Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.He Said & He Said

Sometimes one can raise a question & answer it too. Look at the question raised by the tweet below:

- David Rosenberg @EconguyRosie – Home sales. Capex orders. Philly Fed. Conference Board Leading indicator. Trade numbers out of Korea, Japan and Thailand. I have never seen such incredibly weak data been so readily dismissed by the economics consensus and the financial markets.

Now look at the answer below:

- David Rosenberg @EconguyRosie – Feb 21 – The Fed made it very clear in the minutes that it is focused squarely on the markets. In stark contrast to December, the “we have your back” label was all over yesterday’s document.

How far will the Fed go to guard our back?

- Michael Lebowitz, CFA@michaellebowitz – FED’S CLARIDA SAYS FED WILL CONSIDER NEW TOOLS TO EASE POLICY IF NEEDED : SAYS NEW TOOLS TO BE REVIEWED INCLUDE SOME FED REJECTED BEFORE, LIKE CAPPING TREASURY YIELDS When will the market ask why is the Fed stopping QT, talking about more QE and floating ideas like this????

And yes, as we found out two weeks ago, the Fed has also discussed using negative interest rates. Why? Perhaps, because as Fed Vice Chair Clarida confirmed on Friday, they are now worried about inflation dropping below their lower target.

With such a near-total commitment from the Fed to guard the market’s back, what should smart money be doing?

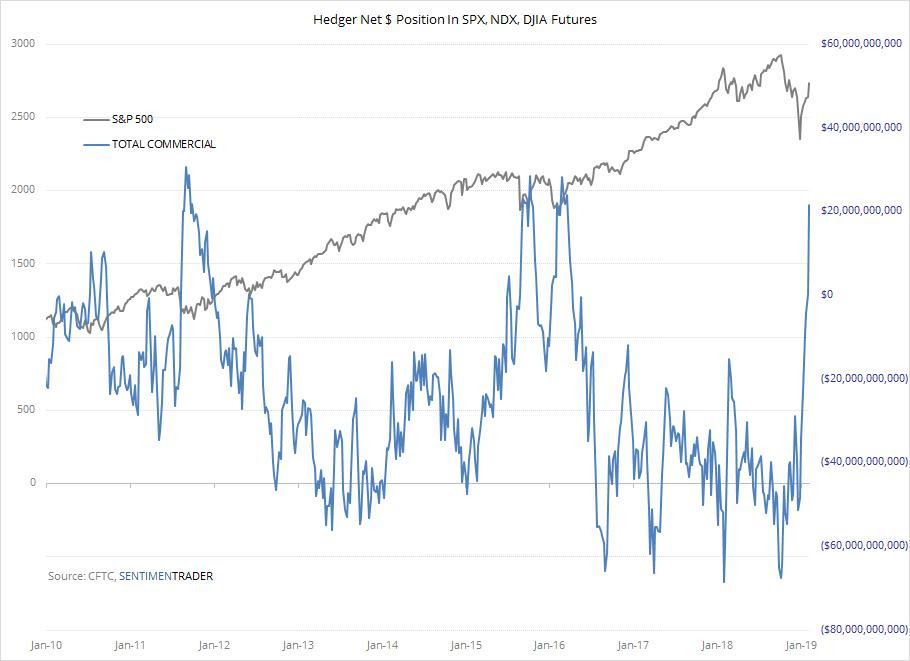

- SentimenTraderVerified account @sentimentrader – The smart money just keeps right on buying. In early February, their net position in index futures was on par with market lows in 2011 and 2015-16. This is extremely unusual, since they usually sell into rising markets.

What is another measure of demand?

- Peter BrandtVerified account @PeterLBrandt – The bullish divergence between S&P breadth and S&P price is stunning. The demand for shares is such that only minor corrections are likely $SPX $ES_F

But is such action finally nearing exhaustion?

- Helene Meisler @hmeisler – ISE Ratio 151% which looks like the highest since it was 201 on 9/20. Wow, folks got bullish today

Some acted on this during the week:

- Douglas KassVerified account @DougKass – in raising my short exposure – but I am no longer waiting. The market has had a fantastic rally from the late December low and I am taking advantage of that setup to expand my short exposure today and all week – regardless of price momentum (which may or may not be faltering now)

The DeMarkians probably concur.

- Mark Newton @MarkNewtonCMT – $CL_F Crude oil pushing up similar to S&P in a stair-stepping pattern & has nearly the IDENTICAL Demark exhaustion count-Note that both WTI and S&P both Bottomed on Christmas Eve, and now heading into first meaningful exhaustoin on strength into next week based on 9-13-9 pattern

Tom McClellan went on CNBC on Friday to warn about a consolidating or somewhat negative action in the stock market during the next two weeks. But he added that he expects this bull market to continue until 2021 & he does not see a big downturn until 2024.

In contrast, Tony Dwyer prefers to look only a year or so out.

- Tony Dwyer @dwyerstrategy – Friday, 92% of SPX stocks traded>50-day ma. Since 1990, median gain 3, 6 &12 months out is 5%, 9% and 16%, respectively. Median drawdown in 1st month after signal was -1%, with the two larger drawdowns of 4% and 7% easily reversed by 3 months.

Next week is the testimony by Chairman Powell to the Congress. Will that add to the “have the market’s back” conviction or will it introduce a doubt or rise in interest rates?

2. Interest Rates

Unlike the stock market, the Treasury market has been consolidating during the past couple of weeks. Will it stay that way or will Chairman Powell introduce some volatility into it?

- Lisa AbramowiczVerified account @lisaabramowicz1 – Implied volatility in Treasury yields has fallen to near an all-time low.

A liquidity-injecting Fed has not usually been good for the long end of the Treasury market. This week, for example, the 30-year yield ROSE by 2 bps while the entire 10-1 year curve fell in yield from down 1 bps in 10-year yield to down 3 bps in the 3-year yield.

What is Gundlach’s trusted Copper/Gold signal saying about interest rates? Below is a DeMarkian’s take:

- Thomas Thornton @TommyThornton Copper vs gold ratio +89bps today. I like short gold, long copper

Is that what many bond market participants are saying?

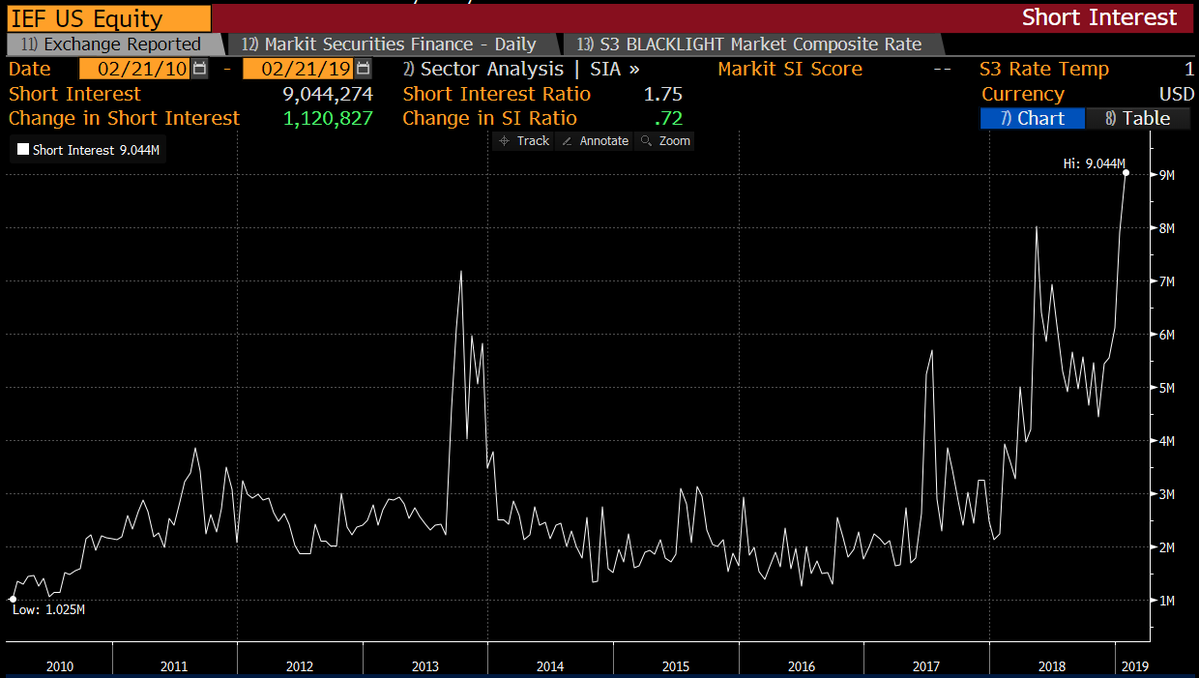

- Lisa AbramowiczVerified account @lisaabramowicz1 – There’s a growing sense that longer-term U.S. rates will rise in the near term. The short interest on BlackRock’s $13 billion 7-10 year U.S. Treasury ETF has surged to a record high. $IEF

This week Pimco came out and warned about credit getting overvalued & suggested moving out of high yield into higher quality credits. Wells Fargo seems to concur:

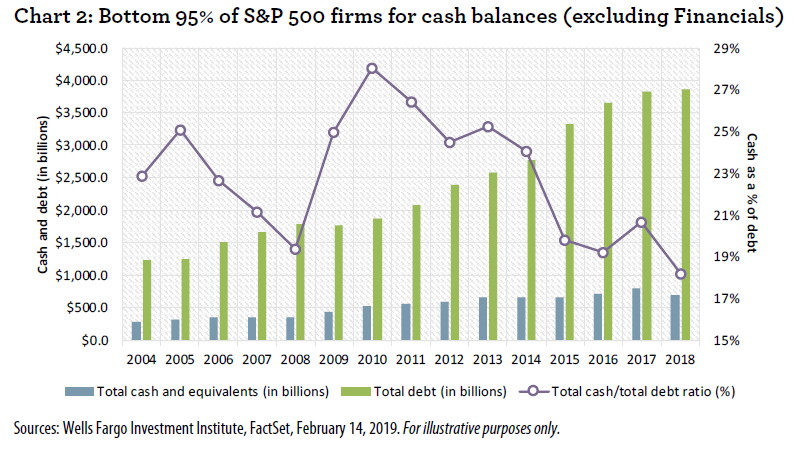

- Lisa AbramowiczVerified account @lisaabramowicz1 – American companies look cash-rich on paper, but average leverage ratios don’t tell the story. 5% of S&P 500 companies hold more than half the overall cash; the other 95% of corporations have cash-to-debt levels that are the lowest in data going back to 2004: Wells Fargo research

If 95% of S&P 500 companies have leverage issues, what about the companies in China?

- Lisa AbramowiczVerified account @lisaabramowicz1 – As more Chinese companies default on their debt, even amid relatively loose lending conditions, concern is rising about the broader economy. Private companies generate 60% of China’s economic growth and 90% of new jobs.

This is from an article in the FT that is fairly alarming:

Will these credit issues of US & Chinese companies be addressed by a trade deal between US & China? Or are these credit issues in China a symptom of the global slowdown that is now being reflected in data?

Will these credit issues of US & Chinese companies be addressed by a trade deal between US & China? Or are these credit issues in China a symptom of the global slowdown that is now being reflected in data?

Who will drive whom? Will weakening credit drive stocks (& treasury rates) down or will rising stocks drive up credit? The Fed clearly understands this & that may explain their intense focus on guarding the stock market’s back.

3. Gold

What was it in the Fed minutes that put down Gold? Look at this week’s chart & notice the peak in GLD just before the release of Fed minutes at 2 pm on Wednesday.

And GDX follows GLD, right?

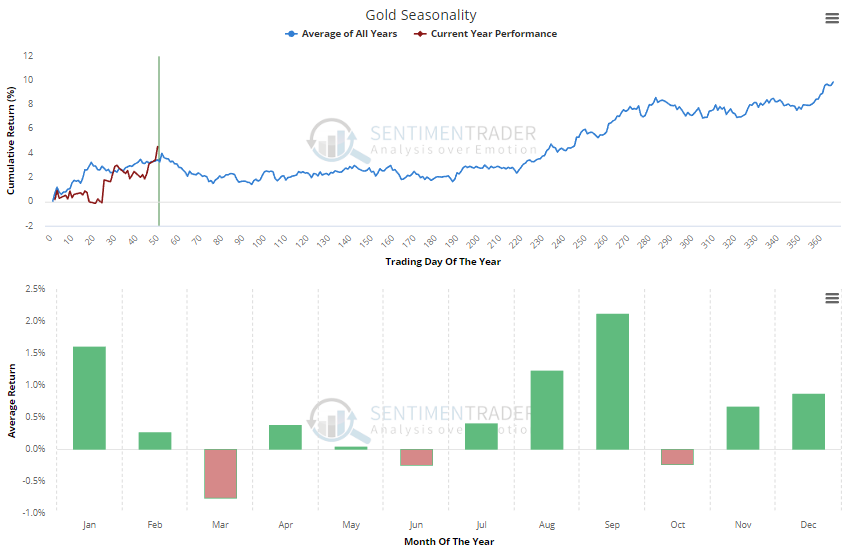

Is this just a quick respite from the rally? Or is this seasonality rearing it’s head?

Is this just a quick respite from the rally? Or is this seasonality rearing it’s head?

- SentimenTraderVerified account @sentimentrader – Feb 20 – Gold has had quite a run. In a typical year (as much as we can rely on “typical”) it peaks right about now.

Now it is Chairman Powell on deck.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter