Summary – A top-down review of interesting calls and comments made last week about monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

1. “he has never disappointed”

We recall the words of Paul Richards of UBS on Wednesday, June 4:

- “the one thing about Draghi, everyone expects disappointment from him. he’s never disappointed. … he going to go for it..he is going to give you 15 bps cut, that is priced in; he is going to start talking about an LTRO may be announce it and then I think he is going to mention QE in his press conference. …

- this is the guy who saved the euro at 1.2450; at 1.3950 he said it is too high, now it is at 1.36; he made two big statements on the Euro – at 1.2450 % 1.3950; the mean is 1.31-1.32 – that’s his target”

You listened to Richards on June 4, you made money on Thursday, June 5. So what did Richards say about Draghi on Friday on CNBC FM 1/2?

- “What Draghi did was historic – next step full QE if this doesn’t work – Draghi is saying he is

all in – very positive for growth & assets” - “Draghi lowered rates because he wanted a lower euro – Euro going to 110-115 ; definitely going lower”

There is no question that Draghi is the man who drives risk assets in the world. It was he who jump started this rally in August 2012 with his verbal promise. And now he has begun doing with a promise to do whatever it takes.

Some produced numbers that were skeptical of how much he could do, like Deutsche Bank:

- “Mario Draghi refused to put a number to the ECB’s new asset purchase programme. Let’s try for him. Of the €1tn outstanding ABS about a third is not acceptable collateral. Next consider that in order to revive the market buying everything eligible is not an option either. As a cross check the Federal Reserve owns a third of the agency MBS market in America. By that benchmark the ECB’s potential pool is closer to €200bn plus a share of any new issuance. How does that number translate into new lending? Certainly being mostly restricted to senior tranches does not free up much bank capital. And €200bn of additional liquidity only makes up for LTRO repayments year to date. What is more half of all eligible securities already sit with the ECB as repos hence the incremental liquidity is smaller still.”

They may be right but they miss the point, the point that David Tepper made to BTV’s Stephanie Ruhle:

- “What the ECB did today is very important- they want growth & increase in money supply and inflation. … Draghi wants inflation in the Euro zone. He will not stop.”

Getting inflation & growth in the Eurozone might be a tall order. But that is in the future. The markets believe in Draghi and that is all that counts until they change their minds.

2. “Sends Yellen back up to the watchtower“.

That’s how Art Cashin described the effect of the much weaker than expected NFP number of 142,000. The consensus had factored in a hawkish statement from Chair Yellen on September 17. Now that is in serious doubt.

- Kathy Lien @kathylienfx – My NFP Take – Fed will still end QE in Oct but expect Yellen to provide ZERO insight on timing of rate rises at this month’s FOMC meeting

A little later came Art Cashin with his “whatever it does, sends Yellen back up to the watchtower” comment. Paul Richards was more emphatic on CNBC FM 1/2:

- “trend closer to 200K than 300K; plays to what Yellen has been saying; no hike in rates till

August 2015“;

Just as on August 1, the markets were ready for a strong number and got a weak number. And the initial action was similar on Friday. TLT jumped a full point in the immediate aftermath of the NFP number and the 10-year yield fell below 2.4%. The rally prompted:

- Jon Najarian @optionmonster – 2.22 right around the corner folks @CNBCFastMoney

But the picture looked different a bit later, especially in the 30-year:

- Peter Tchir @TFMkts – The long bond is trading very “long” – it should be up more than it is on the data – look for fade in price/higher yields.

He called it. The rally in Treasuries began fading after the stock market opened and then faded all afternoon. The 30-10 yr curve closed negative in price & up in yield on the day. Peter Tchir took a victory lap in the afternoon:

- Peter Tchir @TFMkts – @SRuhle market traded very heavy from a minute after the number 🙂seemed an easy fade 3.30 long bond soon

Compare this to August 1 when the 10-yr closed down 6 bps & the 5-year down 9.6 bps. And this Friday’s number was much weaker vs. expectations than the August 1 number. The key, quite possibly, is the positioning. Interestingly, the day before, Tom McClellan had flagged the peak in open interest in T-bond futures as “the highest quarterly peak since early 2008“. The other key might be the double bottom discussed by Rick Santelli on Thursday. In the clip below, Rick pointed to the 2.34% level hit on August 29 & on August 15. On both occasions, the 10-year yield backed up the next day thus creating a basic double bottom in yields.

The 10-year yield closed just above 2.45% on Friday, a key level according to Rick Santelli with a 3- bps noise interval. So what happens next week might be critical.

The fade in Treasuries could also be due to David Tepper’s call on Thursday:

- “Basically what it means for the markets is higher equity prices & the beginning of the end of the world bond market bubble. It’s the beginning of the end of the bond market rally. We are done.”

What we do know is that QE has always led to steepening of the treasury curve and under performance by the 30-year. And that is what happened on post-Draghi Thursday and on Friday, despite a weak jobs number. Goes to show who rules the long end – Draghi & the market’s belief in him.

The weak payroll number revived the “will the real economy stand up” debate about the divergence between the strength in PMI numbers and NFP numbers. An interesting view was offered by Jim Bianco on Friday in his conversation with Rick Santelli:

- “Purchasing Managers report has been unambiguously strong for years. I think it’s because we’ve lost a lot of the weak purchasing managers,” he said. “They’ve left the survey force and it’s unambiguously strong. It says the economy is great and it never seems to play out, and it’s been going on for years right now”

A nearly identical comment was made by JPM’s Andrew Mowat who called EM indices “Darwinian“. Mowat explained that EM indices routinely throw out the weak sectors and replace them by strong sectors. For example. the resource sector is now only 4% of the Brazil index.

3. U.S. Equities

You cannot but give the pole position for equities to David Tepper. No one has been more committed bullish about the impact of QE than him. And characteristically, he said it simply to BTV’s Stephanie Ruhle:

- “Basically what it means for the markets is higher equity prices & the beginning of the end of the world bond market bubble. It’s the beginning of the end of the bond market rally. We are done.

Stephanie,listen again to my statement – this is how I strongly feel about the markets after listening to Mario Draghi. And if you read into what I said, clearly that is how I am positioned.”

Thomas Fitzgerald of CitiFX was mucho bullish with a 2150-2400 target for the S&P on CNBC FM:

- “August was a bullish outside month at the close last Friday. That has only happened on 3 other occasions since 2009 – July 2009, 2011 & February this year 2014. In all three instances, after that bullish outside month, we had an up move in 4 of 5 months – smallest up move we had was 15% & avg up move was 29%;”

- “the 15% level would suggest we could be pushing up to at least 2150-2200;closer to 29% would suggest 2400 & above“

- “longer term chart from 2009 – last time we had a move of this magnitude is really looking back to the up move in 1995-2000; in that up move, we had 3 bullish outside months & they averaged 24% to the topside, so between two periods 7 bullish outside months averaging 26%; the last bullish outside month in Oct 1999, giving us a 26% move; looking at both moves, it comes to 2400 by year end but at least 2200;”

Adam Parker of Morgan Stanley came in with a 3,000 target for the S&P by 2020:

- “U.S. expansion, now in its fifth year, could continue for another five years, hitting his 2020 target of 3,000 for the S&P 500 … small-cap margins today in the U.S. are only at their long-term average. So, in a slowly improving economy, that means a lot of companies that continue to improve“

Long term bull Tony Dwyer has been wrong so far in his prediction of a correction. But as Q4 approaches, he is clear on what to do if market suffers a correction:

- “If the market gods give you a gift of weakness, with the fundamental and tactical backdrop that we have, I think you want to be adding to your core position in equities … Indeed, after a September drop, the markets tend to close the year higher—rising 75 percent of the time in the fourth quarter, for an average gain of 2 percent“

Could this gift of weakness come from sheer tiredness? Lawrence McMillan writes in his Friday summary:

- “The not-so-bullish news is that $SPX has failed to close at a new all-time on any of those days. This is the action of a tired market.”

- “Market breadth has been weakening of late. In fact, both breadth indicators are on the verge of sell signals at this time. Any further negative breadth will generate sell signals.”

- “In summary, the indicators are becoming more mixed. But if $SPX breaks down and $VIX breaks out, the situation will quickly change to bearish.”

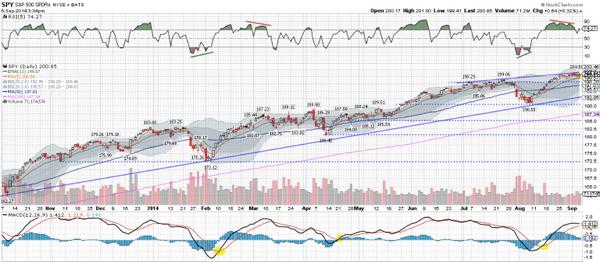

The market has not paid any heed to charts like the ones below. But this is September and, who knows, it might this time.

- Urban Carmel @ukarlewitz – Heading into next week, SPY jammed up against a 2-mo T/L. In past, hard to pop significantly higher before RSI drops pic.twitter.com/OLyGsRIt1

- TheNorthman @NorthmanTrader – @NicTrades @ciscovive The Rydex bull/bear ratio is at lows not seen since 2000 pic.twitter.com/eFQ6WfKHwt

- John Kicklighter @JohnKicklighter – The divergence between $SPX and my Risk-Reward Index (agg 10yr yield / FX VIX) broadening: http://stks.co/i11hz

Only one was willing to talk about a long term top:

- Robert Kelley @robertknyc – Here is my long-term count on the S&P. A decline to 1700 is plausible; alternate count says major top forming now. pic.twitter.com/wjxx1Gs2Jr

4. Commodities

Commodities were shot this week, possibly because the 1% rise in the US Dollar and a steep fall in the Euro. USO, the WTI ETF, was down 2.5% and UNG, the natural gas ETF, was down 7%. Gold Miners, GDX & GDXJ, were down 6% & 7% resp.

5. Top in Credit & Opportunity in Distressed Debt

We have always liked to follow what “smart money” is doing. And this week, we saw what OakTree is doing – “preparing for the economy to falter“. What is OakTree doing? Bloomberg reports:

- “The world’s biggest distressed-debt investor is seeking $10 billion for a new fund with plans to sit on most of the capital until rising markets reverse course,”

Why raise the money now?

- “Credit standards have dropped and non-investment grade debt issuances reached record levels,” John Frank, Oaktree’s managing principal, said July 31 on a conference call with investors and analysts. “Aggressive extensions of credit of the sort we’re seeing today have always been a precursor to a substantial distressed-debt opportunity.”

6. What is the origin of the word “algorithm”?

Two weeks ago, we wrote about how Hemchandra, an Indian Mathematician in the 11th century, had discovered what are now called “Fibonacci numbers”. This was at least one century before Fibonacci. As we discovered recently, Fibonacci did not even discover these numbers himself. And that discovery is linked to the word “algorithm”.

The word “algorithm” comes from “algorithmus”: the Latinised name of al Khwarizmi of the 9th century House of Wisdom in Baghdad. He wrote an expository book on Indian arithmetic called Hisab al Hind. Gerbert d’Aurillac (later Pope Sylvester II), the leading European mathematician of the 10th century, imported these arithmetic techniques from the Umayyad Khilafat of Córdoba.

Later, Florentine merchants realised that efficient Indian arithmetic algorithms conferred a competitive advantage in commerce. Fibonacci, who traded across Islamic Africa, translated al Khwarizmi’s work, as did many others, which is why they came to be known as algorithms. Eventually, after 600 years, Indian algorithms displaced the European abacus and were introduced in the Jesuit syllabus as “practical mathematics” circa 1570 by Christoph Clavius.

These algorithms are found in many early Indian texts, such as the Patiganita of Sridhar (870-930 CE) or the Ganita Sara Sangraha of Mahaaveer (9th century), or the Lilavati of Bhaaskar II.

Send your feedback to [email protected] Or @MacroViewpoints on Twitter