Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Drivers of interest rates

Last week, we featured a prediction about what might happened to Treasuries on Monday, July 23:

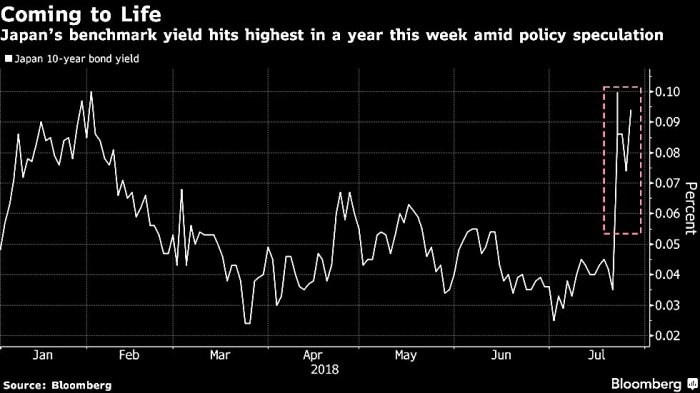

- Igor Schatz @Copernicus2013 – Fri Jul 20 – Huge move in 10yr JGB rate as they have erased 2 months worth of rally in last 3hrs.. this will likely put even more pressure on treasuries once Japan is back in the office Sunday night

$TLT$ZB_F

What happened on Monday? US Treasury rates rose up 6 bps across the 30-5 year curve. But not to worry, said Bank of Japan.

- Holger Zschaepitz @Schuldensuehner – Biggest experiment in monetary history: Intensifying speculation about tweaks to the Bank of Japan’s stimulus program saw 10y JGB yields briefly trading above 0.1% against the BOJ target of about zero BUT BoJ buying operation pushes bond yields back below 0.1%.

But US Treasury rates remained stubborn all week and the 30-year & 10-year yields closed at 3.10% & 2.98% on Thursday, their closing highs for the week. Perhaps that was in anticipation of the glorious Q2 GDP number. It did come in at 4.1%. But it had a silver lining for Bond bulls:

- Ryan Detrick, CMT @RyanDetrick – Strong GDP print gets the news, but don’t forget the core PCE came in at 2% in Q2, below expectations. Down from 2.2% in Q1. This is the Fed’s favorite inflation measure and suggests only modestly higher inflation.

So Treasury rates fell a bit on Friday, with the 30-year – 5-year yields falling by about 1 bps. That prompted:

- Kate’s Dad @KASDad – As a dumb equities guy, am a great believer in the bond guys being smarter. Treasuries rally on 4.1%

#GDP says only one thing to me. They think that is peak growth.$SPX$NDX$IWM

But how does a smart economist say it?

- David Rosenberg @EconguyRosieSo expect the economy to revert to this trend [real GDP growth of 2%, not 4%] as the cumulative effects of everything the Fed has done and intends to do hits the economy with the traditional lags. <2/2>

Who better to tell us about Fed’s intentions than the Fed when the FOMC meets on next Wednesday? Actually, next week promises to shed light on virtually all the factors that drive rates:

- Lawrence McDonald @Convertbond – Busy First Week of August Tue: BOJ + EU CPI and US PCE/ECI Weds: FOMC Thurs: BOE Fri: US jobs Via

@BearTrapsReport

2. Macro Outlook & Credit

One view of the Nasdaq, Commodities & Rates is the following:

Keith McCullough of Hedgeye is looking for the Nasdaq to make its first lower high in a while; he wants to be short of inflation not long. So he is bearish on Commodities. And about rates:

- Keith McCullough ✔@KeithMcCullough –UST 2YR – ramped to a new cycle high of 2.69% yesterday. This reflects both growth and inflation reports mapping towards cycle highs – the market believes that the Fed bites on these late cycle reports, hook-line-and-sinker

And,

- Keith McCullough ✔@KeithMcCullough – On the long end of the curve, which is making lower-highs, the market also believes the Fed will stay too hawkish too late = yield curve #inversion

But isn’t the most important factor corporate credit? If so, then one outlook is scary:

Rosenberg says:

- Something tells me that in the next six months we’re going to have a dramatic widening in credit spreads, … I know what happens at the tail end of every Fed tightening cycle; its getting to the tail end; the yield curve is telling you that;

- the corporate bond market is today’s bubble just like the mortgage market was the bubble back then; corporate debt to GDP at 45% looks hauntingly similar to what mortgage debt to GDP looked back in 2007; half the investment grade market is rated BBB; they are on the cusp of … mountains of refinancing risk ahead; a lot of these companies are going to be pushed into junk bond status …

- “You always know that the bubble that was created by the previous mass of monetary accommodation comes out of the wash. This time around I’m not even saying it’s the equity market, per say. It’s probably more in the corporate bond market,”

That brings us to stocks.

3. Stocks

With all the Central Bank talk ahead of us as well as critical data, we are leery of saying too much in this article. The biggest story of the week was the terrible action in FANG stocks, the leadership of the S&P this year. GOOGL blew away numbers but reversed lower on Friday. AMZN was not a great number and, perhaps appropriately, reversed its early morning gains to $1,888 to close at $1,816. Facebook & Netflix were punished after disappointing on earnings.

But why did Russell 2000 fall 1.89% on Friday and close below its 50-day moving average? Why did micro caps fall 2.06% on Friday?

- Peter BrandtVerified account@PeterLBrandt –

#classical_charting_101 This is potentially nasty price action in the$RUT$RTY_F

In Section 2 above, Keith McCullough said buy bond proxies & short financials, the leading sector of this week. Mark Newton doesn’t say short but posted a negative comment about Broker-Dealers:

In Section 2 above, Keith McCullough said buy bond proxies & short financials, the leading sector of this week. Mark Newton doesn’t say short but posted a negative comment about Broker-Dealers:

- Mark Newton @MarkNewtonCMT –

$IAI IShares Broker Dealer ETF snapping a minor uptrend of the last few weeks after bounce stalled out right at resistance of PRIOR breakdown#IBDPartner@Marketsmith shows volume lower today, but Extent of the technical breakdown makes this important and negative@IBDinvestors

Also,

- Pat Hennessy, CMT @pat_hennessy –

$SPX floor broker on this weeks trading – “Call chasing this week is approaching the January Ray Dailo ‘you’re an idiot not to own stocks’ mentality.”

But all these seem to be short term indicators, while one longer term indicator looks sanguine:

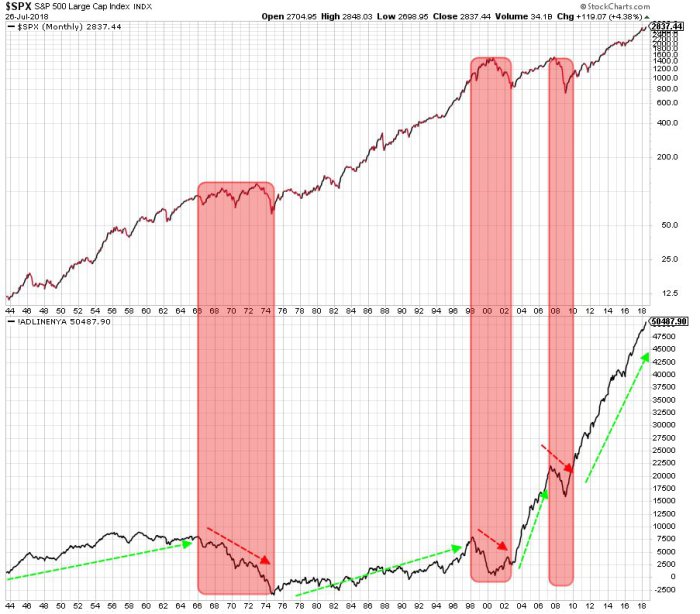

- Ryan Detrick, CMT @RyanDetrick – The NYSE advance/decline line made another new all-time high yesterday, even as one of the ‘5 stocks that account for all the gains’ dropped 19%. This one again shows how broad this market advance is, which should suggest continued gains in 2018 …

4. U.S. Dollar & Commodities

With the caveat that these asset classes are even more affected by Central Bank statements & critical data, here it goes:

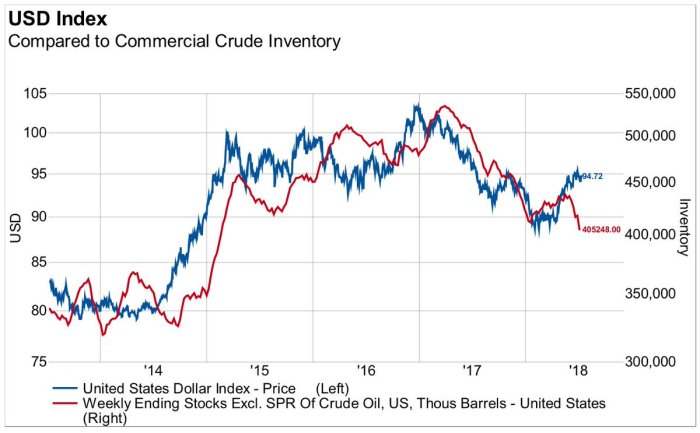

- Jesse Felder @jessefelder – The US dollar has been joined at the hip with crude oil inventories for the last few years. Inventories have turned down significantly in the last few weeks and are now at a new multi-year low. http://ww2.knowledgeleaderscapital.com/l/109202/2018-07-23/64sf3s/109202/69875/Quarterly_Q2_2018_Conference_Call_Version.pdf … by

@KLCapital

If the Dollar follows the falling inventory, then it should be good for Gold, right?

- Thomas Thornton @TommyThornton –

$GLD on day 12 of 13 with DeMark Sequential on downside. A tradeable bottom is near

What about a base metal?

What about a base metal?

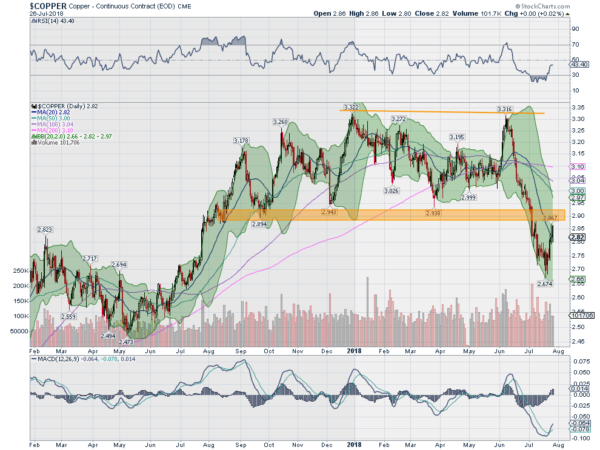

- Greg Harmon, CMTVerified account @harmongreg – dragonfly Capital – A Critical Junction for Copper http://dragonflycap.com/a-crit

ical-junction-for-copper/ … $HG_F$JJCB

He asks:

- The bounce is now approaching that prior support level that held it for the past 11 months. Will it act as resistance this time?

- Early indications suggest yes. The price has initially stalled at the retest of the break down. This happens often after a breakdown, a bounce to retest then continuation, in this case lower. The Bollinger Bands® are pointing down in a sharply descending channel. The RSI, a momentum measure, is stalling prior to giving a bullish reading. Only the MACD, crossed up and rising, looks promising. But that is correcting from a deeply oversold move. This could all change next week, but the onus is on copper to prove its strength by pushing through resistance. Right now that prospect looks dim.

What about the other incredibly important commodity? The above chart of Jesse Felder shows that Commercial Crude Inventories are down. So if the correlation works & the Dollar declines, shouldn’t that be positive for Oil? Greg Harmon of DragonFly Capital comes to that conclusion in his Thursday article Crude Oil Bubbling Up Again:

- “The [bubble up] move Wednesday brought it back to the 50% retracement and the 100 day SMA. Momentum has shifted, with the RSI rounding up at the mid line and the MACD leveling in positive territory. Crude Oil prices are now confirming a higher low. The Bollinger Bands® are tightening, often a precursor to a move. And a Measured Move would give a target to the upside to about 78.25. No guarantees in this life, but Crude Oil looks to be ready for the next leg higher.”

5. Simply Gorgeous

- Back To Nature @backt0nature It took 6 years, 4,200 hours and 720,000 photos for wildlife photographer Alan McFadyen to get this perfect shot. Kingfisher diving into the water.

Thanks to Mark Arbeter for retweeting this photo.

Thanks to Mark Arbeter for retweeting this photo.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter