren’t a cloud company. What exactly would constitute a cloud company then?

EINHORN: Well the way I look at it is there’s two types of — of these Internet companies. There’s ones that have sort of a network effect and there’s others that don’t really have network effects. A network effect to me means that having more users on the network makes the site more valuable to each user. So eBay is a great example of this. Everybody likes auctions and — and knows if you want to auction something off you go to eBay because that’s where the buyers are going to be and the buyers know where

But there’s other types of Internet companies where your relationship is very much with the provider. So having lots of customers, it might help the provider be a little more efficient. It might help them run their business better, but it doesn’t really present them with a competitive position that allows them to earn like huge excess profits over a long period of time. And I think Athena sort of falls more into that latter category.

SCHATZKER: David, if I understand it correctly, you have raised the concern that Athena may not be able to compete with other large vendors like Epic (ph), for example.

EINHORN: Yes.

SCHATZKER: Now —

EINHORN: And the bull case really requires them to make a huge inroads into the hospital market.

SCHATZKER: Okay. So I can understand how investors may have duped themselves into believing that Athena Health can do that, but what about customers? Ascension Health is become a client of Athena

EINHORN: No, no, no. Athena has a good product and — and they have customers and they have real customers, and I wouldn’t tell Ascension or anybody else not to use their product. I think it’s a fine product. I think the market opportunity is maybe smaller than people think because they’re already up to 37,000 doctors, which is a lot, and they concentrate in these — in the ambulatory business, so not in the hospitals.

So a large amount of the doctor population is away from them. And if hospitals buy up doctor practices, the available pool shrinks. Plus there’s been a huge move towards electronic health records. The stimulus provided huge incentives for doctors to take these systems on and a lot of them have done that. And Athena has captured part of that, but there’s been now a huge penetration of electronic health records and in the next year or two we think they’re going to run into a saturation and their growth is going to slow down.

EINHORN: That’s correct.

SCHATZKER: When does the market wake up and revalue these overvalued stocks?

EINHORN: Well I don’t know. Perhaps it already has. It’s possible that the top was in — a few weeks ago.

SCHATZKER: So the biotech sell-off, for example —

EINHORN: The stocks have come in a lot. Now we won’t know. In a year it will be very clear was that the top, was that not the top, did they rally back. Certainly they’re going to have sharp rallies even if they are going to continue to go down, and we’ll know in hindsight whether this was the top or whether this was a correction and so forth. Our strategy is to have relatively small positions in a large number of these things and let time be on our side.

You were at the Ira Sohn conference yesterday presenting one of your best investing ideas, shorting Athena Health. And Paul Tudor Jones, another hedge fund manager, was at Ira Sohn yesterday and he said this. “What we desperately need is a macro doctor to prescribe central bank Viagra because otherwise it’s going to continue to be somewhat dull.” Now Paul may share your concerns about quantitative easing, but quantitative easing has been awfully good for people who are long the stock market at the very least. Do you share that view?

RUHLE: All right. Well you recently had dinner with Ben Bernanke. What went down? We didn’t get to be there.

EINHORN: I was — I’ve been critical. I’ve been critical of him for a very long time. And the dinner for me, in one way it was cathartic because I got to ask him all these questions that — that had been on my mind for a very long period of time, right? And then on the other side, it was like sort of frightening because the answers weren’t any better than I — than I thought that they might be.

SCHATZKER: What did you ask him?

EINHORN: I asked several things. He started out by explaining that he was 100 percent sure that there’s not going to be hyper inflation. And not that I think that there’s going to be hyper inflation, but it’s like how do you get to 100 percent certainty of anything? Like why can’t you be 99 percent certain and like how do you manage that risk in the last 1 percent? And he says, well, hyper inflations generally occur after wars and we didn’t have — that’s not here. And we — we — there’s no sign of inflation now and Japan’s done a lot more quantitative easing than we’ve done, and they don’t have it. So — and if there is a big inflation, the Fed will know what to do. That was kind of the answer. And —

RUHLE: What did you say?

EINHORN: That was it. Then it went to the next question. So then a few minutes later it came back and I got to ask him about the jelly donuts. And my thesis is that it’s like too much of a good thing. Like lowering rates and quantitative easing and these stimulative things, they help but with a diminishing return. And eventually you go too far and it’s like eating the 35th jelly donut. It just doesn’t help you. It actually slows you down and makes you — makes you feel bad. And my feeling has been that by having rates at zero for a very, very long time the harm that we’re doing to savers outweighs the benefits that might be seen elsewhere in the economy. So I got to ask him about this.

SCHATZKER: Okay, and what did he say?

EINHORN: Well he said — he said — first of all he says, you’re wrong. That was good. And then he said the reason is if you raise interest rates for savers, somebody has to pay that interest. So you don’t create any value in the economy because for every saver there has to be a borrower.

And what I came back to him was I said, but wait a minute. You said for a long time we haven’t had enough fiscal stimulus, and who’s on the other side of the low interest trade? It’s the government. And so if the government — if we raise the rates, the government would have to pay more money to savers. You’d have the bigger deficits. You’d create the stimulus, the fiscal stimulus that you’ve been complaining that Congress wouldn’t give to you, right? And savers would benefit from the higher rates and because savings is spent at a very high rate in terms of interest — interest income on savings is spent at a high percentage, you’d get a real flow through into the economy.

SCHATZKER: One of the questions you’ve raised about quantitative easing in one of your letters to investors was about inequality. Did you get any satisfaction from Ben Bernanke on the question of whether quantitative easing exacerbates inequality?

EINHORN: Yeah. He — he sort of — that did come up and I don’t remember exactly what he said. So I don’t want to —

SCHATZKER: It wasn’t memorable.

EINHORN: No.

SCHATZKER: How about this notion that Warren Buffett has propagated that the Fed has become with its $4 trillion balance sheet the greatest hedge fund in history?

EINHORN: Yeah. I’m not sure that’s meant as a compliment.

SCHATZKER: But did that issue come up? There were a number of people (inaudible).

EINHORN: Yeah. There were people — there were people who were asking, yes, and he says — he says the Fed can manage their way out of it when the time comes.

SCHATZKER: But in a persuasive way? Did he — did he convince anyone?

RUHLE: Or did he say Janet’s problem now, not mine? I’ll have another drink.

EINHORN: He was — he was very supportive of Janet.

SCHATZKER: No doubt.

RUHLE: Are you?

EINHORN: I want to keep an open mind here. I saw her speak at the Economics Club a couple weeks ago and I was impressed by her speech. I thought — she said, look, we have a base expectation, but things change. And when things change, we’re going to change our policy. I thought that was good. She’s — I don’t look at one economic factor to drive things. I’m going to look at all of the factors. I thought that was good. I think the way she’s approaching problems at least conceptually is very good. I’d love to see if she has a better reason why rates should remain at zero at this stage in the economy, but you take these things and see where she goes. She’s just gotten started.

SCHATZKER: Do you feel — no, that’s fine. Do you feel any more confident about the Fed’s ability to manage that $4 trillion balance sheet than you felt before? You worry, for example, that if we run into greater economic — if not greater — if we run into economic headwinds at some point in the next few years and the Fed still has trillions of dollars, it’s not going to be able to (inaudible).

Send your feedback to [email protected] Or @MacroViewpoints on Twitter