Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.”These people are just people“

Thus Sprach Cramer on Friday morning. Frankly, we don’t know what Zarathrusta said & so we can’t say whether it was right or wrong. But we can say the above comment of Jim Cramer was succinctly true & very important. There is so much institutional respect for the Fed that we all often give far more credit to their ability to see what mortals like us don’t. So it was important to say that people like Clarida, Vice Chair of the Fed, are just people with the same ability to be wrong & to stubbornly justify their error.

But the stubborn comments of Vice Chair Clarida didn’t matter much on Friday. Because he, despite his almost arrogant posture, seemed to signal what Robert Kaplan, President of Dallas Fed, had said two weeks ago on Friday, October 26:

- ” … I am very sensitive to not being rigid or pre-determined about the pace at which we get there (to neutral rate) and the reason is again, I expect GDP growth in 2018 to be strong but I expect it to to moderate in 19 & 20 as this fiscal stimulus starts to wane …. getting the balance right for me is going to require an open mind & to not be pre-determined or prejudge … “

This was Kaplan walking back Powell’s rash & loose-lipped comments on October 3. But it didn’t move the Treasury market. Then this past week, President Kaplan hosted a public event with Fed Chair Powell in Dallas & smoothly enabled Powell to gently take the sting out of his October 3 comment. Powell acknowledged that the global economy was slowing and almost said that they would be data dependent & not establish arbitrary targets for the eventual neutral rate.

Vice Chair Clarida was not as smooth or confidently gentle as either Chair Powell or President Kaplan. But the Treasury market saw through his bravado and yields fell hard on Friday. What has been the net result of Powell & Clarida comments? A big decline in the belly of the curve, the portion most impacted by reduced expectations of future Fed tightenings:

- 2-year yield down 12 bps on the week, 3-yr yield down 14 bps, 5-year yield down 15 bps, 7-year yield down 14 bps, 10-year yield down 11 bps & the 30-year yield only down 6 bps.

This even impressed David Rosenberg who, a week ago, said all Fed systems were a go to 3% or higher neutral rate.

- David Rosenberg@EconguyRosie – The yield on the 10-year T-note just sliced below the 50-day m.a. like a hot knife through butter. The 200-day trendline at 2.95% beckons.

That 2.95% is another 12 bps below Friday’s close. And Rosenberg also labelled the economy as “cooling” and added – “Every single Fed GDP model – New York, Atlanta and St. Louis – is suggesting that real GDP growth is slowing down.”

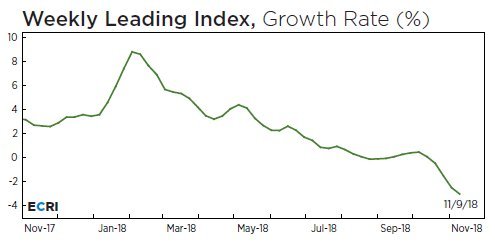

Kudos to ECRI who have been pointing to this slowdown for some time:

- Lakshman AchuthanVerified account@businesscycle – ECRI U.S. Weekly Leading Index growth slips to -3.0%, a 140-week low.

#economyhttps://goo.gl/dLm7HJ

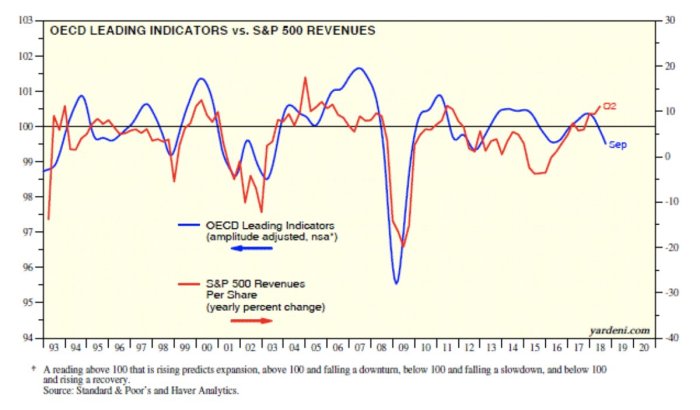

The global picture looks worse, even to a usually bullish Yardeni:

- Jesse Felder@jessefelder – The global economic outlook is deteriorating, as evidenced by the weakening trends in recent months in both the OECD Leading Indicators http://blog.yardeni.com/2018/11/analysts-still-too-high-on-s-500.html…

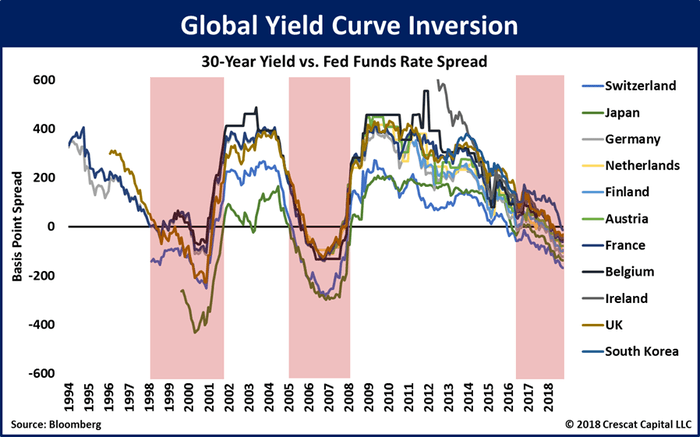

But has the Fed already gone too far in raising rates? About 11 countries would say so. Because 30-year rates in these countries are now LOWER than the Federal Funds rate.

But has the Fed already gone too far in raising rates? About 11 countries would say so. Because 30-year rates in these countries are now LOWER than the Federal Funds rate.

- Otavio (Tavi) Costa@TaviCosta – Flashing signal of recession ahead: Today’s global yield curve inversion looks just as concerning as the ones that preceded the last two market crashes! We now have 11 economies with 30-year yields lower than the fed funds rate. South Korea just joined the pack last month.

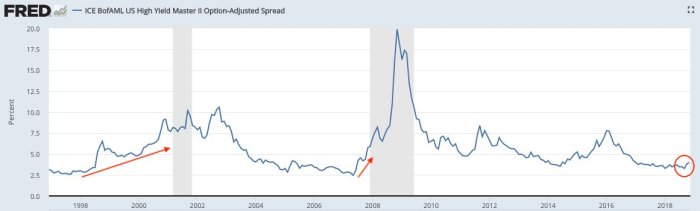

Slowing economic growth is one thing but credit blowing up is an entirely different thing.

2. Credit

Jeffrey Gundlach has been negative on corporate bonds for some time. He got the ball rolling this Tuesday with:

- “A lot of sectors look rich but the one that looks by far the worst – and is the worst – are corporate bonds, … Ultimately, should a recession ever arrive, junk bonds will be particularly dangerous.”

Then we had the specter of GE bonds potentially downgraded to junk status, leading to:

- Lisa AbramowiczVerified account @lisaabramowicz1 – The weakness in credit continues today, with credit-default swap indexes implying the highest relative yields for both investment-grade and high-yield bonds since late 2016.

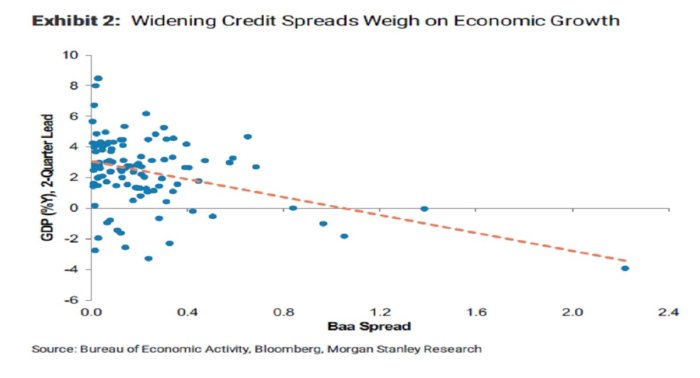

But is there any impact of widening credit spreads on the economy?

- Jesse Felder @jessefelder – A sustained 10 basis-point widening in BBB spreads would spur a 0.3 percentage point reduction in growth while the unemployment rate would rise by 0.15 percentage point, all else being equal. https://www.bloomberg.com/news/articles/2018-11-16/morgan-stanley-warns-bond-boom-and-b-b-bust-would-hit-growth … ht

@lisaabramowicz1

All this sounds so terrible, doesn’t it? So is there another way to look at how much credit spreads have blown out?

All this sounds so terrible, doesn’t it? So is there another way to look at how much credit spreads have blown out?

- Urban Carmel @ukarlewitz – Spreads are really blowing out

But what is the true determinant of this spread widening? And what do we need to weather this storm? Below are answers to these questions from Thomas Tzitzouris of Strategas, a credit manager who won’t buy any high yield bonds today because they are 40 bps too rich:

He said,

- “market is very concerned that the Fed is going too fast or will go too fast; … 50% of investment grade bond debt (about $2.5 trillion) is BBB-rated; every business cycle 10% of its gets downgraded to junk; so if $250 billion, or even $200 billion, gets downgraded to junk … that means high yield spreads have to widen by 100 bps & … investment grade spreads need to be 10 bps higher … those are levels markets can handle assuming Fed doesn’t overtighten … its not the level of interest rates but the pace at which you get there because … bonds & stocks are not priced correctly if you have volatile increase in rates ; we have to stay at goldilocks …

This is why the loose-lipped comment of Chair Powell caused so much havoc in stocks, rates & credit. This is also why the Fed has to be circumspect in raising rates from here without clear improvement in the global economy. Yes, that could prove to be a mistake next year but that mistake can be corrected more easily. As Ray Dalio told CNBC Squawk Box this week, the Fed has already raised rates to a level where we have hurt asset prices and now the risks are symmetric. If you have a downturn in asset prices then the economy can be hurt and the Fed doesn’t have tools that are effective in fixing the downside, especially when asset prices are fully priced.

This is similar to what Stanley Druckenmiller said in his interview with Real Vision – we get deflation when the Fed deflates an asset bubble.

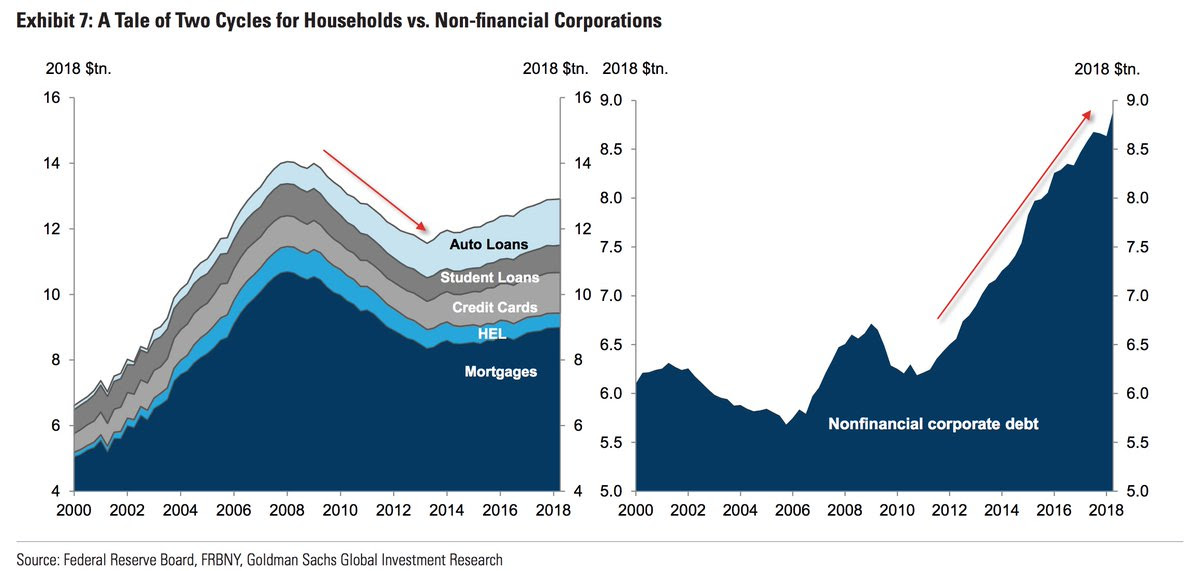

3. Goldilocks vs. Deflation – 1994 vs. 2007

So where is this bubble?

- Holger Zschaepitz @Schuldensuehner – Divergence between household deleveraging & corporate re-leveraging is striking, Goldman says. Owing largely to significant contraction in mortgage loans, level of household debt remains well below 2008 peak in real terms: a sharp contrast to the significant growth in corp debt.

Frankly, lower level of household debt makes this an easier problem to deal with unlike the 2008 kind which created a great recession. While the economy is slowing down, not even Lakshman Achuthan of ECRI expects a recession. Secondly, assuming Mr. Tzitzouris is correct, goldilocks-type interest rates could create a cap on credit problems. After all, a bull steepening fall in Treasury rates could help a lot.

Those who remember October 1994 will agree that we haven’t seen anything yet like the Orange County mess or the Mexican bust. And even those proved manageable after rates began falling in early 1995.

So we are encouraged by what the esteemed Fed leadership said this week. If they keep their balance & look out for contagion coming to US from Europe beset with Italy & Brexit, then a not too hot 2.5% US economic growth can stabilize markets & emotions. And even the Dollar might behave under those circumstances.

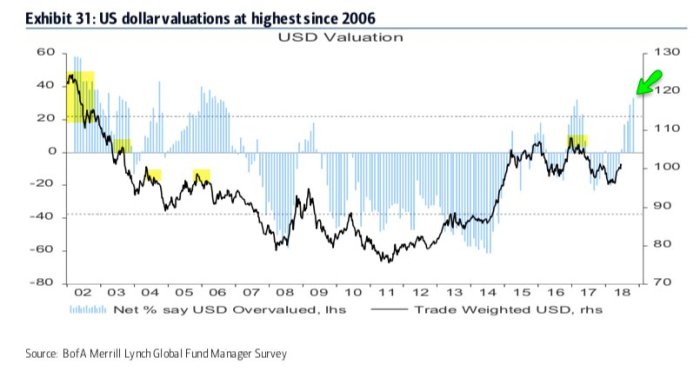

4. Dollar

Comments by Vice Chair Clarida also toppled DXY from its lofty 97-handle. Some might call it a pivot:

- Jeff York, PPT @Pivotal_Pivots –

$UUP the Yearly R1 Pivot Point is strong resistance. YP to Yr1 is a textbbok move@PivotalPivots. Learn pivots here: http://www.pivotalpivots.com/webinar

What is the collective wisdom of Merrill Lynch Fund Managers?

- Urban Carmel @ukarlewitz – Two data points esp. interesting. First, fund managers’ views on the dollar have been highly prescient in the past. They view the

$USD as most overvalued in 12 yrs, a tailwind for US multi-nationals and ex-US equity mkts

Another evidence is the 400 bps outperformance of EEM over SPY this week. China blew away S&P & India, South Korea beat S&P handily as well. Technically, this looks bullish:

Another evidence is the 400 bps outperformance of EEM over SPY this week. China blew away S&P & India, South Korea beat S&P handily as well. Technically, this looks bullish:

- Chris Kimble @KimbleCharting – Emerging/SPY ratio attempting to create back to back to back bullish reversals at 14-year support, while momentum is moving up.

$EEM$SPY

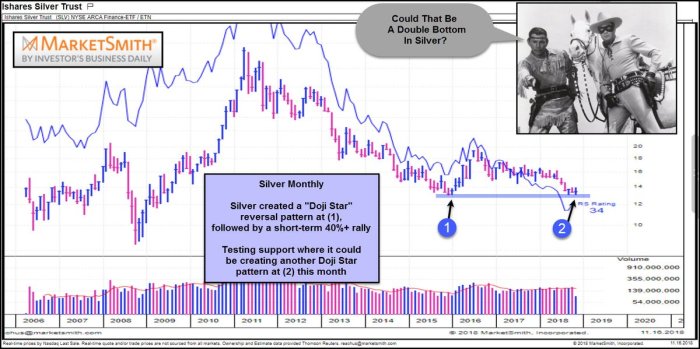

Gold & Silver rallied by 1% & 1.8% resp. this week. Silver looks more technically interesting to Chris Kimble:

- Chris Kimble @KimbleCharting – Silver creating a double bottom & reversal pattern?

$SLV#IBDpartner#IBDinfluencer@MarketSmith https://bit.ly/2K9LthZ$GLD$GDX$EURUSD

5. US Stocks

We begin with Bad & Ugly:

- Lawrence McMillan of Option Strategist – With the gaps having been closed on the $SPX chart, we are now looking at 2820 and 2600 as the significant levels. A break of either one will be important, but it looks like 2600 is going to be tested now that resistance at 2820 has held in such a strong way

And,

- J.C. Parets @allstarcharts there are so many charts that look like this. Are these the types of things we see during environments where we want to be buying stocks?

Now towards the Good.

Now towards the Good.

- SentimenTraderVerified account @sentimentrader The put/call ratio has been above 1.10 on 17 out of the past 30 days, the most since Oct 2015. There have been 27 days with this much of a cluster in history, with a positive return in the S&P 500 two months later after 26 of them.

And,

- SentimenTraderVerified account @sentimentrader – The sentiment of Rydex mutual fund traders has been interesting. Like in April, they seem to be back to believing lower lows are ahead.

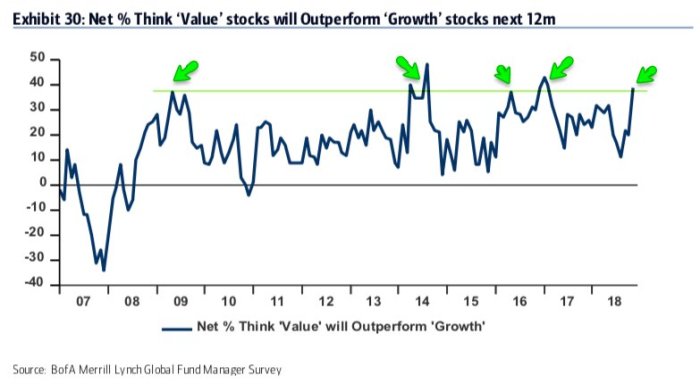

An indicator from Merrill Lynch Fund Manager survey:

An indicator from Merrill Lynch Fund Manager survey:

- Urban Carmel @ukarlewitz Second, they believe ‘value’ will outperform ‘growth’ stocks; similar peaks (in 2009, 2014, 2016 and 2017) marked excellent times to be long equities, especially growth stocks

Finally, an outright call:

Finally, an outright call:

- Cam Hui, CFA @HumbleStudent – Time to position for a year-end rally?

$SPX$SPY#seasonality https://buff.ly/2QHe2Wp

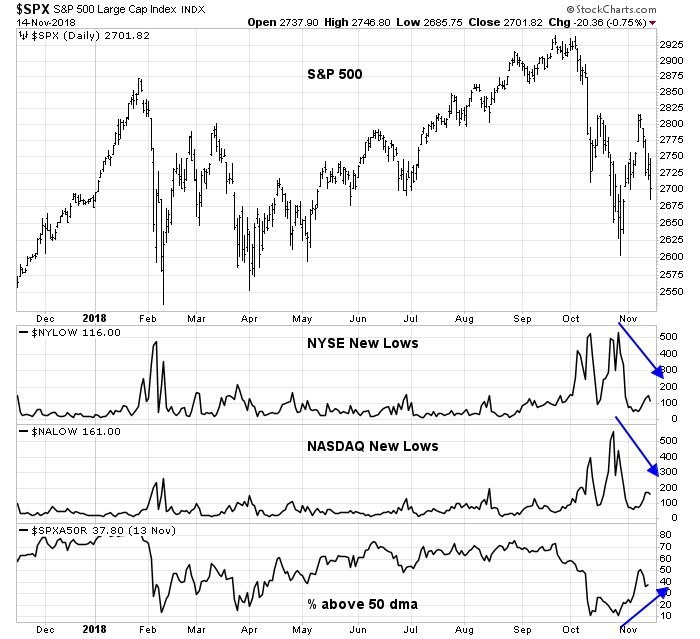

The answer seems yes:

- “Even as stock prices weakened this week, the market appears to be setting up for a year-end rally. The SPX is exhibiting a number of positive divergences. Both the NYSE and NASDAQ new lows are not spiking even as stock prices have fallen. In addition, the percentage of stocks above their 50 day moving averages (dma) are making a series of higher lows, which are all bullish.”

6. A Must Watch

- Real VisionVerified account @realvision In case you missed this on Tuesday, we released the FULL interview with investing LEGEND Stanley F. Druckenmiller and Kiril Sokoloff @WhatILeardedTW for FREE. Don’t miss out watch is now,

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter