Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.”market somewhat unstoppable right now“

said CNBC’s Bob Pisani at the close on Friday. He was not far off the mark. Doesn’t that mean buyers are overwhelming sellers?

- J.C. Parets@allstarcharts – back to back really long tails in the candlesticks for S&P Futures, among other sectors, stocks and indexes. To me that is evidence that sellers tried to take control, only to then be overwhelmed by demand from buyers. Twice. Is that bearish behavior or bullish?

What might have given buyers the confidence to roll over sellers?

- Peter BrandtVerified account@PeterLBrandt – U.S. stock market breadth is extremely healthy. Market tops occur when strength is highly selective, not when NYSE Cume A/D keeps marching into new highs

$NQ_F$ES_F$SPY$QQQ

Any prior instances with a similar condition?

- Ryan Detrick, CMT@RyanDetrick- S&P 500 weekly MACD histogram above 0 currently. March ’16, December ’16, and ‘Oct ’17 are the other recent times this happened. Not the worst times for a continuation of the bull market.

First the Russell 2000 led the broad indices; then Nasdaq 100 took over the lead while the S&P kept behind. Can a rally be justified when the big champ falters behind?

- Peter BrandtVerified account @PeterLBrandt S&Ps

$SPX$ES_F$SPY latest index to join the bull party. Breakout of coil establishes possible target of 3018

What about fundamentals? They suggest S&P target of 3,200 to Tony Dwyer of Cannacord Genuity who front ran our question back on Monday, June 4 on CNBC FM. He said the market has got its mojo back; sentiment among newsletters is only 50% and confidence in economy of of consumers & CEOs is high. He raised his S&P earnings number to $160 and proclaimed that earnings were blowing away expectations.

What about fundamentals? They suggest S&P target of 3,200 to Tony Dwyer of Cannacord Genuity who front ran our question back on Monday, June 4 on CNBC FM. He said the market has got its mojo back; sentiment among newsletters is only 50% and confidence in economy of of consumers & CEOs is high. He raised his S&P earnings number to $160 and proclaimed that earnings were blowing away expectations.

Marko Kolanovic of JP Morgan went a step further and used the MU word. Not Micron but Melt Up. His caveat was that the S&P is up 5-6% in the last month and that pace cannot be maintained. But quiet weeks ahead will actually create a melt up in stocks as volatility will be contained & dealer positions remain suppressed. Unlike Dwyer, Kolanovic didn’t raise targets but simply said the S&P will go to new highs this year.

His most interesting call was to begin legging into Emerging Markets. Part of his reason was the wide performance gap between US stocks & EM stocks over the past 10 years. How wide is that gap? Since a picture is worth much more,

- Charlie BilelloVerified account @charliebilello – Total Returns, last 10 years… US: +150% MSCI World ex-US: +18% MSCI Emerging Markets: +17%

$SPY$ACWX$EEM

On second thoughts, it may be better to hear from Kolanovic directly:

On second thoughts, it may be better to hear from Kolanovic directly:

Does the data match this optimism?

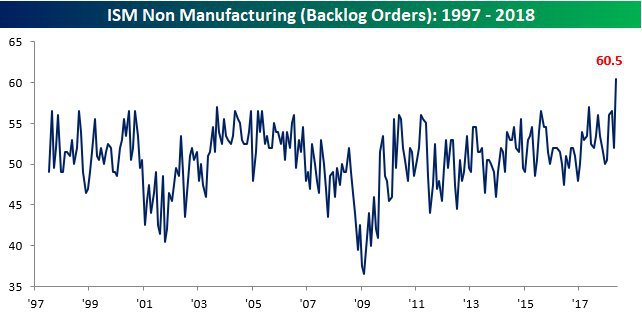

- Bespoke @bespokeinvest – Backlog Orders index in ISM Services report rose to a record high with its third largest m/m increase. https://www.bespokepremium.com

/think-big-blog/ism-services-r eport-tops-expectations/ …

Wait a minute. Such strength in economic data usually results in Treasury rates rising across the curve and prompts the Fed to raise rates with greater urgency. But look what happened on Tuesday, June 5, the day the above data was released?

The 10-year yield fell by 2.2 bps & the 5-year yield fell by 2.6 bps. Warum, as Field Marshal Rommel asked General Jodl during the early stages of the D-day at Normandy. We used the German quote because we don’t know any Italian parallel.

2. Italy-Germany-EM & Wednesday-Thursday-Friday

Let us take it from top down:

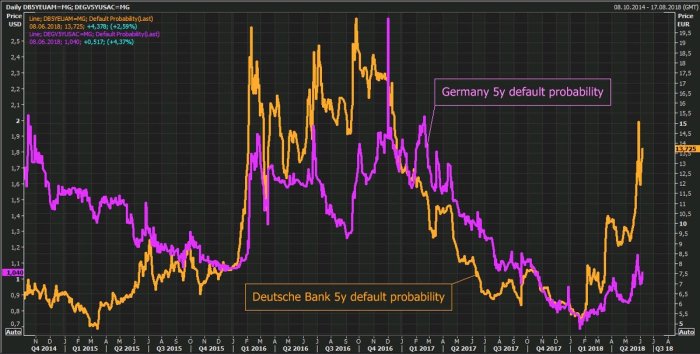

- Raoul PalVerified account @RaoulGMI Weird things happening in EU Investment grade CDS… something is really not right, whether it’s

$DB or a larger risk re-pricing. Equities in Europe are also not trading well in my opinion. Something to keep an eye on. EM CDS are also not looking good.

But isn’t Deutsche Bank much smaller now relative to Germany than it was 10 years ago?

- Holger Zschaepitz @Schuldensuehner Doom loop alive and kicking even in solid good old

#Germany. Germany’s 5y default probability has traded in lockstep w/ Deutsche Bank’s 5y default risk this week despite Deutsche’s balance sheet has shrank to 44.3% of German GDP from >90% in 2007.

That brings up the really big trade war that is bubbling underneath – a war that might persuade Italy to introduce a different currency for use within Italy while staying in the European Monetary Union & keeping the Euro as external currency. Such a new & most certainly much weaker intra-Italy currency would cause a big contraction in Germany’s exports to Italy.

That in turn has prompted the Bank of Italy to warn the Italian Government against such adventurism:

- Holger Schuldensuehner @Schuldensuehner –

#Italy 2y risk spread jumps as Bank of Italy warns Rome against measures that risk pushing the country off a cliff. A possible standoff w/EU adds to the gloomy mood. Just before the G7 summit, Conte said Russia should be invited to rejoin the group. https://dailym.ai/2HwZaEH

With Conte deliberately poking Merkel in the face by agreeing with President Trump about inviting Russia back into G-7, is there any doubt left about the tussle between Italy & Merkel-obedient EU?

With Conte deliberately poking Merkel in the face by agreeing with President Trump about inviting Russia back into G-7, is there any doubt left about the tussle between Italy & Merkel-obedient EU?

That brings up the possibility of Draghi being more hawkish next Thursday in a cut off his nose to spite Italy action. Since major central banks do consult with each other, one assumes Fed Chairman Powell would know by Wednesday what Draghi plans to do on Thursday morning. So would Chairman Powell get more hawkish ahead of Draghi or play dovish to let Draghi have his day?

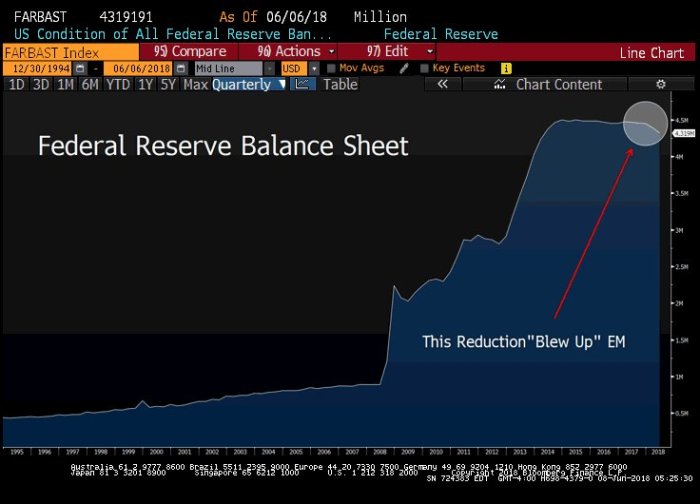

That is not the only reason for Chairman Powell to talk dovishly on Wednesday. EM central banks, including that of healthy growing India, are warning the Fed that the double whammy of Fed contracting its balance sheet & the Treasury increasing its debt issuance is creating a dollar liquidity crisis. Look how an eloquent man expressed the same appeal & added a chart:

- Lawrence McDonald @Convertbond – Dear US Federal Reserve, Removed just a paltry $19B off your $4.49T balance sheet and at the same time blew up the global emerging markets, NOT a good trade. End your experiment now. Signed India, Turkey, Brazil, Argentina, S Africa, Mr. who’s next?

But isn’t reducing the size of the Fed’s balance sheet now a sacred obligation for Chairman Powell and the FOMC? How will they prepare for rebuilding it to protect against a US downturn without contracting it now? So what measures can Chairman Powell use to reduce the panic in EM (assuming he cares)? Talk dovishly & not explicitly reaffirm 3 more rate hikes this year?

And why should he do that? Because otherwise he will see the US yield curve flatten to an extent he has sworn to not tolerate. And perhaps because, a hawkish Fed & a hawkish Draghi would put enormous pressure on a major central bank that just saw its country’s GDP go negative. Rick Santelli explains it much better than we could:

The most important insight about Germany came from Jim Cramer this week. He told his co-anchor David Faber that a source in Washington had told him that President Trump really wants to shut down the import of German luxury cars into America. We believe Cramer’s source.

This is tantamount to waging war on Germany which is the world’s number 1 mercantile economy. Without ending that mercantilism or at least severely curtailing it, Europe will not regain its health & US will not cut its trade deficit with Germany. We would not be surprised to hear that the populist Italian Government has been given at least verbal support by President Trump in its fight against Germany-EU (see last week’s Bannon-Zakaria interview). Read President Trump’s statement about including Russia in a G8 and its swift endorsement by Italy in the above Trump-Germany conflict. Do you really think the two had nothing to do with each other? And Germany has a weak hand right now:

- jeroen bloklandVerified account @jsblokland – Eurozone macro surprises. Lower for longer!

The more scary thought is the Hedgeye statement that

The more scary thought is the Hedgeye statement that #EuropeSlowing is “just getting started“. Now you get why we call Draghi’s hawkish step a cut off Germany’s nose to spite Italy’s face?

But you know who is the stupidest leader in the G7? If you were Theresa May of UK, wouldn’t you use this Italy mess to work with President Trump to challenge Germany & get a better deal for Brexit? Instead, what has she done?

- MacroQuant @MacroQuantCTA Donald Trump ‘tired of Theresa May’s school mistress tone’ and will not hold talks with her at G7’ | via

@telegraph

Contrast that with what Boris Johnson, May’s Foreign Secretary, said to members of Conservative Way Forward – a Thatcherite campaign group:

- “I am increasingly admiring of Donald Trump, … I have become more and more convinced that there is method in his madness. … Imagine Trump doing Brexit, He’d go in bloody hard… There’d be all sorts of breakdowns, all sorts of chaos. Everyone would think he’d gone mad. But actually you might get somewhere. It’s a very, very good thought.”

The Buzzfeed article added:

- “Johnson revealed to the activists that he, too, is gravely worried about the direction of the talks. Johnson insisted he won’t compromise on the final terms of Britain’s future economic relationship, but said the Brexiteers were at risk of getting a deal far worse than they’d hoped for. The government is so terrified of short-term economic disruption that it’s at risk of throwing away the opportunities presented by Brexit, he said. He ridiculed the concerns about disruption at the borders as “pure millennium bug stuff” and said it’s “beyond belief” that the Northern Ireland border has become an obstacle in the negotiations”.

This is the sort of stuff politicians say before they put a dagger in their PM’s back. Imagine Boris Johnson as PM of UK handling Brexit as an ally of President Trump and Italy’s Matteo Salvini demanding & implementing populist measures in opposition to EU-Merkel – all they might need is a mistake by Draghi that blows up European Bonds & crushes Deutsche Bank.

We, of course, don’t know much but we do feel there is lot more going on underneath. Man, we can’t wait for next week.

3. Treasury Rates

Fed Chairman Powell may need to cool down his hawkishness for purely local US concerns as well.

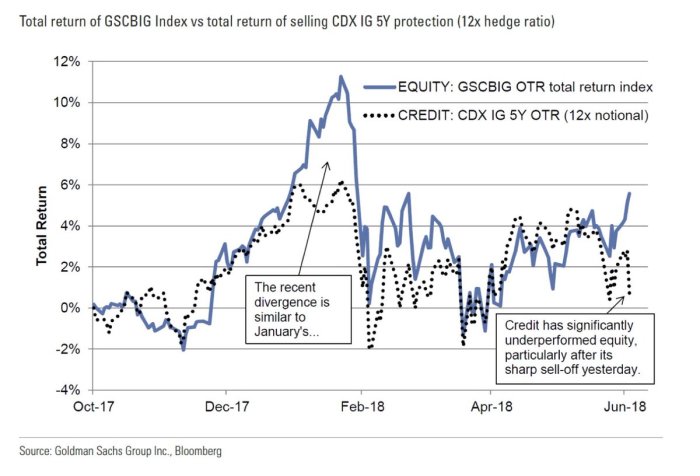

- Jesse Felder @jessefelder Goldman Says the Credit Markets Have Been Ringing the Alarm Bell on Stocks https://www.bloomberg.com/news/articles/2018-06-08/goldman-says-credit-rang-warning-bell-that-stocks-may-be-hearing …

And,

And,

- Lawrence McDonald @Convertbond Credit vs. Equities This week, seeing substantial credit underperformance, Investment Grade US corporate bonds nearly +70bps relative to a tame US equity market, one of these two parties is out to lunch (wrong) (CDX IG 5 year, Bloomberg data) via

@BearTrapsReport

With all this going on, the Treasury yield curve rose 2-4 bps this week. It will be interesting to see how Treasury yields behave next week on Powell-Draghi-Kuroda. But some are placing serious bets already:

- Thomas Thornton @TommyThornton Buying a 5% sized position in

$TLT 5% stop. Not all is lining up but a few indicators are giving me enough to give it a go

That brings up back to :

4. EM Equities

Given all we discussed above, why would any one even venture to get into EM equities?

- Lisa AbramowiczVerified account @lisaabramowicz1 So far, the selloff in emerging-markets assets has been relatively isolated to specific economies with unique difficulties. There hasn’t been an exodus of cash from the biggest EM debt ETFs, with

$IEML, for example, actually seeing some inflows. This doesn’t feel like panic.

Then you have the capitulation-expert getting sarcastic & mega bold:

- Lawrence McDonald @Convertbond – Wall St. Consensus 2018 June: “emerging markets are un-investable” January: “Global Synchonized Growth positions emerging markets in the Sweet Spot”

$EWZ$TUR$ARGT$EEM Via@BearTrapsReport

Meaning things look so bad that they actually may be good to buy. That is also what Marko Kolanovic said in his clip above – that there are both +ve & -ve risks but the payoff from +ve risk may be bigger. Note that the 2-year yields in Turkey & Brazil rose by over 100 bps this week.

Look what Kenneth Rogoff of Harvard wrote in Project Syndicate:

- “The good news is that a full-blown global debt crisis is still relatively unlikely to erupt. … Although it is true that several emerging-market firms have piled up worrisome quantities of dollar-denominated external debt, many foreign central banks are brimming with dollar assets, especially in Asia.”

- “The most important reason for optimism, notwithstanding all the surrounding political noise, is that global long-term real interest rates are still extremely low. Even with all the drama surrounding Fed tightening, 30-year inflation-indexed Treasury bills are paying around 1% – far below long-term real returns, which have averaged closer to 3%. As long as the underlying global interest-rate picture is so benign, it is hard to see the big Kahuna of bond-default waves coming just yet“

Amazon announced this week that they are ready to invest an additional $2 billion in Amazon India, partly in response to Walmart’s acquisition of Flipkart.

Speaking of India, we just have to, despite our grave chagrin, discuss a storm du jour in India, a storm that people are talking about with greater fervor than the monsoon or the Indian 10-year yield breaking above 8%.

Caution – Do Not Read Further if you are sensitive or averse to discussion about certain below the belt behavior.

5. What was so “memorable” about May 28, 2018?

We have been meaning to feature the tweet below since we saw it first on May 9, 2018. But we refrained because May 28, 2018 was also the real Memorial Day. Not only have two weeks elapsed but this topic became a huge point of trolling in India this week.

- Aparna JainVerified account @Aparna – WTF is international masturbation day? Are we all supposed to collectively orgasm tonight at 8pm like Earth Day? No I mean really?

We don’t know Ms. Aparna Jain. We saw this tweet because it was retweeted by another Indian “journalist”. According to Wikipedia, this annual national event, now international event, was first launched in 1995 to protest the firing of Surgeon General Joycelyn Elders by President Bill Clinton.

This topic became the subject of intense discussion because of one scene in a new film “Veere di Wedding”, a scene in which the husband of one of the main female characters “walks in on his wife masturbating with a vibrator“, as the South China Morning Post described it. Viewers of Two & Half Men would take any such scene in stride but Indian audiences reacted with intense trolling, both against & for Swara Bhaskar (phonetically Swaraa Bhaaskar), the female actor.

The heat against Ms. Bhaskar got so intense that, in typical Indian fashion, her mother had to publicly intervene. Her mother, Ira Bhaskar, holds a Ph.D from Tisch School of Arts in New York and now teaches Cinema Studies at New Delhi’s Jawaharlal Nehru University.

The controversy has done wonders for the film at the Box Office, with it running in the top 10 in Britain, Australia and New Zealand, according to South China Morning Post.It remains to be seen whether this film & the controversy does anything to revive the moribund career of Ms. Bhaskar.

The reality is that Indian society is in the midst of a huge sexual revolution in which, thanks to the morning-after contraceptive pill & higher disposable incomes, women are able to engage in as much sex as they want. In contrast, the traditional section of society, both men & women, are reacting in horror. They know that sex has always been a big factor in Indian society. They merely mind it being discussed publicly.

Also they are concerned about peer pressure exerted on young girls and the lack of adequate protection. Exhortations to young women by other women like “chad ja” or “climb on him” are now commonplace in Bollywood films. No wonder abortions among 13-15 year old girls rose 67% year/year in 2017.

Bollywood now routinely shows women executives acting as honey traps against business competition. Witness the song Tu Isak Mera (“you are my love“) from Hate Story 3 after the number 2 executive from one company joins a competitor & meets their CEO. The song is about her day dream and does not represent actual action. This is one videoclip we would prefer to not include here even though YouTube has not classified it as restricted for mature audiences.

Thanks perhaps to her role in Hate Story 3, Daisy Shah is now featured in next week’s big budget film Race 3. We expect Race 3 to be bold but perhaps lacking in semi-virginal innocence of Katrina Kaif in the song from first Race film that said “Zara Zara ( a little bit) Touch me, touch me, touch me; Zara Zara Kiss me, kiss me, kiss me”. Katrina plays a secretary who is trying to woo her boss, a young owner who owns race horses and race cars.

[embedyt] http://www.youtube.com/watch?v=jB_yxQN_qEI[/embedyt]

The Government, run mainly by old men, has reacted by enforcing draconian anti-men laws because, in their view, Indian women are the most virtuous in the world and would never engage in such acts unless somehow tricked by men. Ergo the Gender Apartheid against men in India.

Thank God we live in America. That lets us watch the intensity of this debate in India without being involved. And we can occasionally watch simple family shows like Two & Half Men reruns.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter