Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.China & EM

On most NFP days, we would give the pole position to the NFP number. But not today. Not merely because the reaction in markets was “meh”, but because the worries we saw expressed in graphic terms. Last week we highlighted FCX as the stock we look at to figure out whether markets think China is positive or negative. The chart as of last Friday was simply awesome.

Well, this week FCX fell by 16%, USO fell by 3%, BNO by 4.5% and EEM, the Emerging Markets ETF, fell by 5.6% vs. a mere 40 bps fall in the S&P. Massive underperformance.

- $hane Obata @sobata416 – China commodities selloff deepens, as steel posts worst week since 2009 http://reut.rs/1OgnDv0 via @AlanFournier

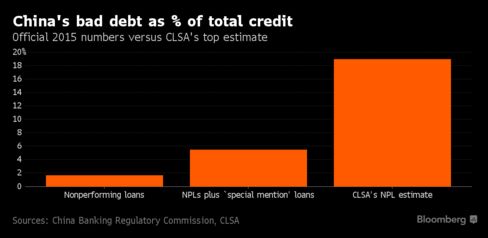

But that may merely be the symptom. Look at the Bloomberg article titled CLSA Sees China Bad-Loan Epidemic With $1 Trillion of Losses. The message in summary

- Chinese banks’ bad loans are at least nine times bigger than official numbers indicate, an “epidemic” that points to potential losses of more than $1 trillion, according to an assessment by brokerage CLSA Ltd. … “China’s banking system has reached a point where it needs a comprehensive solution for the bad-debt problem, but there is no plan yet,”

One trillion in losses seems huge unless you focus on a $25 trillion number. Wouldn’t that bring to mind horrors of an earlier period?

- A Evans-Pritchard

@AmbroseEP – This IIF report on corporate credit excesses frankly scares me. Starting to have same sick feeling had in early 2007http://www.telegraph.co.uk/business/2016/05/06/warnings-mount-on-worlds-corporate-debt-china-crisis/ - Corporate debt has reached extreme levels across much of the world and now far exceeds the pre-Lehman financial bubble by a host of measures, the global banking watchdog has warned in a deeply-disturbing report.

- “As the credit cycle ages, following years of record-setting bond issuance, there are growing concerns about signs of stress in corporate balance sheets,” said the Institute of International Finance in Washington.

- The body flagged a double threat: a five-fold rise in company debt to $25 trillion in emerging marketsover the past decade; and record junk bond issuance in US and Europe, along with shockingly-irresponsible levels of US borrowing to buy back shares and pay dividends.

- “We are far from out of the woods, given new risks and headwinds on multiple fronts,” said Howard Lee, the body’s executive director. “There is the threat of a disorderly pullback in capital out of the region.”

- Mr Lee said the exodus of capital at the beginning of the year – mostly driven by fears of a Chinese devaluation – may be a foretaste of what is to come. “The next episode may be even more damaging given the financial imbalances built up over the past few years,” he told a forum in Hong Kong.

- “While the region has become a key driver of growth globally, this has come at the price of a pretty dramatic rise in debt fueled by easy global liquidity,” he said. “As we have witnessed in advanced economies, disorderly deleveraging may weigh heavily on the economy and may even risk the financial system.”

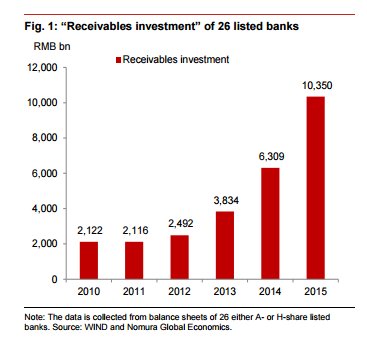

But wasn’t 2007 about the banking system?

- A Evans-Pritchard @AmbroseEP – This is a good proxy for growing risk in China’s banking system, from Nomura today. Latest mini-boom to end badly

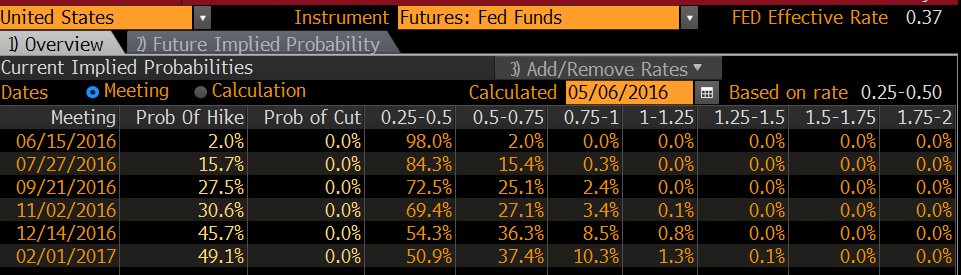

2. “They are pricing out the Fed for the year”

So said CNBC’s Steve Liesman after the tepid 160,000 NFP number, a big miss of the 220,000 expectation.

- Charlie Bilello, CMT @MktOutperform – After payrolls, market is saying no Fed hikes in 2016 & only a 49% chance of a hike in Feb 2017. Dovish expectations

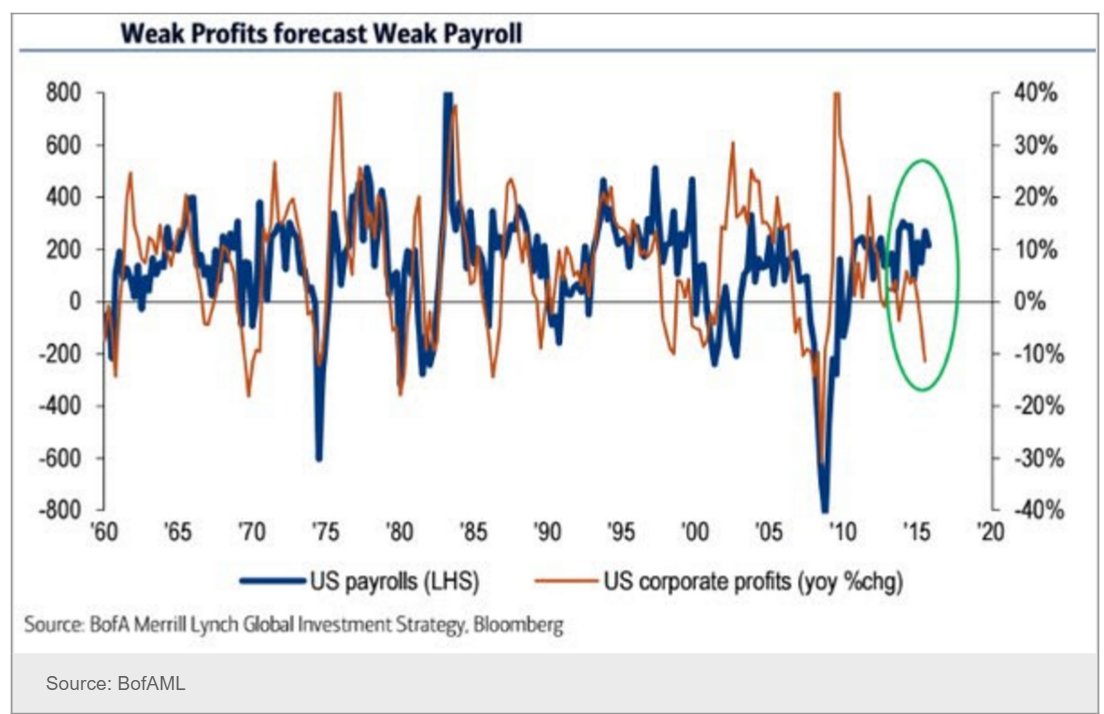

- Carl Riccadonna @Riccanomix – The corporate profit deterioration is an auspicious sign for the medium-term hiring trend.

- Contrahour @Contrahour –@Peter_Atwater @JustinWolfers Profits also not a bad leading indicator

- “Recession risk is rising with big allocation implications – today’s ADP report is worst in three years! Add to this that Fed broad based employment index (# 19 data points) is also making new lows and we have potential for dramatic change in MAIN MACRO concern: I.e: concern will be recession risk.”

- “If Non-farm payroll on Friday confirm today’s ADP number then we could start a big move towards NEW LOWS in US yields…. this would also help EURUSD and Gold higher, but main move would be in fixed income where the market in my opinion is net SHORT”

3. Treasuries

May be so but markets act perversely, don’t they! Right after the NFP number, yields did fall hard with the 10-year yield touching 1.70% only to reverse hard to close at 1.78%. Treasuries did come in somewhat overbought into the NFP number and so Friday’s reversal could simply be profit taking. Despite Friday’s reversal, the yield curve moved lower 4-5 bps in parallel this week. The big change was in German 30-yr & 10-year Bund yields which fell 17 & 14 bps resp.

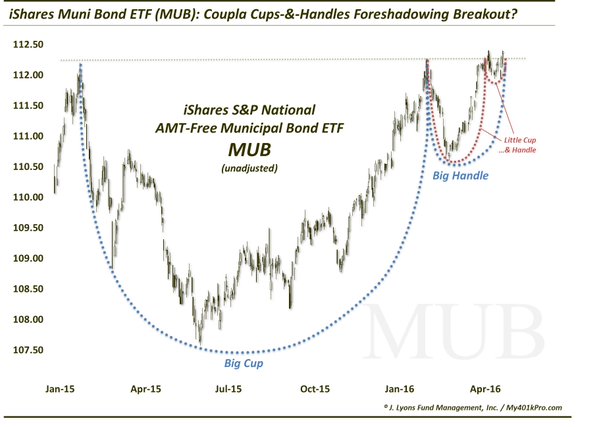

If Treasuries are good, shouldn’t Munis be better?

- Dana Lyons @JLyonsFundMgmt – ChOTD-5/5/16 Coupla Cups-&-Handles A Bullish Sign For Muni Bonds? $MUB

4. Real Macro Views

Rarely do we get absolute clarity from the absolutely successful investors. This was such a week. Thanks to the SOHN conference, we heard from Stanley Druckenmiller & Jeff Gundlach.

4.1 What part of get out of stocks did they not understand?

Was reportedly what Druckenmiller said when asked for a concrete recommendation. His views as reported:

- “I now feel the weight of the evidence has shifted the other way; higher valuations, three more years of unproductive corporate behavior, limits to further easing and excessive borrowing from the future suggest that the bull market is exhausting itself”

- As bankers experiment with “the absurd notion of negative interest rates,” Druckenmiller said, he’s wagering on gold. “Some regard it as a metal, we regard it as a currency and it remains our largest currency allocation”

- central bank has borrowed more “from future consumption than ever before.”

- “By most objective measures, we are deep into the longest period ever of excessively easy monetary policies, … Despite finally ending QE, the Fed’s radical dovishness continues today. By most objective measures, we are deep into the longest period ever of excessively easy monetary policies. In other words, and quite ironically, this is the least ‘data dependent’ Fed we have had in history.”

- Druckenmiller said “volatility in global equity markets over the past year, which often precedes a major trend change, suggests that their risk/reward is negative without substantially lower prices and/or structural reform. Don’t hold your breath for the latter.”

4.2 Buy Mortgage Reits & Short Utilities

Was the trade suggested by Jeff Gundlach. In a bit more detail:

- “Sell the utility index and go long mortgage REITs, which in part could be a mean reversion trade as the utilities have been outperforming year to date. Utilities now have high price-to-earnings ratios, while REITs are a value, he said. Utility stocks have been rising while REIT stocks have been down. The best trade execution is through sector ETFs: iShares Mortgage Real Estate Capped ETF — ticker REM — and the Utilites SPDR — ticker XLU”

What about US stocks?

- “egregiously overvalued versus other stock markets…. fundamentally, it’s very hard to believe in US stocks. Earnings and profit margins are dropping and companies basically are borrowing money to pay dividends and to buy back shares.”

What about Gold?

- “Gold is doing fine. It’s preserving capital in the US, it’s been making money over the last couple of years for European investors. That’s why I own gold. Because in a negative return environment anything that holds its value or makes a little is good.”

What about Oil?

- “Now it’s having a very hard time getting to $45. It bounces up a dollar, down a dollar and I think if oil is going back down to $ 38 people are going to be very concerned“

5. Stocks

With all the luminaries telling people to get out of stocks, wouldn’t it be ironic if stocks rallied hard next week? After all, it is “Sell in May” and “Go Away” period isn’t it? Not in the 2nd term election year according to Tom McClellan who wrote:

- “May 1 is actually not the ideal time to exit in a 2nd term election year. That point is actually in June to July. … May in a 2nd term election year actually sees a bottom mid-month, and then a rally up into June and July. The final top of that rally is ideally due July 10“.

And he had remarked on Thursday that “No daily Arms Index reading above 2.0, but 10-day look shows oversold“.

- Lawrence G. McMillan

@optstrategist – The next support level at 2040 looms large. If taken out, a larger correction will unfold http://www.optionstrategist.com/blog/2016/05/weekly-stock-market-commentary-5616 …

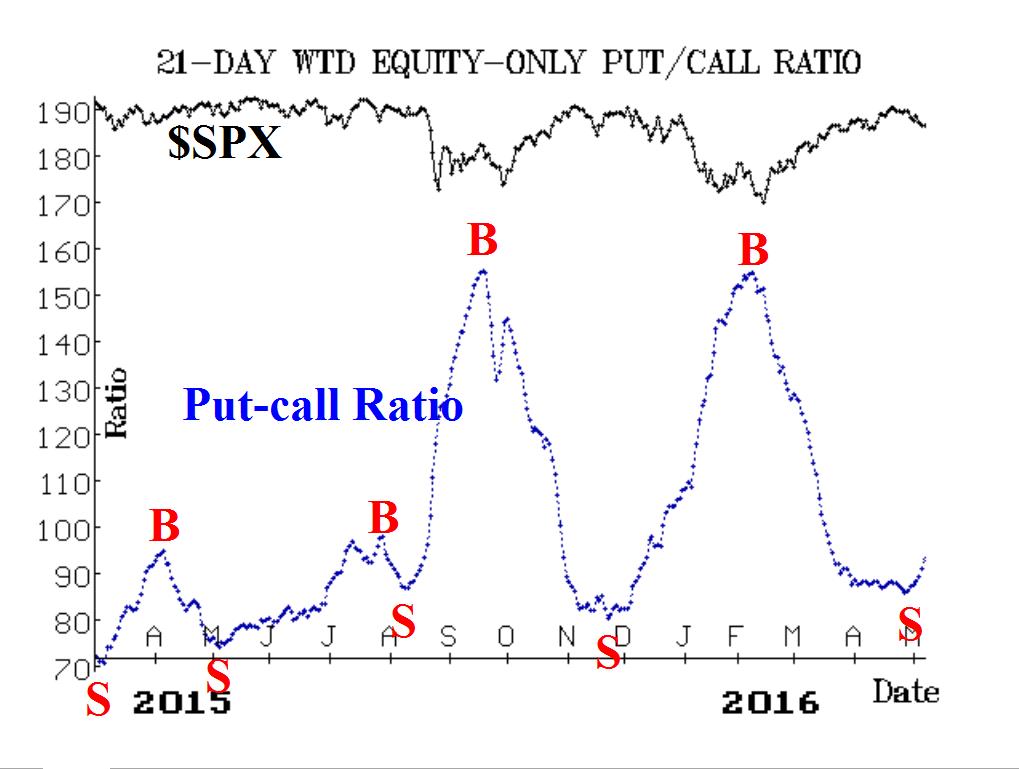

- “In summary, $SPX broke down through one support level, and a correction is clearly underway. Somewhat grudgingly, the put-call ratios and the breadth oscillators have rolled over to sell signals in support of that breakdown. Volatility has remained bullish for stocks, though. The next support level at 2040 thus looms large. If it is taken out, a larger correction will unfold“

What about Monday?

- David Larew

@ThinkTankCharts – In a downtrend you short at the trend line – Tight BB on the 60 min chart – strong move Monday?

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter