Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Same old, Same old?

Something big changed this past week, really big, so big that it will reverberate in homes & sports bars until 1st January 2016 – SEC got wiped out by other conferences especially by the down & out Big 10. So you have to wonder whether that will prove to be an omen for 2015 for down & out asset classes.

But that’s not how it went down on Friday, January 2, 2015 – it was all same old, same old. The inexorable trend for 2014 that began on January 1, 2014 continued on the first trading day of 2015:

- Charlie Bilello, CMT @MktOutperform – One of the key themes in 2014 was the yield curve

flattening. Continuing here today. http://pensionpartners.com/blog/?p=1129

Our preference is to look at the 30-5 year curve to minimize Fed’s involvement to the extent possible & this spread also went lower on Friday to 107 bps with 30-year yield falling by 5.9 bps to 4.1 bps for the 5-year yield.

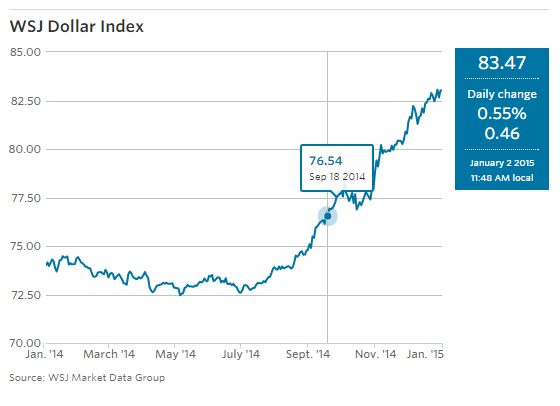

The second inexorable trend, this one just for the 2nd half of 2014, was the rally in the U.S. Dollar.

- Pedro da Costa @pdacosta – Almighty buck: U.S. dollar surges to a nearly 9-

year high against major rivals http://www.wsj.com/articles/dollar-surges-to-

near-9-year-high-against-biggest-rivals-1420215066 … pic.twitter.com/e1eykK9K25

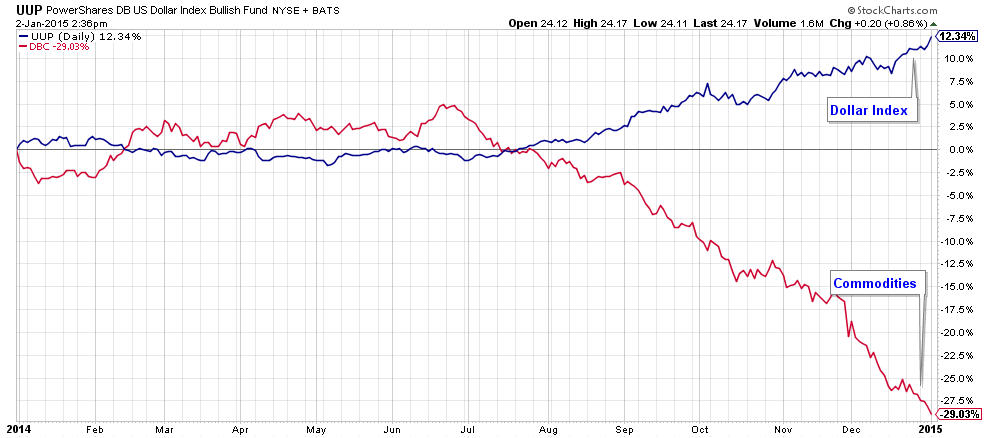

That should say:

- Charlie Bilello, CMT @MktOutperform – Dollar up, Commodities down, picking up right

where they left off. $DBC $UUP http://pensionpartners.com/blog/?p=1129

And what about stocks?

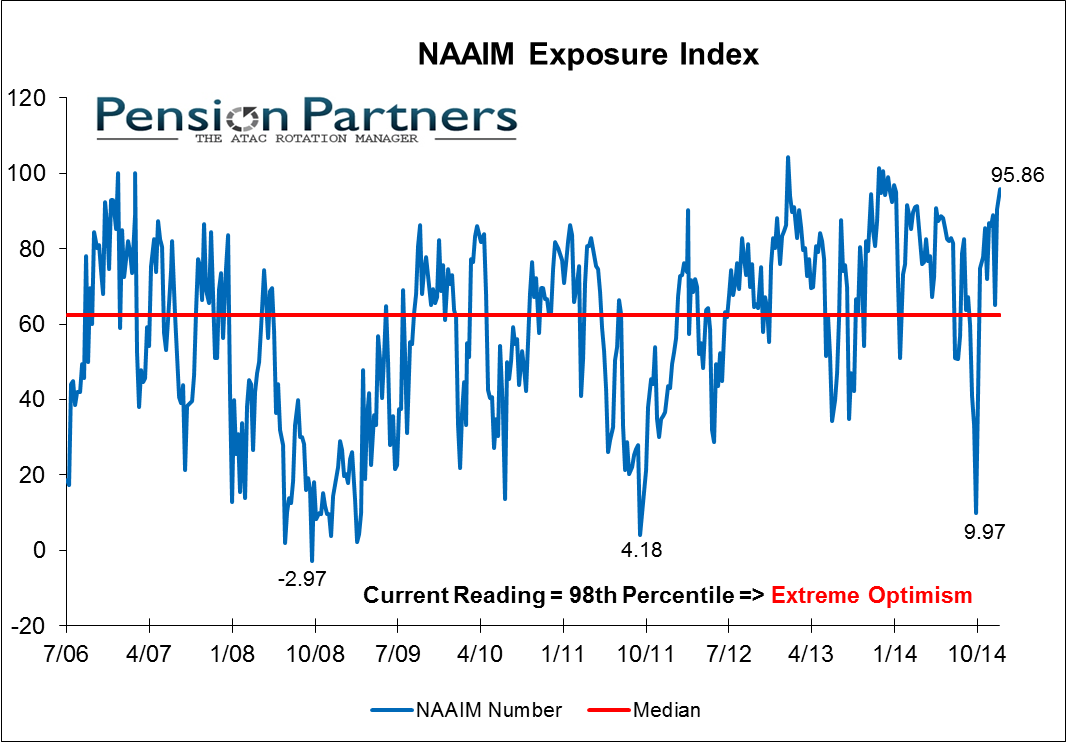

- Charlie Bilello, CMT @MktOutperform – Active managers entered the year 95% net long US

equities. 98th percentile historically.

Can it be same old without waiting for European QE & the endless fall in European sovereign yields? Draghi made noises about large-scale buying of government debt and European debt responded:

- Mark Newton @MarkNewtonCMT – Monthly trends on Italian 10yr yields truly

something to behold- I don’t even enjoy Skiing on slopes this Steep:

.

As in 2014, the yield gap between overseas debt & US treasuries provides a tail wind for US Treasuries:

- Jesse Felder @jessefelder – @marknewtoncmt still fairly large gap between treasuries and gilts, too:

So what can be the agent of change in 2015?

2. Fed

This is the biggest question for 2015, perhaps because the Fed can act if they choose to ignore the rest of the world:

- David Rosenberg in Friday’s weekly summary – For 2015, the one thing we do know with a degree of certainty is that the senior brass at the Fed now seem intent on breaking away from its zero interest rate policy if the economy evolves as planned.

He did say on Friday morning on CNBC SOTS that the U.S. economy is chugging along at 3% growth but he added:

- “ISM probably told you the impact of the strong dollar is probably biting to some extent industrial activity.”

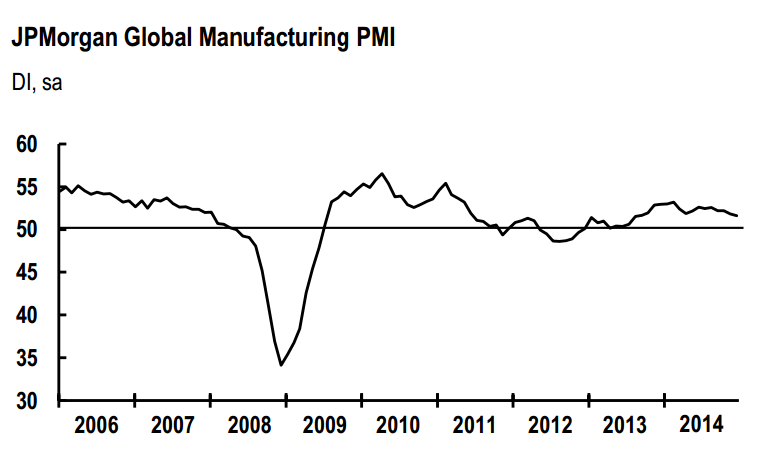

Some “bite” according to:

- Charlie Bilello, CMT @MktOutperform – JPMorgan Global Manufacturing PMI at 51.6 in Dec, lowest level since Aug 2013.

That strong dollar puts Larry McDonald in the opposite camp as he said on CNBC FM 1/2 on Friday:

- “if you look at the world today, what is most disturbing is high yield bonds, leveraged loans, EM sovereigns & EM corporates – that’s about $3 trillion of debt globally that is massively, massively under-performing US equities – the Dollar has the Fed against the wall, the $ is at a 9-year high, it is weakening all those bonds destabilizing the world, destabilizing the high yield, destabilizing EM sovereigns, so the Fed can’t possibly hike rates next year or the 1st 3 quarters” .

3. Draghi, QE & Euro

At this point, it is virtually built-in that Draghi will launch European QE on January 22. What if he does not? Or worse, what if he does & the market dismisses it in the next couple of months? That’s what Paul Richards is concerned about as he said on CNBC FM 1/2 on Monday:

- “the problem I have got with QE is this – its all Europe has got in my opinion – you look at Europe right now, you still have Russia-Ukraine; you have Greece issue that is looming they will probably get through it but overall France is really struggling with budget deficit so what has Europe got – only QE & my issue would be this – the US went 3 times on QE; I don’t think the conviction is there with Europeans to go more than once; what if it doesn’t work? the markets are going to be so impatient; what if six months into QE, suddenly the market says where’s the growth? What have they got then? a Lower currency – its the only thing that can save them – that could be quite systemic for global markets.

A big change over 2014 could well be a fall in the U.S. Dollar vs the Euro. But is that possible and why? Tom McClellan doesn’t guess why but he does say the Euro Is Ripe For An Upturn:

- “there are 3 big clues that an upturn for the value of the euro is coming. How much of an upturn is not indicated, but it should at least be a noticeable upturn in the charts”

- #1 is the Commitment of Traders (COT) Report. It shows that commercial traders of euro currency futures contracts are now net long to the largest degree since July 2012. The commercial traders are the big money, and thus presumably the smart money, but they are often early in getting to an extremely skewed position like this. They have been net long to varying degrees for the past 8 months and it has not mattered yet. But the potential energy is there.

- #2 is that the beginning of a new calendar year usually sees some kind of reversal of the existing trend in the euro. … The Feb. 1, 2013 top was a much later than normal manifestation of this behavior; usually the reversal is closer to New Year’s Day.

- #3 is that gold prices are suggesting that an upturn is coming for the euro.

- Gold is now making higher lows while the euro is making lower lows, and history shows that when the two disagree, it is usually the price of gold that ends up being right about where both are headed. … I still believe that once gold priced in euros can break through 1000, that traders around the world will recognize that and pile in.

On the other hand, Louise Yamada sees more dollar strength in 2015 as she told CNBC FM on Wednesday, December 31:

- “We think the trade-weighted dollar has initiated a new structural bull market and it is very impressive.”

4. “a day that will live in technical infamy”

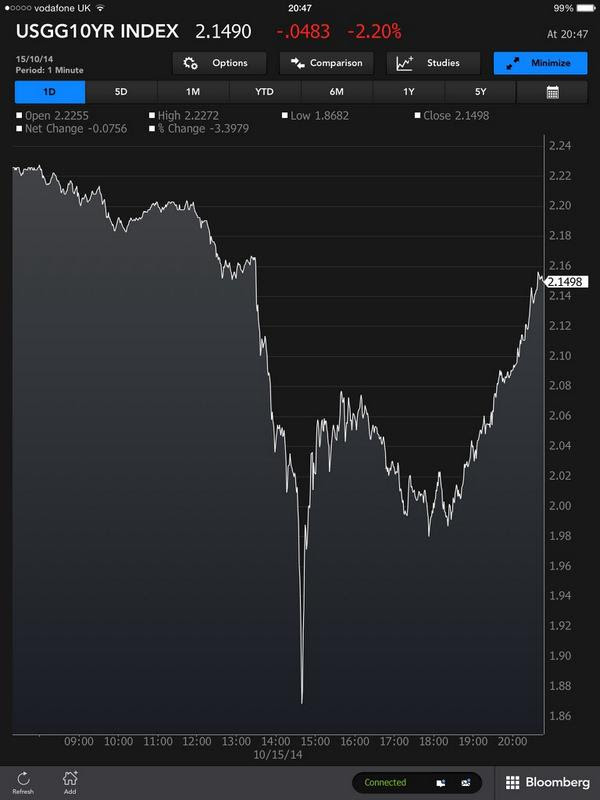

Remember the photo below from Toby Nangle (@toby_n)?

This is the photo of the action in 10-year treasuries on October 15th, the day Rick Santelli called as “a day that will live in technical infamy“. Why did Santelli refer to this day on this Friday? Because, on Friday, the 30-year yield closed at 2.69%, very near the intra-day low of 2.67% of October 15th. Of course, the 10-year is still at 2.12% far away from the 1.86% intra-day low of 10/15 and the 5-year at 1.62% is far far far away from the 1.11% intra-day low on 10/15. This shows both the drop in the steep drop in the 30-year yield relative to the fall in 10-year & 5-year yields. Something is rotten in the state of the U.S. economy, the long bond is saying.

Below is another reason to be long the Long Bond:

- Hedgeye – In size, we would much rather be long the Long Bond via TLT than SPY with this

illiquidity set-up in stocks looking very similar to the end of September and November. That of

course was just before the abrupt 10% and 5% corrections in early October and December.

That brings us to:

5. U.S. Equities

First the very near term:

- Northy @NorthmanTrader – 2nd trading day of January “tends” to be a positive one. Note markets have been down several days in a row now. pic.twitter.com/G71f6194xz

- Paul Richards on Monday – it starts with payrolls; I want to see that data print well again; I think it will – it just feels good on the street right now – you take that into Jan 22 – Europe has to move on QE – that should be a good start for the year for markets – I can see 7-8% but a year out this market could be flat to down – I think the second half of next year is going to be pretty rough … I don’t think the conviction is there with Europeans to go more than once; what if it doesn’t work? the markets are going to be so impatient; what if six months into QE, suddenly the market says where’s the growth? What have they got then? a Lower currency – its the only thing that can save them – that could be quite systemic for global markets – that’s why we could get six months of this, six months of fun & the second half next year needs really careful watching.

- Larry McDonald on Friday – likely that your best purchases in 2015 are likely to be in 2nd quarter – in the 1st quarter, you could get like last year a potentially 10%-15% down move.

The earlier tweet from Larry McDonald amplifies the point he made on CNBC FM 1/2 on Friday:

- Tuesday – Lawrence McDonald @Convertbond – Bought Stocks; Returns in Yr

2014 – Jan 1st: +12.6%; Oct 15: +14.4%

2012 – Jan 1st: +11%; June 5: +11%

2011 – Jan 1st: +0.1%; Oct 3: +17%

There is, of course, no shortage of long-only managers who are bullish on the U.S. stock market and who advise against worrying about short term corrections. And they could be well right as they have been for 2013 & 2014. But there is nothing value added for us to add to that sentiment. There are of course many who predict doom to come, a group that David Rosenberg described as:

- “To these fanatics, if the market rallies, it is due to some unholy alliance somewhere, and if the

market dives, it is good triumphing over evil.”

We will take the middle road today and point out some excerpts from S&P 500 Quarterly Musings by Northmantrader.com:

- “The $SPX is on its 8th consecutive quarterly gain; Each of the past 7 quarters has seen moves exceeding the upper quarterly Bollinger band; Not once in 12 quarters has the $SPX closed below its quarterly 5 EMA; The current run is only outmatched by the run in the 90’s that led to the year 2000 correction. The two major corrections that occurred after the 2000 and 2007 peaks followed quarters with large candlewicks that had pierced the quarterly 5EMA to the downside (see red arrows).”

Their bottom line:

- “Now none of this guarantees such a repeat coming, but it shows that from a charting perspective similar conditions are in place for a repeat to occur. It is a limited sample size no doubt, but it is certainly notable that both previous tops were accompanied by similar patterns.”

A post from Chris Kimble points out that the German DAX is at a Critical Technical Resistance:

- “As you can see in the chart below, the German DAX has formed a topping pattern similar to 2007-2008. How this pattern breaks could have implications for global portfolios. A break above would be very bullish, while follow through lower would be bearish“.

All this will make 2015 very interesting indeed.

6. Commodities

Peter Boockvar made a gutsy call on commodities on Friday on CNBC Street Signs when he said that “the commodity bear market that started in September 2011 when gold topped out is coming to an end“:

- “Oil is the last major commodity to really crash which tells me this is the end of the commodity bear market. Oil will be the last one to recover but gold, agriculture [and] industrial metals will be the first to recover.”

But Louise Yamada sees oil differently as she said on CNBC FM on Wednesday:

- “It is conceivable that we had a lot of year-end tax loss selling that gave us the last downdraft; may be we get a kickback rally as we open 2015; but I think the possibility of coming back and moving even lower is very real”

7. Macro Viewpoints Awards for Financial Guests & Shows

This year has been difficult for guests on Fin TV and for Fin TV shows. No guest, except for perma bulls, added real and consistent value this year. Perhaps consequently no show added more value than other shows either. Frankly, the trading community on Twitter proved more useful than guests on Financial TV. After all, when there is no volatility and when every dip has to be bought, when the flattening trend in yield curve remains in play for all year with a crystal clear Fed, what insights could guests possibly deliver on TV? Therefore, we are suspending our annual awards for Most Useful Guest & Most Useful Show for this year. Hopefully 2015 will be different.

Send your feedback to [email protected] Or @MacroViewpoints on Twitter