Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Bond Selloff

Nothing has been as material in markets as the steep & hard rise in German & Treasury yields. Last week’s divergence in the bear steepening of the 2-10 year curve vs. the flattening of the 10-30 year curve was resolved this week. The 30-year Treasury yield rose 10 bps this week outperforming the 8 bps rise in 10-year yield, 6 bps rise in 5-year yield & a mere 1 bps rise in the 2-year yield.

- Mark Newton@MarkNewton – 2s/10s have escalated pretty rapidly but we’re JUST seeing initial steepening out of 5/30, and 10/30s curves, 10/30 reversal shown here.

There is no evidence of inflation. So is this rise in 30-year yield more about positioning?

- David Rosenberg – Well, many pundits [guess he means pandits] are focusing on the spasm in global bond yields as something fundamental and long-lasting but instead it is about shifts in market positioning and central bank expectations

Is that why the 2-year yield stopped going up this week?

- SentimenTraderVerified account @sentimentrader When “smart money” hedgers get massively long 2-year Treasuries, cash substitutes tend to do well. They’re now record long.

Last week, Jeff Gundlach warned about the 2.32% level in 10-year yield & 0.50% level in 10-year German Bunds. These were blown past this week. What key levels did he identify on Friday?

- Jeffrey GundlachVerified account @TruthGundlach Big levels nearby for 10/30 US Tsys. Closes above 2.42 /2.95, respectively, flash bearish. Best news is sell-off stall of 2 yr. Levels hold?

This is a far less bearish tweet than Gundlach’s tweets of Friday June 30. If this selloff is more about positioning, then is the below significant?

- zerohedge @zerohedge – July 5 – Morgan Treasury Client Shorts Highest This Year. So the squeeze is next

What are the big options players doing in TLT? Jon Najarian of CNBC FM said on Friday halftime – “lots of puts bought in TBT [double-short TLT] today“.

With all this, was there any one bold enough to say Buy long Treasuries? Carter Worth, resident technician of CNBC Options Action, was bold enough to do so on Wednesday, July 5. Except he was early. The 30-year yield dropped another 7 bps during the two days following his recommendation.

Carter Worth also predicted outperformance of XLU, the S&P Utilities ETF, in the above clip. That seems statistically consistent per,

- Urban Carmel @ukarlewitz – –

$XLU down 10 of the last 11 days. Down 12 of 13 days in October before a 5% rally

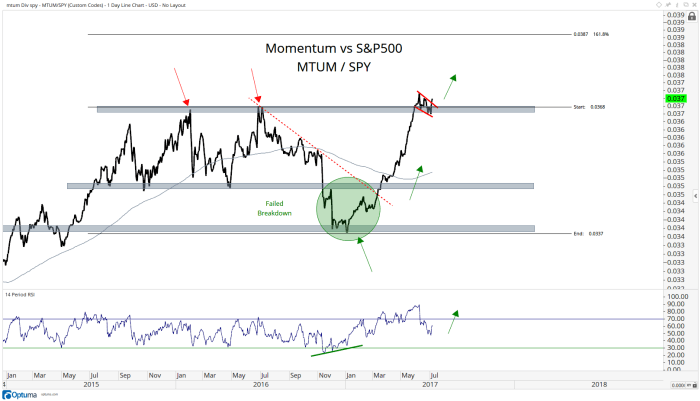

2. Et Tu Momentum?

It is a well established empirical tenet that Nasdaq PEs are inversely correlated to Treasury interest rates. So if the gurus above are right & yields fall some, then shouldn’t high beta Nasdaq stocks outperform? J C Parets not only seems to think so but he applied this argument to Momentum stocks as a whole in his Chart of the Week.

- The first chart is the one I’m referring where Momentum Stocks are breaking out relative to the S&P500. This ratio approached the former highs from last year in late May. Since then, we’ve seen a 6-week sideways consolidation that appears to be resolving higher. This is a bullish characteristic, not a bearish one. If this ratio is above the upper of these two parallel trendlines we need to err on the bullish side of Momentum, particularly compared with the rest of the market.

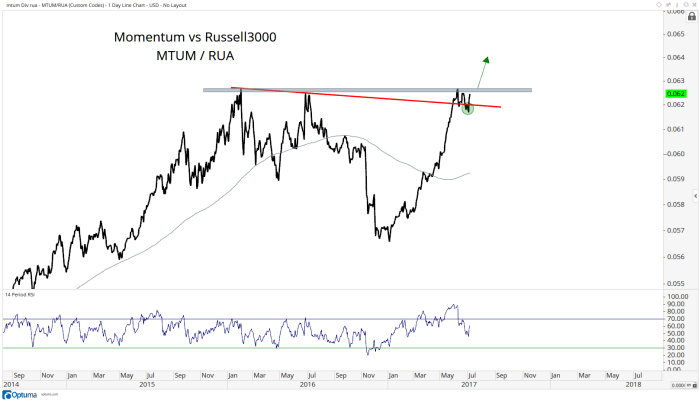

- I find it helpful to compare Momentum stocks to the Russell3000, which represents approximately 98% of all investable assets in the US equities market. This to me has upside resolution written all over it as well.

- These Momentum stocks can really have a run here in the summer based on what we’re seeing. I think this bodes well for the overall market as Banks are an integral piece of this index. If Banks are ripping and outperforming the market, I find it difficult to see it taking place within the context of a steep decline for the overall market. I believe that these developments bigger picture are another feather in the hat for the U.S. stock market bulls

3. Transports

The best performing Dow index of the week was Dow Transports. Isn’t that a big deal, a clear signal about the economy & the broad market?

- J.C. Parets @allstarcharts – Dow Jones Transportation Average going out at new all-time weekly closing highs, just like last week. This is becoming a trend….

$DJT$IYT

Not quite per,

- Charlie BilelloVerified account @charliebilello – Tall Tales and Transports. NEW POST on the myth of the all-powerful Transportation Index.

$IYT$TRAN

Their article Tall Tales & Transports points out:

- there’s nothing in the data to suggest that Transports hitting new highs are an unusually bullish signal. And as we saw in 2001, 2008, and 2011, there’s nothing to suggest that sharp declines can be ruled out when Transports are strong. To the contrary, the last 3 bear markets all saw Transports hitting new all-time highs just prior to the steepest losses.

What happened in those cases?

- Back in July 2011, we heard the same fable from a renowned pundit. Transports were hitting new highs with the S&P 500 still below its peak in April. “Bullish,” he said. What followed? A sharp sell-off and 20% decline until a bottom was hit in October.

- I can still recall the days in early June 2008 when the Transports rallied to hit new highs. “The Bear Market is over,” I remember one so-called “Technician” declare without an ounce of reservation. What followed? The worst declines since the Great Depression, in a bear market that took the S&P 500 down 57% before bottoming in March 2009.

- In January 2001, the Transports hit a new all-time high, leading many to say that the broad market declines which began in March 2000 were over. What followed? The sharpest losses bear market that took the S&P 500 down 51% before bottoming in October 2002.

4. Commodities

- Mark Newton @MarkNewtonCMT – Dollar/Yen breaking out, something that historically has correlated fairly positively to S&P at R=.43 over last 2 yrs, while -0.70 to

#GOLD

Now he tells us, after gold fell 2.3% this week & after GDX & GDXJ, Gold Miner ETFs fell 4.1% & 6.5% resp. And the worst might be ahead for GDXJ per,

- J.C. Parets @allstarcharts – July 6 – Junior Gold Miners breaking a 2-month uptrend line that defined a counter-trend rally within an ongoing structural downtrend $GDXJ

If Gold fell this hard, Silver must have collapsed!

- Joe Weisenthal @TheStalwart – Silver fell below the flash crash lows https://www.bloomberg.com/news/articles/2017-07-07/silver-leads-gold-lower-as-bond-yield-gains-bash-metals-allure …

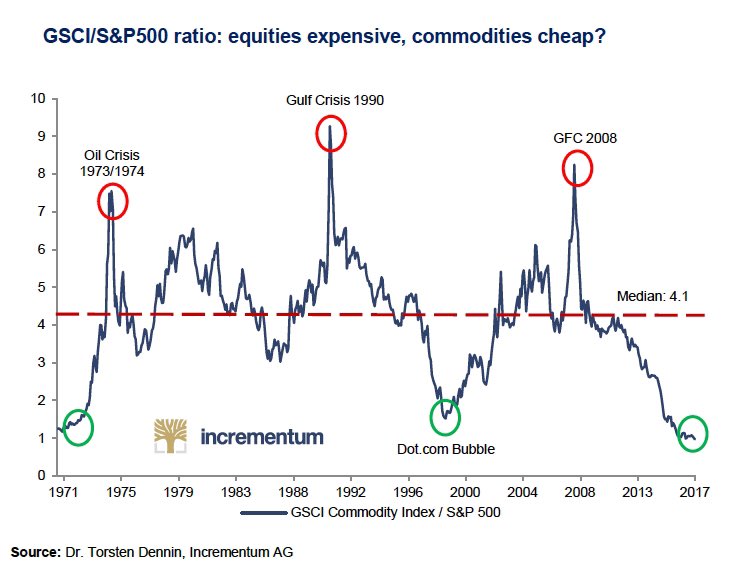

Forget Gold & Silver. What about Oil? You know what! Down 4% this week after a big rally last week. Why? We haven’t found any one who has a clue.

So is there any hope for this asset class? One glimmer could be seen from the chart below:

- Jesse Felder @jessefelder – July 7 – Over the past 45 years commodities have not been cheaper relative to equities than they are today http://www.visualcapitalist.com/commodities-h1-2017-cheap/ …

5. Jewish Beauty Queens – an Untold Story

We found this story by accident and actually thanks to this week’s psychologically rewarding visit to Israel of India’s Prime Minister Modi (pronounced as Mo-thee except by the not knowing & the knowingly uncaring like some Fin TV anchors). It is a filmmaker’s journey to uncover the story of Jews in Bollywood. We knew some of it but not as much as revealed in this article on the website My Jewish Learning:

- Fourthly, while in Hollywood, Jews were behind the camera and used cinema as a vehicle to assimilate, in India not only were these Jewish stars front and center on screen, but they openly identified as Jews. They attended synagogue, gave to Jewish charities and filled their homes with Judaica.

- Fifthly, anti-Semitism was not part of the Indian experience – yes it’s true, there is a country without anti-Semitism. In fact, in their personal lives, these Jewish stars were friends with, and even married, Muslims and coexisted happily. Boy, was this a refreshing story.

Ms. Ezekiel, better known as her screen name Nadira, is reputed to be the first vamp of Bollywood. She was so successful that she was the first Indian actress (of any religion or background) to own a Rolls Royce. We knew her mainly for her role in Shree 420, one of the most iconic films in Bollywood, in which she persuades a bright young man to leave his girlfriend to join her network of corporate larceny.

[embedyt] http://www.youtube.com/watch?v=Ci6OfLH6Ogo[/embedyt]

The readership of our articles does include some affluent Jewish investors who probably know even more affluent Jewish people. Perhaps, they could circulate the appeal of the filmmaker, Danny Ben-Moshe within their network:

- While I had a great story it was hard to get it commissioned i.e. funded. As I pitched it to broadcasters I was told it was either too Jewish, or too Indian, or too historical, or not historical enough. So, for several years, between making other films, I incrementally put the pieces of Shalom Bollywood together. Now 11 years on the film is almost finished. I am still raising money and invite you to contribute. I can’t wait to finish the film so that the story of Jews and Bollywood can finally be told.

Send your feedback to [email protected] Or @Macro Viewpoints on Twitter