Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. “Interest rates dropped like a rock”

said Rick Santelli about the immediate fall in yields after a decent payrolls number on Friday morning. The 10-year yield dropped from 2.39% just before the number to 2.34% almost instantly and closed on the lows of the day at 2.30%. Was Santelli exaggerating? Not according to the chart below from Forexlive.com:

Why such a move after a 214,000 number? First the expectations were for a higher number with one whisper number as high as 300,000.

Secondly, the positioning. As GaveKal wrote on Tuesday, November 4:

- “Meanwhile, speculators are still carrying a hefty short position in 10-year treasury futures and options contracts, implying that yields have further to fall yet. Speculators are currently short about 160,000 contracts. Over the last several years, significant lows in yields have not been achieved until speculators became net long about 100,000 contracts, implying a 260,000 long contract delta that would need to be filled to achieve a low in yields (1st chart below). Simply put, if history is a guide we are going to have to observe a massive change in positioning before yields make a low.”

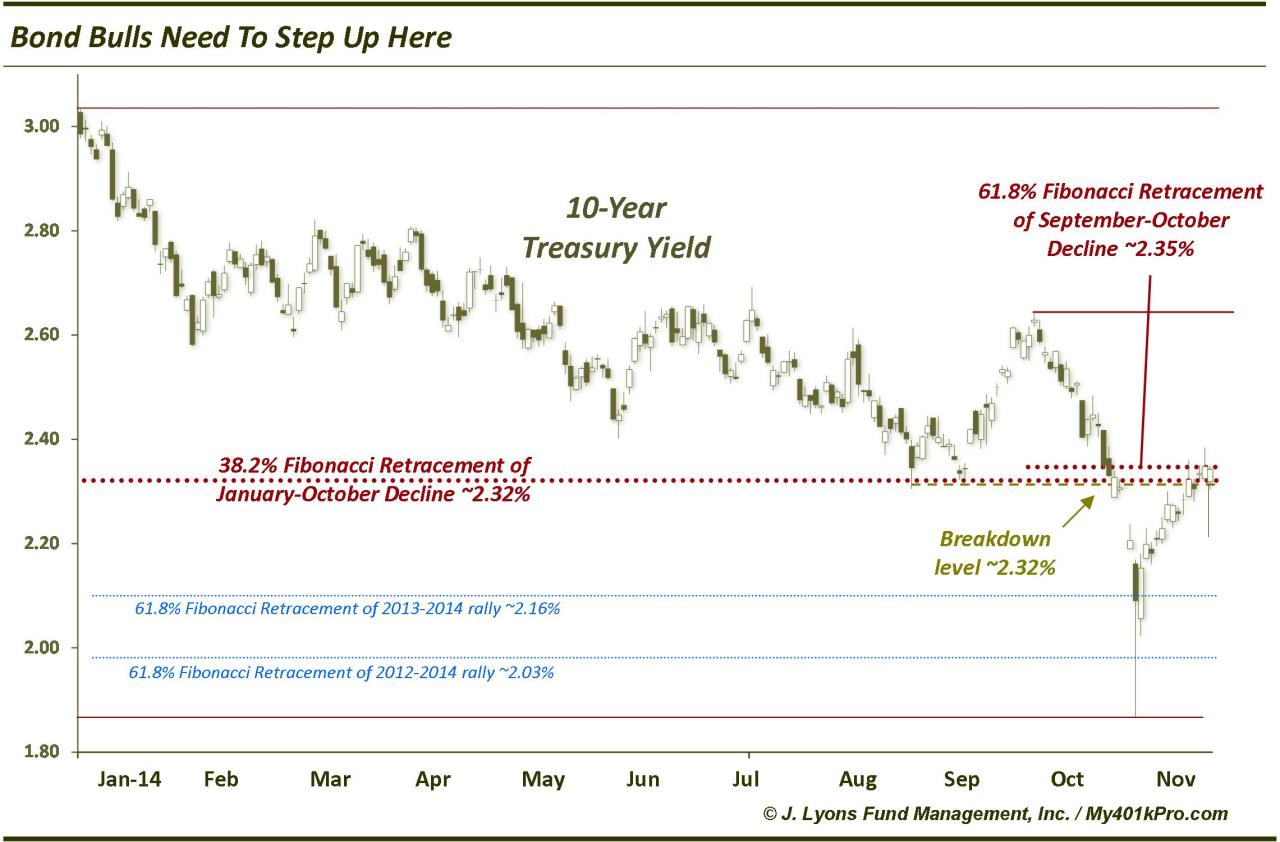

And Treasuries were oversold. With the Fed slightly hawkish and with Kuroda’s howitzer on October 31, treasury yields closed on Thursday at an important technical juncture as Dana Lyons noted on Wednesday, November 5 in the chart in his article Bond Bulls Need To Step Up Now:

So you had it all on Friday at 8:25 am – fundamental opportunity, positioning ripe for an unwind, & oversold condition sitting at a key Hemachandra-Fibonacci retracement level. Buying TLT just before the release of the NFP number would have given you at 1.2% gain by the end of the day.

The Treasury curve bull-steepened a bit on Friday with the 2-5 year yields dropping 4-7 bps on the day. The Yellen Fed is focused on inflation and there is no sign of that. Perhaps you need lots of new jobs with higher incomes to create fear of inflation. From that perspective, Friday’s NFP number failed because:

- Northy @NorthmanTrader – RT @m_cof Majority of new jobs created in October pay below average hourly wage of $24.57 http://on.mktw.net/1EbFLkg

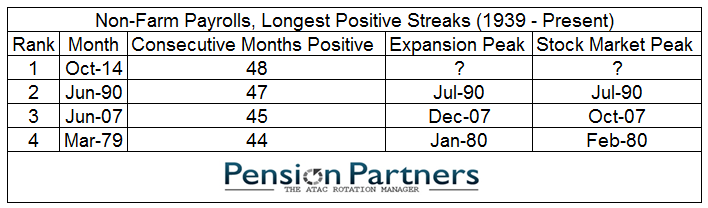

The only question we have these days is when we will see a 300K+ jobs number. At least we take it for granted that we will see a positive payroll number. That’s why we were jolted by the tweet below:

- Friday – Charlie Bilello, CMT @MktOutperform – The only other consecutive streaks above 40 months for non-farm payrolls ended in June ’90, June ’07, and March ’79.

2. “so pumped”

were the words J.C. Parets used about himself about the action in commodities. He added late Friday:

- J.C. Parets @allstarcharts – watch these energy commodities next week. I think we’re going to see some fireworks…..you heard it here first!

Which energy commodities? Larry McDonald specified to Bill Griffeth on CNBC Closing Bell on Friday:

- “in the entire enery space, Bill, the best buy is Coal – the Coal names have made 10-16% bounce in KOL, BTU over the last 2 weeks; I think that is a catalyst for the next couple of months; thats really a cheap space; I think they run for the next 6 months; I think the Republicans will undo a lot of the damage the EPA has created for the coal space.” . .

Not only was McDonald recommending Coal stocks for some time, he recommended buying Uranium ETF, URA, Friday morning before the opening bell in his proprietary Bear Traps newsletter. It opened at $11.66 & closed at $13.09, a 13.33% move in one day.

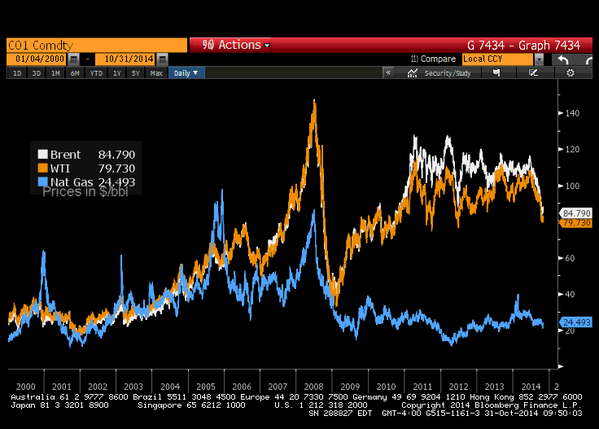

The week before, BTV’s Erik Schatzker had tweeted with the graph below:

- Friday 10/31 – Erik Schatzker @ErikSchatzker – What if oil went back to trading in step with natural gas? Uh, that’d be $25 a barrel.

Coincidentally or predictably, natural gas rallied every day this week with a two week rally of 19% in UNG.

Oil joined the natural gas rally on Friday. But that rally was muted compared to the bigger move in energy ETFs, XLE & OIH. Oil has so underperformed XLE & OIH in the past several weeks that Carter Worth of CNBC Options Action called it “as wide as it has ever been” and suggested buying USO, the WTI ETF.

As a technician, Carter Worth is a semi-doer but Harold Hamm of Continental Resources is a pure doer. And he acted as a doer on Thursday by calling a bottom in oil prices and “scrapping all of the North Dakota energy producer’s oil hedges, betting that prices will recover soon after sinking 25 percent in recent months“, according to Kate Kelly of CNBC. It would be an understatement to call this a gutsy move.

3. Gold Miners, Gold & Silver

Gold Miners, Gold & Silver rallied viciously on Thursday & Friday. GDX & GDXJ rallied by 12% & 15% from Wednesday’s close to Friday’s close while GLD & SLV rallied by 3%. Thursday’s rally merely got back Wednesday’s vicious mauling. But Friday’s rally seemed real. From the pre-market levels at 08:25 am, GLD, GDX, GDXJ & SLV rallied by 2.7%, 8.4%, 11% and 2.2% by Friday’s close. And the rally was with volume:

- Friday – Chart Freak @chart_freak – HUGE volume in $GDXJ & $GDX for the 1st half hr. we used to get that in an entire day.

Some in the Twitter-sphere kinda called this rally:

- Dale Brethauer – in $GDX Trading Gold on Wednesday – I think we are going to have a call opportunity in the Gold Miner ETF coming up shortly;its something to watch

- Thursday – FxMacro @fxmacro – GDX looks like it has bottomed ECB one step closer to QE think buying GOLD is worth a shot here

- Thursday – “as I measure the equity markets’ internal energy, it has been totally used up in this upside dash from the October 15th lows. … I think the odds favor a near-term trading top between now and Friday. Consequently, those of you with the fortitude to buy trading positions near the mid-October “lows,” I would advise selling them, or at least pressing up stop-loss orders.”

- Friday – “I continue to believe there is compromise in the air, but we will have to see how that plays out between now and year-end. If my view prevails, it would be pretty bullish for the equity markets. But, in the near term, I think we are making a short-term trading top.”

- Friday – Peter Ghostine @PeterGhostine – SPY is suggesting a nearby tradable top. $SPX ~2040. http://www.61point8.com/Portals/0/article% 20images/20141107/20141107SPY1.png …

{kind=link}

Though Dow and S&P rallied this week, the Nasdaq, NDX & Russell did nothing leading to:

- Friday – Northy @NorthmanTrader – So these new highs have been a narrow gap affair not a broad based rally of conviction

Then you have the sentiment:

- Friday – Charlie Bilello, CMT @MktOutperform – AAII Sentiment Poll: 70% bearish in March 2009, 15% bearish today. Sell low, buy high, again and again

Tom McClellan suggested similar caution in his article More from Investors Intelligence Data:

- the rapid drop in this category (“correction” in Investors Intelligence data) since the Ebola scare bottom in October 2014 perhaps suggests that traders and analysts have given up their worry a little bit too quickly. That is not healthy for an uptrend, and so it indicates that a pause in the new uptrend is necessary, just to help store up some more worry as fuel for the uptrend to consume later.

On the other hand,

- Friday – StockTwits @StockTwits This chart shows why it’s so hard to short the stock market right now -> http://stks.co/e1EGg $SPX $AAPL

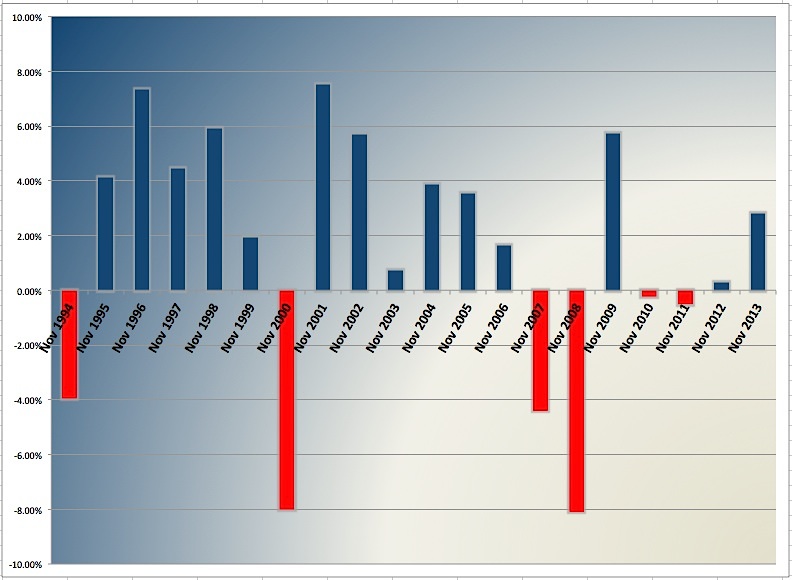

The direction matters more this month because as Andrew Nyquist points out in his article:

- “there isn’t much room for neutrality with the November stock market. It’s either really bullish or really bearish. Let’s run through some recent numbers, then look at some charts. Note that the S&P 500 was used for this study, and it spans the past 20 years.”

Send your feedback to [email protected] Or @MacroViewpoints on Twitter