On March 14, 2015, we described our dissatisfaction about Reserve Bank of India Governor Rajan (pronounced “Raajan”) in our article Macro Risk in the Indian economy – Financial Infrastructure:

- ” … India doesn’t have a bankruptcy law that makes equity ownership worthless. … This allows family owners to default without losing any share of their ownership or their management powers. The real solution is to build corporate bond markets that function in the open with a sensible bankruptcy law – both investment grade and high yield bond markets that can fund companies in a transparent manner. These will not replace big Indian banks but provide an alternate access to funding. This will also provide Indian people and foreign investors another way to invest in India’s corporate sector. “

- “Very few economists and finance managers in India understand this because they have never ever experienced or participated in open bond markets. But Raghuram Rajan has and he has the experience, knowledge & authority to begin this process. Unfortunately, Governor Rajan has shown no drive to build bond markets in India. He seems content to address cyclical problems rather than build a secular, structurally strong, market-driven financial infrastructure that will live on long after he leaves. That is a tragedy for India and will be regarded as his biggest failure.”

We are absolutely delighted to report that Gov. Rajan is now addressing all the problems we wrote about in our Financial Infrastructure article on March 14, 2015.

This is not a topic for finance professionals only. The issues we wrote about and the solutions Rajan is proposing matter to all Indians:

- It is a basic fact that the growth of an economy depends on the size & growth of the country’s financial system. So broadening financial markets and making them deeper is a prerequisite for healthy growth in an economy.

- Broad and deep bond markets provide greater income and flexibility to individual investors which helps minimize financial repression (forced lower rates for savers) by large banks & financial institutions.

So what we discuss below is critically important to the Indian Economy, to all Indians, and to all investors in India.

1. Bond Market Access for Individual Investors in India

The vast majority of Indians invest their savings in Bank savings accounts or Bank Fixed Deposits. The interest rates offered by the banks on these products are lower than what the Government Bond market offers. But the Government Bond market, so far, has been closed to individual investors in India. This repression might soon be replaced by freedom.

As Live Mint reported, the first monetary policy of 2015-16 announced by Rajan on Tuesday, April 7, 2015

- “proposes to throw open the government bond market to individual investors. … Once the proposal takes effect, they can freely and directly buy and sell over RBI’s bond trading platform, without involving any intermediary … once RBI finalizes the rules, any investor with a linked demat account can probably trade even in a single bond … “

Why is this so beneficial for Indian savers?

- First & foremost, Indian Treasury bills offer higher interest than bank savings accounts or fixed deposits.

- A bank deposit cannot be liquidated at a short notice without some form of penalty, but selling securities in the market costs nothing in penalties.

- Also, income from Fixed Deposits is subject to 30% tax, while that from Treasury bills is taxed at the short-term capital gains tax of 20%.

- The credit quality or safety of Government Treasury bills is much much higher than that of Indian banks, many of which are bloated with non-performing loans.

Indians are smart savers & they will gravitate towards a higher paying, more liquid, and safer Government bond market. We would not be surprised to see 50-100 million Indian investors investing & trading Indian Treasuries in the next few years. What a deep liquid efficient market would that be?

2. Forced Conversion of Bad Debts into Equity

As we wrote in our Macro Risk to the Indian Economy article, the biggest problem for the Indian economy is the mass of non-performing loans on the books of Indian banks. That is a direct result of the lack of a bankruptcy law. This lack allows owners of corporations, also called promoters, to default on loans without any risk to their ownership of “their” companies.

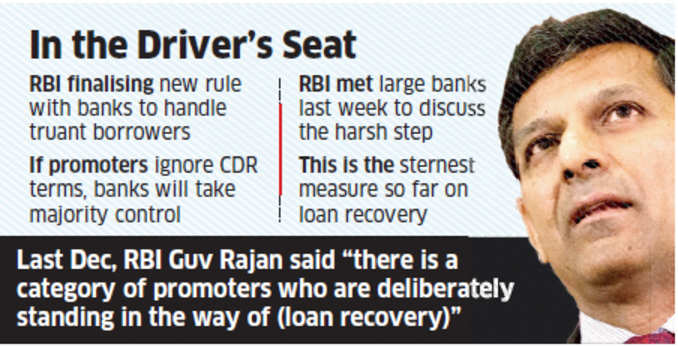

Governor Rajan and Indian banks are getting absolutely fed up with this. And on Monday, June 8, Rajan put forth a harsh new rule they called “strategic debt conversion“. According to the Economic Times of India,

- this rule “automatically give lenders 51% equity control in a company that fails to repay even after its debts are rejigged to give the management a second chance … The rule will kick in irrespective of the amount of outstanding loan and equity stake of the promoter. Thus, even if a promoter, whose shares are pledged with banks, holds 30% equity stake, stocks will be issued to raise lenders’ joint holding in the company to 51%”

- “For instance, even if the unpaid loan amount is as little as .`500 crore (80 million USD), breach of certain pre-agreed covenants would pave the way for lenders to gain 51% control of the equity. Once the CDR covenants are breached, lenders would decide in a month or so whether they would accelerate the process to take control. If banks think there is reason to move in, they would then serve a notice to the company where it would be mentioned that after a certain time, the lenders would become the majority shareholder,” said another banker.”

When put into effect, this rule will essentially eliminate the problem of bad corporate loans that has bedeviled the Indian economy. Owners of Indian corporations have had the luxury of borrowing massive sums of money and failing to pay interest & principal without any risk to their ownership of their companies. That changes with this rule. So, going forward, defaulting “owners” will run serious risk of losing their “ownership” of their companies and then be replaced by another management team brought in by the new “owners”, the Banks.

We cannot overstate the importance of this development, a true reform that could potentially transform how the Indian corporate sector functions.

3. That’s not all – believe it or not

Arundhati Bhattacharya, the Chair of the State Bank of India, publicly urged the Indian Government to expedite the creation of a Commercial Court system with expertise in handling credit default issues. Such a system would make the implementation of the above “Strategic Debt Conversion’ efficient. What is required now, she said “is to enable the banks to work through the legal processes very quickly.”

Foreign exchange risk is one that Indian corporations cannot seem to handle. Past patterns indicate that Indian corporations tend to borrow in foreign currencies when the rates are low and when the foreign currencies are cheaper to the Rupee. A strong rupee and low overseas rates make it alluring to borrow in Dollars. But, more often than not, this backfires because the Rupee weakens relative to the Dollar and what seemed to be a cheap loan becomes a very expensive loan.

This week, the Reserve Bank of India issued draft guidelines to allow Indian companies to sell Rupee-bonds in overseas markets. As Live Mint reported, the rate will be capped at 500 basis points above the equivalent maturity benchmark Indian government bond. For example,

- “the benchmark 5-year government bond yield is now 8.04%. A 500 bps spread above the benchmark means the issuer company can offer as high as 13.04% of coupon to lure overseas investors”

A coupon of 13% for a 5-year paper from a well managed Indian company with a high credit rating? Soft-circle us right now!

Wait a minute. Very few investors will invest in corporate paper without the ability to hedge credit risk via Credit Default Swaps (“CDS”). And trading in CDS is prohibited in India, right? True but so last week. This week’s guidelines enable investors to hedge credit risk in their investments in Indian corporate bonds. This will enable development of a CDS market in India.

Frankly, we can’t restrain our enthusiasm about the above developments. We have been bullish on the transformative potential of the Modi-Rajan team. Prime Minister Modi has already changed the reality of India, strategically & politically. Now Governor Rajan seems poised to change the financial reality of India and usher in an era of financial growth for the long term.

As we have written consistently, the Modi-Rajan duo reminds us of the Reagan-Volcker duo and how they transformed America in the 1980s. The long term macro story of India looks very positive to us.

4. But then, why the Selloff in the Indian stock market?

Our bullishness is rational, never blind. We have been steadfastly positive on the Indian stock market since our article on August 31, 2013. Earlier this year, we noticed an extreme level of bullishness about Indian Stocks. So, on February 28, 2015, we featured a warning from a smart technician about a correction in the Indian stock market. How smart was that technical analyst? The Sensex has dropped by 10% since our article on February 28, 2015 – from 29,220 to 26,425 this Friday.

More than half that drop came in the last 8 trading days. This followed the decision of RBI Governor Rajan to cut interest rates by 25 bps, only 25 bps without any commitment to reduce rates further. We applaud his decision and welcome the drop in the Sensex in the Warren Buffet sense.

This year is very different from the past two years. The biggest difference is the divergence that has opened up between directions in monetary policy in countries. The US Federal Reserve is in a tightening-soon posture while both Europe and Japan have been extremely easy & stimulative. Then China joined the stimulus camp and boom!!!!. The Chinese stock market has exploded in an orgy of a rally. Whatever China does is huge and this year’s rally in China is one for the ages. The European & Japanese markets saw powerful rallies in the first few months of 2015. In contrast, the US stock market is flat in 2015. The world is divided into stimulators & non-stimulators and this division is reflected in global stock markets. India under Governor Rajan is not in the stimulative camp.

Global Macro WE 29th May 2015

This divergence in monetary policy has resulted in massive moves in foreign exchange markets. The Euro and the Yen have suffered unprecedented declines in value.

When elephants fight, foxes dive into holes. Those who don’t, get trampled. Just look at prior emerging market darlings like Brazil & Turkey. Carnage is the word that comes to mind. And remember, the much feared Fed tightening is yet to come. These times call for Sayyam, the Sanskrut word for balanced patience and that is today’s stance of Governor Rajan. We applaud him for that.

The level of the stock market is the sum of the market values of the corporations in the stock market. There is no question that at 29,000, the market value of Indian companies in the Sensex was overvalued. Many sectors of the Indian corporate market are leveraged and groaning under the weight of their loans. So it was appropriate for the Indian Sensex to correct its overvaluation.

Finally, money is always moving. And this year it is moving to markets where the Central Banks are pouring in money. That is not India, thankfully. The overly stimulative policies of Europe, Japan & China are a desperate experiment to cure their economies of the dread of deflation. So pouring in money is their attempt to light the fires of economic growth in their ice-laden economies.

India’s problem has never been deflation. India’s problem is rapid inflation. So reducing rates lower & faster could backfire both on the Indian Rupee and on the Indian people. That doesn’t mean the Rupee won’t fall when the Fed raises interest rates, if the Fed actually does in 2015. But such a fall combined with the Sayyam or balanced patience of Rajan would make Indian stock market cheap again.

When markets change their focus from overly aggressive monetary stimulation to organic growth, Indian market will be one of the attractive choices for global investors. This week one first-tier US investment bank advised investors to move some money from China to India. Sayyam is the word now for India and Gov. Rajan gets it.

This again reminds us of Reagan-Volcker. President Reagan must have become impatient with Chairman Volcker’s hard monetary policy, impatient when Volcker refused to cut rates in the first two years of the Reagan administration. We have no doubt that Finance Minister Jaitley is impatient with the conservative approach of Governor Rajan. We would remind him that Volcker’s hard stance in early years paid off with a multi-decade bull market in America. And President Reagan got elected with a massive mandate in 1984 with a simple message “Are you better off than you were four years ago?”

Given the enormously important steps Rajan is taking in reforming India’s financial infrastructure and given the balanced patience Rajan is displaying in monetary policy, we think a multi-decade bull market could rise in India. And, Prime Minister Modi will get reelected in 2019 with a simple Reagan-like question to the Indian people “Aaj ke din acche hai ki 5 saal purane?” – “Are these days better than those 5 years ago?“

Now, Governor Rajan, get your plans implemented.