Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.“They have no clue“

said Ellen Zentner of Morgan Stanley in her conversation with BTV’s Tom Keene about the next hike in rates. Clearly no one needs to be told who “they” are. Following Ms. Zenter & instead of using the first letter of their name, today we will follow the “name that is not be mentioned” dictum of the late Mark Haynes of CNBC.

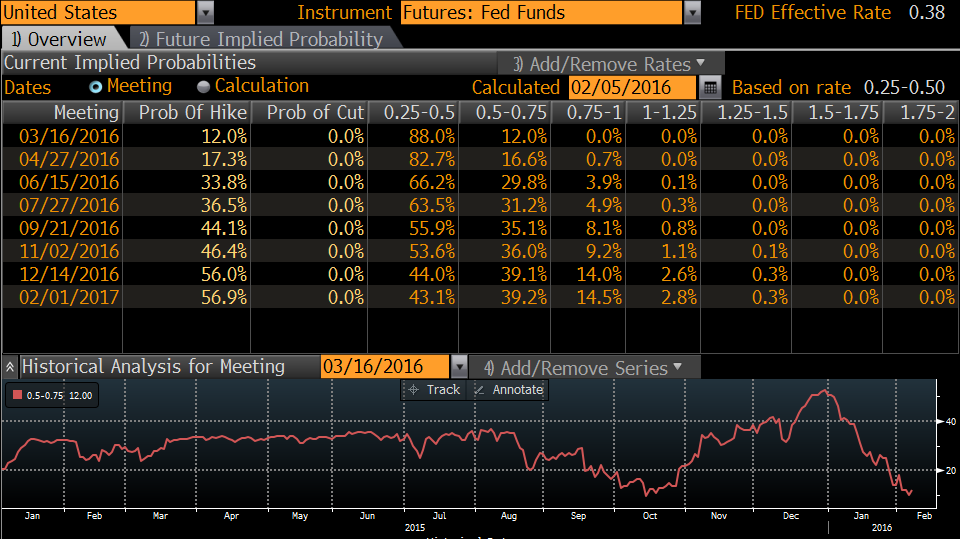

Last week, we asked Art Cashin to proclaim “0% before 1/2%” as an update to his obsolete “0% before 1%” proclamation. He should because he was with us in dismissing the “tapering is not tightening” nonsense “they” were propagating in 2013 and in early 2014. A few weeks ago, Jeffrey Gundlach pointed out the shadow Federal Funds rate at the peak of QE4ever was -3%. So the ending of QE & the last hike in 25 bps has meant a cumulative tightening of 325 basis points since the end of QE4ever.

Don’t the global markets act just like they should act after a cumulative 325 basis point rate hike campaign? They sure do. That is why even “they” are coming around to questioning their own commitment to raise rates further. But, as we are told, “they” really want to raise rates a couple of more times just to feel good about themselves. Markets are not built to gauge feelings. That is why the markets may be so volatile these days, especially on days when data lends differing interpretations.

Look how quickly the sentiment turns. On this Thursday, we saw:

- ValueWalk @valuewalk – Crazy how quickly it changes: Here is the likelihood of a March hike via @SoberLook

One day later on Friday after a ho-hum NFP number of 151,000, the 10-2 year Treasury spread flattened by 3.5 bps, a clear sign of some tightening and:

- Charlie Bilello, CMT @MktOutperform – Fed hike expectations: moved from Aug ’17 to Dec ’16 after the payroll report.

What is important is the direction of the movement & not the scale. And that movement is simply to fulfill the necessity to feel good that “they” have.

We all know what happens near the end of the rate hiking cycle – the good ones, the previously strong ones get pummeled & dragged to the same woodshed where their weaker, lower quality brethren had been dragged before. That’s why McDonald’s and Starbucks were down nearly 5% on Friday despite their recent earnings strength.

TV networks know how to make Donald Trump feel good – publish a survey that shows him with a big lead. So can Fin TV arrange a survey that shows a big majority approving “their” performance? If that makes them feel good, then may be the markets can relax.

- Bloomberg View

@BV – Global indicators point to Fed rate reversal. http://bv.ms/1PoXGd5

2.Recession-Smrecession

- David Rosenberg on Friday – Recession? What Recession? – The headline unemployment rate gripped a “four-handle” for the first time in eight years and did so with the participation rate climbing to 62.7% from 62.6%

On the other hand,

- Tomi Kilgore @TomiKilgore – That ‘recession’ word is starting to trend among Wall Street strategists http://on.mktw.net/1Px8RE7

And,

Hedgeye provided a “causal not coincident” indicator that has portended a recession before:

And an indicator that is new to us:

- ForexLive @ForexLive – This is an economic indicator you never hear about (and it’s sending a warning sign) http://bit.ly/1SvZaZa

3. Treasuries

The action in US financials was horrific on Wednesday morning. Nomura had been semi-literally broken up the night before in Tokyo and worries about European financials were rampant. Interest rates were plunging and TLT was running up to $130, the level it reached in the morning of the August 24, 2015 flash crash. When that subsided, we felt what the tweet below said on Wednesday late morning:

- Igor Des @Copernicus2013 – Feels like we saw a blow off top in bonds this morning and with higher oil and lower usd bonds can get creamed into the close $ZB_F

The Dow closed up on Wednesday some 370 points from its intra-day low and bonds did sell off by about 2% or so. But they rallied some on Thursday and backed off some after the NFP number on Friday morning. Then they caught a strong bid on Friday afternoon closing the week up 1.3% on TLT and down 7-8 bps across the 30-5 year curve. And the 30-2, 10-2 & even the 5-2 year Treasury curves flattened on Friday.

- J.C. Parets @allstarcharts – Junk bonds continue to get smoked relative to Treasury bonds. Excellent trend. Should continue to 08 low $HYG $TLT

4. Gold

The best asset class of the week was Gold & Gold miners. Both GLD & SLV were up 5% on the week and GDX & NEM were up 19% & 22% resp. By Thursday morning, the two week performance line of NEM had become nearly vertical and its RSI touched 80. That seemed like an invitation to sell NEM & GDX. That action looked just fine because by Thursday afternoon NEM had fallen almost 7-8% from morning’s high. The action in GLD, GDX & NEM was slightly negative after the NFP number on Friday. But then NEM, GDX & GLD went on a tear on Friday afternoon with NEM & GDX closing up 4% on Friday. In the last two weeks, NEM has rallied by 44%. Will this continue?

Yes, in a relative way argues:

- J.C. Parets

@allstarcharts – Gold looks just about ready to breakout relative to S&Ps. Interesting developments in gold this year$GC_F$GLD$SPY

But what about the absolute performance of gold? A Bearish view argues:

- Tom McClellan @McClellanOsc – GLD Assets Show Resurgent Interest in Gold by http://www.mcoscillator.com/

learning_center/weekly_chart/ gld_assets_show_resurgent_ interest_in_gold/ …

- And when there is a big surge into GLD, as we have been seeing over the past 2 weeks, it is a sign that there is huge bullish interest, a phenomenon which typically happens as gold prices are topping. … The current reading for this rate of change indicator is not the highest ever, but it is higher than all of the other recent readings except for the big blowoff in late January 2015. So we are seeing now a sentiment condition consistent with important tops in gold prices

- Mark Arbeter, CMT @MarkArbeter – $GLD overbought in a bear market, at TL resistance, with unsustainable parabolic slope. We’ve seen this before.

- Charlie Bilello, CMT @MktOutperform – Gold Miners First close above 200-day moving avg since last Feb One of the most hated assets in the world $GDX

- Peter Brandt

@PeterLBrandt – Thursday – For my friends in India — Metals in short term bull phase. See report here. http://goo.gl/QQGxyj$SI_F$GLD - If Gold can rally to 1180 to 1190, it will be the first constructive daily chart configuration to reach its target in several years.

A more detailed comment:

- ForexLive

@ForexLive – Gold trades at the highest level since October 2015 today http://technical-analysis.forexlive.com/!/gold-trades-at-the-highest-level-since-october-2015-today-20160205 … - A move above that level will next target the 1177 area which is the 50% of the move down from the March 2015 high. The price last week based against the 100 day MA (blue line in the chart below before heading higher) This week, the 200 week MA was broken (green line in the chart below). That MA currently comes in at 1130.46. The last time the price was above the 200 day MA was back in October. That MA represents a risk level for those who are long now. Stay above and get above the topside trend line will have more traders looking for the either safety of Gold or since rates are low and even below 0% in some countries, a store of value.

What about Silver?

- Peter Brandt

@PeterLBrandt – Thursday – $GC_F$GLD$SI_F$SLV Gold/Silver ratio near historic lows.

5. “Tremendous Revulsion“

They say pain is the progenitor of poetry. We saw a glimpse of that in Jim Cramer on Friday afternoon. He was poetically eloquent first with phrases like “streams of ethereal revenue” and then saying – “I think there is a tremendous revulsion for the asset class we spend so much time on“. Cramer is right. We don’t know about revulsion but it is clear that investors are rejecting the TINA-based mandate to own stocks, TINA being the dictum “There Is No Alternative” to stocks.

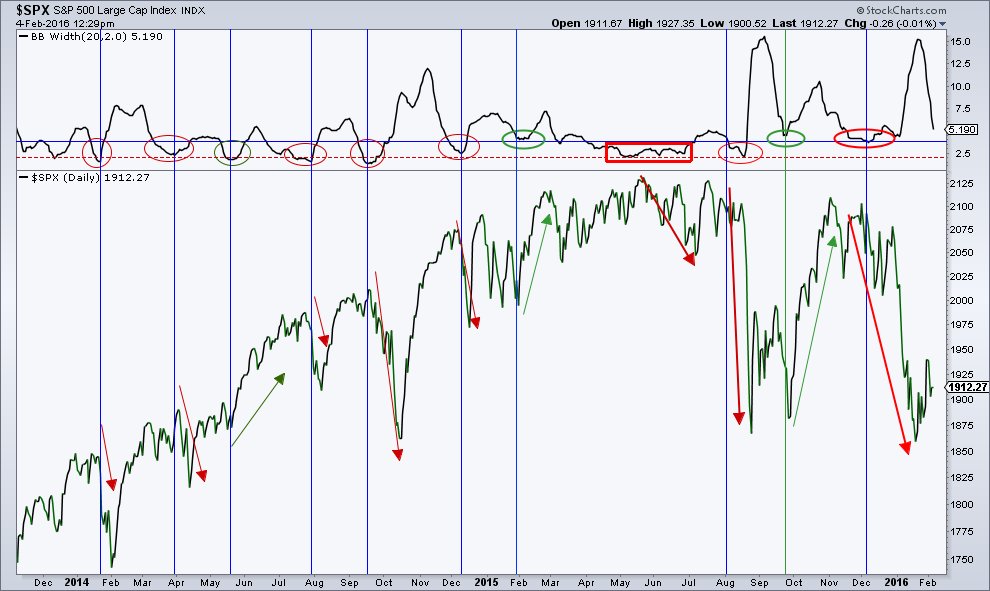

The Friday sell off has positioned the S&P 500 back in the neighborhood of 1867-1870.

- Mark Arbeter, CMT

@MarkArbeter –$SPY,$SPX I guess this area is important.

What do they say about repeated tests of a level? That it tends to give way? And what may happen if this area is broken to the downside? Then we get a retest of 1812, the intra-day low of January, according to both Art Cashin & Steve Grasso. If that retest fails, we could see 1600 next. But if it holds the 1867 level, will we get another short term bounce or a major move up?

One argument says the move will be large regardless of the direction:

- Mark Arbeter, CMT @MarkArbeter – Bollinger Bands constricting rapidly on $SPY, $SPX. Getting near levels that have produced some minor to major moves

The biggest events of next week, events that could overshadow & invalidate all this technical stuff – Chair Yellen delivers her annual Humphrey-Hawkins testimony to the Congress on Wednesday & Thursday. And Chancellor Merkel also speaks on Wednesday & Thursday.

6. 2000-2007/8-2016 parallels

Can you really discuss any intermediate term outlook for the stock market without bringing up 2000 & 2007-2008? Not if you follow the folks we do.

- Steve Burns

@SJosephBurns –$QQQ being down 3.25% in a day is so March 2000ish.

On a more detailed level:

- Chris Kimble @KimbleCharting – S&P could reach 1,600 if this gives way, says Joe Friday http://bit.ly/1SPGsu0

- S&P 500 tops in 2000 and 2007 took place 91 one months apart. Did another top take place 91 months after the 2007 top. So far it looks very possible.

- If you double that time frame, you get 182 months. What is the odds that the NDX 100 topped 182 months after the 2000 high, at the SAME price it hit in 2000?

- We applied monthly momentum to the charts above, reflecting that momentum for the S&P is back at 2000 and 2007 highs and turning lower and the momentum for the NDX is back at 2000 levels.

The conclusion:

- “Joe Friday Just The Fact…Both indices have traded sideways the over the past year plus. If support gives way of this sideways chop, the S&P 500 could find itself testing the 1,600 level. Sideways support is the key, which is still in play”

- “If history repeats itself, I could see us getting as low as 1,680 in the S&P,” the former head of cross-asset management for Wells Fargo said. That’s 11 percent lower than where the S&P 500 was trading on Tuesday and 21 percent from its May high”

- “His analysis found that prior to the market highs in 2015, breadth had climbed upward for a period of 320 weeks. In the last bull run, the market rallied for 323 weeks from the secular lows in 2000 to the highs in April and October 2007. Following that advance, there were roughly 92 weeks of declines.”

- “As a result, Bensignor is calling for caution. “Over [this current period] of 92 weeks, if the market in any way duplicates the type of breadth sell-off that we saw from 2007 to 2009, it puts the entire year of 2016 as an equal to bearish [market].”

- “On the Street, when people say ‘things are different this time,’ they rarely are. History often does repeat itself, and this is too similar a type of pattern to just think that there isn’t any negativity still to come.”

Before we get to the intermediate term, we have next week. And that begins with

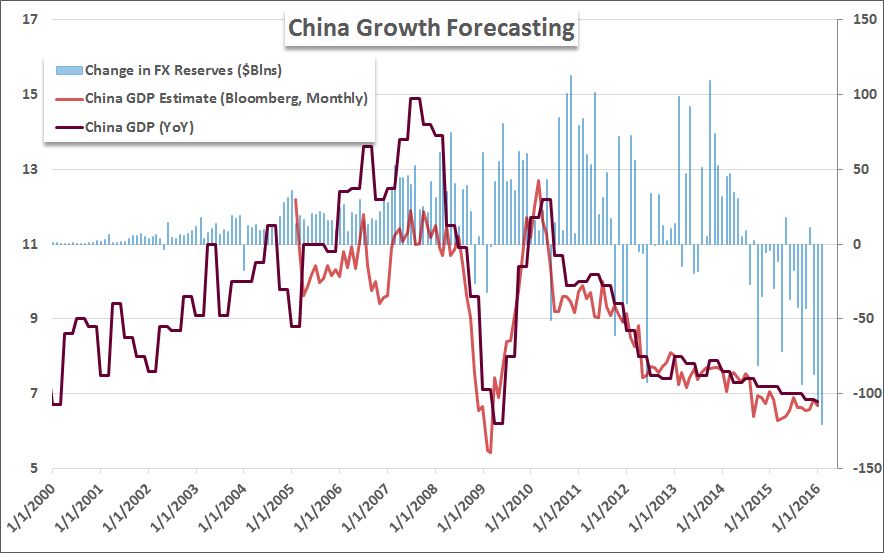

7. China

The growth in China has become a secondary factor of concern. Markets are more focused on China’s FX reserves.

- John Kicklighter

@JohnKicklighter – The Chinese FX reserves figures for Jan are due Sunday (no time). If the forecast is correct, this is the change

If the reserves number comes in better than expected, then we could see a global rally. If not, hmmm. That is of course assuming the number is real and not made up. Chinese markets have a holiday next week. So one worry is they devalue their currency while their own markets are closed. If that happens, then forget about technical levels.

8. EM

The fundamental story looks really bad especially as summarized in the FT article:

- michael mackenzie

@michaellachlan – Lending to emerging markets comes to halt: http://on.ft.com/1nSfwP2#FT

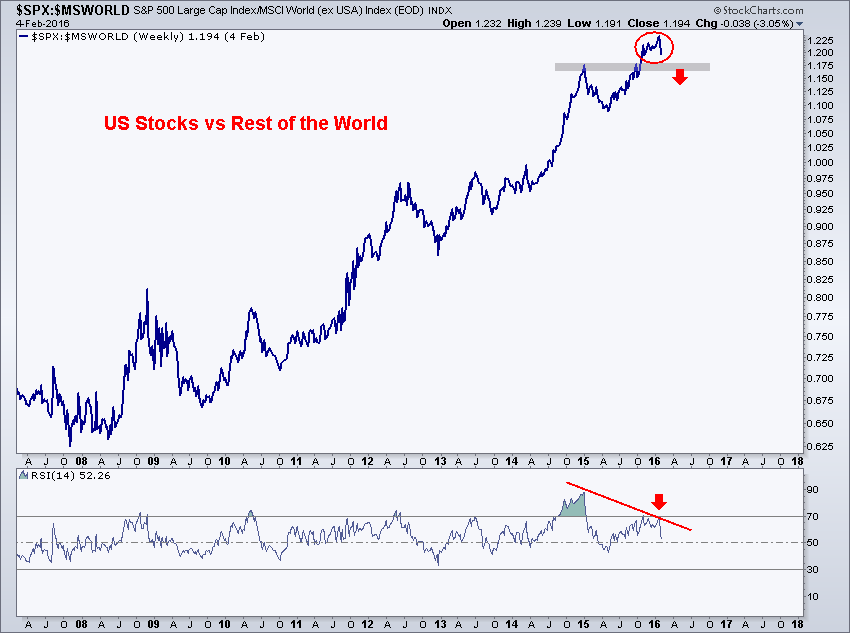

When faced with such fundamentals, who would suggest outperformance of EM over S&P 500? J. C. Parets did last week in his article Why Emerging Markets Will Outperform U.S. Stocks? And EEM did outperform S&P 500 as well as NDX & COMP. This week Parets broadened his call in his article Why US Stocks Will Now Underperform The Rest of the World?

- One of the strongest and most impressive trends over the past 8 years has been the fierce and dramatic outperformance of the United States Stock Market over everyone else. … But the weight of the evidence is suggesting that this is all about to change.

- The Chart of the Week represents the S&P500 vs the MSCI World (Ex-USA) Index. What I see is an exhaustion of trend accompanied by a nasty bearish divergence in momentum. … I think this divergence will be the catalyst to send US Stocks tumbling relative to the rest of the world:

- The way to execute is for every dollar long $ACWX, we are short one dollar worth of $SPY. I think this one has a long way to go and would be aggressively short this spread

9. Oilmageddon

This word is not our creation. Apparently it was coined by Citi Strategist Jonathan Stubbs. The title of the CNBC article that reviewed his work is not for the faint of heart – World Economy Trapped in Death Spiral.

- “The world appears to be trapped in a circular reference death spiral,” Citi strategists led by Jonathan Stubbs said in a report on Thursday.

- “Stronger U.S. dollar, weaker oil/commodity prices, weaker world trade/petrodollar liquidity, weaker EM (and global growth)… and repeat. Ad infinitum, this would lead to Oilmageddon, a ‘significant and synchronized’ global recession and a proper modern-day equity bear market.”

- “The death spiral is in nobody’s interest. Rational behavior, most likely, will prevail,” he said in the report.

- “This is fundamental to avoiding a proper/full global recession and dangerous disorder across financial markets. The stakes are high, perhaps higher than they have ever been in the post-World War II era,” he said.

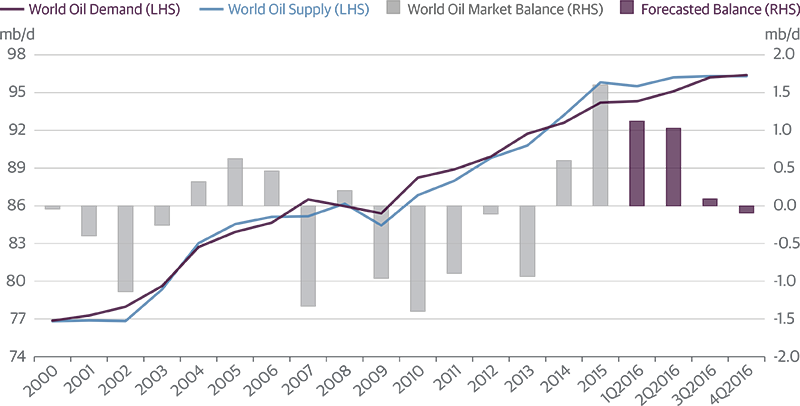

There can be another End Game for Oil. That could come from the claim from Guggenheim Partners that World Oil Supply/Demand Should Balance in 2016.

Send your feedback to [email protected] Or @MacroViewpoints on Twitter