Editor’s Note: In this series of articles, we include important or interesting tweets, articles, videoclips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Pattern continues

Last Friday morning we stopped worrying about Iraq and so did the stock market. We were dumb to wonder last week whether the stock market would follow its current pattern and rally to a new highs. Of course it did. In fact, the Dow and the S&P rallied every day this week.

Chair Yellen will get the credit but we would rather give the credit to the lead horse – Mario Draghi. The way we see it, the tone of all financial markets changed when Draghi served notice on May 8. Chair Yellen backed it up this Wednesday by merely moving “from extremely bullish to just bullish” in the words of Larry Fink. She proved to be a worthy wing woman to Draghi by suppressing VIX to 10.60 with her press conference on Wednesday, a 10% drop from just last Friday. How did the volatility ETF close on Wednesday?

- Wednesday after-market – Ophir Gottlieb @OphirGottlieb $VXX has hit an all-time low and is down 99.52% since originally listed (pic) pic.twitter.com/Z9lyLu8sFo

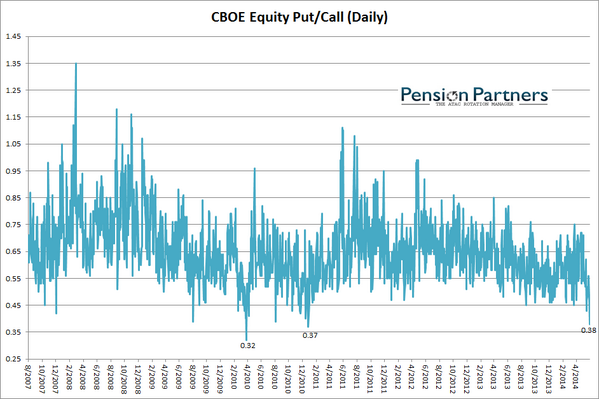

Conversely, how bullish were investors?

- Wednesday after-market – Charlie Bilello, CMT @MktOutperform – 6th lowest equity put/call ratio in history today @ .38. Just an incredible amount of bullishness out there. pic.twitter.com/dYBmHGNgHx

BlackRock had predicted rise in volatility this year and asked clients to buy cheap protection in December 2013. Why didn’t CNBC Squawk Box anchor squad ask Larry Fink about that prediction in their hour long conversation on Friday morning?

Shouldn’t EM currencies be doing well when both the US Dollar and the Euro are being debased by their central banks? They are not according to:

- Wednesday post-Fed statement – J.C. Parets @allstarcharts – Emerging Mkt currencies vs Dollars coming off double top & broken trendline. Now @ support $CEW $UUP http://stks.co/p0RtQ

Since Chair Yellen is a labor economist and deeply concerned about the job market, we thought we would insert an interesting tweet & story that we found this week. And yes, it merges the concept of asset rich millionaires & the paucity of jobs:

- Name withheld – Just how bad is the academic job market? “Yes, I am a stripper with a Ph.D. I own that, and I’m proud of that.” goo.gl/LcVead

This is an interesting interview with the Ph.D. stripper especially the excerpt below:

- “My strip club caters to a very high-class clientele, and I use the Ph.D. schtick all the time, when I sense the customer might like it. These men are often millionaires, and are interested in a woman with some culture. These men are the best catches—love them!—because they just want to talk. … With these men, I will usually talk Faulkner topless for $600 an hour.”

Her last academic job paid her $16,000 annually, she said.

2. Gold & Silver

Last week we called Gold & Silver the stars of that week. They acted like meteorites this Thursday. Gold rallied by over $40 on Thursday alone to close up 3% on the week. Silver, perhaps for the first time this year, is outperforming Gold with a rally of 5%+ on the week. The miners were up 9% (GDXJ) and 8% (GDX) by Thursday. But GDXJ gave up half its gains on Friday.

Clearly what Dr. Yellen said in her press conference lit a fuse of short covering. Perhaps the man who said Buy GDX for a short term trade on June 2, 2014 turned with the huge rally on Thursday & tweeted:

- Lawrence McDonald @Convertbond – Time to lighten up on the #gold miners friends, most overbought since August 16, 2013

He followed up on Friday morning with a formal recommendation in his Bear Traps newsletter. This is more of a risk management move and he still likes GDX vs. S&P.

On the other hand, George Gero of RBC called it a “repricing” of gold on CNBC Street Signs on Friday and said the repricing gets to $1350 area. His reason – most portfolios are “woefully underweight” Gold.

Keith McCullough of HedgEye has been bullish on gold all year. He said in his What’s the next stop for Gold videoclip on Friday:

- “mid 1300s much more probable than sub-1200; If Gold gets over $1336, it gets to $1380 in fairly short order. looking for gold to test this year’s high”

Market Anthropolgoy wrote on Friday in their Beware Fury of Patient Position:

- “We would also caution anyone connecting the recent moves in precious metals directly to the latest geopolitical concerns in the Middle East, because the typical performance markers of those special situations are simply not present. Namely, the silver gold ratio has been trending higher

– which is more indicative of a reflationary bid than fear. Typically, in a more geopolitically driven move, gold will strongly outperform silver as a safe-haven reaction to those concerns.” - “The bottom line with respect to silver and the precious metals sector in general, is that conditions have only improved in the space over the past year – while their respective market structures has been trending to resolution.”

3. Oil & Gasoline

Oil has been a strong performer with Brent outperforming WTI as everyone would expect given Iraq & Ukraine. The tweet below is indicative of what we heard from many.

- Friday – John Kicklighter @JohnKicklighter – Having overtaken 114, Brent crude may have broken a six-year wedge pattern: stks.co/f0k4H

Source – www.mcoscillator.com

- “… there is big disagreement among the different oil futures contracts across the maturity spectrum. The near month contract, which is currently the July 2014 contract, is priced at $106/barrel. But if we go out to the June 2015 contract, it is $9 lower.”

- “So now we have a condition where the potential energy of the backwardation condition says prices should head downward, and we have a very low volatility condition which suggests that a trending move should unfold in some direction. My conclusion is that a big down move is coming for oil prices. We just need to have peace break out somewhere to make that happen”

But Gasoline is different from oil. So is there any one who can tell us where gasoline will go and when? Thanks to CNBC Closing Bell, we found one, a guru so bold & so certain that he put aside the old wisdom of never predicting both price target & time frame at the same time.

That guru is Kent Moors, Money Map Press global energy strategist. And he told his old friend Bill Griffeth that Gasoline will go to $4 in most of USA by Friday of next week:

- “first & perhaps most important is what is occurring at the Baiji refinery in Iraq; that is the largest refinery in Iraq; it services only the domestic market but that knock-on effect is going to be rather significant; we are already beginning to see indications of accelerated volatility moving forward in very near term futures contracts. So the price of gasoline can only be going up in the United states – We will see $4 in many regions of the United States as early as this time next week”

Why is ISIS so focused on the Baiji refinery when they already have $2.3 billion*? Moors explained:

- “the strategy here by ISIS is not to control the export flow – strategy is to immobilize the current Shiite government in Baghdad – if you do that, those companies that are producing the oil, those companies that are exporting the oil no longer have a central government guidance upon which they need to act – at that point prices become exceptionally unstable”

And what does Moors think about the current government in Baghdad?

- “I can tell you as of this morning it is virtually a certainty that this government in Baghdad will not survive the convening of the new parliament in the first week in July. Mr Maliki is virtually gone“

So there is no one to take any decisions in Baghdad? Talk about a confluence of “uncertainty perception factors” to use a term of Kent Moors! By the way what did the Baiji refinery look like last night NY time?

* the $2.3 billion figure comes from Martin Chulov of the Guardian – His article is a must read in our opinion. .

4. Treasuries

The volatility in the Treasury curve, especially the 30-5 year spread, was intense between the Fed statement on Wednesday & Yellen’s press conference and after the press conference into the close. A mirror into that volatility is the tweet below on Wednesday afternoon:

- Yield Curve @TenYearNote – UST Market right now: Adult Swim Only

The emotional action in the Long bond post-Fed on Wednesday afternoon was reflected in the tweets below:

- Jeff Kilburg @TheKillir – #30yr Long Bond back making new highs after buyers got absolutely punished off of initial grab post release #FOMC

- Michael A. Gayed,CFA @pensionpartners – Long Bond to Yellen: I got your taper…RIGHT HERE $TLT

The long end continued the rally on Thursday morning until the stronger than expected Philly Fed number hit the tape. The rally reversed with that number and turned into a sell off after a mediocre TIPS auction at 1 pm. The 30-year yield rose by 5bps by Thursday’s close giving up more than what it had gained on Wednesday.

After all this, the Treasury curve closed flattish on the week except for the 30-year yield which fell by 2.4 bps. The channel that had been in place for TL

T between March & June has been broken to the downside. On the other hand, TLT did regain its 50-day moving average on Friday. Does this spell data dependency or inflation fears?

What Dr. Yellen decidedly did is to drive yields down in the short end of the Treasury curve. The 5-year & 3-year yields fell by 5 bps from Tuesday’s close to Friday’s close.

5. U.S. Equities

What can you expect but calls for a secular multi-year bull market after a go-ahead from Chair Yellen? We got two such calls on Friday from two smart gurus:

- Mary Ann Bartels of BAC-Merrill Lynch on CNBC FM 1/2 – “the pain trade is still high. and we’re seeing a melt up and we see bullish through May, we never said sell in May go away. this is the most hating bull market i have seen and what people do not understand and this is very important. we went into a new secular bull market last year. It is 1982 all over again. Markets can go up for 13 years. You will get bear markets but until you get everybody in you can’t get these markets down. The only other worry is if crude oil spikes because of Iraq.”

- Jeff Saut of Raymond James – we are overbought on a short term basis with very stiff overhead resistance . I think you could get some kind of pull back, don’t think it will be much, I still think we are in a secular bull market that has years left to run

A similar note came from Lawrence McMillan in his weekly summary on Friday:

- “Once again we see that nothing really can stop this bullish market. … In summary, all of our indicators are bullish (there are no sell signals in place at this time), and we thus remain intermediate-term bullish. Overbought conditions might produce a sharp, but short-lived correction at any time“

The only lukewarm note we heard was from Larry Fink on Friday morning when he said, as we recall,

- “Europe may melt up not US.. US market may go up a couple of % by year end … like stocks over bonds.”

We could not find any one tweeting or talking about a top in the market. Is that a contrary indicator for next week?

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter