Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.”think of a nicer set up“?

Paul Hickey of Bespoke said on Tuesday – “last hour strength is ridiculously high“. Isn’t that the hour for institutions to buy? What does that say about positioning? That large players are not invested enough and they are trying to get in almost every day. That may be why Thursday morning’s of 235 points was nearly wiped out by mid-afternoon and why the pre-market decline on Friday was reversed & converted into a up 443 point day with news of a China deal and postponement of tariff escalation slated for March 1.

As the remaining obstacles get removed (shutdown averted) or get diluted (China tariffs)), the US indices vaulted over to have a great week with Dow up 3%, S&P up 2.5% & Russell 2000 up 4.2%.

Of course the indices were propelled up over the obstacles by news & hopes of a large liquidity injection in China (Chinese market up 6% on the week & $ASHR up 5%) and renewed bond buying discussion in the ECB. Also Dr. Brainard of the US Fed openly spoke about curtailing or pausing the Fed’s QT.

Are we back in a period like 2011-2012 when QE got adopted around the world? If so, why would any one worry about earnings estimates getting cut hard or even about a global synchronized slowdown? Especially when positioning is still not what it should be in a rally with such momentum.

This combination of not-so-full positioning and expectations of greater central bank liquidity around the world is overwhelming fears of a global slowdown. It is as if the Tepper Corollary is back – if slowdown is not as bad as feared, if earnings downgrades trough soon, then markets should rally and if slowdown is really bad then we can trust the Central Banks to inject more liquidity that would propel stocks.

Rick Santelli said it succinctly on Friday afternoon:

- “I think the economy is not as solid as it was but it is plenty solid enough given the global liquidity & how much better our economy fares than everyone else’s and while the rest of the world pressures our interest rates down … I think its a perfect goldilocks set up; I would be shocked if we don’t hit all time high in the next month & half or sooner“

In a similar spirit, Jim Cramer summarized the views of Carley Garner, a technical guru at his RealMoney in a detailed clip:

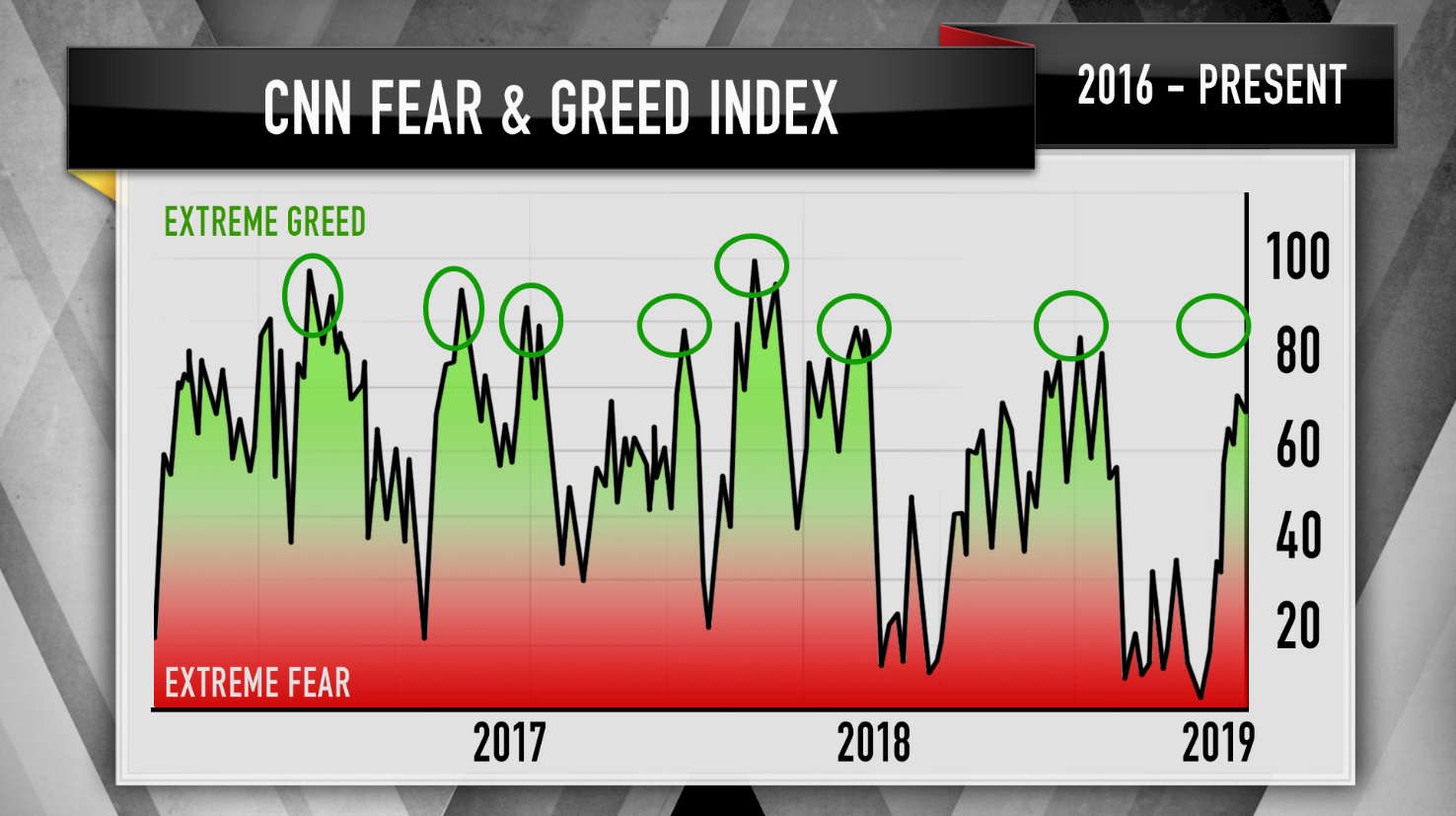

- Right now, the index sits at 67 out of 100, signaling more greed than fear, but still “a far cry from the extreme levels where you need to start worrying,” Cramer explained. When the major averages peaked going into the fourth quarter of 2018, the index hit 90, and according to Garner, “we usually don’t peak until we hit 90 or above,” he said.

Where could the S&P go in the current move?

- “Even if the S&P 500 keeps climbing to, say, … 2,800 — up 2 percent from here — Garner doesn’t anticipate either the RSI or the slow stochastic [to] hit extreme overbought levels,” Cramer said, adding that the technician could even see the S&P climbing to 3,000 if it breaks above the 2,800 level.

- “To Garner, that means going higher is the path of least resistance for the S&P,” the “Mad Money” host said. “Once the S&P climbs to 2,800, or perhaps … to the mid-2,900s, that’s where Garner expects things will turn south and the pendulum will start swinging in the opposite direction.”

Lawrence McMillan of Option Strategist was more subdued & prosaic when he said stay long for now:

- To sum this all up: there is still only the one sell signal (mBB), and it is in some jeopardy of being stopped out. The other indicators (save the chart of $SPX) are on buy signals. Thus it is necessary to retain longs in line with those indicators. What will trigger a reversal to the bearish side? Perhaps the resolution of the China trade deal (“sell on the news?”). In any case, we remain short-term bullish, but are keeping a wary eye out for negative developments. Don’t be caught sleeping.

What could be a reason to not get caught sleeping?

- SentimenTraderVerified account @sentimentrader – In 119 years of history, the Dow Industrials have swung from a 52-week low to an 8-week win streak of > 15%. Those were November 29, 2002. And today.

With $VIX closing below 15 on Friday, one way to protect your portfolio while you sleep would be to buy cheap puts.

2. Rates & Credit

Clearly the Treasury market is not prone to the bullishness evident in the stock market. In a glorious week for the US stock market, the 30-year yield only rose by 2 bps & the 10-year yield by only 3 bps. The 2-5 year curve rose by 5 bps but remained inverted vs. the 1-year yield. Incredibly, the 1-year yield is 2.55%, a full 5 bps higher than the 2.5% 5-year yield. How bullish is this for PE multiples for US stocks?

What should one buy when the Fed gets dovish? Leveraged closed end bond funds is the simple answer. Remember the high yield fund $DPG that Gundlach recommended after the sell off in February 2016? It is up 19.8% in price in the last month & half of 2019 & left $HYG in the dust.

And what about Muni closed end funds? The Pimco NY Muni fund PNF is up 10% in price.

Isn’t life simple when Central Banks ease?

But what if stock indices revisit their lows when the macro picture gets bad, as Doug Ramsay of the Leuthold group said this week? He said the 2-5-10 year Treasuries will trade with a 1-handle in yield. That would be great for Treasuries but, possibly bad for High Yield & not so good for NY Munis (especially after Amazon’s exit).

3. Financials

What did mere talk about renewed bond buying by the ECB do to European banks? $DB rallied 7.5% on the week and all European banks followed. No wonder Citi rallied by 3.7% on the week & $GS by 3.6%.

- Mark Newton @MarkNewtonCMT – #Financials RELATIVE to market have stabilized & now have broken out ABOVE this downtrend, just this week– Last 2 out of 3 days have been convincing in this regard- This group deserves careful scrutiny given its SPX weighting, but looks to be turning higher technically – $XLF

Will the prospect of renewed bond buying by the ECB lead to rally in European stocks? Well, $EWG, the German DAX ETF, rallied by 3% on the week, beating the S&P by 50 bps.

4. Gold & Oil

Oil was this week’s star with a 5.8% rally. Brent was up 6.8% with oil stock ETFS up 6.5% (OIH) and 5% (XLE).

- Greg HarmonVerified account @harmongreg – Dragonfly Capital – Crude Oil asking for a retest http://dragonflycap.com/crude-

oil-asking-for-a-retest/ … $USO $CL_F

- “… over this week it has been rising back to retest the prior resistance area. It is looking for a make up exam on whether it can make a higher high. … The price action suggests a positive response at this point. The RSI is rising off of the mid line with the MACD about to cross up and positive. The Bollinger Bands® are squeezed in which is often a precursor to a big move. Perhaps resolution one way or the other is coming very soon. Look for a move over 56 to confirm a successful move to the upside with more to follow.”

What about Gold?

- Peter BrandtVerified account @PeterLBrandt – Highest daily close in 10 months as #GOLD bull market continues to unfold. Next major challenge $GC_F $GLD is neckline of multi-year inverted H&S pattern — if penetrated target becomes 1844

5. Did Walmart Buy Flipkart on the Cheap?

Walmart reports earnings on Tuesday morning. Will Walmart talk, as Amazon did, about its investment of $16 billion to buy 77% of Flipkart, the online retailer in India. By now, investors are bracing for negative comments by Walmart about their problems with India’s new e-commerce law & the upcoming brutal fight with Reliance.

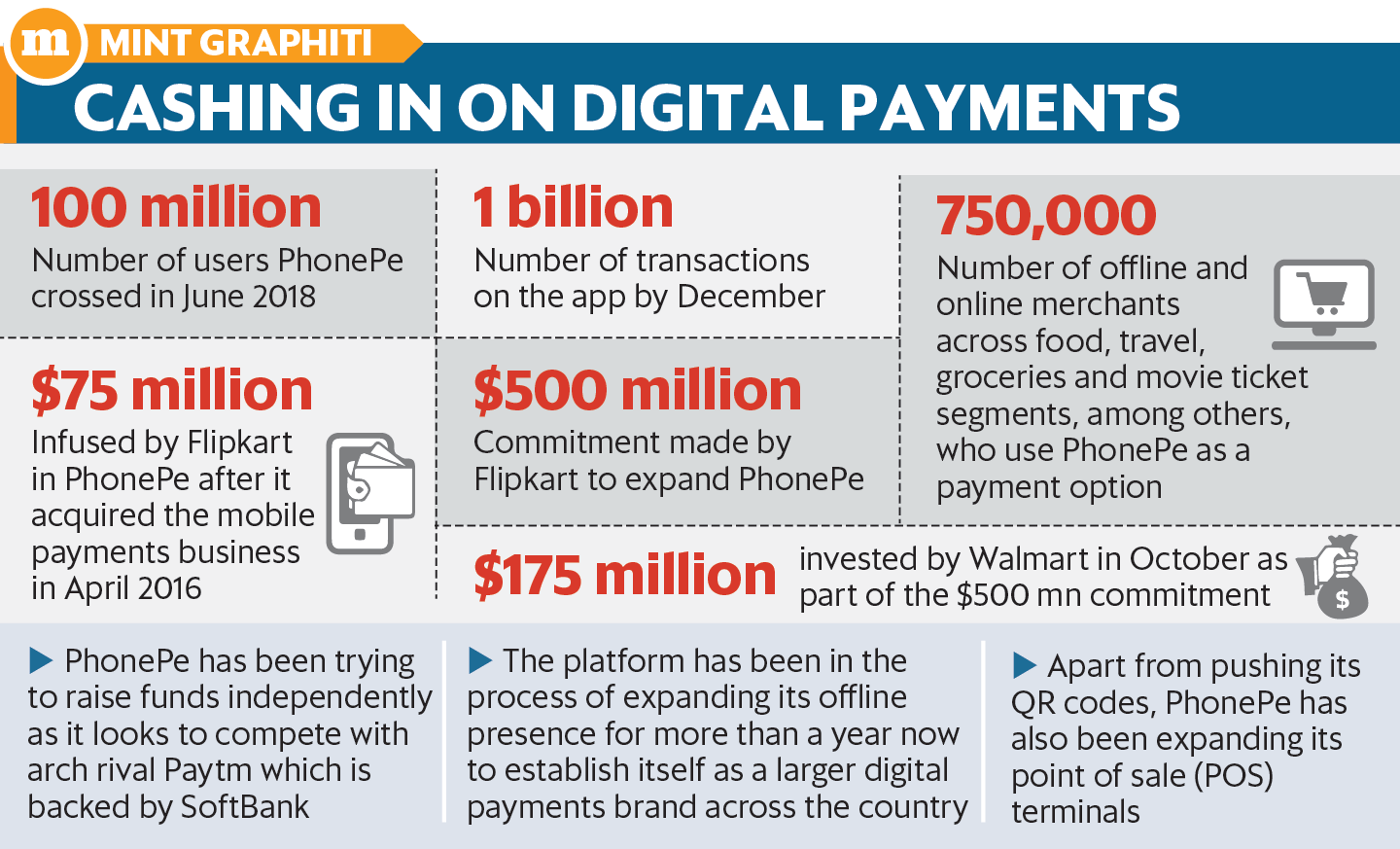

We actually wonder whether Walmart might share good news with investors. Most are unaware of PhonePe, Flipkart’s digital payments arm. When Walmart bought its stake in Flipkart for $16 billion last year, PhonePe was valued at $1.5 billion.

Guess what PhonePe is valued at now, a mere 1-year later. The answer is $10 billion. This massive $8.5 billion increase in value has made Walmart’s acquisition of 77% of Flipkart a value buy, right? According to Indian media, major firms like KKR, General Atlantic are interested in investing in PhonePe.

Walmart is thinking of spinning off PhonePe while retaining a majority interest. Spinning off PhonePe at a $10 billion valuation should be positive for Walmart stock, right? Look at the growth of PhonePe:

But PhonePe is NOT the leader in digital payments in India. That honor goes to Paytm which was valued at $16 billion when Berkshire Hathway invested $300 million in Paytm. Who is another major investor in Paytm? Alibaba.

And yes, Google Pay is another competitor in the Indian digital payments scene. Where does that leave Amazon, India? Restricted to the intensely price-competitive retail sales field?

Frankly, these valuations don’t make sense to us, especially given the cut-throat price competition in India. But such valuations are the price of entry into India & its organic growth over the next 2-3 decades.

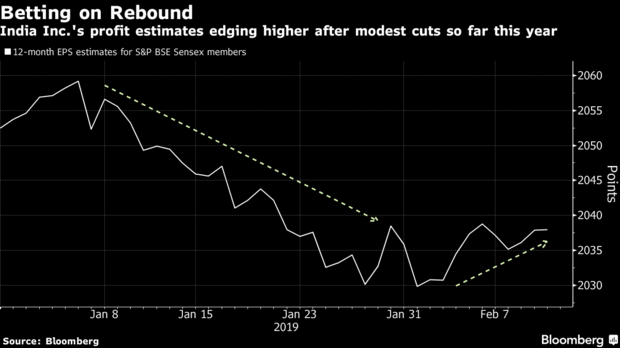

6. Indian market in 2019

The above three-month parity looks very different when you focus only on 2019:

The Indian stock market has been a terrible performer in 2019. But there are indications of a turn in profits, currency & lower rates because of lower inflation.

The Indian stock market has been a terrible performer in 2019. But there are indications of a turn in profits, currency & lower rates because of lower inflation.

That looks promising but the biggest obstacle for Indian stocks is the May 2019 general election. If Prime Minister Modi does not get a majority, then he may not be able to form a coalition government. That will be awful & could lead to carnage in both stocks & currency. That chaos may not last for more than a year or two and Modi could return after the chaos runs its course. This specific scenario is the prediction of a major astrologer.

So depending on your thinking, you may choose to rely on earnings expectations, strategist recommendations or relative value analysis to decide on the scale of your investments in India. Or you could consult an astrologer you trust. If India is still the same & if astrologers are as good as they used to be in our childhood, then chances are the astrologer might prove more accurate.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter