Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. “If you didn’t know any better,”

said Jim Cramer on Friday evening,

- “you might think the Federal Reserve should be cutting interest rates, not raising them which we somehow accept as inevitable; … every industry I follow is coming up short … startling decline in commerce in the past 5 weeks; yet it is a matter of when not if rate hike will occur … you dont raise interest tates in a faltering economy; heck you don’t even talk about raising rates; however it almost feels like the Fed is courting what happened in Europe a few years ago when Jean Claude Trichet put an all clear through and then added 2 rate hikes to boot pushing the continent into a talispin that it is still trying to recover from ..”

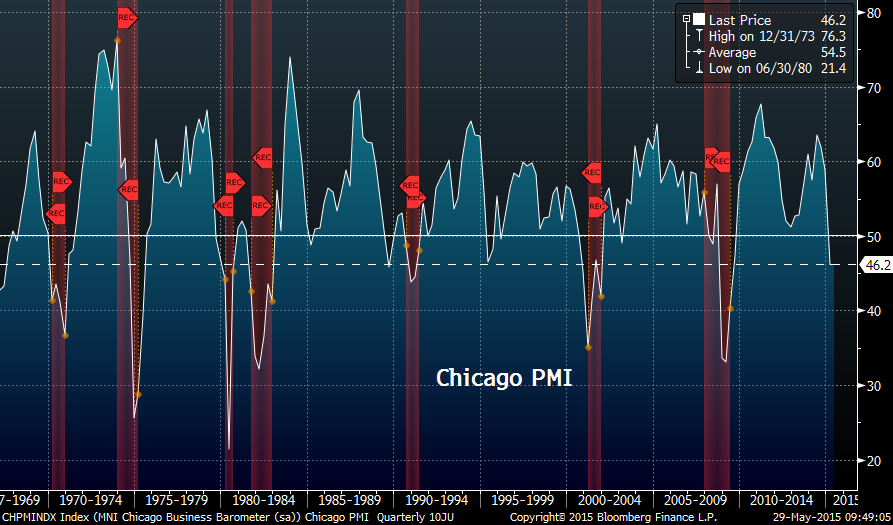

Those who remember Cramer’s tirade in the fall of 2007 should remember that Cramer might have been late to that protest but he was indeed correct to protest. So is Cramer correct about what’s happening to the US economy today? He himself doesn’t know and, like all of us, he is waiting for yet another month’s payroll number to resolve our “What gives?” question about the US economy. After all, it is the only piece of data that remains strong. The rest are bad like Q1 GDP of -0.7% and the stunningly bad Chicago Fed that was:

- zerohedge ?@zerohedge – Chicago PMI was 7 sigma miss http://www.zerohedge.com/news/2015-05-29/chicago-pmi-bounce-dead-crashes-back-near-6-year-lows …

Apart from going one-up on old GE, the importance of this Chicago Fed number is:

- Charlie Bilello, CMT ?@MktOutperform – Chicago PMI at 46.2 vs. 53 consensus. Outside of ’89, drops below this level were associated with recessions

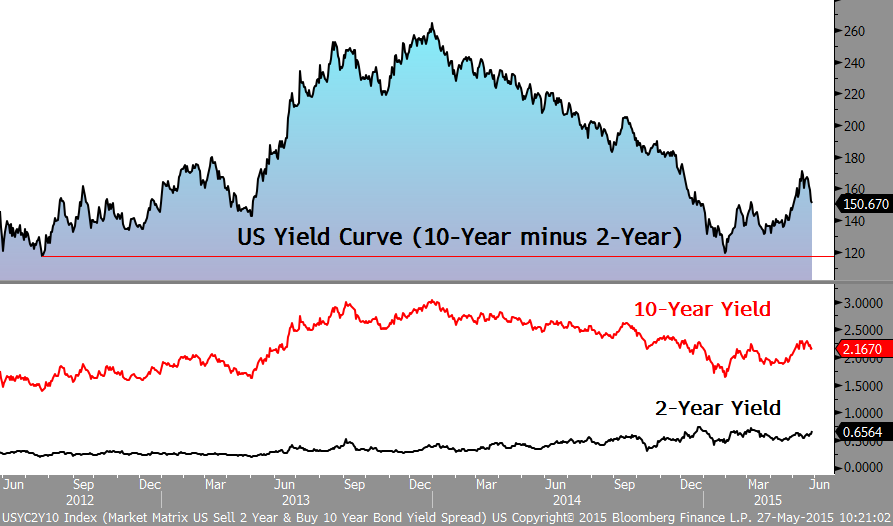

And what should happen if such conditions are possibly upon us? What has happened over the past two weeks:

- Wed – Charlie Bilello, CMT ?@MktOutperform – Yield Curve flattening over the past two weeks.

We remember the day of the 30-year auction in June 2007 and its aftermath very vividly. As we wrote two weeks ago, the bad 30-year auction of Thursday, May 14, 2015 resembled that June 2007 auction. And its aftermath seems to be following the 2007 precedent – the 30-year yield is down 19 bps from the pre-auction Wednesday (5/13/2015) to this Friday; the 10-year yield is down 16 bps & the 5-year yield down 7.5 bps. The 30-5 year curve has flattened by 12 bps from 151 bps to 139 bps. So has the inexorable steepening trend of 2015 now reversed? Are we back in the inexorable flattening trend of 2014 with the long end warning the Fed of risks of tightening? The bond market may be bigger and more correct in its messages, but it can’t deliver a message like Cramer did on Friday – by bringing in the proverbial ghost of Trichet.

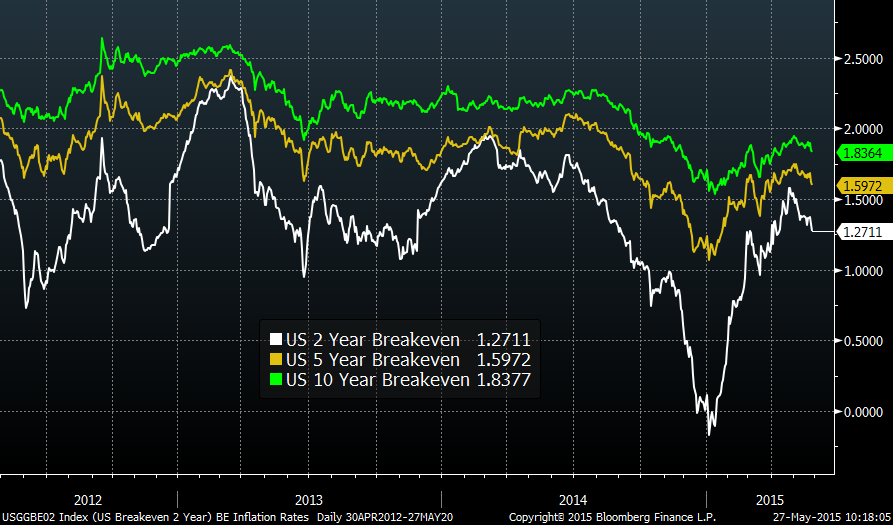

What about inflation, you ask?

- Wed – Charlie Bilello, CMT ?@MktOutperform – Breakeven inflation rates peaked a month ago, starting to turn down here.

It is very simple but very frustrating:

- Fri – David Rosenberg in his weekly buffet – It all comes down to economic growth and the Federal reserve policy and its a waste of time to try and make it any more complicated than that.

Chair Yellen is trying hard to send a hawkish signal to prevent stocks going to the moon. That makes sense unless she turns into a Bernanke who waited too long in 2007 to ease & then found he could not reverse the slowdown. If that happens, then Cramer will have to rant even louder & with more emotion than he did in 2007.

Let’s see what next Friday brings.

2. Treasuries

Last week, we highlighted tweets of J.C. Parets about Treasury yields. He proved correct this week and raised his conviction level:

- J.C. Parets ?@allstarcharts – 1 thing keeping me bullish bonds, other than terrible economists, is 10yr Note.Higher lows & higher highs above rising 200 day mov avg $ZN_F

- J.C. Parets ?@allstarcharts – those interest rates really look vulnerable here. I can’t help it. Been buying bonds very aggressively looking for a break $TNX

- J.C. Parets ?@allstarcharts – I really think if 2.13% breaks on a closing basis in the 10-year it’s game over $TNX

And the 10-year yield did break 2.13% to the downside on Friday, a weekly close below the 200-day as well. But that break of 200-day has not yet been confirmed by the 30-year yield or by TLT.

The rally of the past two weeks and the looming trend line persuaded the ACG-Bear Traps team to recommend selling 1/3rd of the TLT position they had added in early May. They think TLT has further to go but discretion being better part of valor seems to the message.

3. Equities

This week, the VIX index rallied by 10% from utter complacency to a high complacency level of 13.84. That did coincide with a 1% decline in Dow and S&P. But is that positive for next week?

- Friday – Tsachy Mishal ?@CapitalObserver – $CBOE put/call at 1.39. It doesn’t get much higher than that

- Chad Gassaway, CMT @WildcatTrader – Narrow ranges through the end of May has led to positive returns the remainder of the year.

- Chad Gassaway, CMT @WildcatTrader – Since 2012, when the SPX lost >1% for the first time in two weeks, the index closed higher at some point over the next week 25 of 27 times.

But,

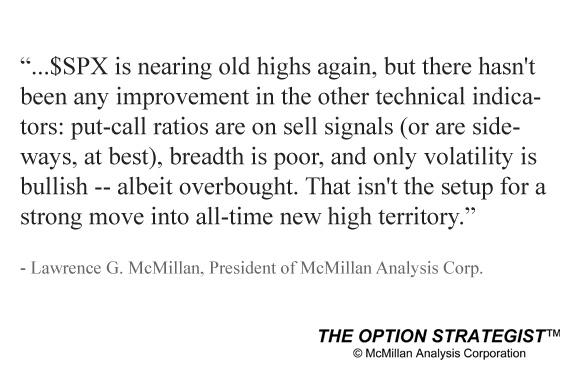

- Lawrence G. McMillan ?@optstrategist – My Weekly Market Commentary http://www.optionstrategist.com/blog/2015/05/weekly-stock-market-commentary-52915 … $SPX $VIX #options

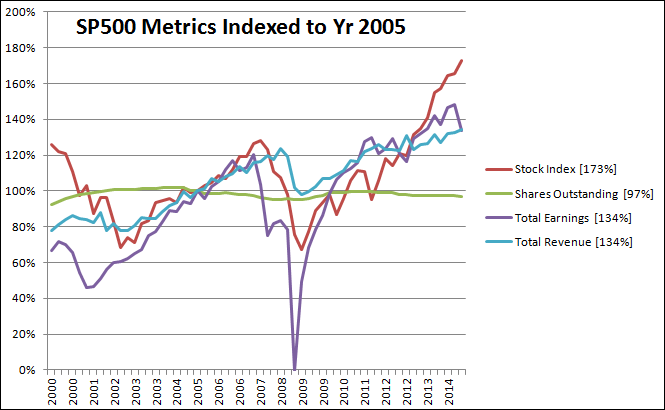

That seems to be the message of the following chart from S&P 500 Valuations Still Lofty Per Sales, Earnings, And PE Multiples.

That brings us to breadth or the divergence between the cap-weighted S&P 500 & the equal-weighted S&P 500.

- Dana Lyons ?@JLyonsFundMgmt – ICYMI>ChOTD-5/28/15 Equal-Weight S&P 500 Losing Relative Strength $RSP $SPY Post: http://tmblr.co/Zyun3q1lttlFs

Lyons explained further in his article:

- Despite the Equal-Weight RSP’s new price high in May, there are a number of negative developments on the chart regarding its ratio versus SPY:

- The March breakout in the RSP:SPY ratio was not sustainable. 2 weeks later, the ratio was back below its highs of February-April 2014, June 2014 and February 2015, creating a likely “false breakout”.

- RSP’s May price high was not confirmed by a new high in the RSP:SPY ratio.

- The RSP:SPY ratio has broken its post 2012 UP trendline (of course, we are breaking our own trendline rule of requiring at least 3 points of contact to constitute a valid trendline. However, even if it is not significant, the break is not a positive.)

- It is true that this “ratio” breakdown between the Equal-Weight S&P 500 and the cap-weighted index is still based on a 2nd-derivative measure. The true warning sign will be a breakdown of price itself. However, the warnings are getting closer as this ratio is at least based on prices. Thus, we deem it to be more relevant and significant in assessing the market’s prospects than the ancillary concerns pertaining to things like valuation, sentiment, investor allocations, etc. Furthermore, the ratio does have a track record as a reliable gauge of broad market health.

- Therefore, with signs of cracks in the Equal-Weight S&P 500’s relative performance, we have more evidence that all is not necessarily as rosy as it may seem with the major averages near all-time highs.

Speaking of false breakouts,

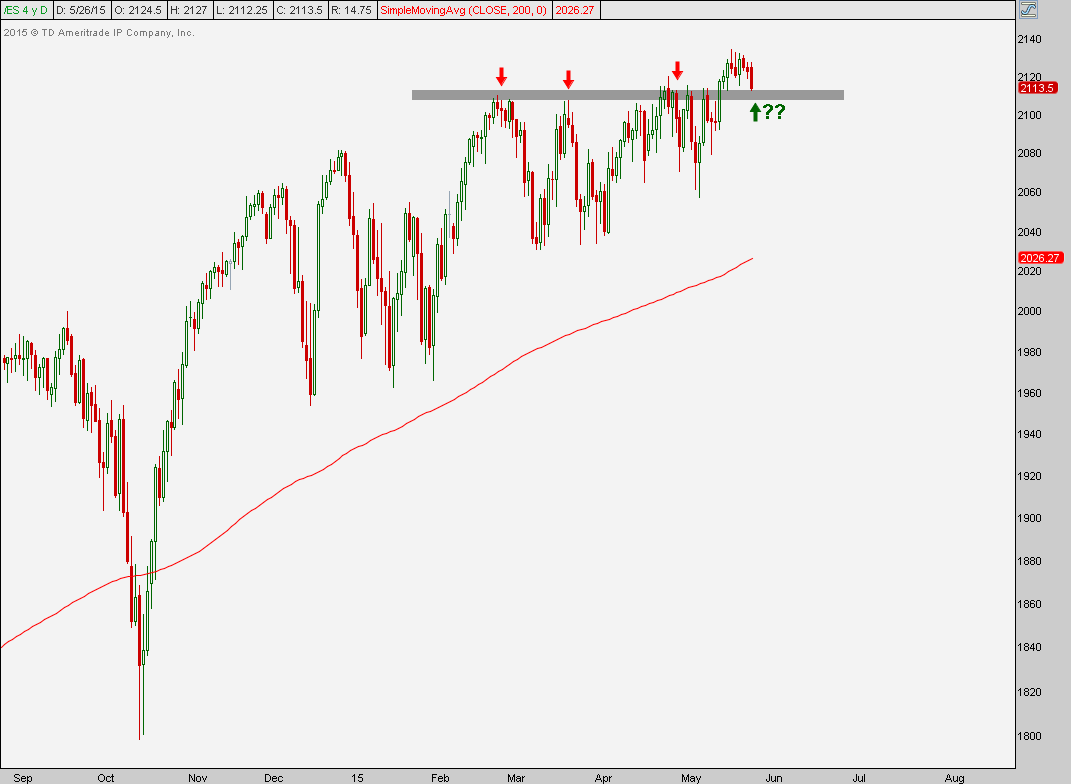

- Mon – J.C. Parets ?@allstarcharts – Is this going to be a successful test of former resistance in S&P futures? or beginning of a failed breakout? $ES_F

Then there are those who have conviction:

- CNBC Futures Now ?@CNBCFuturesNow – Piper Jaffray’s @cwjmn says the S&P 500 could hit 2,350

and,

- Wed – James Goode ?@OntheMoneyUK – Prepare for a major opportunity: 20%+ BEAR MARKET IN US SMALL CAPS MAY HAVE JUST BEGUN http://schrts.co/N8d6M0 $RUT $IWM $RWM $TWM

Finally, a word from a fundamental guy who has been right far more than he has been wrong during this bull market – Jim Paulsen of Wells Capital Management used the two words in his conversation with CNBC’s Brian Sullivan on Tuesday:

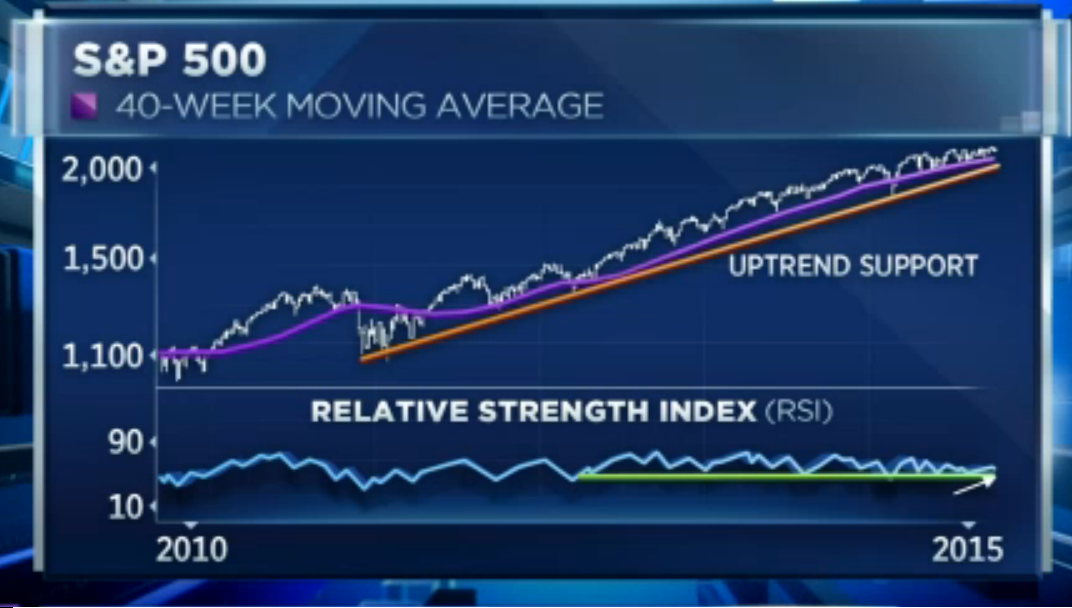

- “This continuous failure of the stock market to rise to and extend a sustained rally;how many times have we done this now? going back to last year we make a run and refail again – if we close below 2100 again today, that’s giving a sense of a major top“.

4. Gold

The Dollar was up by about 90 bps this week and Gold was down by 1.3% with Silver down 2.2%. One trader is not taken in by Gold’s allure.

- Wed – J.C. Parets ?@allstarcharts – Gold probably sees $1000

On the other hand, Chris Gersch of Bell Curve Capital said on BTV Market Makers that this is a great time to buy Gold. He says going back last 6 months, the 1180 level has been a great place to buy from. But he did say on Wednesday that Gold will close the week above $1,200 which it did not.

We wonder what happens when it becomes abundantly clear that Chair Yellen will not raise rates in 2015. If that doesn’t create a rally in Gold, is there anything that can?

5. Oil

Since Dollar rallied this week, Oil should have fallen. And it did until Friday. Both USO & BNO were up 4% on Friday. Warum? Was it the drop of 13 in the oil rig count? Or was it Saudi Arabia travelling the road to NonPakistan? ISIS managed to set off its 2nd bomb in a Shiite mosque in Saudi Arabia killing innocent civilians. ISIS doing what it wants in Syria and Sunni Iraq is horrible but that doesn’t move oil. Virtually all of the large Saudi oil fields are located in Shiite majority section of Saudi Arabia. That area becoming the center of NonPakistan-like Shia killings cannot but be positive for oil. Add to that worries about Saudi Arabia getting badly bogged down in Yemen.

Saudi Arabia has maintained that Iran poses greater risk than ISIS just as NonPak has maintained for decades that India poses a greater risk than Talebani terrorists. Now there are reports that ISIS has established a partnership with the Hekmatyar group in Afghanistan. No one is more experienced in insurgency-terrorism than Gulbuddin (body like a rose?) Hekmatyar who was a major ally of US-CIA in the 1980s against the Soviet army occupying Afghanistan. Then Hekmatyar was a major player in the Afghan civil war that killed 50,000 in Kabul alone. After Taleban’s victory, Hekmatyar participated in the Nagorno-Karabakh conflict between Azerbaijan & Armenia. Now he is back opposing the Taleban by allying himself with ISIS?

That won’t change the minds of NonPak Generals just as ISIS-sponsored terrorism inside Saudi Arabia will not change the minds of Saudi rulers who hate Iran more passionately than anything else. Saudi Arabia & NonPakistan have been allies for decades. Now their terrorist enemies are also becoming allies. That cannot but be positive for oil for the intermediate term. And in the short term, we have next week’s OPEC meeting in Vienna.

.

Send your feedback to [email protected] Or @MacroViewpoints on Twitter