Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Confused?

The tweet series below seems to sum up the action in all markets:

Friday – Urban_Carmel @ukarlewitz –

- You’d think investors would be worn out, but II bull ratio back over 4x and equity inflows 6 weeks in a row … 2015 so far. SPY essential flat. January oscillated up and down by 5% 5 times in one month. Feb was up then up 3 weeks in a row… followed by a 3 week drop into March. Then a 3% rally last week. Followed by close to a 3% drop this week.

Interest rates are behaving similarly. And the most definitively acting asset class, the U.S. Dollar, is now acting indecisively. Is it about the economy or is it about the Fed? Virtually all data except employment numbers are “not strong” to use a Greenspanism. It seems the asset classes have accepted Vice Chair Stanley Fisher’s declaration that interest rates will rise in 2015. But there is a big tactical difference between July & December. Now that “patient” is gone, all data is being analyzed to get a handle on the July-September-December decision. A data-dependent view is:

- Friday – Lawrence McDonald @Convertbond – Rate Hike When? US GDP – Q1 2015: 1.5%*,

Q4 2014: 2.2%, Q3 2014: 5.0% *Tracking #Fed

McDonald went on to add on CNBC Closing Bell on Friday that the Fed remains concerned about the Dollar. Another view seems to argue that economic data is sort of irrelevant to the Yellen Fed which is reportedly determined to get out of the ZIRP trap. This view leads to the probabilities in the table below from Charlie Bilello of Pension Partners:

His rationale:

- “They [Fed] cannot serve two masters and they have shown time and again that they will choose the short-term movement of the stock market over the real economy in making policy decisions.”

2. U.S. Treasuries

The week began with massively bullish 1.5% 10-year yield predictions by Sri Kumar on BTV Surveillance on Monday and Phil Orlando on CNBC Power Lunch on Tuesday. The low closing yields of the week were on Tuesday. That action led to the following observation on Tuesday after the close:

- Tuesday – Dana Lyons @JLyonsFundMgmt – 10 & 30-Yr Yields testing 61.8% Fib Retracement of Feb-Mar bounce = important spot. Interesting Utilities not following suit. $TLT $XLU $TNX

Treasury yields fell below their October 2014 crash lows of 1.86% on 10s & reversed almost immediately. Between the lows on Wednesday morning & Thursday’s close, the 10-year yield shot up by 14 bps and the 5-yr yield by 12bps. It was almost those levels were scalding hot and led to fast heavy selling. Rick Santelli opined that the October flash crash lows were like fair value and led to retracement. About 40% of that rate rise was reversed on Friday. Next week should bring some clarity & perhaps a trend with ISM & payroll data. BofAML clients seem clear in their minds already:

- Wednesday -StockTwits retweeted – Julie VerHage @julieverhage – BofAML client survey shows 85% expect US 10yr yields to end year higher..but we all know how that played out last yr

3. U.S. Equities

First the positive or semi-positive observations:

- Friday – Chad Gassaway, CMT @WildcatTrader – When the SPX closed lower for four sessions then closed higher on the 5th, it added to gains 2 days later 13 of 14 times since 2010.

- Friday – Chad Gassaway, CMT @WildcatTrader – DSI fell to 26. Nearing extremes. Market has typically found a bottom somewhere between 10 and 20

- Thu – Antony Filippo @Vconomics – Despite this week’s carnage, the Russell 2000 is technically still a longer term buy. http://bit.ly/19US2lg

Back on March 9, Jeremy Siegel sounded cautious about stocks. This Friday, he told CNBC Squawk Box anchors that he feels a lot better about stocks despite the choppiness he expects in the near term. His target for fair value remains 20,000 for Dow.

In contrast, a usually bullish Jack Bouroudjian was cautious on Wednesday:

- “We are getting very close to the end of the quarter; a lot of what you are seeing today is a large footprint of what looks like profit taking; they are selling everything across the board; and if you look at what they are buying, they are buying whatever they were short – oil; that tells me this is end of quarter type of action; the real questsion is what we see happening in the beginning of the next quarter; we are entering a very difficult time for stocks; I do get cautions in the first couple of weeks in April & October; this is the time to put out protection & look for that 5%-7% move; it can come very very quickly”;

A similar point was made by:

- Friday – Urban Carmel @ukarlewitz – The 1st two wks of April are supposed to be strong, but they’ve been crap the past 4 yrs. 2nd half of month better

Steve Grasso of CNBC FM was more explicit & far more negative about the quarter end on Friday:

- “we are quarterly overbought in S&P; If we close negative for the quarter on Tuesday 3/31, then we will have a negative overbought quarter which happened in 2000 & 2007”

Grasso didn’t only talk. He said on air that he had sold all his stocks.

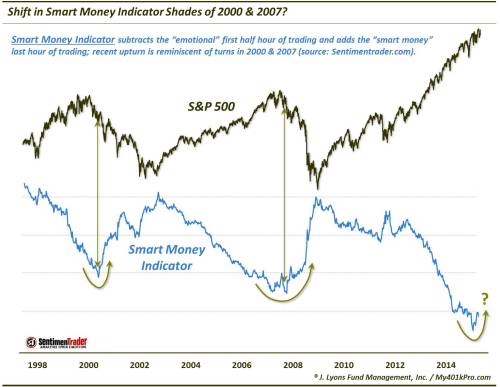

Another indicator (of Jason Goepfert at SentimentTrader.com) that brings up 2000 & 2007 was discussed by Dana Lyons in his article This shift in a Smart Money indicator may be negative for stocks.

If this is not enough, how about a double top?

- Thursday – Northy @NorthmanTrader – Unless we get a miracle rally into month end, the monthly $OEX shows a double top

James Paulsen has been bullish on stocks for years. He turned cautious last year and remains so:

- “I think we’re going to get through this, but I think the market’s vulnerable with a little too positive sentiment, a little too high valuations, and a need to reset rates; Until we deal with those, I think it’s going to struggle and remain volatile”

His main concern is Greenspanish:

- Most post-war bull markets have been associated with better-than-average productivity growth. This has not been one of those, … If we don’t get that, then I’m a little concerned about the longevity of the recovery”

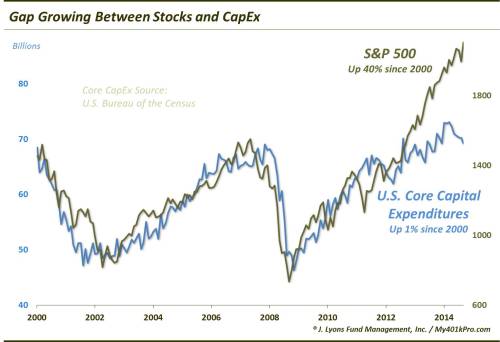

If you think productivity has anything to do with capex, then look at the chart below from Dana Lyons and read his article Gap Widening Between Stocks & CapEx

Those worried about an imminent bear market in stocks might want to read Tom McClellan’s article No Bear Market Signal Yet From Housing:

- “Before each of the really ugly bear markets of the past 30 years, there has been an important signal from housing data well ahead of time. We do not have such a signal now, and so that portends more upside in the months ahead for stock prices“

4. Oil

This, by far, was the most in the news asset class this week. As such it was the most volatile with USO up 2.13%, up 6bps, up 3.39%, up 4.90% from Monday to Thursday and then down 5.88% on Friday. The big question is whether oil has found a bottom.

- Dennis Gartman on Monday on CNBC FM – It does look like we very likely very possibly have seen the bottom – we have seen the term structure begin to change, the front month gained upon the back months, you had an outside reversal in crude last week and now you are starting to have outside reversal weeks occuring, you are getting a change in the dollar; I think the time has come to change; interesting you traded higher today after overtly bearish news from Al Naimi who started the oil market on the downside today, yet the market closed higher; one of the oldest rules in the trading book is that a market that gets bearish news & doesnt go down may not be bearish any longer; outside revesal days, outside reversal weeks, changes in the Dollar & the term structure shifting,

- Darren Wolfberg of BNP Paribas on Thursday on CNBC Futures Now – I think we are in the process of creating that floor; we are in a range right now – 44-54; if we get thru 54 to the upside, I think 60 is going to be the next level in the cards & we are almost close through refinery maintenance; once that is behind us, we are going to start seeing these inventories go down,you have seen the rig count come down significantly, so right now I am tempted to say that we have seen the bottom but we could see one more flush; either way I don’t see going to new lows; … we are looking at a recent uptrend; kind of that 48-50 level is an important level for us; breaking thru there would open up the bottom of the range, the 44 level; if we get through 52, then if we get through 54, then 60 is the next point;

The most interesting tweet was on Thursday afternoon:

- StockTwits @StockTwits – If crude oil reverses now, it will form one of biggest swings in energy market history -> http://bit.ly/OilReversalMarch ….

The biggest in history comment makes sense when you click on the link which featured the comment & chart below:

- Thursday morning – KimbleCharting Chris Kimble – Largest “monthly” bullish wick in History? Will see if so, come next Tuesday! $USO $XLE $XOM $XOP

On the other hand, Bear Traps of ACG Analytics put out a Sell USO & BNO on Friday morning. That proved prescient by the close on Friday.

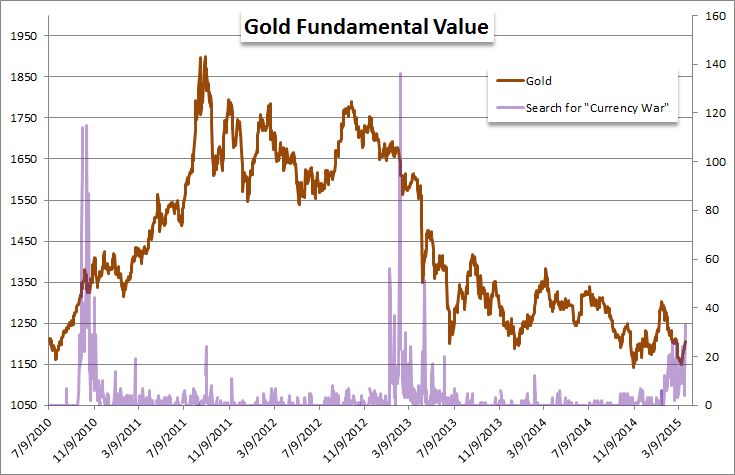

5. Gold

What moves gold? We haven’t found any one who knows. Is it the Fed?

- Bespoke @bespokeinvest – Spot gold was down 9 sessions in a row 3/2 to 3/12. It’s now been up 7 in a row since 3/18.

What happened on March 18? Chair Yellen surprised markets with her dovish view.

- Friday – John Kicklighter @JohnKicklighter – Irony there’s more evidence of concerted exchange rate manipulation (currency war) than ever, but gold struggles:

MacNeil Curry of BAC-ML bravely gave both a target price and a time frame this week. He called for Gold to rally to $1307 in the next couple of months:

- “rates are headed lower & dollar is likely to remain in a corrective sequence, gold should rally in that environment; price action says that; gold made its lows back in November; it went from 1132 to 1307 & through out that time, the Dollar index actually rose from 87.5 to almost 95; so the big thing is we are going to see continued breakdown in the negative correlation between gold & dollar over the course of next couple of weeks; if you look at the price action, gold should resume higher; 200-day at 1238 is a pivot & on the downside, the big support is 1143 – March 17 low”

Curry seemed to assume congruent action from both US Dollar and Treasury Rates. What if yields ramp higher and the Dollar resumes its rally? Curry was not asked on CNBC Futures Now and didn’t say.

6. U.S. Dollar

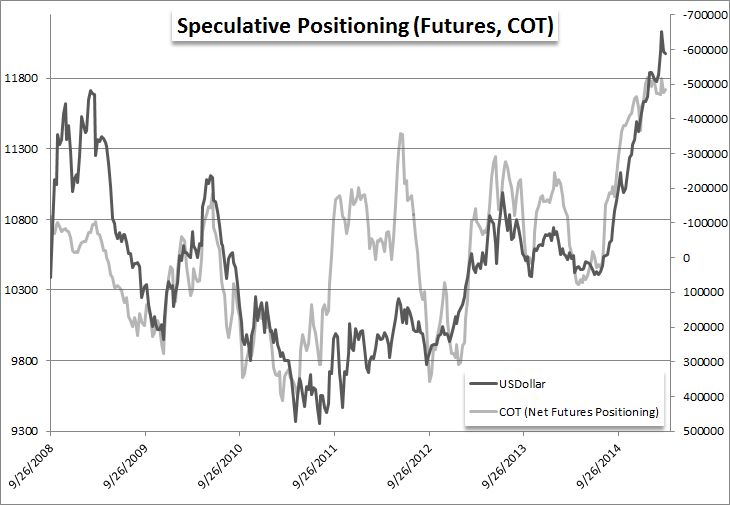

Everything seems to be a FX trade these days. So what did the large speculators do in response to the FOMC meeting of last week?

- Friday – John Kicklighter @JohnKicklighter – Despite the $USDollar’s volatility in response to last week’s FOMC, spec futures positioning was little changed

MacNeil Curry called for choppiness in the Dollar in the near term. Dennis Gartman was more explicit on Monday on CNBC FM:

- “I think you actually have seen a top in the US Dollar that may be rather material for a long period of time; you had an outside reversal to the upside in Sterling last week; you had reversals for the Dollar against Canadian Dollar, Australian Dollar, against the Kiwi, you had changes in the Dollar relative to Remnimbi, things are shifting in the FX market; that has been one of the driving forces in all the capital markets; suddenly in the past 5,6,7 days you can sense a change taking place”

On Friday, Forexlive.com wrote Seven Reasons to Sell USD/JPY:

The most overlooked action in Japan has been the behavior of the Japanese bond market. Is that material or is it just internal to Japan, internal to the Japanese bond market that is mainly internally supported in Japan?

7. Seinfeld still fits

Amazing how Seinfeld episodes still fit! Read the tweet-exchange below from Monday:

- Sara Eisen @SaraEisen – the only thing I like better than peanut butter cups is Dark chocolate peanut butter cups

- Francine Lacqua @flacqua – @SaraEisen why don’t white chocolate peanut butter cups exist?

What Seinfeld episode immediately comes to mind?

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter