Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.”Circle the Wagons & Protect the Leadership“

What a perfect description from Rick Santelli for the ridiculous round table of Volcker/Greenspan/Bernanke/Yellen hosted by Fareed Zakaria on Thursday! Zakaria is superb as a mouthpiece for the establishment and he served his purpose by giving lay up questions to the esteemed Fed chairs. He achieved his purpose of mocking Donald Trump with the first question to Chair Yellen which she promptly hit out of the park.

What Zakaria didn’t understand and couldn’t possibly understand, Larry McDonald & David Rosenberg understood so well:

- David Rosenberg in his Friday email – I continue to hold the view that what Janet Yellen had to say at her speech last week titled The Outlook, Uncertainty, and Monetary Policy was seminal in nature

- Larry McDonald on CNBC Trading Nation on Thursday – the biggest news really that a lot of clients are being focused on is on the 29th Yellen speech she moved the accepted level of inflation that the Fed is willing to accept ; also in the minutes there is hints to that it is really a game changer; yesterday clients were talking about a very large Euro dollar trade, that is an interest rate trade bet – a bet that we will have two rate cuts by 2017; so we are seeing money pile in on these bets, rate cuts – two of them by 2017 – that puts us in negative rate territory – they have gone from 1-2% chance of rate cuts in 2017 to 10-15% chance of rate cuts

- David Rosenberg on BTV on Thursday – I don’t ever remember a central bank chief having the title “uncertainty” of their speech; Janet Yellen had the word uncertainty in the title of her speech; that tells you right there – she spoke repeatedly about the global risks; particularly what is happening in the US domestic economy; we printed 1.4% on Q4 real GDP and latest number on Atlanta GDP tracker for Q1 is 0.4%; so whether you look at global developments or at US domestic economy at stall speed, the case for the FED to do nothing for an extended period of time is actually quite strong right now

2. R-Word?

Just one day after David Rosenberg spoke of 0.4% tracker, the Atlanta Fed lowered the estimate for Q1 real GDP from 0.4% to 0.1%, just above a negative number.

Actually, on a year-on-year basis, retail sales are down 0.1% & the U.S. consumer went AWOL in March, according to Michelle Meyer of BAML:

- Bloomberg

@business – The biggest part of the U.S. economy might be rolling over, Bank of America sayshttp://bloom.bg/1MkblX7

Given all of this, what did NY Fed President Dudley signal in his speech?

- Lawrence McDonald @Convertbond – Yellen’s Inner Circle Dudley moving to shoot the June rate hike between the eyes “growth outlooks to be titled to the downside”

This is why we believe “zero before 50bps”. For those who believe R-word has to be resuscitated before a rate cut,

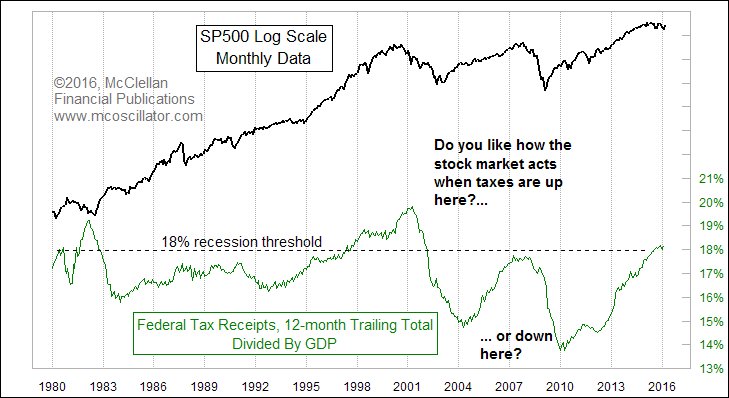

- Tom McClellan @McClellanOsc – Not being discussed by presidential candidates: total federal tax receipts now up to recession-inducing level.

And what do high taxes mean for the Americans?

- Lawrence McDonald @Convertbond – Why USA in 1.8% GDP growth purgatory? 2016 Collectively, Americans will spend more on taxes than food, clothing, housing combined

So why shouldn’t retail sales be down year-over-year?

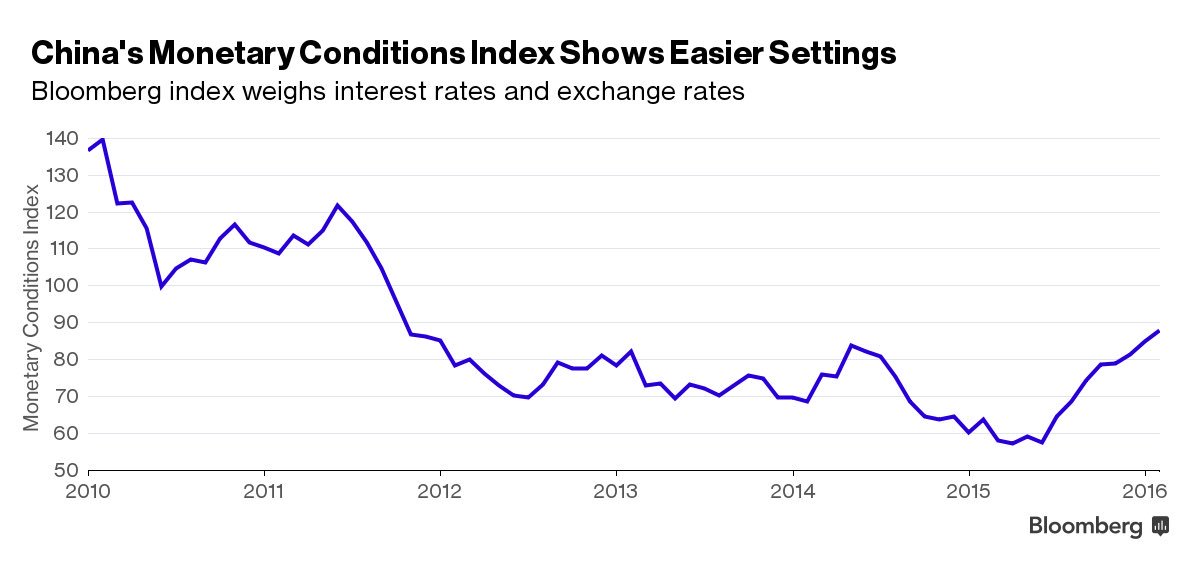

3. Shanghai Accord & BoJ

Three weeks ago, the markets were convinced of a G20 deal to take the pressure off of China via a globally coordinated central bank effort to weaken the Dollar. How well has this effort succeeded, especially where it counts?

- Holger Zschaepitz

@Schuldensuehner –#China‘s monetary easing is starting to hit home: Bubbles building everywhere.http://bloom.bg/1NbW1a1

But the pressure on China to devalue cannot come off without a rise in the Yen. So a major part of the Shanghai G20 deal was Japanese acquiescence of a rise in the Yen vs. the Dollar. How well has that worked out? Measured in FXY, the Yen is up 5.2% against the Dollar since the G20.

- Chess @chessNwine – $FXY Weekly. Japanese Yen ETF on track for largest weekly buy volume since 2013 on the price breakout.

So what does Japan do now? Their experiment in negative rates has backfired. That threat has essentially shut down the longer end of the JGB market according to a Bloomberg article.

So do they go nuclear? And by that mean, force a perpetual maturity. How?

- “The authorities are attempting to push bond yields down below existing nominal GDP, so that the existing debt can be converted or ‘consolidated’ into a perpetual zero coupon bond presumably before any ‘tapering announcement”

We have no clue what that would do to investor appetite for Japanese bonds. Nor do we have a clue about its impact on the Yen.

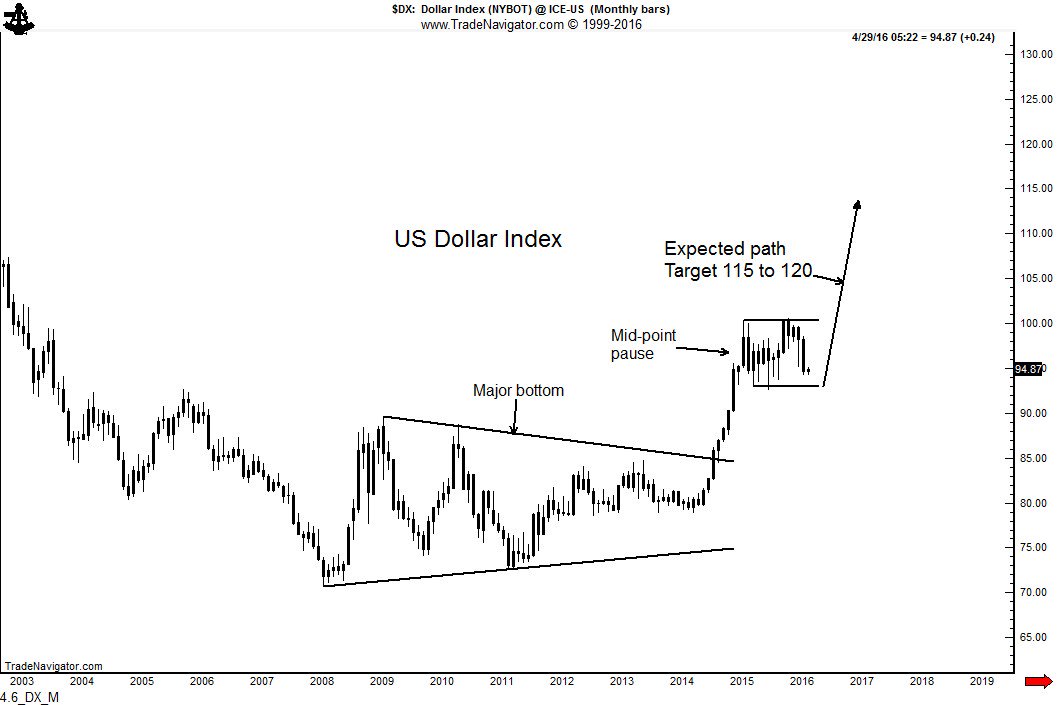

But the markets have done virtually every thing they can to heap scorn on the desires of the central banks. So could the below come true?

- Peter Brandt @PeterLBrandt Apr 6 – For the record, I am major bull on $DX_F USD pausing for run to 115 to 120. Thrust will rip eyeballs out of bears

4. Treasuries

Why shouldn’t Treasuries keep rallying in such a global environment? The 2-year yield fell by 6 bps this week. That is as much as the fall in the 30-year yield. The 5-year yield fell by 8 bps thus bull-steepening the 30-5 year curve again. The 5-year yield is now just above 1.15%, a critical level according to Rick Santelli. Remember the level Jeff Gundlach considered critical for the 5-year just a few weeks ago – 1.80%. Now even the 10-year yield has fallen below that. Actually the 10-year yield closed below 1.7% on Thursday before closing the week at 1.72%.

A sweet spot this year has been closed end fixed income funds. Since these funds go long about 135% by borrowing 35% in the short end, a drop in short rates acts like a driver for their performance.

As David Rosenberg wrote this week:

- “I am convinced that if it were not for the fact that 10-year Japanese Government bond yields

were trading at -9 basis points and German bunds at +0.16% (on the back of rampant central bank intervention), the 10-year Treasury note yield would be closer to 4% right now rather than the 1.8% level we have on our hands today”

But why would that change given:

- Holger Zschaepitz @Schuldensuehner – German stagnation ahead? #Japanification of #Germany continues as 10y bund yields mimicking Japan’s 1990s experience

David Rosenberg may be right. Given what Yellen said in March, the real trigger for a sell off in Treasuries would probably come from a surprising strength in European data.

5. Stocks

Last week we asked “Since both Treasuries & stocks are overbought & overloved, which one sells off first?” Stocks fell by 1% this week and Treasuries rallied 1%. Is that decisive? Not according to Lawrence McMillan of Option Strategist:

- In summary, there has been some weakening in the indicators, but most of the sell signals have been indecisive and quickly canceled out. These are warning signs, but not yet a sell signal

We can look at various factors but the S&P has been governed by technicals all year. So what do we look at?

- David Larew

@ThinkTankCharts – Buying the 52 week highs vs. 52 week lows – generally ignoring tops is not good. 2040 SPX is the line in sand

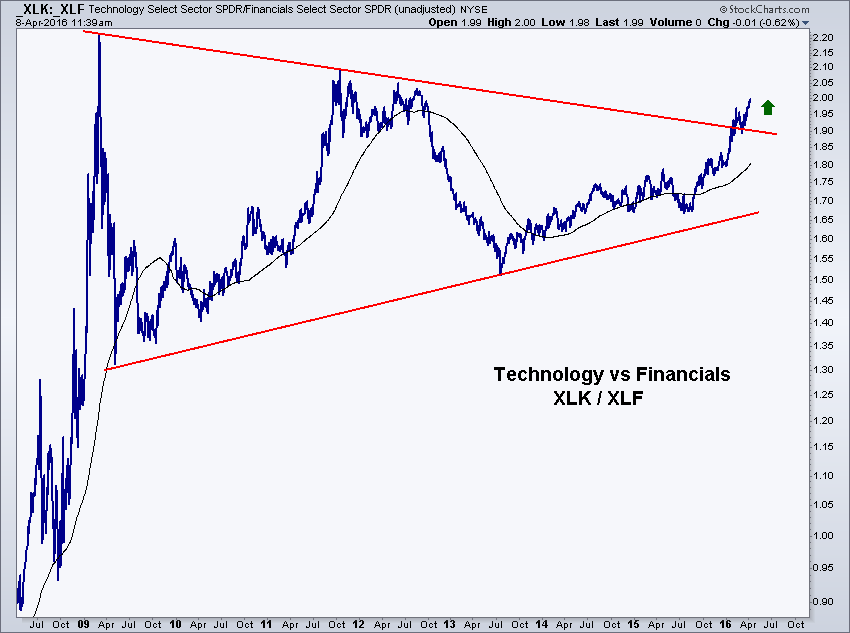

The real sore spot in the S&P is the financial sector, especially the leader Goldman Sachs, Yes, the stock was downgraded this week but the problem has been all year:

- HCPG @HCPG – $GS vs $SPY for this year

US financials are also being buffeted by the horrible action in European & Asian bank stocks. Some like Anastasia Amoroso, global market strategist at JPMorgan funds, think financials have priced in all the bad news. In contrast, J.C.Parets is recommending a pair trade – Long XLK (technology) & Short XLF (financials):

- “This is a chart of the U.S. Technology Sector vs the U.S. Financial Sector $XLK/$XLF. Notice how this monster consolidation goes back to early March 2009. We are currently breaking out above the downtrend from those 2009 highs and I believe heading a lot higher”

We will see how the financials perform after earnings beginning next week.

6. Gold

Last Friday, Carter Worth of CNBC Options Action asked viewers to buy Gold. Good call. This week, Carter said “there is much more to come“. This Thursday, Larry McDonald of ACG Analytics said buy Gold Miners. And GDX,GDXJ rallied by 3% & 4% on Friday. His case was the seminal change in Yellen’s outlook and the global reality:

- Lawrence McDonald @Convertbond – Supported by World of 0% Rates Gold Miners $GDX breakout of key technical trading range Via @BearTrapsReport

The Dollar has not mattered much this year. Perhaps because:

- $hane Obata @sobata416 – Gold has a higher correlation with real rates than it does with the USD:

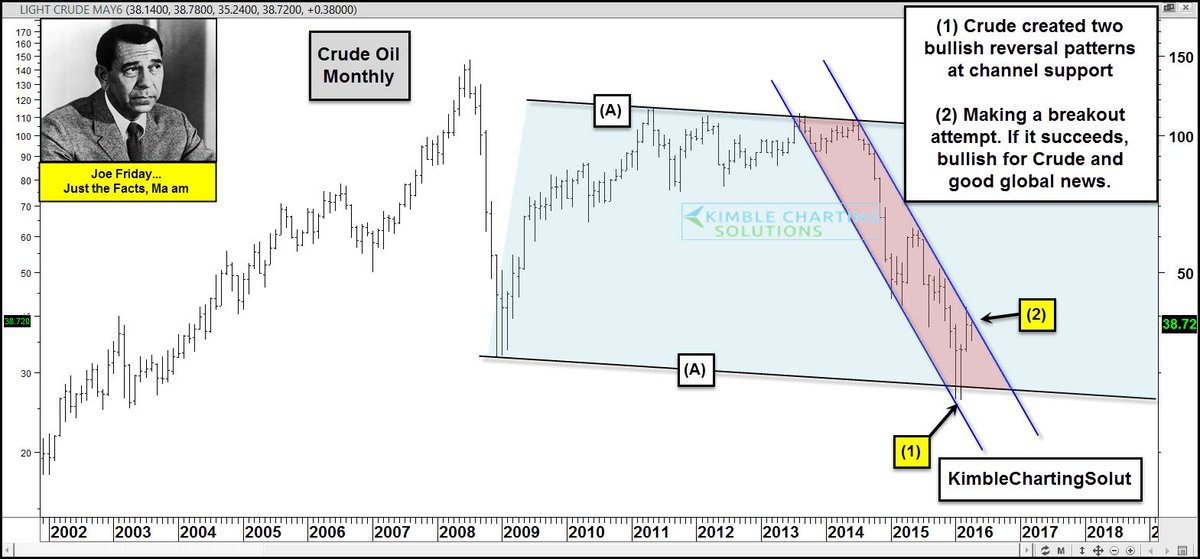

7. Oil

First,

- Ryan Detrick, CMT@RyanDetrick – Crude oil beneath its 200-day MA for 426 days. Far and away longest bear market it has ever had. Previous longest was 280 days in ’93/’94.

Where does Oil go from here? Some say down to $32 and then to mid-twenties. Some see a potential breakout:

- Chris Kimble

@KimbleCharting – Breakout attempt in play. If it does, should be good for stocks.$CL_Fhttp://blog.kimblechartingsolutions.com/2016/04/crude-oil-breakout-would-be-good-for-it-and-stocks-says-joe-friday/ …$USO$SPY

And what about oil stocks?

- Mark Arbeter, CMT

@MarkArbeter – Energy Update: Thinking one more low for$XLE into 58/59ish area to end wave 4. Looks like bullish wedge forming.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter