Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Medicine too strong for bears – “higher than … if Brexit didn’t exist” –

Kevin Warsh, the brash youngish ex-member of the FOMC said on Thursday on CNBC Squawk Box that “financial markets are higher than they would be if Brexit didn’t exist“. He is not just factually correct but also correct in a markets-reality way.

That is what we have seen since Bernanke began administering his medicine years ago. And this week proved once again that his medicine is much much powerful than that of the bears, shorts, technicians & chartists. How powerful? Almost five straight days of new all-time highs in S&P 500 and the Dow. Look what a veteran technician said only two days into the 5-day move this week:

- Mark Arbeter, CMT @MarkArbeter Jul 12 – This slope needs to reset….. one of these days. Unsustainable. Parabolic & Asymptotic! $SPY, $SPX

Of course, all of Arbeter’s fulsome adjectives became more fulsome by Thursday. That is because of expectations of a new dose of Bernanke medicine from Abe-Kuroda by month-end.

Why was this week’s rally so different from the previous week’s including the NFP-led rally on Friday, July 8? After all, the S&P rallied in both these weeks by about 30 handles. Because the yield curve behavior was starkly different. On Friday, July 8, the 10-2 year curve bear-flattened by 5.4 bps and this week the 10-2 curve bear-steepened by 15 bps. Go back to the beginning of the Bernanke medicine and you will see that stocks rally and yield curve bear-steepens when markets smell a believable level of stimulus is coming. And when the markets smell that, EM outperforms, cyclicals outperform and STUB (staples, telecoms, utilities, bonds) loses appeal.

That is what happened this week and that was directly due to Abe winning the super-majority last weekend & Bernanke’s visit to Kuroda presumably to teach him how a helicopter works. That is why all the charts & stuff we featured last week proved worthless on Monday morning. And it worked wonders for Japan with Yen down 4% vs. the Dollar and DXJ, the currency hedged Japan ETF, up 9.5% for the week.

If that wasn’t enough:

- Komal Sri-Kumar

@SriKGlobal –#BOE Chief Eco suggests massive, rapid monetary stimulus. Prepares mkts for lower rate, possibly more#qe at 8/4#MPC mtg#uk#Carney

This is why the snapback from an event-fear induced steep sell off is much steeper & taller than the fall. Steroids of massive central bank stimulus work very well in the short term despite what their long term consequences may be.

2. State of Markets

The hardest fall among asset classes was among sovereign bonds. Both the US & German 30-year yields rose by 18-20 bps. Both the US & German 10-year yields rose by 22-23 bps & closed above important levels, above 0% for 10-year Bund & above 1.57% for the US 10-year. The weekly close of 1.587% could establish a new range between 1.57% & 1.66% according to Rick Santelli. A more visual way to see where Treasuries closed is:

- Dana Lyons

@JLyonsFundMgmt – ChOTD-7/15/16 #1) 10-Year Treasury Yield Testing Breakdown Level To All-Time Low…$TNX$IEF

Stocks did very well this week almost achieving 5 straight days of new highs for the S&P, a feat that hasn’t been seen since March 1998. What does that mean for sentiment?

- Anil @anilvohra69 Jul 14 – CNN Fear & Greed at 90 right now (intraday)

- Chad Gassaway, CMT

@WildcatTrader – SPX DSI rose to 87 today.

and

- Andrew Thrasher, CMT @AndrewThrasher – Appears the Volatility Index will see its lowest close since August ’15 $VIX

But what about next week?

- Ryan Detrick, CMT

@RyanDetrick – S&P 500 up >1% 3 straight wks. Looking for big dip next wk? Past 5 times the next wk: +1.1% -0.7% -1.1% +2.1% +3.8% Big pullback unlikely

Resource EM outperformed S&P despite the big rally for the S&P – EWZ up 5% & EEM up 3.5% vs. 1.5% for S&P. Not only did EEM outperform, but it closed the week tantalizingly.

- Al Sabogal

@alsabogal –$EEM vs$SPY potentially ready to break 6yr bear channel

3. Economy

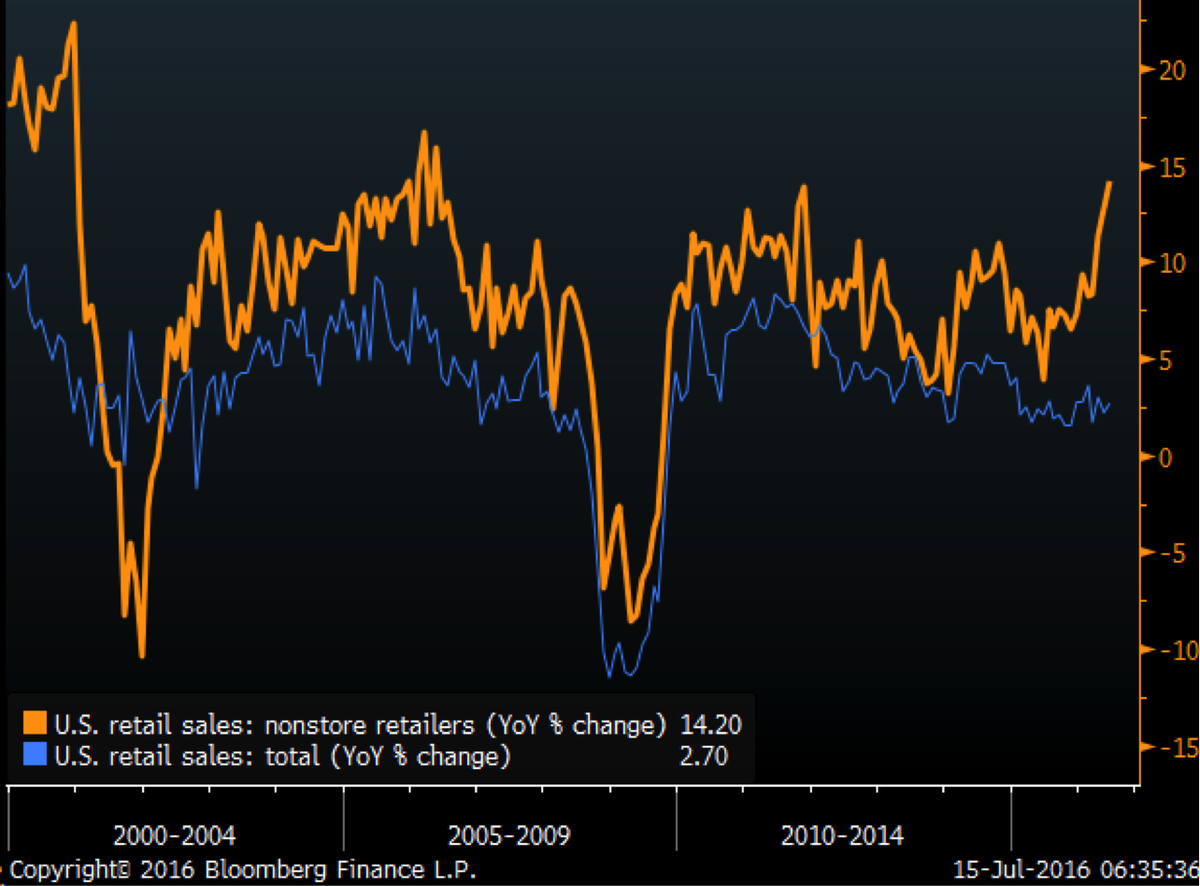

Tony Dwyer, the bullish strategist, said this week – “leading indicators over last 6 months are ramping; US data is way better“. His view was supported by retail sales:

- Matthew B @boes_ – U.S. nonstore retail sales grew at the fastest pace in the 12 months through June since 2006

But what about the question raised by David Rosenberg on Thursday?

- If the U.S. economy is so solid, why are personal income taxes down 11.3% YoY as of June, and negative in two of the past three months?

But we wouldn’t know what the economy is really doing until the next payroll number, would we? Until then, US economic data is a tailwind, expectations of helicopter money from Kuroda and a big stimulus from BoE are major tailwinds. And then you have the declaration by Dana Lyons that The month of July has never played host to a major stock market top.

All of a sudden, this feels like July 2012, doesn’t it? Or is that too pat for a world where anything can happen & where valuations are way high? How high? Even Larry Fink said on Thursday on CNBC Squawk box – “I don’t think we have enough evidence to justify these levels in the stock market at the moment“.

That is not a negative or bearish statement if earnings are at a cyclical trough & will rebound from “these levels“, right? Rich Bernstein has been in print stating that we are at a cyclical trough in profits & there is a recovery coming. Tony Dwyer went a step better and said “earnings are better than we thought they would be“.

And regarding anything can happen in our world? The attempted coup in Turkey that riveted us to TV sets on Friday night went poof over night. So how do emerging markets open on Monday? In concern or with another snap back from Friday’s concern?

Send your feedback to [email protected] Or @MacroViewpoints on Twitter