Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.”… a little pain …” & “… that’s what I’m all about … ”

Two weeks ago we wrote in that week’s TACs article:

- “As we argued three weeks ago in our article President Trump’s Tariffs Announcement – Oh Yeah, Baby?, he is making a turn into a FDR like figure who roared against the interests of the rich. And that means to hell with the stock market if necessary.”

President Trump confirmed this on Thursday evening in his radio interview with WABC in the following words:

- “Now we could — the easiest thing for me to do would be just to close my eyes and forget it; … “If I did that, I’m not doing my job. So, I’m not saying there won’t be a little pain, but the market’s gone up 40 percent, 42 percent — so we might lose a little bit of it — but we’re going to have a much stronger country when we’re finished. And that’s what I’m all about. We have to do things that other people wouldn’t do.”

As we wrote two weeks ago, “the US stock market is beginning to sense this significant change, a change that is deeper than any one trade dispute.” It is just beginning to sense this but it still isn’t a believer. Because it keeps bouncing off S&P 200-day of 2590, or the 2580-2590 range. What would it do if it believed what Elizabeth Economy, China Fellow-Council of Foreign Relations, wrote this week?

- “Xi’s response to Trump’s initiatives has not been a creative “win-win” solution but rather a “lose-lose” proposition. The relationship is spiraling downwards, and the risk of a miscalculation or accident is only increasing.”

Almost all of the coverage on FinTV is geared towards arguing that President Trump’s tweets are mostly a negotiating tactic and that these should not be taken very seriously. Other coverage suggests that President Trump is acting “childlishly” and believes he will eventually realize that.

We think they are totally wrong. We believe President Trump is deadly serious and his statement “that’s what I am all about” is to be taken literally. And, as the Stratfor article on Friday April 6, states succinctly:

- “U.S. President Donald Trump keeps nudging China toward a trade war … Rather than an off-the-cuff trade policy statement or tweet, Trump’s decision to up the ante is a clear and calculated decision. “

Stratfor is 100% correct in our view. Any one who calls this US-China exchange a childish tit-for-tat is terribly wrong. President Trump began pushing Chinese President Xi to react and Xi fell for it.

- George Magnus @georgemagnus1 – Can’t see any happy ending here or how RMB isn’t going to take a plunge, unless wiser political counsels prevail. Strongman Xi Jinping may play victim here, but he’s already making strategic errors that will not benefit China which needs a trade war like a hole in the head

Remember how people used to talk about current situation being analogous to the 1930 when deflation was the main fear? They forget how President FDR deliberately pushed that imperial Japan to modify its mercantile ways; how he eventually put an embargo on Japan & forced Japan to either acquiesce or lash out militarily. See our adjacent article for a more detailed discussion on this analogy, but make no mistake about President Trump’s determination to force China to make structural changes.

Unfortunately President Xi’s China simply cannot acquiesce having already opened the ball. But they can’t put tariffs beyond matching what President Trump has done because the amount would exceed total US exports to China. So what is the next major weapon China might use?

- Raoul PalVerified account @RaoulGMI – China could just devalue the Yuan and stop fiddling around with new tariffs…that’s the nuclear option here.

The trouble with a nuclear option is that it forces the opponent to respond with a nuclear option. What if President Trump responds by declaring China a “currency manipulator”? That would, at the very least. justify imposing a blanket tariff on all Chinese exports to America. It would also enable the Trump Administration to get EU, Japan & even South Korea to respond because a Chinese devaluation would be injurious to all of them.

Hopefully, President Xi learns from Jeff Bezos and stops responding publicly to tweets & comments from President Trump. That might facilitate quiet negotiations over the next eight weeks and may help stabilize the US stock market.

But the long term trend may be changing as we see it from our views above. And some see it via their own discipline:

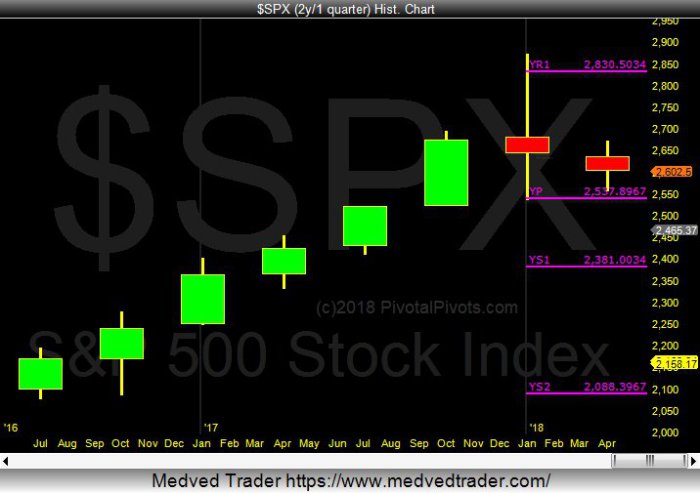

- Jeff York, PPT @Pivotal_Pivots –Should long term investors be worried about this Doji candlestick on the

$SPX? It maybe a signal that the longer term trend is changing!

2. Global Economy, Rates & Credit

The March payroll number promised to come in like a lion, but actually came in like a lamb – a mere 103K print in jobs after a strong 241K ADP number. David Rosenberg gave the report a big fat C. But signs were visible before the NFP report:

- Martin Enlund ?

@enlundm – S&P500 and other equity markets would have swooned even if there hadn’t been a so-called trade war brewing. Because macro.

$spy

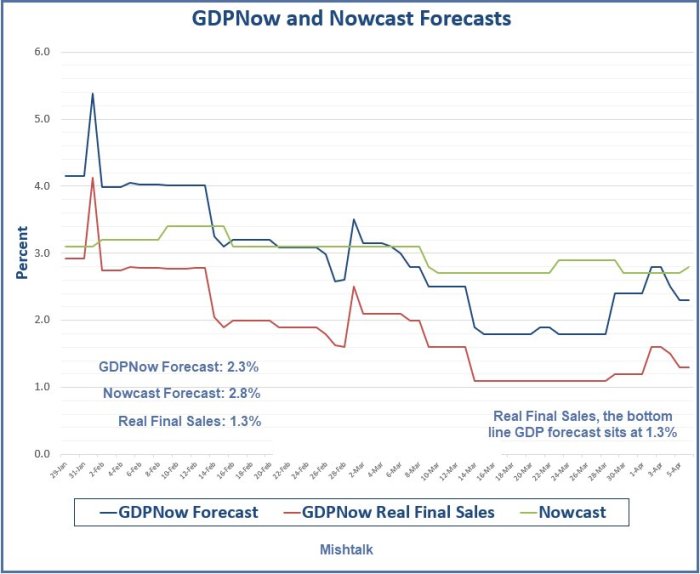

What about US GDP?

- Mike Mish Shedlock @MishGEA – GDPNow Forecast Dips to 2.3%: Real Final Sales 1.3% https://www.themaven.net/misht

alk/economics/gdpnow-forecast- dips-to-2-3-real-final-sales-1 -3-J09G_fSUbkWqu6R2kJr2Hg/ …

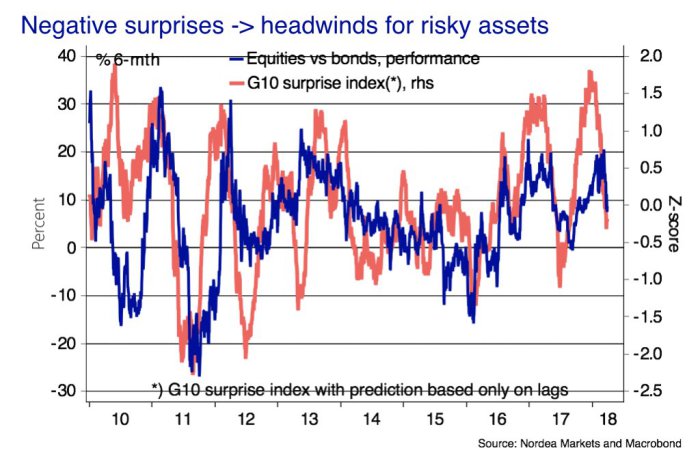

How do Treasury rates keep going up with this US Macro? Perhaps with impetus from Europe? Probably, but impetus in what direction?

- Holger Zschaepitz @Schuldensuehner – Ouch!

#Eurozone Economic Surprise Index has collapsed to -72.5, the weakest reading since May 2013 as the sovereign debt crisis flamed up. (via Amherst Pierpont)

What do you think Draghi is going to with the above reality? Start QT, reduce QE or stay pat? We think the last. Well, if this is all true, then it would be such an inconvenient time for the global DM cycle, right?

What do you think Draghi is going to with the above reality? Start QT, reduce QE or stay pat? We think the last. Well, if this is all true, then it would be such an inconvenient time for the global DM cycle, right?

Now add to this the serious possibility of a trade conflict between US & China, a conflict that may actually threaten the current global trade order. Are you now surprised to hear that Gary Shilling is calling for 30-year yield to drop to 2%, a fall that would deliver 30% return in a year? Nothing is as deflationary as protectionism and a global trade war.

Now add to this the serious possibility of a trade conflict between US & China, a conflict that may actually threaten the current global trade order. Are you now surprised to hear that Gary Shilling is calling for 30-year yield to drop to 2%, a fall that would deliver 30% return in a year? Nothing is as deflationary as protectionism and a global trade war.

Before any wrists are slashed, remember the 10-year yield has first to break below the support line at 2.63%. That might be hard as long as Chairman Powell keeps steadfast to his 3-4 rate hikes scenario. More dangerously, he remains publicly committed to contracting the Fed’s balance sheet via QT. Of course, the sooner he contracts it, the sooner he & Draghi can open the spigots through a new QE if the trade war between US & China materializes.

3. Stocks

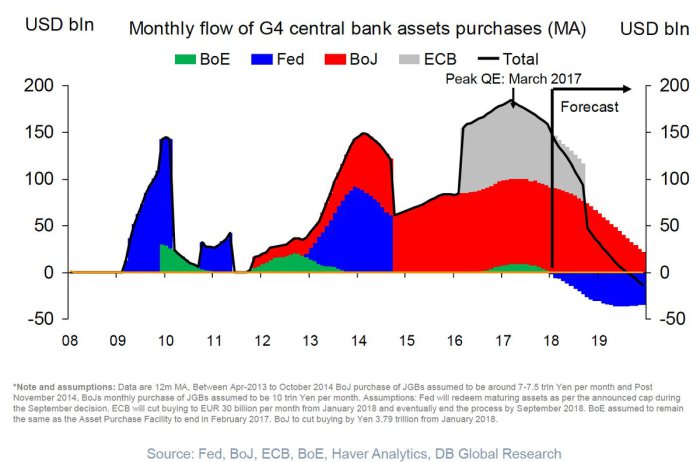

Powell’s QT determination may be what made Rosie revert back to his old reliable un-Rosie self:

- Holger Zschaepitz @Schuldensuehner – Peak liquidity behind us: That chart shows why fmr Merrill Chief econ David Rosenberg has turned bearish for the first time since 2012. MUST HEAR! …http://adventuresinfinance.realvision.libsynpro.com/60-look-out-below-david-rosenbergs-stormy-outlook …

If that is not enough,

- David Rosenberg @EconguyRosie – Barely over 3 months into the year and already no fewer than 22 sessions with intra-day moves in the Dow of 400+ points. We had 1 all of last year. The only other time in the past have we seen so many 400 point moves bunched into such a short period — Oct 2008 to Jan 2009.

On the other hand, let us note that the Put-Call ratios are very high; VIX levels are high; the stock market is oversold and held its critical 200-day & February low. So if no bad news hits and earnings come in strong, we could easily see a bounce.

Send your feedback to [email protected] Or @MacroViewpoints on Twitter