Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Europe comes home to Jay Powell?

It was Rick Santelli who tried to focus viewers on the rates explosion in UK & Germany during the last couple of days. The German 2-yr yield rose hard by 16 bps this past week. All this while Germany is in the throes of a massive energy problem that actually might force some Germans to choose between “eating” & “heating”. UK energy prices also exploded this week. What’s going on? A move to protect the Euro currency by hiking interest rates?

- Robin Brooks@RobinBrooksIIF – – There’s a lesson here for ECB policy makers. If you try to keep Euro strong with hikes, it won’t work. Markets will ignore you and push Euro down regardless. All you risk accomplishing is making the coming recession deeper at a time when Europe already faces massive challenges…

What Europe is facing are the results of a “colossal regime change” it undertook:

- Lawrence McDonald@Convertbond – – Europe´s Colossal Regime Change 2010-2019 – Forcing austerity on Greece and the rest of the periphery – endless “black zero.” 2020-2030: Massive covid lockdown Euro subsidies and even larger social energy cost bailouts, much fueling – financing higher energy prices.

He doesn’t mention it in the above tweet but he has before – that German & EU policies neglected/discarded old methods of energy generation in favor of “clean” energy plans & increased dependence on cheap Russian energy. And Germany is not alone in facing the consequences:

What should it mean for the Euro?

- Robin Brooks@RobinBrooksIIF – – We’ve forecast that the Euro would fall below parity since March. Russia’s invasion of Ukraine means that Europe’s main growth engine – Germany – will have to retool its growth model away from Russian energy. That means weak growth & big trade deficits. Euro will fall lots more.

In fact, Jordan Rochester of Nomura argued on Bloomberg Surveillance on Monday, August 22, that

- “…. the FX market is totally mispricing the situation in Europe; credit markets are doing a better job .. we are seeing credit spreads widen … ; … the energy price spike is getting worse; … if you look at the past 22 days, 80% higher energy prices this month alone ; … situation is a complete rethink of the economic model of the eurozone; its strange for us to see the Euro fall so slowly I think it should be much faster ; we will be testing 97.50 down towards 95 in the next few months ”

How much of a rethink? Read what we noted from what RBC’s Biraj Borkhataria told CNBC’s Brian Sullivan on Tuesday, August 23:

- “.. we argue that there is too much focus on this winter because of what [scramble for gas] you have seen; this winter is probably going to be OK … however once you roll through post winter, you end up in exactly the same situation next year – scramble for gas in summer 23 & winter 23-24 looks pretty painful … unless something changes with the war, sanctions on Gazprom … this is not a 6-month issue; this can go on for years & get worse … it took multiple years to get into this situation & its likely to take multiple years to get out of the situation … also you have to consider the structural aspects of what happens to demand … “

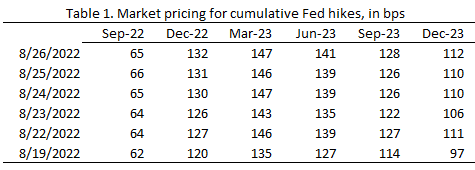

Given all of this, is hiking interest rates the ideal move for the ECB? Ideal or otherwise, the European Bond markets voted this past week that the ECB will hike interest rates to push down inflation in Europe. It is as if the ECB wants to be recognized as the new Volcker.

And that came home to put huge pressure on Chairman Powell to talk far more angrily than he did at the August post-FOMC presser. But were his angry comments at Jackson Hole a serious jump in hawkishness or just another blow cold, blow hot version of Fedspeak? Why not ask the most independent & historically most accurate of inflation measurers?

- 30-year yield FELL 4 bps on Powell Jackson Hole Friday; 20-year yield fell 3.2 bps; 10-yr yield up 0.8 bps while the 7-1 year curve rose 3-5 bps …

For those who continuously seek confirmation from Goldman Sachs:

- Robin Brooks@RobinBrooksIIF – – On the fixed income trading floor at GS, we often saw equities – just one floor below us – have different takes on the Fed. Yesterday was one of those days. Market pricing for hikes was unchanged after Powell’s speech, but S&P 500 fell. I’d trust fixed income markets on this one.

The reality is Chair Powell professed data-dependency in his post-FOMC presser & he professed data-dependency on August 26 at Jackson Hole. So, in our unstudied & irrelevant opinion,

- if next week’s NFP report comes in strong as the previous one did AND the CPI, a week later, is hot, then you know the Fed will raise rates by 75 bps;

- if next week’s NFP report comes in much weaker than expected AND CPI comes in way softer, then the FOMC will tighten by 25-50 bps;

- if we get one hot data point & one cool data point, then the FOMC will tighten by 50 bps.

Powell’s words & tone has very little to do with this reality. The bottom line is that Powell should not waste the opportunity he has to raise rates on September 21 and we don’t think he will.

2. China – blowing colder & colder?

Thursday was the one up day in stocks last week with Dow up 323 points, S&P up 58 bps, NDX up 226 points & Transports up 255 points. That was due to the “large” stimulus poured in by China both into the economy & into real-estate developers. This is old action-reaction routine. But is it valid? Look what Leland Miller, founder & CEO of China Beige Book, said on BTV Surveillance on Monday, August 22 (minute 1:21-1;29). Tom Keene asked him whether we will see 5% GDP growth in China. Miller replied:

- “I don’t even say we are going to get 3% …. this is really a very weak economy… how weak the consumption is, how weak the property sector is, how weak every aspect of the entire economy outside exports has been. And even exports are now fading. .. so not 5% GDP but significantly less than half that at this point … what firms are telling us on the ground is they don’t want to borrow, they don’t want to invest, they don’t want to hire because they don’t see this Covid zero nightmare ending anytime soon … you have got a global slowdown. So the demand is faltering around the globe. This is very concerning. …. ”

And David Rosenberg twitted on Thursday:

- David Rosenberg – @EconguyRosie – – China’s fiscal stimulus package barely covers the bad debt losses in the country’s property market. This ain’t no 2008-09 budget game-changer. #RosenbergResearch

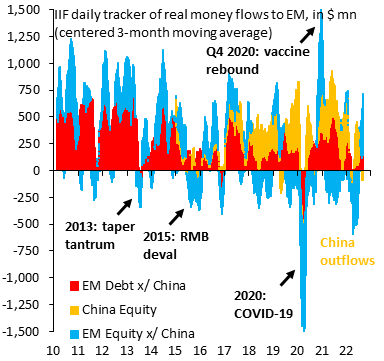

So how are inflows-outflows in & out of China doing?

- Robin Brooks@RobinBrooksIIF – – Markets are looking at China in a new light. We saw outflows from China immediately after Russia invaded Ukraine. We see outflows again now, even as the rest of EM gets “Fed pivot” inflows. It’s very rare we see weak China flows and strong non-China EM flows. Something’s changed.

Does that mean China cannot play its previous role of exporting low prices or disinflation into America? And does it also mean U.S. companies operating in China may not report strong numbers in Q3 & Q4? That is not good news for Chairman Powell.

The above really does not impact Chinese ADRs in America which got a big boost from the deal struck with the SEC this past week. Look KWEB was 10% on the week.

3. U.S. Economy & US Stocks

Why talk about the U.S. economy today when we will know much more by Friday? That brings us to the isolation of Fed Chair Jay Powell because of the dismal condition of America’s two largest trading partners & the two largest economic regions after America – Europe & China. On top of that, he faces an previously unseen landscape as JPM’s Bob Michele said this week on Bloomberg Open:

- ” … for God’s sake, we are facing the highest inflation in 40 years; the most aggressive global policy response in that in 40 years we are seeing rate hikes nobody ever imagined; we are going to see a liquidity withdrawal from Quantitative Tightening that we have never experienced before… ”

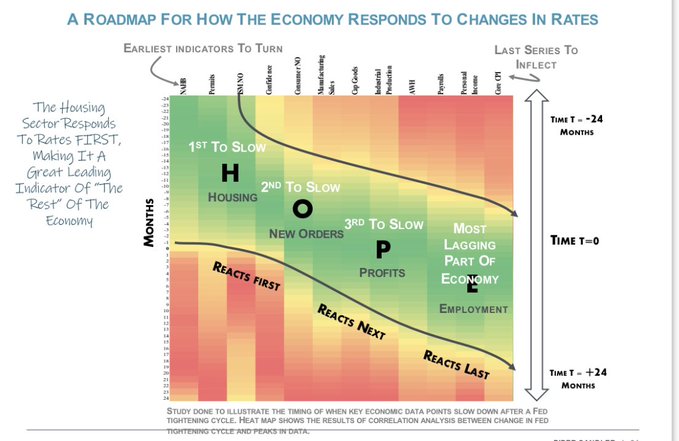

But why haven’t these massive rate hikes impacted the U.S. economy? We saw an interesting chart this week that might provide a clue (with thanks to @LynAldencontact for her retweet):

- Kantro@MichaelKantro – Replying to @andycwest – #HOPE. Playing out in classic fashion in 2022. #macro

Another “classic fashion” in Fedspeak was highlighted below:

- Lawrence McDonald@Convertbond – Every Cycle – they bleed out the truth: MESTER: NOT PENCILING IN A RECESSION, BUT RISKS HAVE RISEN; IF THERE IS A RECESSION, WON’T BE DEEP. August: Ok, recession risk is rising but it won’t be deep. June: Small chance, but in 2024. May: No chance of recession, don’t be silly.

Fin TV anchors are not that far behind with CNBC’s Jon Fortt saying on Thursday that “a lot would prefer a baby recession at this point“. We have however seen babies grow into adults & that is our serious fear about this situation – that the simultaneous downdraft in global economic growth (at least in the 2nd & 3rd economic regions) and increase in inflation are going to convert this baby recession into a nasty young college guy recession.

What do the gurus tell us? On one hand we have,

- Marko Kolanovic on CNBC on Wednesday – U.S. recession won’t happen; expect China to pick up slack; Europe is in recession but what has been priced in is worse; things might be bad but positioning is worse; global investors are 10% invested;

- Jeff DeFraff on CNBC on Tuesday – pretty rare & pretty unique & typically the beginning of a bull market… more disdained rally & momentum I have seen ; price tends to lead the narrative …

- Tom Lee on Friday on CNBC – drivers for inflation have essentially evaporated; this selloff is going to be bought

On the other hand, we have

- Kathryn Rooney Vera on CNBC Squawk Box on Wednesday, August 24 – “I am telling investors to position for a real recession, a recession where you will see unemployment go above 4%-4.5% by 2023“

- David Rosenberg on Financial Post on Monday August 22 – an 11:58 minute clip that reminds you of the Summer of 2008 & what followed in Fall 2008; says next year we will be talking about deflation; says earnings recession has just started & says we are going to break through June lows … In another 3:10 minute clip on the same day – Rosenberg says at 3,000 on S&P “this bear will come out of the cave & enter the bull ring“.

- Mike Wilson on BTV Real Yield – extremely high conviction that earnings expectations are still too high; it is similar to my conviction level about the Fed in December; earnings revision breadth is one of the worst we have ever seen .. forward earnings are 5% too high and, if it is a recession, probably 15% too high …

What Chairman Powell said on Friday does not change much in terms of data dependency. But it seems to have changed a lot in the minds of stock players as the superb pair of charts below show:

4. Fishook in Gold & “Gates of Hell”

In case you didn’t know (we certainly didn’t),

- “A fishhook occurs when there is a temporary reversal in the direction of the Price Oscillator’s travel, and that reversal itself gets reversed. It signifies that the forces of reversal have failed, and that opens up the door to the prior trend to reassert itself with renewed vigor.”

For example?

- “Perhaps the biggest and most dramatic example of a fishhook was the one that occurred just before the 1987 crash. This next chart shows the fishhook that appeared in the chart of the NYSE’s McClellan A-D Summation Index, which is effectively a Price Oscillator for the cumulative daily A-D Line. When that December 1987 fishhook turned back up again, it unleashed a more powerful up move. That is the potential which a fishhook structure conveys. Prices do not always deliver on that potential, but the possibility is there.”

The above and the conclusion below are from the article of Tom McClellan titled A Signal Called Fishhook in Gold on August 26, 2022.

- “As of Aug. 25, 2022, the Price Oscillator for gold prices has turned up again, making for a fishhook structure in gold’s Price Oscillator, which conveys the message that there is the potential now for a more powerful up move in gold prices“.

Remember the line “Hell is coming with me” warning from Tombstone?

Not as chilling to hear but probably worse in its impact is the clip titled “the gates of hell???“. It is not about physical violence as in Tombstone but it is probably about far more misery & economic violence in the 2nd largest region in the world. At minute 24:24 of the clip, Louis Gave, CEO of Gavekal Research, discussed how “We’re ending up at the gates of hell” in Europe.

- “… if you think we can gave massive energy shortage in Europe & not have supply chain disruptions all over the world … so many auto parts are still manufactured in Europe … if you have energy shortages, you are going to have auto parts shortages … so Europe is in a big bind, its going to be a hit for global growth & potentially another boost for inflation at the same time … “

So is Europe in hell already or is there a “saving grace” for Europe?

- “… Europe’s saving grace, silver lining in all of this – oil prices at $95 are actually not that high … right now electricity cost in Europe, in oil equivalents, is $1,000 per barrel; natural gas in Europe is $600/barrel … “

So? Gave says:

- “What Europe can do is buy very large copious amounts of oil & … burn it for energy which is polluting & a stupid way of producing energy … saving grace is 1) oil is really not that expensive and 2) moving oil around is actually quite easy .. much easier than moving natural gas .. so Europe this winter will have no choice than to buy copious amounts of oil … that’s pretty bearish for Euro because they have to buy oil in U.S. Dollars “ …

We are not as “smart” as Louis Gave but we have to wonder where Europe can buy that amount of Oil especially when Saudis are talking about a cut in supply. Wait a minute, they can buy oil directly from Russia. But they will have to pay in Rubles that would violate EU sanctions. And instead of that, wouldn’t it be easier to open NordStream 2 (as some German lawmakers have demanded) & have natural gas piped in in “copious amounts”?

But instead of that, EU is threatening to impose sanctions on Russia on December 5 that will at least curtail the supply of oil. So they would rather force their people to enter through the gates of hell & choose “eating” vs. “heating”!

Is all this a negative for oil prices? Actually Paul Sankey sees Oil going to $150 but not staying above that on a sustained basis. And that is without Europe buying “copious amounts” of oil to burn for heat.

Send your feedback to [email protected] Or @MacroViewpoints on Twitter