Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Three Strikes – Three +ve Signs

Remember our excerpt of last week from last Friday’s summary from Larry McMillan of Option Strategist:

- “In summary, the market is at a crucial point right now. If $SPX can close above 2750 and $VIX can close below 17, that would be an all-clear sign for the upside, in my opinion.”

Both of his conditions were met the next trading day, Monday February 26. On that day, the S&P closed at 2779.60, well above 2750 and the VIX closed at 15.86 well below 17. Unfortunately, it was not an all-clear sign for upside. In fact, it marked the top for the week and the S&P closed 89 handles lower at 2691 at the end of week.

Why? Because as we all know, nothing matters as the Fed. And the new Fed Chairman, Jay Powell, spoke softly but clearly on Tuesday in his Congressional testimony. That was strike one.

That very afternoon came the surprising declaration from GOP leadership that the infrastructure bill was as good as shelved for this year. That took stocks lower fast – strike two.

The fear about what Chairman Powell would say in day two of his testimony on Thursday showed up in a hard decline on Wednesday afternoon. That should have been a buying opportunity on Thursday morning because, speaking empirically, day two of Fed Chair testimony usually reverses the market action on day one. Chairman Powell was indeed more dovish and that sparked a rally on Thursday morning until the axe fell. The news that President Trump was going to announce trade tariffs took the rally down. The actual announcement was harder than expected and stocks fell very hard & very fast – strike 3.

But instead of going out, we saw a fast rally into the close raising expectations of the worst being over. Then came overnight Thursday, Friday pre-open and the open. The Dow was down 390 points but it wasn’t an out call. Because as, Jon Najarian of CNBC FM pointed out at noon, that VIX, that shot to 50 in early morning, was sold via puts. And VIX coming down prompted a rally in stocks that actually accelerated a bit into the close.

The Trump tariffs dominated Friday morning and had an “impact emotionally“, to use the words of Larry McDonald of Bear Traps Report. But , as he added, ” for it to be contagious …, we need retaliation“. That was also the opinion of Jim Cramer who said in his Friday show that whether the market opens down or upon on Monday depends on whether we see a retaliation over the weekend from some country.

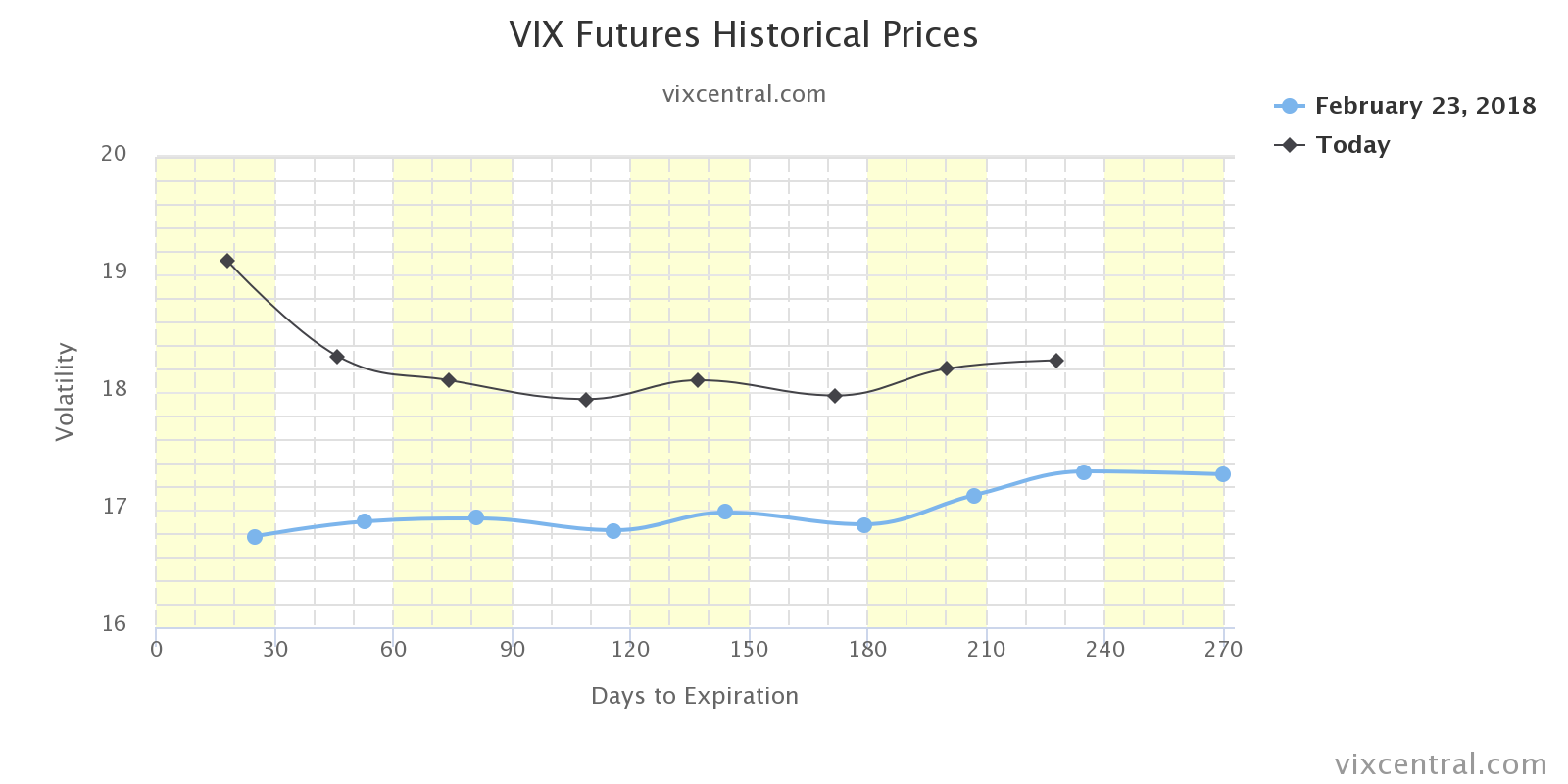

Barring the retaliation possibility, there are three positive signs for Monday. First the VIX curve is now inverted from March into June, a big change from Friday, February 23:

Second is the bullish divergence on Friday between Dow (down 29 bps), SPX (up 51 bps) and Nasdaq 100 (up 90 bps), Russell Small Caps (up 1.71%) & Micro Caps (up 2.04%). So does any have a target for Monday?

- Peter Ghostine @PeterGhostine – I’m looking for

$SPY to bounce back to 272.50 by Monday.

And, third as a proof that technicians can also have a sense of humor and appreciation for media signals:

- Chris Kimble @KimbleCharting – Markets often close to short-term Lowe’s when CNBC ask Ron to come on TV

Actually Mr. Insana made a second appearance on CNBC on Friday afternoon. Wouldn’t it be nice if a double Insana appearance doubled the strength of the signal?

2. Wax (not eloquent) on VIX

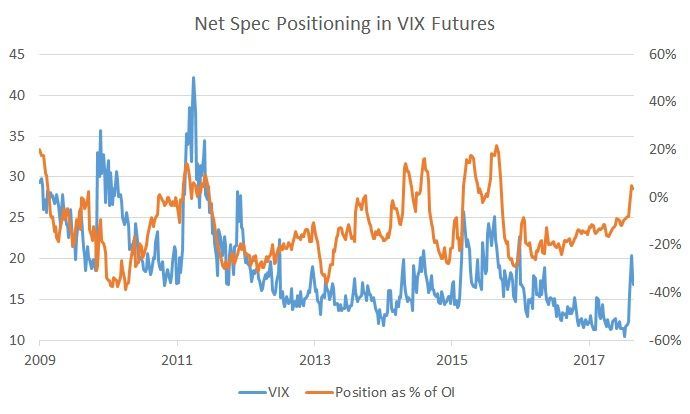

The first question is what is the current positioning in VIX Futures?

- Movement Capital @movement_cap – traders are net long VIX futures. extremely rare https://freecotdata.com/stocks/

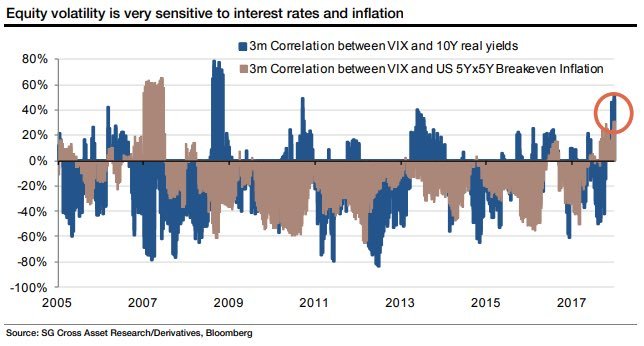

Despite all the action in the S&P this week, nothing has changed fundamentally. And the action in the S&P has been led by the action in VIX. So the real question is why is the VIX so uncharacteristically sensitive to action in rates and inflation?

- Jesse Felder @jessefelder ‘The VIX has never, at least in the last 12 years, been this sensitive to both real yields and long-term inflation expectations simultaneously.’ http://www.marketwatch.com/story/stock-market-investors-lost-their-ultralow-volatility-security-blanket-2018-02-28 … ht

@trevornoren

The MarketWatch article quotes a note on Wednesday, February 28, from Jitesh Kumar and Vincent Cassot, a pair of quantitative analysts at Société Générale.

The MarketWatch article quotes a note on Wednesday, February 28, from Jitesh Kumar and Vincent Cassot, a pair of quantitative analysts at Société Générale.

- “The only factor pointing to lower volatility, they said, is strong and synchronized global economic growth. Periods of robust growth are expected to lead to better corporate earnings keeping a lid on volatility.”

- “As far as macro factors are concerned, the analysts said the unwinding of central-bank balance sheets would make for lower liquidity and should allow volatility to rise.”

- “U.S. Treasury yields are straddling historically significant technical levels even as markets are trying to second guess the Fed’s hiking path and digest higher Treasury issuance (as a consequence of recent tax cuts) at the same time.”

Tom McClellan made a similar point in his article It’s the Fed, Yanking The Punchbowl :

These amounts might seem like they should be inconsequential, especially for a stock market which trades $100-200 billion of stock every day. But the top chart shows that the Fed’s actions do seem to matter, and the drops in the Fed’s balance sheet are coinciding with the big weekly drops for stock prices.

These amounts might seem like they should be inconsequential, especially for a stock market which trades $100-200 billion of stock every day. But the top chart shows that the Fed’s actions do seem to matter, and the drops in the Fed’s balance sheet are coinciding with the big weekly drops for stock prices.

He makes an interesting prediction at the end of his article:

- “My expectation for 2018 is that the officials at the Federal Reserve are eventually going to realize that their proposed accelerating rate of bond sales is having an adverse effect, and they will alter their course. But they are not going to realize that for a while, and so stock investors are in for a much wilder ride in 2018 than what they have become accustomed to.”

What until then? Guess we have to look at the positioning in VIX Futures!

3. Reverse Gundlach?

Look back to the Gundlach tweets from January:

- Jeffrey GundlachVerified account @TruthGundlach JNK ETF now down YTD. If rates keep rising, I expect JNK to underperform Treasuries. Even more likely if rates fall. Not a good JNK set-up.

- Jeffrey GundlachVerified account @TruthGundlach Junk Bond ETF JNK has been below its 200-day moving average every day but one since Nov 1st! Amazing, given SPX is up almost 9% since then.

He turned out to be correct. It took a couple of weeks but the S&P did fall hard to join the fall in JNK. So shouldn’t high yield bounce to lead a bounce in S&P? And Gundlach is a believer in positioning:

- Babak @TN junk bond

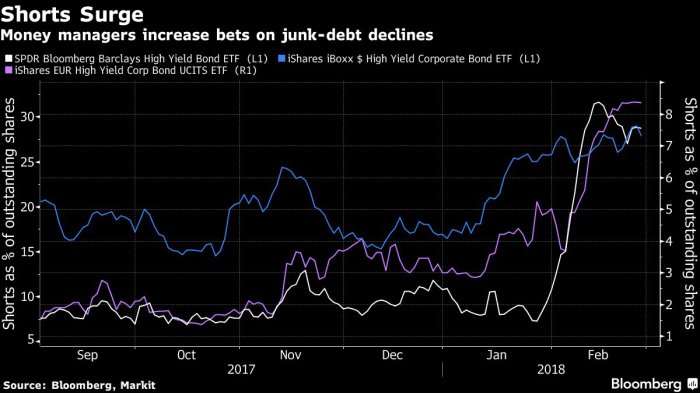

#sentiment is so terrible$HYG ETF has 29% short interest ratio, the highest on record$JNK$TLT$BND – everyone is so convinced that a credit Armageddon is around the corner they’re willing to pay up to short high yields https://www.bloomberg.com/news/articles/2018-02-28/short-interest-in-high-yield-etfs-hits-record-as-rate-rises-loom …

One day doesn’t make a trend but look:

One day doesn’t make a trend but look:

- J.C. Parets @allstarcharts – Credit spreads narrowing folks. Stock market bears conveniently failing to mention that

What about the sentiment about the economy?

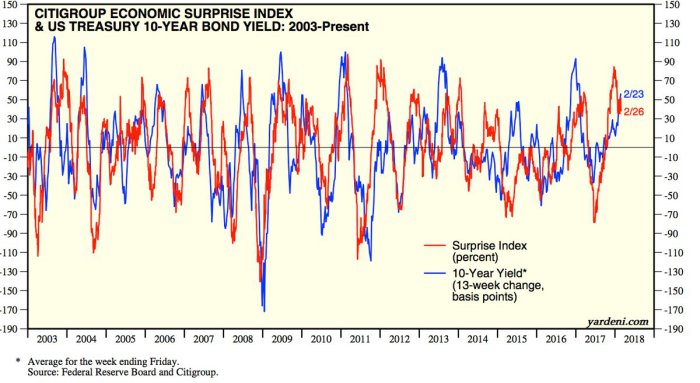

- Urban Carmel @ukarlewitz – Feb 27 –1. Economic upside surprise at 5 yr high and 2. probability of 4 rate hikes in 2018 at a high. This usually doesn’t last (from Ed Yardeni)

Could bond fund inflows lead some shorts to cover?

- Lisa AbramowiczVerified account @lisaabramowicz1 – BlackRock’s Core U.S. Aggregate Bond ETF saw an unprecedented $1.5 billion inflow yesterday. That’s gotta be the biggest one-day flow into any fixed-income ETF, or close to it.

So what if we see some short covering in Treasury & Junk Bond shorts? Does that force liquidation of long VIX positions and create a bounce in stocks? That sounds juicy except next week we have two events that can change everything – President Trump signing the Tariffs and the Non-Farm Payroll report.

4. US Stocks

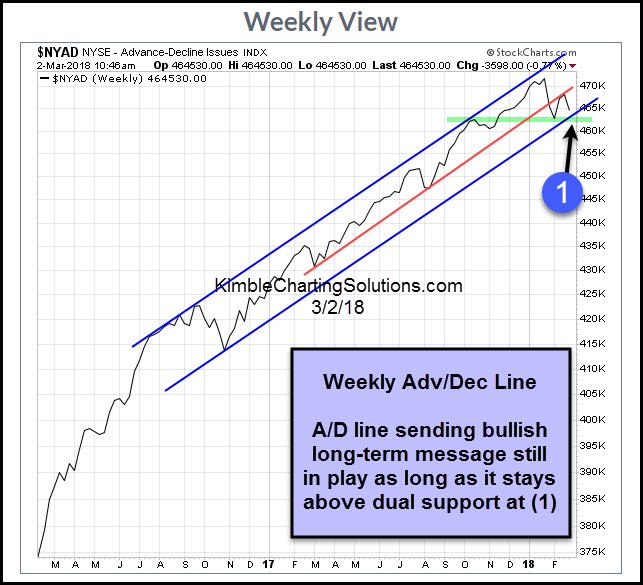

Remember the adage about breadth worsening before the market does?

- See It Market @seeitmarket –chart via

@KimbleCharting: “Advance/Decline line remains sending bullish message as long as it stays above dual support at (2).“

Since earnings do have something to do with stock performance,

Since earnings do have something to do with stock performance,

- Charlie BilelloVerified account @charliebilello –Current estimates from S&P Dow Jones: 25% operating earnings growth in 2018 for the S&P 500 (From $124.87 to $156.19).

But what about guidance?

- Ryan Detrick, CMT @RyanDetrick –As earnings season wraps up, we have seen a record number of S&P 500 companies raise EPS guidance. That is how 2018 earnings can go from 10% growth at the start of the year to 19% currently. https://lpl-research.com/hoc/

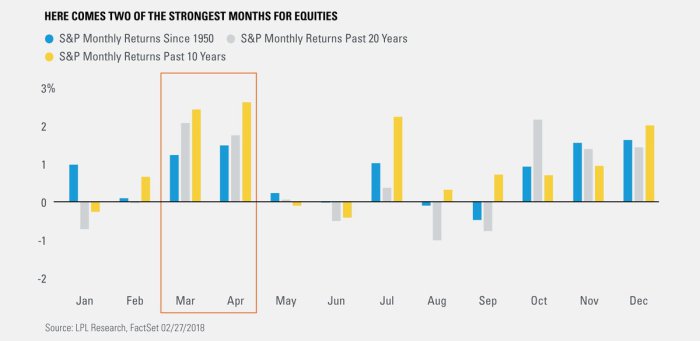

What about seasonality?

What about seasonality?

- Ryan Detrick, CMT @RyanDetrick – Feb 28 –March and April historically are two of the best months for stocks. https://lplresearch.com/2018/0

2/28/march-madness/ …

What about the U.S. Dollar?

- Mark Newton @MarkNewtonCMT –The most important move might not have been with US equities, but in the Dollar, which turned down following Trump’s Tariff proposal plans for next week- This should aid EEM, EURUSD, GBPUSD, and Metals after a recent pullback

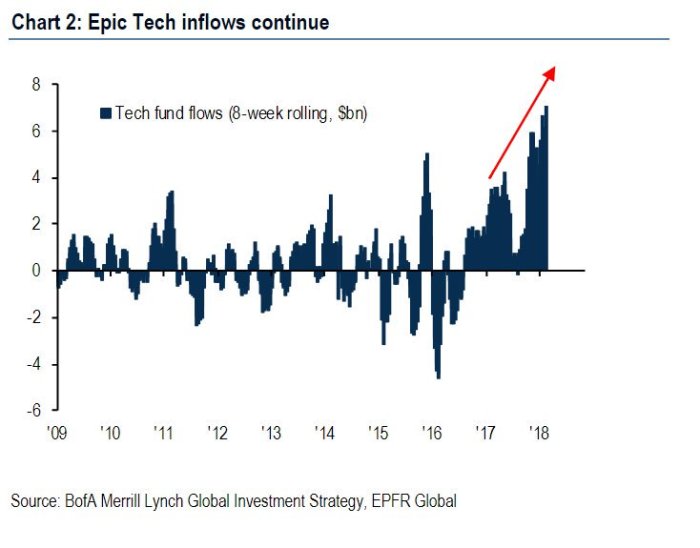

Shouldn’t it also aid tech stocks? Especially given the inflows:

Shouldn’t it also aid tech stocks? Especially given the inflows:

- Robin WigglesworthVerified account @RobinWigg – Technology fund inflows have been particularly epic.

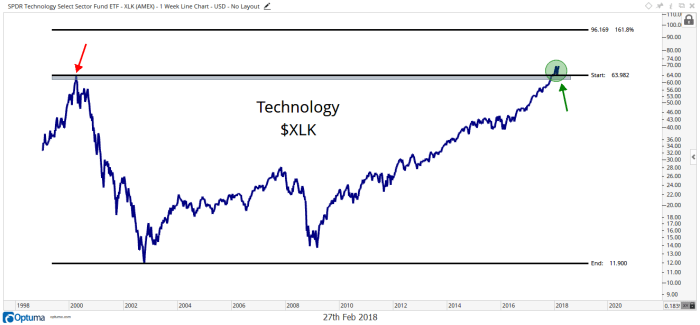

But are these inflows a positive signal or a negative signal? That depends on a line in the sand, per J.C.Parets from his post of February 27- It’s Make Or Break Time For Technology:

- “Here is the Technology Sector Index Fund $XLK trying to hold above that historic top near 64. As far as I’m concerned, this is the line in the sand. If we’re above that level, then the path of least resistance is much higher, in my opinion: 50% higher towards 96:”

Semiconductor stocks look the same way to Parets, subject to SOX staying above 1332.

Semiconductor stocks look the same way to Parets, subject to SOX staying above 1332.

5. Gold

If the Dollar does stay weak and rates fall some, wouldn’t that be good for Gold?

- FBX258 @fbx258 –Who said the GAP was a myth ?

$HUI#GOLD gap filled 15 months later. Positive divergence in RSI#Silver$silver

What about Gold Miners?

- fred hickey @htsfhickey – Gold’s $1320, up on yr& average selling prices for 1st 2 months of Q1 over $55 higher than last qtr- nearly guaranteeing big EPS beats when miners report Q1 results, yet investors allow themselves to get played by wise guy shorts taking out chart points, causing stop loss selling

Send your feedback to [email protected] Or @MacroViewpoints on Twitter