Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.On the way?

Yes it seems to be. Of course, by “it” we mean the promise of lower taxes & bigger paychecks. The Senate passed the budget deal on Thursday evening and the House is expected to pass the same bill next week. The final lap is the $1.5 trillion tax cut, sorry tax reform. We heard some one with impeccable credentials say on TV that it could be passed this year.

Was it already factored in by markets? Heck no, said risk markets. The entire Treasury curve shot up in yield on Friday and steepened too. Gold fell & stocks rallied. Why shouldn’t they? You have the stimulus from the hurricanes and now the $1.5 trillion tax cut. And if all this was not enough, even IBM went from really bad to not all that bad and rallied by $26. The final forget about it was sounded by Lakshman Achuthan of ECRI who told BTV to forget about recession any time soon. Wow!

The real wow is due to Jeffrey Gundlach who, on September 12, said that he was getting “a July 2016 type feeling in the bond market” and predicted a 2.44% 10-year yield by year end.We pointed out in our September 16, 2017 article that the 10-year yield rose from 1.36% on July 15, 2016 to 1.83% the day before the election. That is a rise of 47 bps. Well, the 10-year yield has already risen from 2.01% in the morning of Thursday September 8, 2017 to 2.38% on Friday – a rise of 37 bps. So a couple of days like Friday and the rise in the 10-year yield would match the rise from July 15, 2016 to the election and the 10-year yield would be at 2.48%, above Gundlach’s year end target of 2.44%.

Something interesting happened to the 10-5 year curve. It closed at 36 bps, a low for this year we think, a steep drop from the 51 bps at the end of 2016. And a drop of 6 bps from Friday, September 8, the day before Irma. Given that the big 4 on the Treasury curve are 30 yrs, 10, 5 & 2, the 10-5 spread is lower than both 51 bps for 30-10 spread and 44 bps for 5-2 spread. What does this mean? Frankly, we don’t know except the obvious that the force driving up the belly of the curve is stronger than the force driving the longer end up. Aggressive bond market or aggressive Fed?

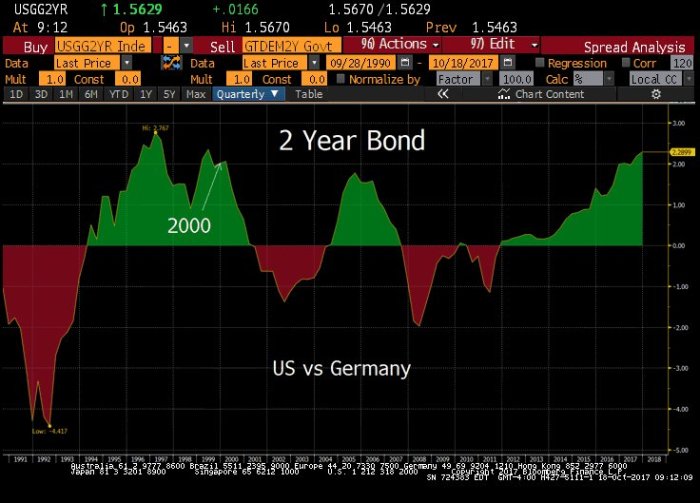

But wait! Didn’t Gundlach say the push upwards in Treasury yields would come from rise in German 2-year yields? That has not happened. The spread between 2-year Treasury yield and the German 2-year yield has widened to 2.30%. How rare is this?

- Lawrence McDonald @Convertbond Bond Yield spread US vs. Germany 2yr highest since 2000

If you look closely, you see that this current spread widening began in late 2010. Did it have anything to do with the start of QE? If so, will it begin reversing when QT begins in October 2017 as Chair Yellen has announced? Why is this important? Perhaps because, as J C Parets said to Larry McDonald in their podcast this week, the chart of the S&P shows a strong correlation to the 2-year Treasury-Bund spread.

If you look closely, you see that this current spread widening began in late 2010. Did it have anything to do with the start of QE? If so, will it begin reversing when QT begins in October 2017 as Chair Yellen has announced? Why is this important? Perhaps because, as J C Parets said to Larry McDonald in their podcast this week, the chart of the S&P shows a strong correlation to the 2-year Treasury-Bund spread.

The chart also shows that this spread widening is a part of the post-Irma trend, the trend that continues to be supported by rising expectations of a tax cut. Look at the performance of the asset classes since Friday, September 8, 2017 – the Friday before Irma:

- Dollar up 2.7%; Gold down 5.5%; S&P up 4.6% outperforming EEM (up 3.3%); Rates rising with 10-yr yield up 32 bps; 5 year yield up 38 bps & the 2-year yield up 31 bps; the 30-year a laggard with rise of 22 bps;

What can derail this train before year-end?

2. Happy Diwali – the Festival of Lights

Why read when you can watch?

[embedyt] http://www.youtube.com/watch?v=Xsoml52_asE[/embedyt]

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter