Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. “at a level previously thought unthinkable“

said Jeffrey Gundlach this week about his biggest surprise of 2015*:

- “Yield curve will flatten at a level previously thought unthinkable“

If it comes true, this will be a major event for the economy & markets. We recall Barton Biggs describing an ‘Ice” scenario in late 1990 that had 3-month T-bills falling to 3% within a couple of years. That was when the yield curve had flattened just above 9%. At that time, a 3% T-bill was dismissed as laughable. Three years later, the 3-month T-bill did fall to 3%. That was a major bull-steepening move & not a flattening. The yield curve flattened around 5.25% in June 2007 and we know what happened afterwards. So a flat yield curve is a bad thing that often leads to a recession or a serious slowdown.

So for the yield curve to flatten in 2015, short rates have to rise in 2015. To what? 2%, 2.5%? Very few are calling for the Fed to raise rates with such clarity as to send the 2-year yield up by 200 bps. So that suggests, the 10-year & 30-year yields have to come down to say 2%. The only way the treasury curve flattens at 2% or below is what we have been dreading for awhile – that the Fed makes a mistake and longer maturities viciously trade down in yield in response.

Remember Bullard’s expressed concern about falling inflation expectations on October 16?

- ForexLive @ForexLive – Here is why the Fed should be extremely worried http://bit.ly/1A0li1f

Gundlach concurs & adds why, in his opinion, there aren’t any fundamental reasons for the Fed to raise rates next year:

- “particularly the inflation argument has become completely de-bunked; commodity prices are the same they were in 2010, we have 4 months in a row of CPI being zero & if oil is going to stay in the mid-70s or go lower which is possible, you are probably going to see year/year CPI at zero“

So what then could persuade the Fed to raise rates according to Gundlach?

- “so the Fed should not be raising interest rates & yet they don’t want to be at zero; they are in a conundrum; they might raise rates just to see what happens“

But that is very different than raising the rates to 2%. So for Gundlach’s call to come true in 2015, the 10-year has to fall to about 1.5%, right? Frankly, we don’t believe Chair Yellen will gamble on raising rates hard in 2015. What might happen is that short rates might rise on a growth spike in 1st half of 2015 and the 10-5 year spread could narrow to 25-50 bps or so – a semi-flattening if you will.

We got a taste of how bonds can react to stronger economic data after a stronger than expected 3.9% print on Q3 GDP on Tuesday:

- Dividend Master @DividendMaster @Kelly_Evans look at 30yr UST yields collapasing . Thats biggest pools of money on planet laughing at that theory we’re ‘closed economy

- Helene Meisler @hmeisler Did bonds not get the memo on this morning’s GDP?

But what if the economy is not that strong?

- Steve Kroll on CNBC Closing Bell on Tuesday 11/25 – “I think the 10-year can go under 1.8% …they can raise Fed Funds rate 25bps but I think rates are still gonna come down for the next year; because I think the world economy is slow;”

- David Rosenberg on Thursday – “It now looks like the U.S. economy has hit a bit of a soft patch in Q4; Real GDP growth looks set to come in closer to a 2% annual rate for the moment versus the 2.6% consensus estimate and we could end up seeing payrolls running closer to 200K for November than 225K”

So either way, bond yields fall? That doesn’t happen unless positioning needs to unscramble.

- Hedgeye on Wednesday, November 26 – “Right now, the market is still positioned net SHORT -128,000 contracts (net futures and options positions) in the 10YR treasury bond market. In other words, bond bears are getting royally creamed as the 10YR crashes alongside growth and inflation expectations. … For the record, we still think yields go lower as the Fed freaks about #deflation in Q1 of 2015.“

Rick Santelli said “Treasurys love ‘short shorts’” and explained why the 10-year yield could drop to the pivotal 2.14% yield by year-end. The 10-year closed at 2.17% on Friday. So only 3 bps to go for Santell’s forecast to come true.

* The most important line in Gundlach’s commentary & CNBC.com webmasters dropped it from their clips. Another reason how CNBC keeps failing its readers. Their mandate is short videoclips & they don’t care whether their clips omit critical comments.

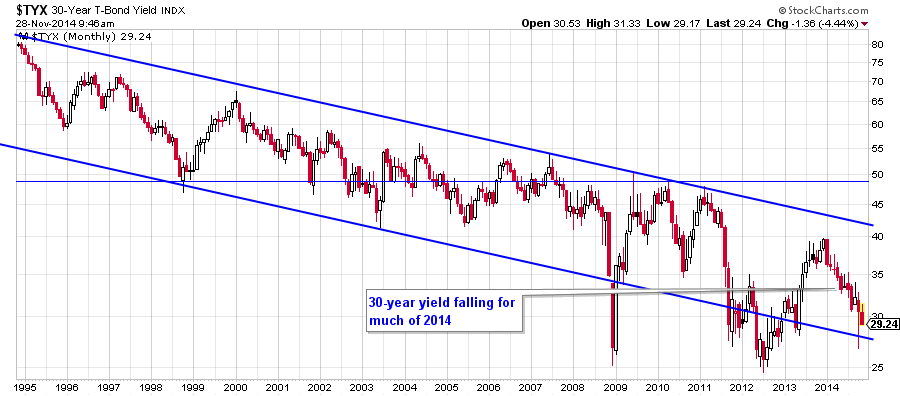

2. “The name is Bond, Long Bond“.

Not ours at all.And yes, the tweet below did come with a photo of Sean Connery as Bond.

- Master Muppet ™ retweeted $hane Obata @sobata416 Nov 25 coming soon to a theater? near you… “The Name Is Bond, Long Bond”

You can’t argue that Long Bond has been the winner this week and this year. Recall Santelli talking about the Treasury flash crash of October 15 and now ponder the reality that Friday’s close of 30-year Treasury yield at 2.898% has already fallen below the close on Wednesday, October 15, of 2.92%. The rest of the on-the-run treasury curve is still above the close on October 15th. The 5-year yield is still 15 bps higher than the 10/15 close, for example. So the 30-year bond is the champ:

- Charlie Bilello, CMT @MktOutperform – Most persistent trend in 2014 is falling yields. Race to 0% across the globe. http://pensionpartners.com/blog/?p=953

We do feel for Gundlach. For the second time this year, he called the 10-year yield of 2.20% as “the line in the sand“. And on both occasions, the 10-year yield rubbed out his line in the sand by dropping below the same week.

Next comes the payroll report.

3. U.S. Economy

- Bob Doll, Nuveen @BobDollNuveen – Compared to the aftermath of the credit crisis, every major segment of the U.S. economy is looking better. http://ow.ly/ENJgv

- Richard Bernstein @RBAdvisors – GDP: 4 of the last 5 quarters > +3.5% with exception blizzard-related. Is this really a “slow-growth” #economy?

- Lawrence McDonald @Convertbond @RBAdvisors yes, let’s get real, year over year Q3 GDP growth is 2.4%, rates don’t lie; 2s-10s, 5s-30, multi year tights, commodities lows

David Rosenberg talked about a soft patch in Q4 & 200K payroll number. In the other corner we have, Ian Shepherdson on CNBC Closing Bell on Tuesday:

- “this time it is really different; an absence of the fiscal drag we had for 2-3 years and we have got a much much better credit environment; bank lending to US businesses is rising by about 12% yr/yr; … the banking system is fixed; we have done that now in the US & credit is flowing again properly; that’s why we are getting the acceleration now;I think the payrolls pushing up for the past 6 months continues to accelerate & it wouldnt surprise me if over the next 6 months, we printed numbers like 275, may be even 300; it is going to drive down the unemployment rate & finally its going to start boosting wage growth; it is highly achievable – the key thing about that is not the numbers; it is about what it does to wages- starts to push them up;”

At the other extreme, we have:

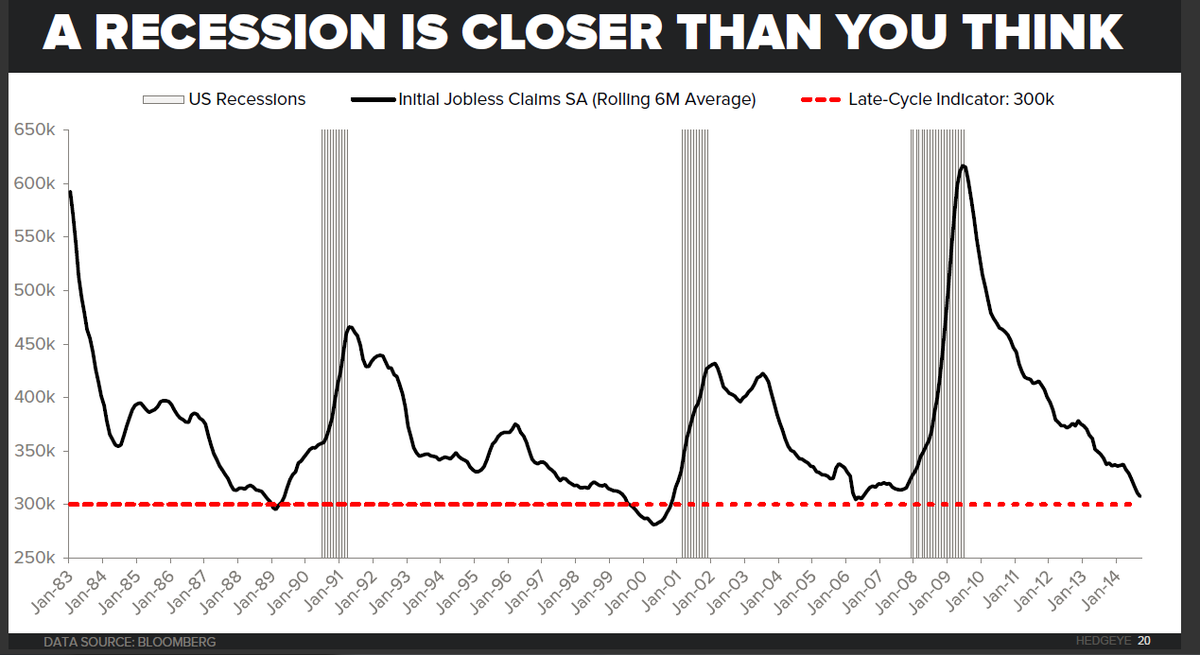

- Keith McCullough @KeithMcCullough – Do not ignore this chart – Jobless Claims always bottom < 300,000, then ramp

You don’t need a recession for a fall in Treasury yields. A fear of contagion can suffice:

- “This is the one thing I’ve seen over and over again,” said Larry McDonald, head of U.S

strategy at Newedge USA’s macro group. “When high yield underperforms equity, a major credit event occurs. It’s the canary in the coal mine.”

4. Global Economy

Silly us. We actually wondered last week whether EM would lead the beta-chase to year-end. Instead EEM fell by 1% this week. Oil & commodities collapsed on Friday & commodity EM markets from Brazil to South Korea to South Africa dropped by 3% or more.

- Lawrence McDonald @Convertbond – Dr. *Copper, fresh 8 year low; *He has a real word PHD in economics

Normally, fall in Treasury yields is bullish for EM Debt. But not on Friday. The EM debt ETFs, both sovereign & high yield, fell sharply in price while the 30-year Treasury rallied by 1% or so. Is this an EM-version of Larry McDonald’s canary in the coal mine (see section 3 above)?

Oil fell by 10% from Wednesday to Friday – that’s not just OPEC’s refusal to cut. It simply says that the world is awash in oil and that OPEC led by Saudi Arabia is going to take down oil prices to hurt competitors. Remember that can only happen in a slowing economy. Rick Santelli is probably right in his prediction about “permanently bending the cost of energy” but that good news is for the future. Today’s reality seems really bad for EM.

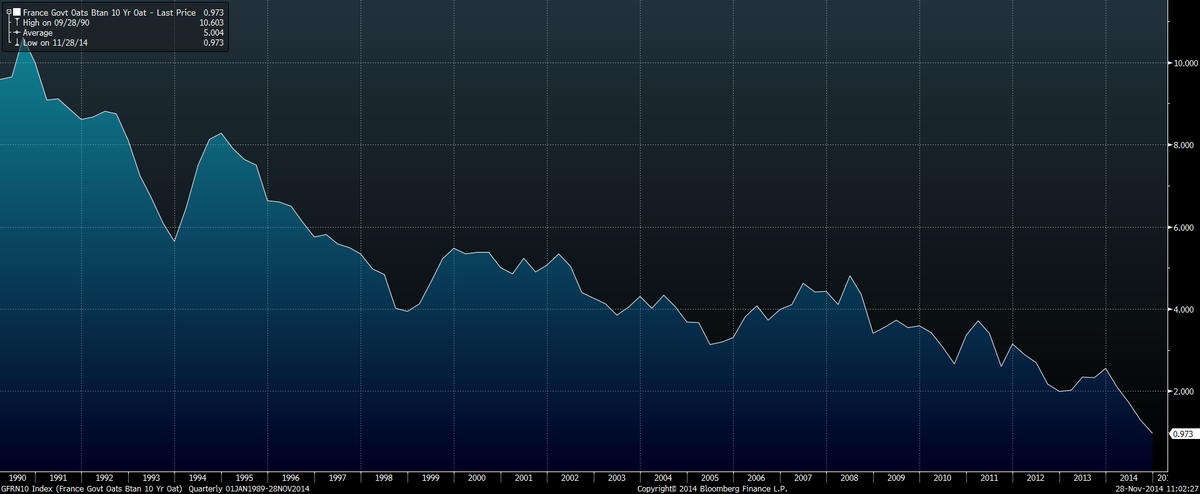

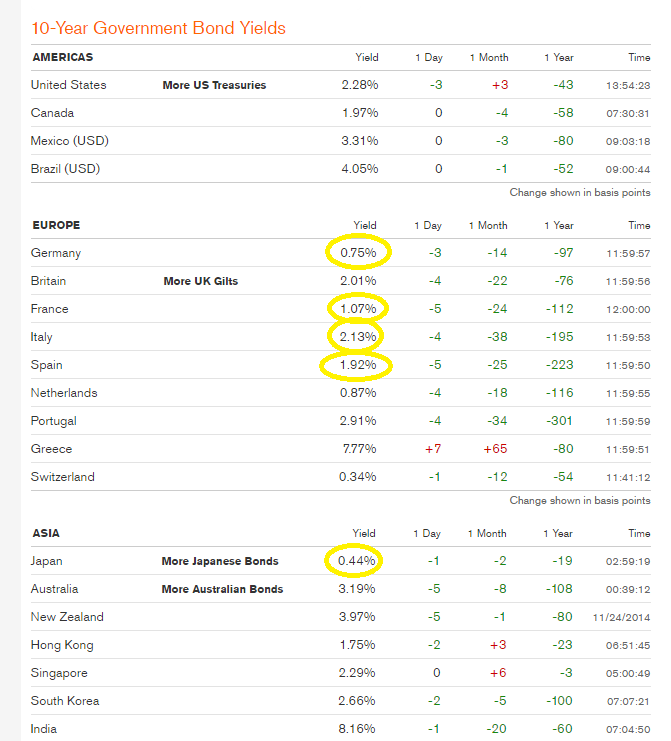

And Europe that should benefit big is acting badly. European bond markets are literally screaming deflation. The German 10-year closed at 70 bps for the first time ever. And:

- Charlie Bilello, CMT @MktOutperform – French 10-year yield under 1% for the first time in history. http://pensionpartners.com/blog/?p=953

- ForexLive @ForexLive – Italy’s GDP down almost 20% in USD terms since end-2007. http://www.forexlive.com/blog/2014/11/28/italy-stats-office-sees-q4-gdp-flat/ …

Does this force Draghi’s hand this Thursday? Will it be bullish if Draghi announces additional buying of corporate/asset-backed bonds or even sovereign bonds? One skeptic voice:

- Charlie Bilello, CMT @MktOutperform – Plummeting yields & no growth is massively bullish b/c it means more central bank easing. Guide to Investing in 2014.

On the other hand,

- Gemma Godfrey on CNBC FM 1/2 on Monday – “we are seeing the asset-backed securities buying alrready impacting and already boosting loan demand and having an impact; the risk investors face is that by waiting for this QE there are big opportunity costs there are assets out there that are going to be rising – on risk side, investing in Italian banks which ultimately are the biggest beneficiaries of borrowing low and lending high, & you obviously have an export-led economy that is benefiting from a crushed euro;& the loan growth we are seeing is in Italy“

5. U.S. Equities

The leading developed market in the world was placid this week. The outlier was the 1.5% fall in RUT on Friday – just a part of the growth scare? The other curious action was the rally in European banks versus a decline in US mega banks. The regional bank ETF was down almost 2%. Next week should be less placid with Draghi & payrolls.

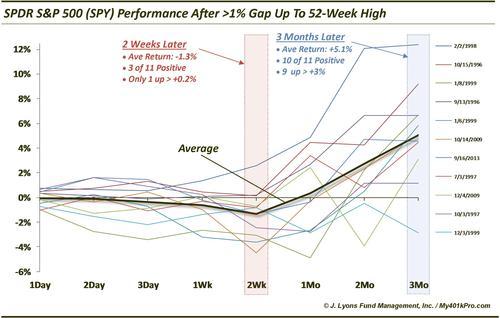

This week Dana Lyons amplified the view Chad Gassaway had expressed last week about big gaps at the open in US indices:

- Dana Lyons @JLyonsFundMgmt – ICYMI>ChOTD-11/24/14 1% $SPY Gaps Up To New Highs Have Led To S/T Pain, L/T Gain Post: http://tmblr.co/Zyun3q1WNsoxz

- “Again, there is no guarantee that stocks will follow the same general pattern this time around. However, the historical tendencies do mesh with some of the other studies we’ve looked at recently that suggest a short-term cooling of the recent red-hot market, before making another run to new highs.”

6. Gold

Does seasonality prevail over major events? First the seasonality from Jeffrey Hirsch:

- “Back on Veteran’s Day we alerted Almanac Investor subscribers and our loyal blog followers to gold’s seasonal tendency to begin to rally in mid-November. … At that time we noted that SPDR Gold’s (GLD) technical indicators were setting up nicely for an early entry into a new long position. … on the thirteenth, GLD’s MACD buy indicator confirmed a shift in momentum by issuing a confirming buy signal. GLD closed today slightly lower at $115.11, good enough for a 2.8% gain in eight trading days. Stochastic and relative strength indicators are also positive. A decisive move higher above, GLD’s descending 50-day moving average would be further confirmation that gold’s typical yearend rally has begun and is for real.”

The major event is the Swiss Referendum on Sunday. Assuming it fails, the real test of seasonality described above will come next week. Friday’s action was scary enough – GLD fell by 2.6% & SLV by 6.5%. And gold miners fell more than Oil ETFs – GDX fell 8.7% & GDXJ fell 12% on Friday. Perhaps, people were getting out of the way after seeing how Oil & Energy stocks fell.

On the other hand, a big sell off could be a buying opportunity. Tom McClellan discusses an interesting indicator for Gold on Thanksgiving day in his GOFO Squeeze article:

- “Right now, all lease periods out to 6 months are showing negative rates, meaning that the lessors are willing to actually pay you to borrow gold from them.”

- “Only 4 other times in history has this 1-month lease rate gone negative, and all were associated with important lows for gold prices. This is a bit of an unusual time, though, because interest rates generally are low right now.”

- “Those of us who follow these lease rates typically compare them to the same term LIBOR rate (London InterBank Offered Rate). That helps to normalize the lease rates for what other rates are doing at the moment. Just recently, that spread has widened to the largest degree since the 2008 commodities bubble collapse.”

- “Thus far that squeeze has not started to matter much for gold prices. But we have a lot of history on these data, and every time a squeeze like this starts, it eventually leads to a sizable rally for gold prices in the weeks or months to follow. So I am confident that this one is going to “work” as well, perhaps after the Nov. 30 Swiss referendum on its central bank gold reserves.”

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter