Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.When Governments Panic ….

The biggest stunner of this week or perhaps this year was the sudden & decisive dovish turn of the Federal Reserve. After steadfastly holding to the prospect of 4 potential rate hikes this year, Chair Yellen, suddenly & without any prior signals that have been the hall mark of the Fed since Bernanke, dropped this number from 4 to 2. This came 4 business days after Draghi went farther than what markets had expected & priced in. And Yellen’s stunner came despite the visible increase of inflation this week.

- Charlie Bilello, CMT

@MktOutperform – Rising Inflation Expectations 2-Yr: 1.62% (highest since Jul ’14) 5-Yr: 1.53% (highest since Jul ’15) 10-Yr: 1.63%

So what made Chair Yellen perform such a u-turn and stun the markets? Yields across the 2-5 year Treasury curve fell and kept falling until the close of Friday – a fall of 14-18 basis points. The Dollar fell by 1.4%, Gold & Gold Miners exploded and so did stocks – the Dow rallied by 380 points during the 2 & 1/4 days after the Fed stunner. And the 30-5 year yield spread steepened by 9 bps this week, the clearest & loudest statement that the markets consider Yellen’s declaration as unabashedly stimulative.

What gives? We all know that the biggest risk to the global macro environment is the prospect of devaluation by China. Neither US nor Europe want to lose the gains in the markets achieved at the cost of trillions of QE because of turmoil resulting from a Chinese devaluation. So was a deal struck at the recent G20 between China, Europe and the Fed to increase stimulus in the west in exchange for Chinese holding to the current band of the Yuan?

- Mr TopStep @MrTopStep – Did central bankers make a secret deal to drive markets? This rumor says yes –https://mrtopstep.com/did-

central-bankers-make-a-secret- deal-to-drive-markets-this- rumor-says-yes/ …

According to the article:

- Chris Weston, chief market strategist at IG, in a note Friday. “There is a global coordinated central bank effort to weaken the [dollar] in play, which in turn has led to a massive de-risking in equity and credit markets.”

- “Since the G20 meeting in Shanghai there have been many red flags,” noted Weston. “Whether it’s the [People’s Bank of China] easing the Reserve Ratio Requirements (RRR) by 50 basis points, the [Reserve Bank of New Zealand] cutting its cash rate by 25 basis points (very much out of consensus), or the ECB moving to a focus on credit markets and going significantly above and beyond expectations.”

Joachim Fels, an advisor to Pimco, went beyond the “rumor” designation in a Bloomberg article:

- “There seems to be some kind of tacit Shanghai Accord in place, … The agreement is to roughly stabilize the dollar versus the major currencies through appropriate monetary policy action, not through intervention.”

Another school chose to go directly to the intended result – to weaken the currency:

- “In a word: trade. Since the depths of the Great Financial Crisis in 2009, global trade has expanded consistently, quarter-by-quarter, creating an ever-increasing global pie so that each country could see steady growth in international trade. For the first time in seven years though (see below), global trade is showing signs of flattening out, meaning that each country now has to fight harder to secure its same sized piece of the global trade pie. The longer that global trade growth continues to flat-line, the more aggressively central banks will try to devalue their currencies (note we’re not referring to just the value, which can fluctuate with day-to-day currency movements, but the actual volume of trade here).”

Either way, will Chair Yellen actually go thru the 2 Fed rate hikes she mentioned or, as we have argued, is the Fed done for 2016? It seems Art Cashin of the “0% before 1%” forecast came over to our side on Thursday when he said on CNBC SOTS “I think they will be be lucky to raise rates one more time this year – I doubt if they will“.

That fits in what Ellen Zentner of Morgan Stanley said on BTV on Tuesday – “we have already seen the peak for the year – that is a very important point – 1.7% core PCE in January was peak of the year“. And:

- Bloomberg View @BV – The Fed may have to cut rates, not raise them. http://bv.ms/1Ww5PRk

How did global bond markets react to the Fed? The German 30-year yield fell by 17 bps this week & decisively broke thru the 1% support.

- Mr TopStep @MrTopStep – Japan 10-Year Yield Drops to Record, Below Negative Deposit Rate –https://mrtopstep.com/japan-

10-year-yield-drops-to-record- below-negative-deposit-rate/ …

As we write this, CNN is discussing the increasing attacks by President Obama against Donald Trump & that led us a conspiratorial thought – President Obama knows that he became President because of the spectacular bust of the housing bubble & Lehman in the fall of 2008. There is no doubt that he will do everything he can to make sure that global financial markets don’t crash this year. And what could be the most likely cause of a crash? China. Is that why Secretary of Treasury Lew participated actively in the discussions in the G20?

2. U.S. Dollar

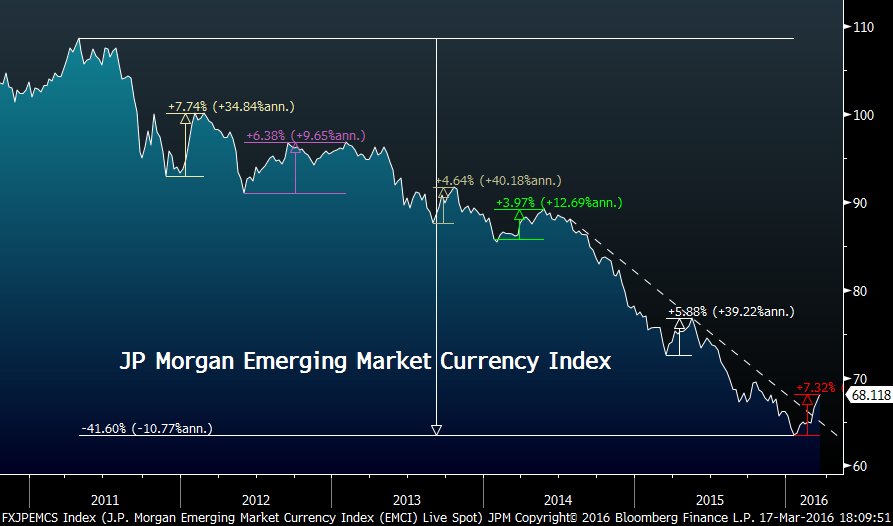

Emerging Markets, commodities and risk assets in general do best when the US Dollar is weak. That is EM rallied so strongly as the Dollar weakened after the Yellen stunner on Wednesday. In fact, the rally in EEM was twice as strong as the rally in the SPY this week. The Dollar has been weak all month and that has meant:

- Charlie Bilello, CMT

@MktOutperform – Strongest rally in EM currencies since ’12. If this has legs marks an important shift in market dynamics/leadership.

Wouldn’t be ironic if Yellen’s stunner actually leads to some sort of a bottom for the U.S. Dollar?

- David Larew

@ThinkTankCharts – US Dollar – Generally you buy at the bottom of the channel and sell at the top of the channel

What if the Dollar does find a bottom and reverses the decline of recent weeks? Will that mean the rally in risk assets will reverse as well? And what assets are most linked to a weak Dollar?

- David Larew

@ThinkTankCharts – Emerging Markets – gravestone Doji today? Possible top?

3. Stocks

A couple of weeks ago, smart veteran technicians and analysts like Tom DeMark and Tom McClellan argued for a reversal in the stock market rally in early March. But, as we have seen since the launch of the first QE, the models of such gurus fail in the face of waves of liquidity injected by central bankers. We saw that last week with Draghi and we saw during the 2 & 1/4 days of this week post-FOMC. But that doesn’t mean everybody likes it:

- Closing Print: Fait Accompli http://northmantrader.com/technical-charts/ …

$DJIA - Fait Accompli. “Bulls got everything. All MA’s reconnected, the January gap filled and markets green for the year. In process $VIX hit its lowest RSI since 2013 and all fear or sense of risk has been removed from markets. All it took was massive central bank intervention, dovish talk & record Fed enabled buybacks. What bulls didn’t get: Expanding earnings or revenues. Per FactSet: “Bottom-up EPS for $SPX for Q1 has declined 9.0% since Dec. 31 and 14.8% over past 26 weeks.” Consequently markets have gotten more expensive. It matters not. For now“:

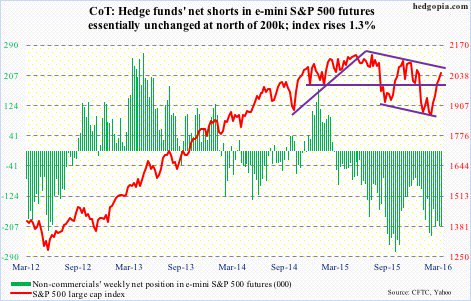

That has been exacerbated because of the low positioning of equity investors:

- hedgopia

@hedgopia –#Hedgefunds‘ net shorts in$SPX futures unch. Holdings as of Tue. Since then, breaks out of 200DMA + 2040. Squeezed?

That is essentially what Marko Kolanovic of JP Morgan said this week about the rally:

- “Kolanovic looks at causation for the market bounce and thinks more could come. A significant point of causation for the previous market rally “was due to systematic investors covering their short positions,” he wrote. “Over the past few days, dealers’ option imbalance was tilted towards calls (long gamma) which forced the market to trade in a tight range. This has reduced realized volatility and attracted some inflows from volatility based allocators such as Volatility Targeting and Risk Parity funds.”

- “Momentum can sometimes beget momentum and create a feedback continuum. The exposure of systematic investors to Equities is not very high and further inflows could materialize if the S&P 500 were to get into a 2050-2100 range, where S&P 500 momentum would turn solidly positive across term structure. … However, in the next week, we could see some downward pressure as the impact of option hedging is reversed.”

How light are positions of large investors?

- Urban Carmel

@ukarlewitz – Most interesting chart from BAML fund mgr survey: allocation to equities very light relative to cash/bonds/etc$spy

So how far can this rally run? To S&P 2200 by summer according to Jim Paulsen of Wells Management and,

- Ralph Acampora CMT @Ralph_Acampora – Russell 2000 is making a higher high; this extends its uptrend that began at its Feb.11th low. Next resistance is in the 1,140/1,200 area.

Greg Harmon of Dragonfly Capital wrote on Friday:

- ” … reflecting back at the end of the week there are a lot of positive things in the SPY chart. It moved over the 200 day SMA this week, and held. A weekly close over that level is a big plus. The Bollinger Bands® have turned higher. This allows the SPY to continue higher without becoming overbought. Momentum is also in favor of more upside price action with both the RSI and MACD rising and bullish”.

- The “W” in the chart that I first noted as building 3 weeks ago, has continued to control the path. And it is closing in on that symmetrical move at about 208. This will likely be a big battle ground for all parties. I have included the broader picture back to August in the chart above to help explain why. There was “W” before. And that “W” ended up being the top as price rolled back lower into the end of the year before starting the current “W”. Sentiment from my unscientific study remains rather bearish. Participants continually describe the current leg higher as a relief or bear market rally. This view will be defended at that 208 level no doubt. How it resolves could set the course of price action for the next 6 to 12 months

Caroline Boroden, a colleague of Jim Cramer, said in February that the double bottom around 1810 was an important bottom and that, in her opinion, the rally could even get to a new high. But such a big move is neither vertical nor uninterrupted. In fact, Boroden sounded a cautionary note on Thursday evening:

- Carolyn Boroden

@Fibonacciqueen –$SPX time symmetry here….tighten up

She spoke about time & price resistance and cautioned “we are getting to extremes where we have to watch for a possible failure”.

That is what Tony Dwyer said this week on CNBC FM 1/2 – “we are entering a period where we can expect a 3-5% pull back- weakness in the $ is a huge deal … with liquidity from ECB Fed etc – can get into a growth based bull market over 12-18 months“

4. Gold

First the near term:

- Chris Kimble

@KimbleCharting – Gold- Dual resistance could be heavy, says Joe Friday http://bit.ly/1Vkkz7B

But,

- David Larew

@ThinkTankCharts – Gold – Symmetrical Triangle – watch for breakout next week – generally it goes the same direction as the Yen

What about the long term?

- Smaulgld @Smaulgld – Buying #gold in 2016 is like buying stocks in 1941 http://on.mktw.net/21yWppB

And where could Gold go according to the MarketWatch article?

- “Right now, I view the pattern in the metals and mining stocks as being analogous to the pattern Elliott saw in the equity markets back in 1941. In fact, if you look at the Gold Bugs Index HUI, +1.17% chart linked at the end of this piece, you will see that our projections are calling for an almost tenfold increase in this index over the next decade or so, which will likely increase to a fiftyfold increase in the index over the next 20 or so years, and well beyond that in 50 years. The HUI has finally struck our ideal correction target in the 100 region, in similar fashion as to the Dow striking its low region of 100 in 1941″.

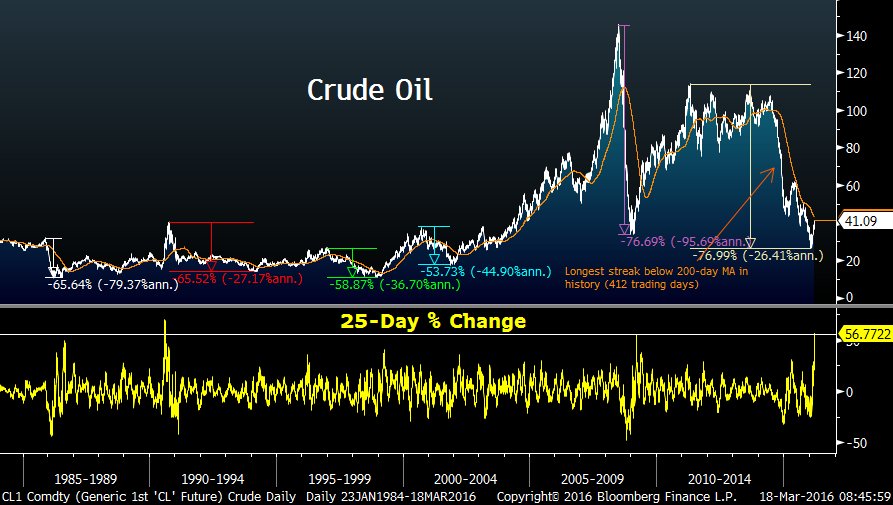

5. Oil.

As Marko Kolanovic wrote “over the past week, oil short-term momentum turned positive (1M and 3M), which led to CTA funds closing most of their shorts“. He added this “one of the most profitable short positions for momentum investing, and we think this trade is over“.

How big was the trade?

- Charlie Bilello, CMT

@MktOutperform – Crude Oil up 57% in the past 25 trading days, largest gain over this time period in history outside of August 1990.

Kolanovic added “We have called for Oil to outperform the S&P 500 this year (YTD it outperformed by ~5%), and we expect this trend to continue, especially in H2“.

But the action on Friday afternoon suggests a reversal in price action of oil, the 1st such since February according to CNBC’s Guy Adami. He added that OVX, the Oil volatility index, bottomed yesterday. That is also the message of :

- David Busick @TheFibDoctor – $CL_F 42.4i = March 17th, 2015 low and still a thorn in crude’s side.

But what about the relationship between Oil & Energy Stocks?

- J.C. Parets

@allstarcharts – Still my favorite energy trade. Long Oil / Short Energy Stocks working well. I think has long way to go$CL_F$USO

Send your feedback to [email protected] Or @MacroViewpoints on Twitter