Editor’s Note: In this series of articles, we include important or interesting videoclips with our comments. This is an article that expresses our personal opinions about comments made on Television and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. She took it all back

So Dr. Yellen never really made that “6 months” comment, right? There was no mention of it in the Fed minutes released this week. In other words, Dr. Yellen took it all back via the minutes. And the 5-year yield dropped by 8 bps from 1.66% on pre-minutes-Tuesday to 1.58% on Friday. This is close enough to 1.55% on pre-6-FOMC-Tuesday, March 18. So the market has seemingly taken it all back as well.

We say seemingly because the 30-year yield has fallen by 13 bps from pre-6-months Tuesday 3/18 to this Friday. Which means the 30-5 year yield curve has flattened by 10 bps from March 18 to this Friday. This brings the spread back in the direction of the the 32 bps flattening of the 30-5 year yield spread since 2014 began.

This flattening got the attention of GaveKal capital in their US Losing Currency War article of this week.

- “One of things that has gotten some attention lately is the spread compression in the long end of the yield curve. This looks to us like a classic deflationary configuration. Consider that: 1) nominal rates have been falling for both the 10 and 30 year bonds and 2) while nominal spreads have dropped by 37bps since last April, the inflation spread (or simply the spread between 10 and 30 year inflation expectations) has dropped by 51bps. This suggest to us that over 100% of the compression in long bond spreads is due to falling inflation expectations. This evidence points more toward the secular stagnation hypothesis of the US rather than the growth resurgence“

David Rosenberg for one has been scoffing at the “secular stagnation in US” hypothesis. He saw nothing that weak in the payroll number and he points to jobless claims that are “almost 50K lower than they are normally in an expansion“. So why is the Fed so afraid of talking about raising rates? He answered on Friday:

- “Central banks live in fear. They feel they cannot raise rates because that would burst yet another credit bubble and cause another recession, yet by maintaining negative real yields at the short end of the curve they are actually helping to create the very same problem of excessive debt creation we faced in 2008. History rhymes, after all, as Mark Twain warned. As such something tells me that this is the sort of environment that is going to have the gold bugs smiling from ear to ear down the road, if not right now.”

2. Excessive Credit Creation, did he say?

Rosie was almost red when he discussed the Greek bond issue of this week.

- “Greek bond issue being 5X oversubscribed at these yield levels… nobody wanted to touch them at 30% at the height of the crisis, now folks can’t get enough of ’em with a ‘5-handle’; last week we had a brief period where Spanish 5s’ traded through Treasuries “

Rick Santelli saw a positive message in this madness on Wednesday:

- “in my opinion, it is almost virtually impossible to see a huge run-up in U.S. rates. why? because are world investors truly going to pay up to a lower yield on a Southern European economy than on a ten-year note, it doesn’t make any sense. If the world stays as it is on this kind of weird-value trade, it will be a stopper for any significant increase in U.S. rates. So either U.S. rates have to come down, or Europe’s rates have to go up. There’s no other way to explain it.”

But you ain’t seen nothing yet was the message that Brian Reynolds of Rosenblatt Securities gave CNBC’s Kelly Evans on Friday:

- “in the credit market last two days junk yields have come down a little bit, people are buying high yield as equity investors selling like crazy. … it hasn’t mattered whether rates have gone up or down in the last five years. our nation’s pensions need to make 5.7% they are bringing in more money from the cities and towns that fund them & that’s the big thing that is driving this; the spread between optimism among credit investors and pessimism amongst stock investors has never been bigger.”

- “credit booms lead to bubbles elsewhere and … this credit boom is going to be so long and so intense that we have a real estate bubble coming in commercial real estate and those activities lead to higher stock prices while the credit boom is going on.”

In contrast, his segment-mate Larry McDonald sees a problem now:

- “so I sense that’s a tremendous amount of froth. In corporate funds we’re hearing about Covenant Light 2.0. – the standards given to investors are even worse than 2007 levels“

We would like to humbly point out that both in 2007-2008 & in 2000-2002, corporate & lower rated sovereign credit collapsed and all that money poured into U.S. Treasuries. .

Long duration treasuries were a standout performer this week with 30-year & 10-year yields falling by 10 bps each and the 5-year yield falling by 13 bps. The disparity between Treasuries rallying and stocks falling was such that Jim Cramer began calling TLT as “rally killer“.

Art Cashin was more explanatory in his comments on Friday afternoon on CNBC Closing Bell:

- “the flattening of the yield curve & what’s going on in the 10-year strongly hints that the economy may in fact be slipping & losing a little strength”

- “and of course with the 10-year we get the added bonus that its the litmus test for any geopolitical problems.. it will be important how they close here for sto

cks but the 10-year has guided us pretty well”.

3. U.S. Equities.

The stock market absolutely loved the Fed minutes it saw on Wednesday. They celebrated it with a 181 point rally more than making up for the 167 point loss on Monday. Then came the deluge of 267 points on Thursday. Was it the China-Japan data overnight?

Or was it the simple but inevitable realization that no matter what the Fed does, they cannot get this economy to recover strongly. We came into 2014 with confidence about the trajectory of the U.S. recovery and conviction about interest rates going up sustainably. That was tempered by the weather but now after last week’s payrolls number, no one believes the weather story anymore. In our opinion, the Yellen spectacle was a late late straw at least for now.

Dr. Yellen sounded confident in March and led markets to believe in speedier rate normalization. The payrolls number took away some of market’s confidence in her. But to see her do a complete take back of the “6 months” comment in the Fed minutes was simply too much. To see the Fed so dovish after so much QE is a scary proposition for us. It shows that they don’t have any confidence whatsoever in what they are doing. If Yellen & co. are living in fear as David Rosenberg wrote, then shouldn’t the markets be afraid too? This Wednesday’s shredding of trust in the efficacy of QE may have led to a capitulation in stocks on Thursday. That would be our bet for now.

The stock market is pretty oversold at this stage. And Thursday was pretty bad per Bespoke “The Nasdaq closed today [thursday] at its most oversold level in relation to its 50-day since November 2012.” Larry McDonald of NewEdge commented on the difference between the Nasdaq & S&P on Friday:

- “take the VIX volatility versus the Nasdaq volatility – we saw a two standard deviation spread this week for the first time since Lehman. That tells you there is de-frothing going on there and there’s potentially a near-term snap back rally and so much future volatility.”

And what would he buy? IBB the Biotech ETF:

- “the biotechs today made I think a near-term bottom on the IBB and I just see massive capitulation, we have a capitulation model that measures that, and I think there’s capitulation in a lot of these names.”

But Brian Kelly of CNBC FM would rather wait for IBB to get to $210 and see whether it bounces. If it does, then his “BK” persona would “perk up“, he said on Friday 5 pm edition.

Well known investor Bill Miller was unabashedly bullish this week on CNBC:

- “The conditions for a bad market just don’t exist,… I think after this correction you can throw a dart at the market and about anything you hit is gonna go up the next six months.”

But he did not say when or at what level he expects the correction to end.

Mary Ann Bartels of BAC-Merrill Lynch was more specific on CNBC Futures Now on Tuesday, April 11:

- “April showers bring May flowers; we have a little bit of rain in the markets but we are going to get flowers; this is an opportunity to buy the market. We still find value in the energy sector. It’s one of the most oppressed sectors, Industrials and Technologies, other select technology.”

- “we do a survey at Bank of America-Merrill Lynch called the global fund management survey and clients are sitting on cash, 4.8%. You don’t see markets go down even 10% when there’s that much cash on the sidelines.”

Her colleague Michael Hartnett wrote in his Hard Reversal report on Thursday:

- “Big correction in autumn not spring – High cash, low leverage…bull markets don’t end this way. We think bigger 10-15% correction more likely in autumn as Fed QE ends and rate hike expectations grow.”

Lawrence McMillan was cautiously bearish in his Friday summary:

- “In summary, the breakdown by $SPX is bearish. But it would be much more convincing if it were accompanied by a sell signal in volatility“

Dennis Gartman turned neutral on Monday and stayed that way as he told CNBC FM on Thursday:

- “I have gone to neutrality. … Friday, as I said, somewhere between 11:00 and 11:15 the switch got flipped. I still don’t know what that switch was, but something material happened on Friday. we continued on Monday, and today I’m sad to say devastating if you’re a long term bull. I still think the bull market is intact. I will not be short of stocks. It may be months before I am. Neutrality seems to be the right place to be and cash seems to be the right holding.”

Back on Friday, March 14, veteran trader Lawrence Altman told CNBC FM 1/2 that “trading pattern have changed dramatically from last year”. In his repeat appearance this Friday, he said that “something very important, the equation of the market has changed“. He added:

- “When I came on the show, it was March 14th – the S&P was trading 1,839. Nasdaq was trading 3,630, and Russell was trading around 118. Today, Russell’s 111.50, Nasdaq is down almost 200 points and the S&P is only down 20 points. … if the market’s going to have a correction, and the action is leading to that, they don’t really leave anything alone.”

- “something was very significant to yesterday’s close. you know, we took out last month’s high, which was an all-time high last week, and now we’re below last month’s low. now, that’s a pretty significant thing. off contract highs. i mean, if it happens in a week, that’s significant. but if it closes below 1,830, the S&P, for the month, you’re definitely going to test the 200-day moving average. And who knows where we’re going to go from there?”

When Carl Icahn speaks, we all listen, right!

Well he spoke on CNBC FM 1/2 on Thursday, April 10:

- “everybody loves this market … you talk in your barber shop and everybody is buying this, buying that and talking about it. That’s the time to be cautious. That’s not the only reason. The reason to be cautious, I think, is that a lot of the earnings are sort of artificial because, you know, the Fed did a great job in saving this country. but right now with these low interest rates it’s easy to make earnings. and I don’t think that can continue forever.”

- “I’ve said that before and I continue to say it. I think that there will be a major correction, but I don’t know when. it could be three years. it could be three days … but that’s my belief.”

Howard Rosencrans, founder of Value Advisory with Maria Bartiromo on FBN on Thursday, April 10:

- “not just the M&A and the IPO world that are in fantasy land but you have also got sentiment; you have a market that is now up 200% in 5 years; valuations are not a lot higher albeit sort of average over historical range; you also got very negative seasonal factors;2nd year of a presidential cycle, 2nd year of a second term; we are going to see 10-15% correction over the next 6-9 months;”

- “Sentiment here is incredibly positive, sentiment over there is incredibly negative, I like India first and foremost; I think China is cheap as well; we can debate whether Brazil is an opportunity; I am not rushing to dedicate capital to Brazil; you are going to see some improvement in some of the tertiary European countries which are just coming out of a horrible time;”

Obviously no one beats Marc Faber in being dramatic. And he outdid himself on CNBC Futures Now on Tuesday, April 8:

- “I think it’s very likely that we’re seeing, in the next 12 months, an ’87-type of crash,” Faber said with a devious chuckle on Thursday’s episode of “Futures Now.” “And I suspect it will be even worse.”

- “This year, for sure—maybe from a higher diving board—the S&P will drop 20 percent,” Faber said, adding: “I think, rather, 30 percent. Who knows. But all I’m saying is that it’s not a very good time, right now, to buy stocks.”

Back on March 12, Jeff Cooper said the following in a Minyanville article titled Did Yesterday Mark a Market Top?:

- “The big picture indicates the possibility of a third leg down within the context of a 13-year Broadening or Megaphone Top formation. Theoretically, that implies lows below the March 2009 low. A third leg down could see a decline hold between 740 and 1100 S&P to carve out a major inverse right shoulder”

This Thursday morning, he tweeted:

- Jeff Cooper @JeffCooperLive – as shown in Daily Market Report throughout March, the pattern before the deluge in ’87 was a one day turn up in dailies that defined a high

Then came the following tweet:

- Minyanville @Minyanville – Jeff Cooper: Are We Facing a Bigger, Stronger, Faster 1987? minyanville.com/

business-news/ markets/articles/monthly-s2526p-chart- … pic.twitter.com/YLyHKYgVSUGreat-Depression-Daily/4/11/ 2014/id/54564

The macro gist of his detailed article is:

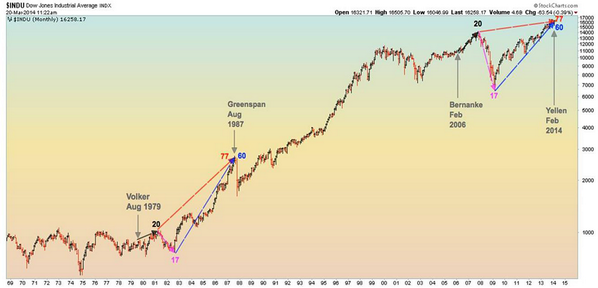

- “New Fed chairs are usually tested by the markets with a 16% correction on average in the first year. Yesterday may have begun a similar test for new Fed Chair Janet Yellen as the cascade setup warned about earlier this week [subscription required] seems to be unfolding on trade below the March low and the 50-day moving average.”

- “On Thursday April 10, Yellen tried to jawbone the market, and a few hours later, the market landed a left hook on the bull’s jaw. I can’t remember when I’ve seen two such breathtaking reversals in a span of just four days.”

What about positioning & sentiment?

- Charlie Bilello, CMT @MktOutperform – Would have thought with damage to small caps/momo names active managers would have cut exposure, hasn’t happened yet. pic.twitter

.com/iqsXnnnnhV

4. EM, US Dollar and Gold

One of the best equity trades of the past month or so has been Long EM & Short SPY. When was the last time, EM equities were a safe haven for those fleeing S&P 500? Does it go to show it is all about positioning? After all, after the carnage in EM in January-early February, they were very long S&P and very short EM. Have they reversed that positioning? We don’t know. But the flows have reversed massively as Michael Hartnett of BAC-Merill Lynch wrote in his The EMpire Strikes Back report on Thursday:

- “Capitulation back into EM: largest weekly inflows to EM debt & equity funds in more than a year ($4.7bn combined ). The flow differential between DM and EM equity funds reached an extreme 98th percentile in Mar’14 .”

Source: BofA Merrill Lynch Global Investment Strategy, EPFR Global

Is Gold a risk asset or is it a safe haven asset? We don’t know. We did notice that Gold went down when stocks sold off. May be it is simply a margined asset. We cannot find anyone who understands why Gold is behaving the it is and how it will trade going forward. It used to sell off when the U.S. Dollar rallied. Will it still do so? We shall know if and when the U.S. Dollar rallies. And why might it rally or at least bounce?

$USDOLLAR net spec futures positioning is the most extreme since 2/22/13:http://stks.co/h0Uem

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter