Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. It’s All About Greece

But that doesn’t make it easy.

- Thursday – Bespoke @bespokeinvest – Trading Greece is hard

https://www.bespokepremium.com/think-big-blog/trading-greece-is-hard/ … .

This “Dangit” reaction became worse on Friday with the Dow closing down 140 points.

- Friday Mark Arbeter @MarkArbeter – For what it’s worth: $SPX, $SPY falls for fourth Friday in a row. Somebody worried about the weekends? Not that country in Europe?

The action in Treasuries is also governed by the action in German Bunds. Treasury fell on Friday morning despite a hotter PPI. They were simply following the lead of German Bund yields which were falling hard. German 30-yr & 10-yr yields closed down 5 bps on Friday. Come Friday afternoon, Treasury yields began rising from their lows of the morning and actually closed up on Friday.

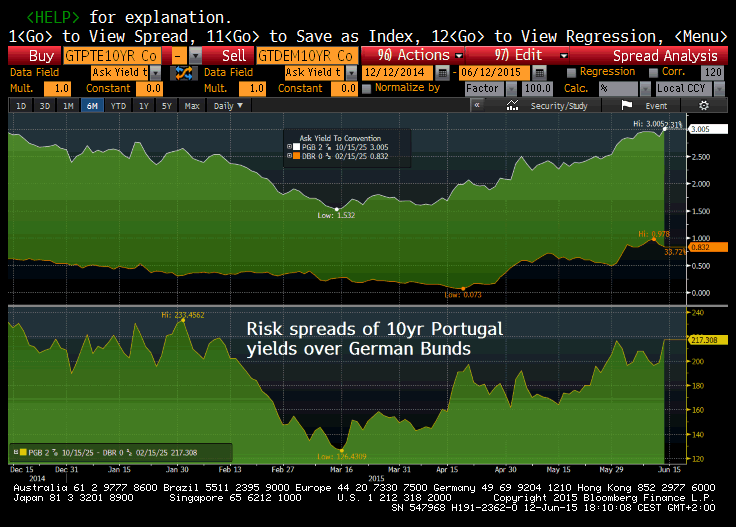

- Friday – Holger Zschaepitz @Schuldensuehner – Athens last hope: Eurozone contagion! Risk spread of 10yr Portugese bonds over German Bunds has risen to 217bps.

- jeroen blokland @jsblokland – The end of an era? After a massive three year rally, peripheral bonds prices are coming down.

It seems a majority of Greek people want to accept the deal offered by the creditors because they are tired & they want to stay in the Europe. But a third won’t accept it. The key is that this third is who put Greek Prime Minister Tsipras and his Syriza party in power. There is no future for Tsipiras & Syriza if they accept this deal from Europe. So they may have nothing to lose. It may also be about respect. Germans & Europe have treated Greeks as semi-beggers who can’t afford to choose. How real is the 24-hour deadline that has already passed? We will know next week.

Everyone seems to have figured out that the end of the Greece-EU relationship is not that big a deal. What if the IMF is wrong and Germany is about to screw up badly again?

- Holger Zschaepitz @Schuldensuehner – #IMF’s ‘never again’ experience in #Greece may get worse. http://news.yahoo.com/imfs-never-again-experience-greece-may-worse-183334227–business.html?soc_src=mediacontentstory&soc_trk=tw …

Is this why German 30-yr yields & 10-yr yields fell by 16 bps & 14 bps in the last two days?

2. Yellen on Deck

Last week, we urged Chair Yellen to take advantage of the 280,000 NFP number and raise rates by 25 bps on Wednesday, June 17. This week we argue that such a rate rise may be the kick Germany-Europe need to decide on a cease-fire with Greece with enough money to tide it over for some months. Because Draghi & Merkel both know Europe cannot handle the twin problems of Greece collapse & Fed hiking rates.

Look at what is happening already in advance of Yellen’s expected hawkish stance next Wednesday:

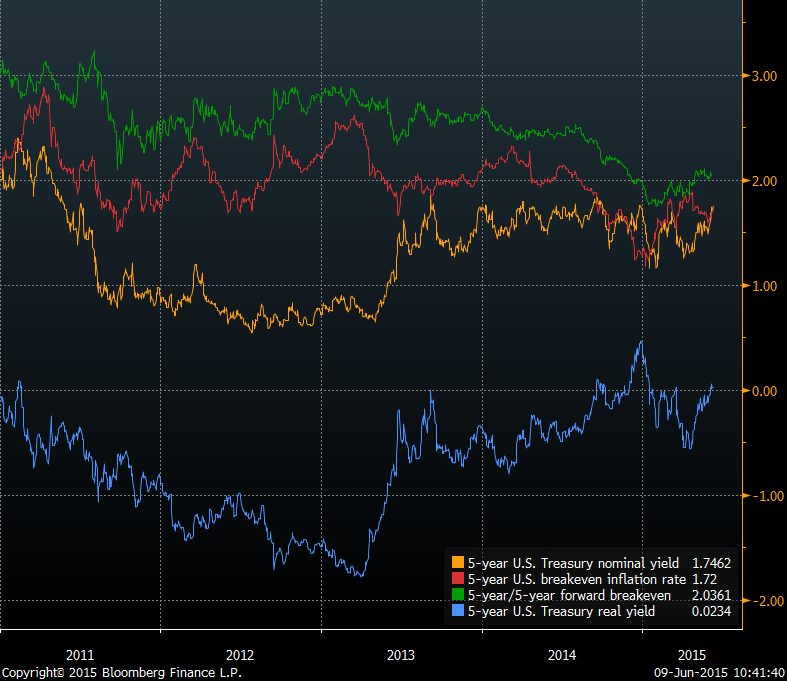

- Matthew B @boes_ – 5y real yields have crept back above zero again in the last few days for the first time since day before March FOMC

- Lisa Abramowicz @LisaAbramowicz1 – Suddenly junk bonds lost their luster, w/investors pulling $1.5 billion from the 2 biggest HY ETFs in the past week. http://bloom.bg/1HZkRGw

- Tuesday – Mark Newton @MarkNewtonCMT – Weekly charts of $JNK to $LQD also might give some insight as to Credit spreads starting to widen in the near future

- EM funds have suffered the biggest outflow in 7 years

So the markets are prepped and the stage is set for Chair Yellen to raise rates by 25 bps next week and promise no more hikes for the rest of 2015. Do we think she will? No. Will she at least sound dovish? We doubt it unless the stock market falls out of bed before the FOMC meeting on Wednesday. Our fear is that she may use her megaphone to sound more hawkish than she really is and that might create unnecessary turmoil.

3. Volatility & Sentiment

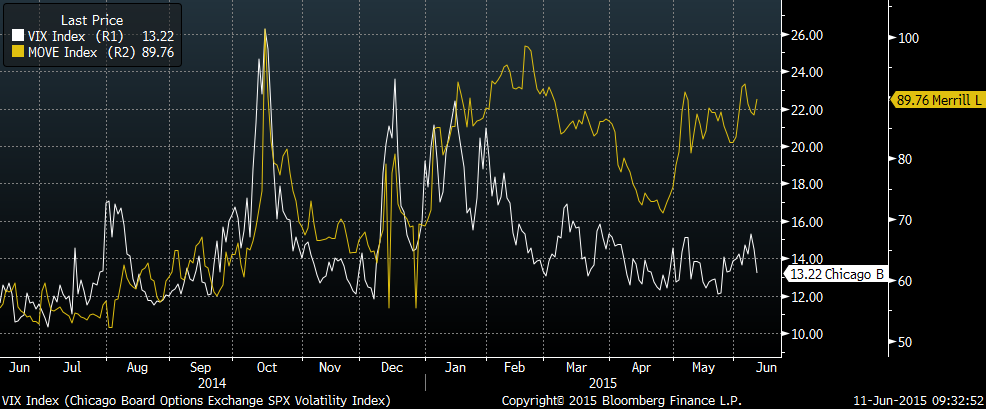

What a spread between volatility in Treasuries & volatility in stocks?

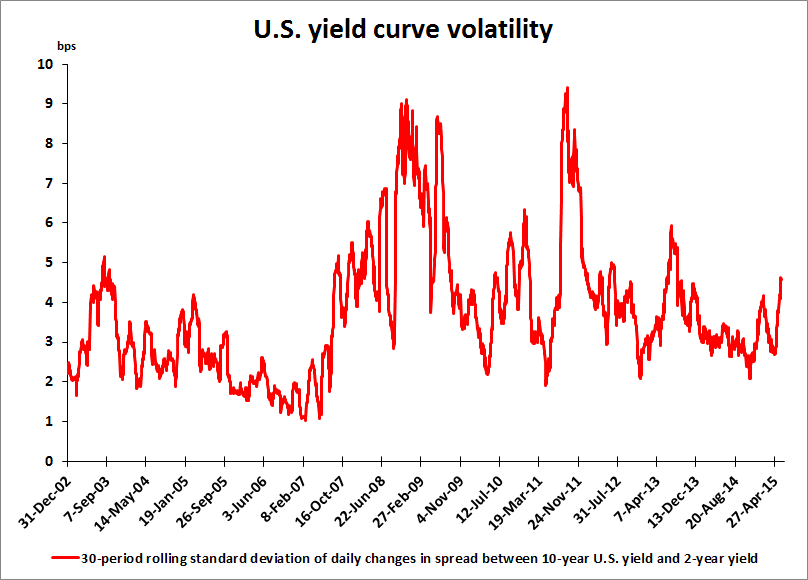

- Wednesday – Matthew B @boes_ Yield curve schiz: U.S. 2s10s volatility highest since the taper tantrum

.

The story in stocks is so different. The VIX fell below 13 again this week.

- Bespoke @bespokeinvest – The S&P 500 has not has a weekly gain or loss of more than 1% since end of April (six weeks). $SPY

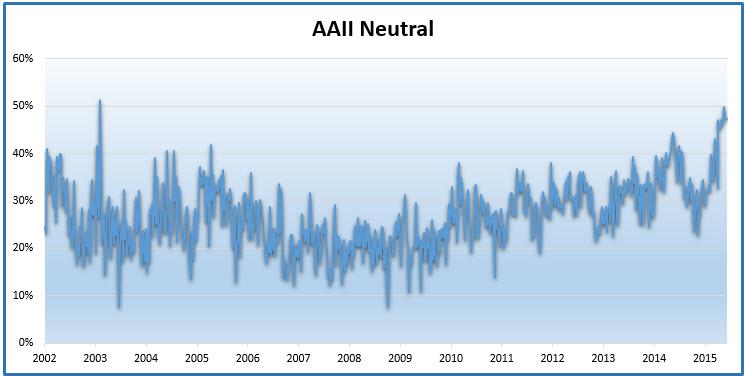

- Ryan Detrick, CMT @RyanDetrick – AAII neutral above 45% for record 10 straight wks. 6 back in ’88 was previous record. No one knows what to do. .

But next week might prove different:

- Friday – Bloomberg Business @business – You can’t keep the panic out of stocks forever, VIX traders say http://bloom.bg/1Giil00

4. Treasuries

Unless Chair Yellen does something completely unexpected, Treasury yields should remain joined at the hip with Bund yields. And Bund yields should be tied to the drama being played in Athens-Brussels-Frankfurt. But for Greece, we would have argued that June is, in our experience, the month that reverses the direction of yield movement of April-May. So this week’s action should, playing percentages, lead to a rally in Treasury prices.

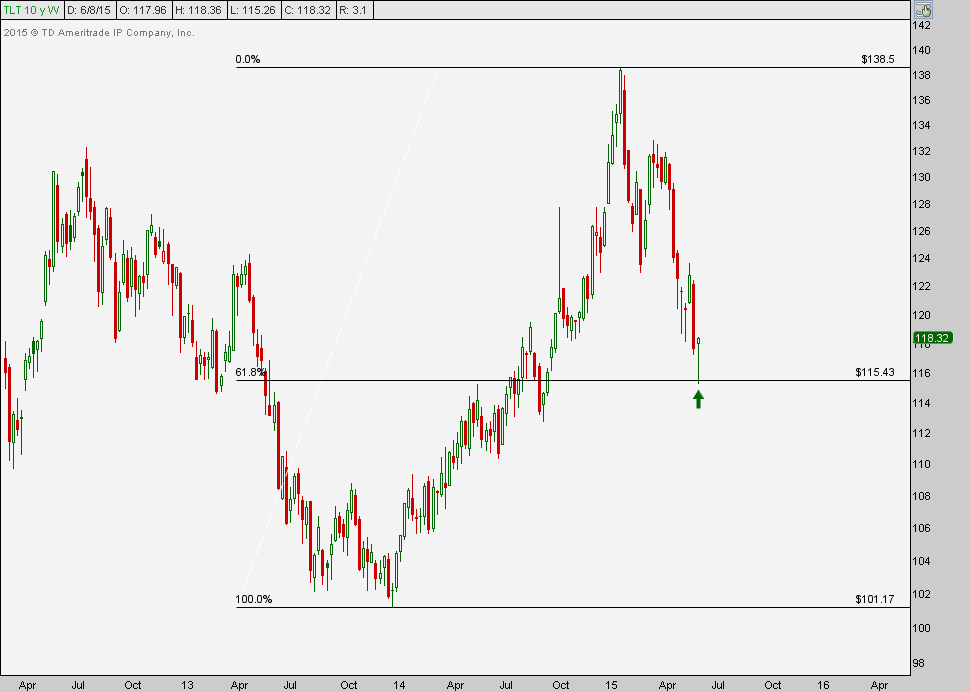

Barring a sudden surrender from Greece or a sensible pragmatic offer from Merkel, the Greece uncertainty should remain elevated. That should be positive for German Bunds & for Treasuries. Remember the call from ACG Analytics on Friday, May 28 to sell a portion of TLT or long duration Treasuries? That turned to be a superb call. ACG did it again with a call to buy TLT or long-duration Treasuries on Wednesday after the close. What a perfectly timed call? Kudos to ACG.

J.C.Parets kept tweeting his positive stance towards TLT all week:

- Monday – .C. Parets @allstarcharts – we’re seeing huge outflows from $TLT lately. Most since we were going into 2014 and also in early 2011, just before huge rallies….

- Tuesday – J.C. Parets @allstarcharts – 30% of the $TLT Market Cap was wiped out in the 6 weeks ended June 5. $1.7B in outflows from what was a $4.3B Fund. I’ll take the other side

- Friday – J.C. Parets @allstarcharts – here’s what I see in $TLT weekly timeframe – bouncing off 61.8% Fibonacci retracement of 2014 rally

- Friday – J.C. Parets @allstarcharts – Here’s what I see in the $TLT daily timeframe – failing to hold below the lower of the two converging trendlines

On the other hand, Market Anthropology wrote this week:

- “With the 10-year yield breaking away from the top of its 2015 range, Treasury yields continue to push higher with all the bravado of an Italian cutterracing in Bloomington. Technically, the 10-year remains on course towards challenging long-term overhead resistance, which we expect will come in ~ 2.65% – after retracing and digesting the large moves over the past few weeks.”

Rick Santelli also described the technical case of 10-year yields going to low 2.60s this week. When asked directly whether he expects the 10-year yield to close at 2.30% or 2.50% by next weekend, Rick Santelli said 2.50%. Our guess would be that the 10-yr Bund yield would decisively break 1% for the 10-year Treasury yield to close about 2.50%.

5. Stocks

Waiting for volatility to spike has been like waiting for Godot. For weeks, we have been featuring comments about imminent breakout of the S&P trading range. Most commentators have played safe by pretending to not have an opinion about the direction of the break. But it is possible to see a downside bias in their public indecision. That is what makes the next call interesting & potentially rewarding:

- Friday – Chad Gassaway, CMT @WildcatTrader – Why Bearish Complacency Could Take Us To New All Time Highs

His article provides a detailed discussion with several charts to support his argument. His conclusion:

- “While complacency has been mentioned as a bearish catalyst by a number of commentators, we lean towards the side that bears remain too complacent that a rally could take place soon that takes us to new highs.”

On the other hand,

- Not Fred Goodwin @Not_Mr_Risk – Call the divorce lawyer! prediction – 5y yields reverse the 70bp ramp and go down as stocks drop 20%

More specifically:

- Friday – Nautilus Research @NautilusCap – the small-cap seasonal trade… $IWM

And the reality:

- Wed – Northy @NorthmanTrader – For giggles: And, yet again, the monthly 8MA was a bottom.The autopilot continues unabated until this breaks. $SPX

6. Oil

Sorry to be consistent & boring, but is Oil also linked to Greece? Surely, oil is about production from Saudi Arabia, Rig Count in America & demand from India-China. Well, not really & not in the immediate term as Friday’s Greece exasperations roil oil article points out:

- “I guess we could talk about the International Energy Agency (IEA) raising global crude oil demand by an impressive 1.4 million barrels a day or the fact that the private forecaster Genscape reported another big 750, 00 barrel drawdown in Cushing, Okla., the Nymex delivery point but instead we are talking about Greece.”

- “Oil prices sold off after members from the International Monetary Fund (IMF) walked out of a meeting with Greece as frustration grows over the unrealistic demands of the Greek government. New concerns about Greek default and the IMF and the European Union getting sick of Greek Prime Minister Alexis Tsipras disconnection with reality and told him to stop gambling with Greece’s future. Tsipras took exception to that characterization but in part because of this Greek tragedy the World Bank cut its world growth outlook to 2.8 pct. from 3 pct.”

7. Must Watch FinTV

We have been meaning to give a shout out to the new Wall Street Week. Any one who has not watched the two Carl Icahn interviews should do so right away. Kudos to Fox Business Network to get and broadcast this weekly show. We dare say, at least so far, that this new WSW is more useful than the classic WSW. Kudos to Anthony Scaramucci & Gary Kaminsky.

8. The Tune from Greece

After so much ado about Greece, how could we not include the Greek tune?

Send your feedback to [email protected] Or @MacroViewpoints on Twitter.