Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

1. “Who’s your Commodities Daddy?”

This singularly unoriginal title is courtesy of the new Red Robin slogan “who’s your burger daddy?“. We won’t accept Red Robin as our “burger daddy”, but no one can doubt that China is the daddy of commodities. Not after Friday’s rally in Commodities after China lowered interest rates Friday early morning. EEM, EWZ, EZA, CLF, FCX rallied 3%, 7%, 4%, 13%, 3% on Friday, a huge outperformance over S&P 500 which was up only 1/2%. Wilbur Ross described this move as a “very good and very useful move” because “it is an early stage of quantitative easing“. Tim Seymour of CNBC FM called it “definitely a FX war” between China & Japan, a stronger point than his tweet on Friday morning:

- Tim Seymour @timseymour – If U believe #China rate cut is beginning of policy easing cycle(I do) #EmergingMarkets eq’s head into best seasonal period w/wind!

Forexlive.com seemed to concur with Seymour in their post “almost everyone is missing the point with the Chinese rate cut”:

- “China is opaque so there are no easy answers but Xinhua has just published a commentary saying the rate cut is not a signal about a big liquidity ease, so that might be a small tell. … That could be some double-speak to keep a lid on lending excesses but the market is reading it as a signal that no more easing is coming.”

As Seymour’s FM colleague Brian Kelly said, things must really be bad in China for them to take this drastic step. On the other hand, it could be a pre-emptive step against Japan’s deliberate crash of the Yen. The Yen-Yuan ratio used to be critical in the days when China was content to be an exporting nation. Now China is supposedly trying to focus on consumption. Friday’s easing suggests that the restructuring of the Chinese economy is not going smoothly. So the big question remains whether Friday’s easing is merely the first step to further easing. That answer or the market’s perception of that answer will determine how far the commodity rally runs.

The entire commodity & commodity-nations rally has been due to the Chinese credit bubble as the chart below from EconMatters demonstrates:

- “By the time the Fed (yellow line) and the Bank of England (red line) made their moves in 2008 to bail out toppling megabanks, other financial institutions, and the largest investors in the world, the balance sheet of the PBOC had nearly quadrupled.”

- “Its a little odd that investors have reacted so positively to Mario Draghi’s statements because I would argue he has absolutely no credibility; two years ago, two & half years ago, he said the ECB would do anything possible to fight deflation in Europe; and then the ECB promptly cut their balance sheet almost in half; So I don’t think you need a Ph D in economics to know when deflationary forces are mounting around the world & credit in your region is contracting, you don’t shrink your balance sheet; & now he is saying they are going to expand their balance sheet;that probably good given that in the last several weeks, they have actually contracted their balance sheet; So I am a little bit confused, I don’t think Mr. Draghi has any credibility & why anybody would believe him is beyond me.”

Bernstein said on this CNBC Squawk Box. Had he said that on CNBC StreetSigns, Drury-Sullivan duo might have educated him about “hopium”, their favorite word. You see, Mr. Bernstein, markets will believe what is convenient for them to believe. And what is convenient right now is bullishness on stocks & risk assets for a run into year-end. So everyone is waiting for Draghi to say something more concrete & ideally do something in the first week of December. Because no one wants to have to sell before year-end.

What does Draghi want above all? 2% Inflation. And how does that look now to ThomsonReuters?

So what can Draghi do? What the BoJ did as WSJ argued on Friday:

- “To some extent, the ECB is competing with the BOJ. A weaker yen poses problems for Germany, where growth is already very sluggish, given Japanese competition for exports. It is also acting as a brake on the euro’s descent. While the yen accounts for only 7.5% of the trade- weighted index, its decline means that bigger falls are required against other currencies such as the dollar and sterling to weaken the euro.”

This does create fodder for some:

- Friday – Charlie Bilello, CMT @MktOutperform

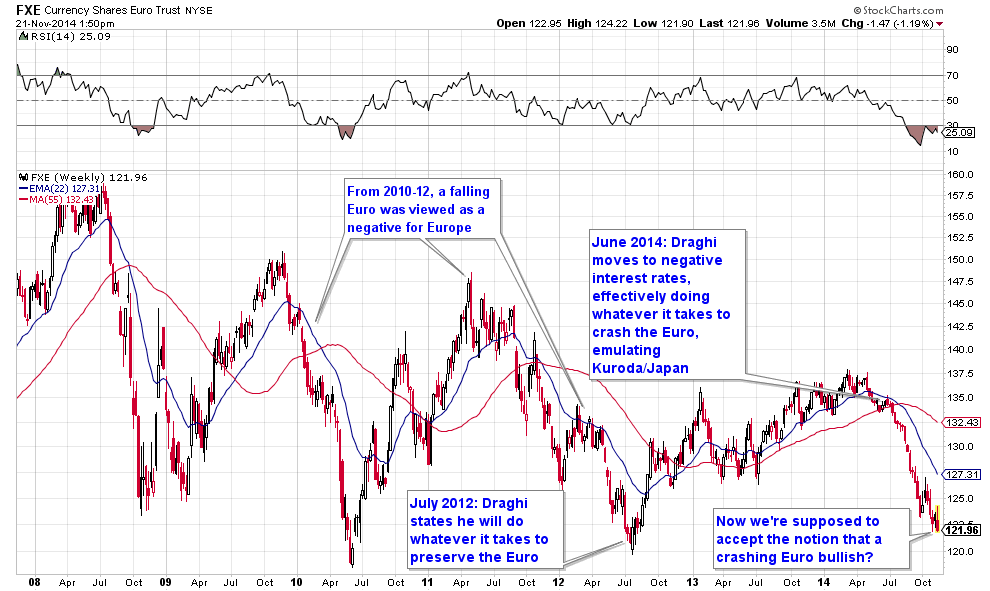

Jul ’12: Whatever it takes to save the Euro

Jun ’14: Whatever it takes to crash it

Believe Draghi: it will be enough

Draghi gets Bilello’s sarcasm but Bilello doesn’t get Draghi’s reality. What matters right now is effort and not outcome. No one knows what the outcome of all this global QE will be anyway. So, sort of like Tennyson’s brigade, it is but to do right now and hope. Fortunately, markets so far have been willing to go along with hope.

3. The D & B Oracles

At this point, there may be only two truths. The first is secular:

- Rich Bernstein – “gradual type improvement in the economy is fantastic for investing; similar to 1986; then goldilocks; today horrible”

- Tony Dwyer – “the great mistake we convey & make to the investing public is that you need great economic activity to have a great stock market; it is actually the opposite;the last thing you want is very high consumer confidence, very high growth rates because that brings in the Fed, ultimately inverts the curve and shuts down credit; so this kind of moderate rate of economic activity going into the end of the year hopefully continues”

The second is as near-term as you can get:

- Dwyer – It ultimately comes down to the end of the year run is based more on the need for performance than it is based on fundamental developments;

- Bernstein – “in the biggest bull market of our career;market is fairly valued where it should be”

- Jeffery Saut – very difficult to get the market down between thanksgiving and Christmas; seasonal upside bias; 8-10 years left in a secular bull market; everything works in a secular bull market

4. Equities

The U.S. market has been about gaps – upside gaps at the open due to news events like Friday morning. What happens to such opens. Chad Gassaway explains in his article Big Gaps At All Time Highs:

- “When this has taken place there has been a downside bias from the open to the close with an average return of -0.37%. While win rates were 50%, the average loss has over doubled the average gain on the session which skews the risk of intraday downside versus upside.The following session has been

lower 66.66% of the time and has averaged a loss of -0.76%.Furthermore, average losses of -1.37% versus average gains of 0.46% have made the risk to reward unfavorable. Losses have continued three session later with average returns of -0.92% and a 33.33% win rate. From this point forward, while

returns remained negative the losses became gradually smaller going out to two months.Finally, three months later the market averaged a 4.05% return and a 100% win rate. In conclusion, while it has been difficult to enter new positions on these gaps at all time highs, it has paid off over the long term.”

That is why those hooked on hopium who buy upside gaps have been rewarded this year.

Kudos to Jeremy Siegel for making a call for Dow 18,000 when it sounded far away. We are already there now. So this week Prof. Siegel now called for 20,000 on Dow by year-end 2015. Tony Dwyer’s target is still 8% away, but he is undeterred and called for 2237 by year-end 2015:

- “2230 by end of the year? if it doesn’t happen by end of the year, it will happen in early January; again there is a history here where, in midterm election years in Nov & Dec us up 5.2%; we have low inflation which pulls in the Fed, the real funds rate has not changed in 4 years which is why I haven’t changed in 4 years, so 17.5 times earnings when the market should trade at 19 times in sub-3% core inflation environment, you got to buy it, its not expensive.”

Kudos to a twitter-trader who has been right often. Where does she think S&P goes next year?

- Friday – Mella @Mella_TA U need to wait for a little pullback and then get ur little ass’s long again and come back next year at 2350 $SPX

- Friday – Mella @Mella_TA $SPX monthly target next year possible – FRAME IT ;-))

Bernstein & Dwyer consider the market as fairly valued or not expensive. The other side comes from :

- Friday – Urban Carmel @ukarlewitz What that also means is that price/sales (1.75x) multiples are driving gains. 2003-07 peak was 1.6x. 1998-01 peak was ~2x. Remarkable

and from:

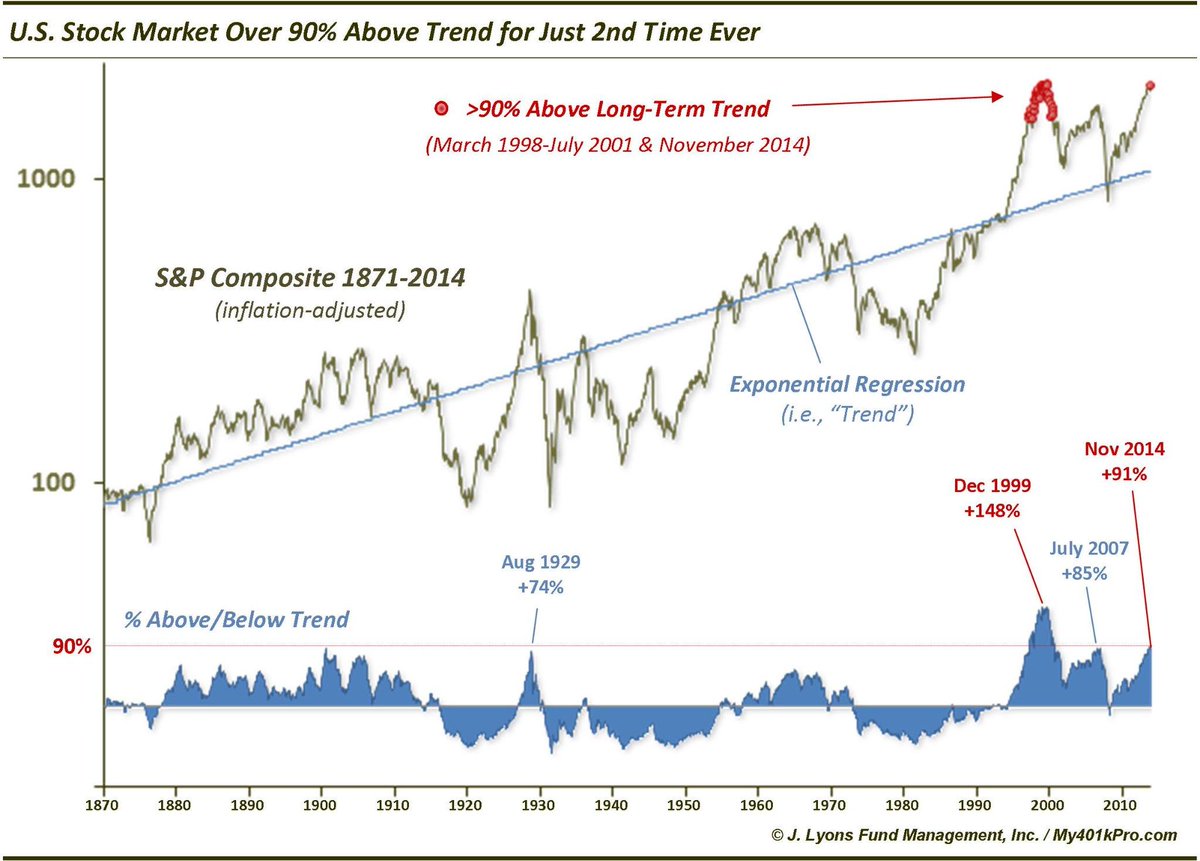

- Friday – Dana Lyons @JLyonsFundMgmt – ChOTD-11/21/14 US Stocks Now 2nd Most Overbought In History $SPY $SPX

Notice that the S&P did not make its high of that cycle in December 1999 but three months later on March 24, 2000. So the chart above is not necessarily a sell signal right now.

But what about out-performance of US equities?

- Urban Carmel @ukarlewitz – BAML: funds are 25% o/w US equities, a 15-mo high. This is where US outperformance has ceased in the past

That brings us to where we began. Does EM provide a beta-charged return over the next 5-6 weeks?

5. Interest Rates

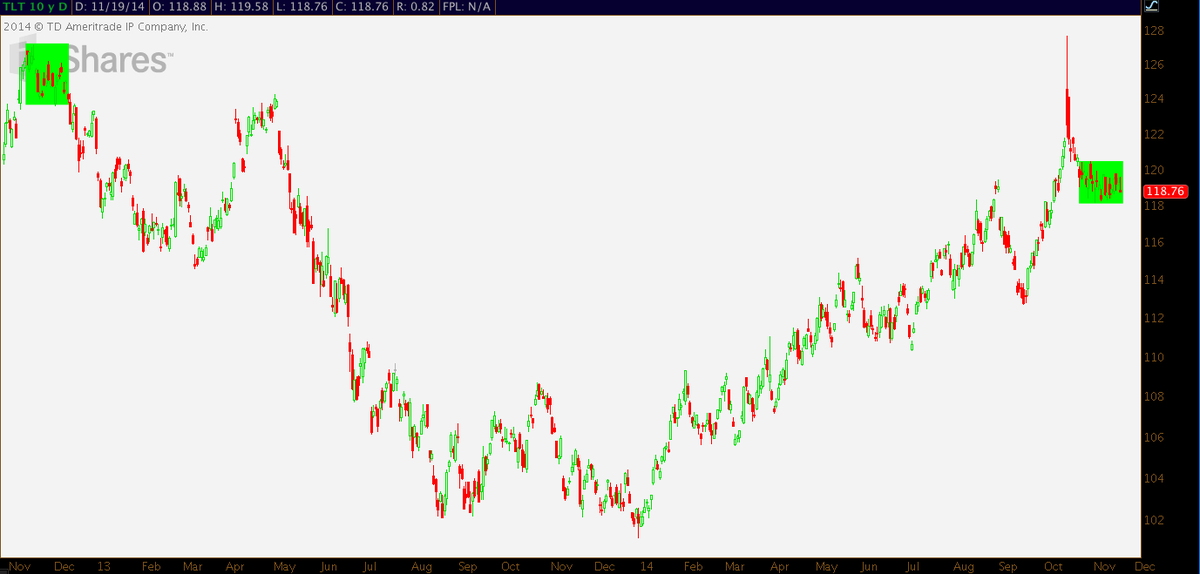

Interest rates fell a bit this week, thanks again to another Friday. It was amazing to see the 30-year yield fall by 3 bps on such an up risk day as Friday. Is the consolidation since the flash crash over? Guy Adami of CNBC FM argued yes because TLT recaptured the 120 level.

- Friday – J.C. Parets @allstarcharts – I still don’t see anything to not like about bonds. The economists for some reason still tell us to sell them. If $TLT breaks 121 goodbye…

- Wednesday – Rachel @Sassy_SPY – “@michaelbatnick: $TLT Trading in the tightest 20-day range since the end of 2012. ” – going to explode

The 30-5 year curve flattened by 3 bps this week. Will the Fed tighten as long as the 30-year keeps getting lower & the 30-5 curve flattens? How can the Fed steepen the curve? One way is, as Ira Harris told Rick Santelli, the Fed will not tighten in 2015 if the economy stays like it is now. And,

- Holger Zschaepitz @Schuldensuehner – Citi changes Fed call. Pushes back Fed hike forecast. Expects 1st US rate hike by Dec2015.

Isn’t inflation is the primary consideration for the Fed?

- FxMacro @fxmacro USD5y5y inflation swap new lows on the year

With Japan, China & Europe all serially & seriously engaged in lowering their currencies, how does the U.S. Dollar stop becoming stronger? And how does inflation get into America with a strengthening U.S. Dollar? So why shouldn’t Chair Yellen keep rates low and allow for wages to rise in a disinflationary America? That is why we think the Treasury market will have to raise short rates and lead the Fed. But for that, the 30-5 year curve has to bear-steepen.

6. Gold, Oil

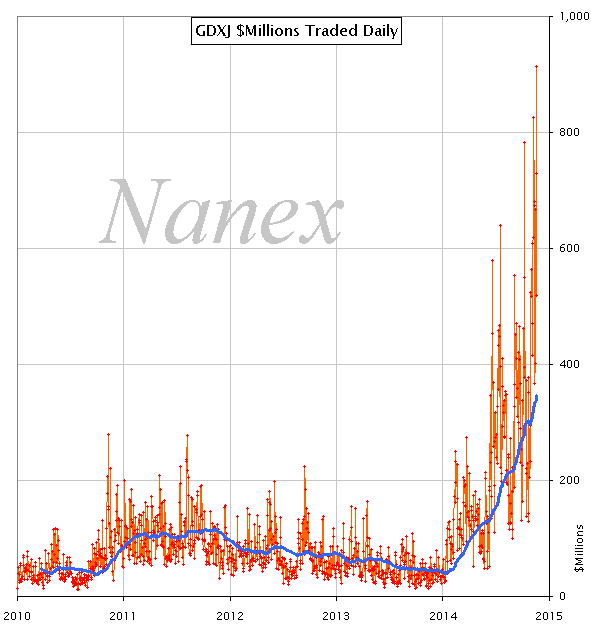

Gold miners had another good week with GDX up 4% and GDXJ up 9.5%. Gold & Silver were up about 50 bps and 1% resp. A world in which rates are falling faster than falling inflation cannot be all that negative for gold, especially after rates get near their lows. Add a stock rally to that and you could have some action in Gold miners despite their overbought condition after a ferocious rally since the first week of November. And those who prefer volume with price gains should look at:

- Wednesday – Eric Scott Hunsader @nanexllc – Trading in Market Vectors Junior Gold Miners ETF (GDXJ) has exploded – set record today:

Then you have:

- Wednesday – Market Anthropology @MktAnthropology – That said, gold (shown inverted) has in the past led the pivots lower in the $ & real rates.

What will next week’s OPEC meeting bring? Tim Seymour of CNBC FM predicted on Friday that OPEC is willing to wait out the decline but they will cut production by 500,000 barrels and Oil will rally. His FM colleague Steve Grasso suggested selling energy stocks next Friday. Here was Seymour talking major policy change in China & predicting a rally in Oil only to suggest “sell IWM” as his final trade on Friday. And Steve Grasso despite his negative talk about energy stocks suggesting buying energy stock MHR as his final trade. What’s with that? Walk contrary to talk?

We may not get these FM guys but we do get what Wilbur Ross says and said on Friday on CNBC Squawk Box:

- “Chinese revealed yesterday for the first time their strategic oil reserves are about 91 million barrels, that’s only about 10 days supply & as far as one can tell, the govt had been targeting to get permanent reserves of as high as 30-days so that augurs well for some near term buying of oil as well”

Natural Gas fell hard on Friday. Is that because the cold arctic blast is behind us? Bespoke seems to think so in their article Is The Short Term Top in on Natural Gas?

Send your feedback to [email protected] Or @MacroViewpoints on Twitter