Editor’s Note: In this series of articles, we include important or interesting articles, tweets, videoclips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Repeat without Rinsing

Wasn’t “Rinse & Repeat” an adage of sorts? Well, 2014 has been a case of repeat without rinsing. The themes repeat almost every week – yield curve flattens, treasury yields move lower, stocks chop around and economy still waits for the growth “Godot”.

This week, the 30-5 yr yield curve flattened to 172 bps from 179 bps last week and from 223 bps on December 31, 2013. The entire Treasury curve fell a little this week but the bulk of the move down came on Thursday & Friday after Ukraine scared some on Thursday morning. And what about stocks?

- Ryan Detrick, CMT @RyanDetrick – $SPX down on week. The past 8 weeks looks like this – up/down/up/down/up/down/up/down. Ha. Chop city. Last time 8 wk alternating?

2. Twitter beating Fin TV?

The title of this series of articles, “Interesting Videoclips”, is rapidly turning into a misnomer. We simply cannot find FinTV clips that are worth discussing. We scan BTV, CNBC and FBN regularly to find clips that can teach us something, provide interesting insight into markets or add value in any real manner. The networks don’t have any.

Take CNBC – apart from Santelli’s clips, Cramer’s initial thoughts at 9 am and the two Fast Money shows, the rest of CNBC has almost become a waste of time. Ditto for BTV & FBN. Not all their fault though. The repeat without rinsing and the technical nature of the stock market has made most of their guests useless except for some occasional insights.

In contrast, the Tweetosphere has become much more interesting and useful. We get a lot of value from sharp tweets & interesting charts from many tweeters who tend to be traders or ex-traders. So those are what we include more and more. We don’t know the majority of people whose tweets we include and we remind readers that they should exercise their diligent & defensive judgement in reading such tweets & the charts referred to in the tweets. Caveat Reader is the loud message we want readers to get.

3. U.S. Economy

- “Sales of previously owned properties in March tumbled 7.5 percent from a

year earlier to the slowest pace in 20 months, while purchases of new houses 14.5 percent from February, according to reports this week. Mortgage applications to buy homes plunged 19 percent from a year earlier, indicating slowing

demand during what is typically the busiest season for deals.”

Why? Bloomberg wrote:

- It’s the reduction in affordability, the lack of inventory, also weak growth in median household income – all these are contributing to the sluggish recovery in housing,” said Ryan Sweet, a senior economist at Moody’s Analytics Inc. in West Chester, Pennsylvania, who forecast sales would drop in March. “It’s going to raise concerns

about the strength of the housing recovery, but it’s too early to be too

worried”

Elliot Wave International seems to disagree vehemently with the above “it’s too early to be too worried” message. The video & the chart below from their article Phase II of Housing’s Deep Slide paints a terribly different picture:

Fortunately others are more sanguine at least about other sectors of the U.S. economy:

- BlackRock® @blackrock – Rick Rieder: Finally, a clear picture of economy not clouded by weather. Latest manufacturing data = good sign for Q2 reut.rs/1hkzueg

- Gluskin Sheff @GluskinSheffInc – David Rosenberg: Richmond Fed index yet another in a long line of Q2 re-acceleration growth gauges

Jim Paulsen had the most optimistic comment about the economy on Monday, April 21:

- “if you look at the economy, it’s been awful good. we’ve got clay numbers that have been good, retail sales numbers better than expected. industrial numbers better than expected, confidence moved to the highest level of the cycle. i really think the economy might be growing close to 4% here in the second quarter”.

A two-handed comment from a trader:

- Mike Valletutti @marketmodel – Jobless claims, manufacturing, durable goods, confidence, all improved as FOMC meets again next week. Inflation only laggard.

- Mike Valletutti @marketmodel – Energy leads as macro improves. Financials lag as yields curve flattens, reflecting a slowdown. Only one is right.

4. Bonds

The 30-year yield fell by 7 bps (10-year yld by 5 bps) this week with a 4-day consecutive drop from Tuesday to Friday leading to:

- Urban Carmel @ukarlewitz – The most telling chart is 30-yr yields. Fresh 10-mo low yields today. There’s your growth story.

- Keith McCullough @KeithMcCullough – Hedgeye Risk Mgt reiterates the US #ConsumerSlowing in long bond $TLT terms

- Guy Adami on CNBC FM On Friday – sort of reaffirmed his $115 target for TLT.

- Scott Minerd @ScottMinerd – Areas of U.S. credit markets are overheating. This will be an important topic at #2014GC bit.ly/1jCHJ2i

How great has been the U.S. High yield rally?

- Lawrence McDonald @Convertbond – US “High Yield” Bonds – 2014: 5.08%**; 2013: 4.95%*; 2012: 8%; 2011: 11%; 2010: 11%; 2009: 24%

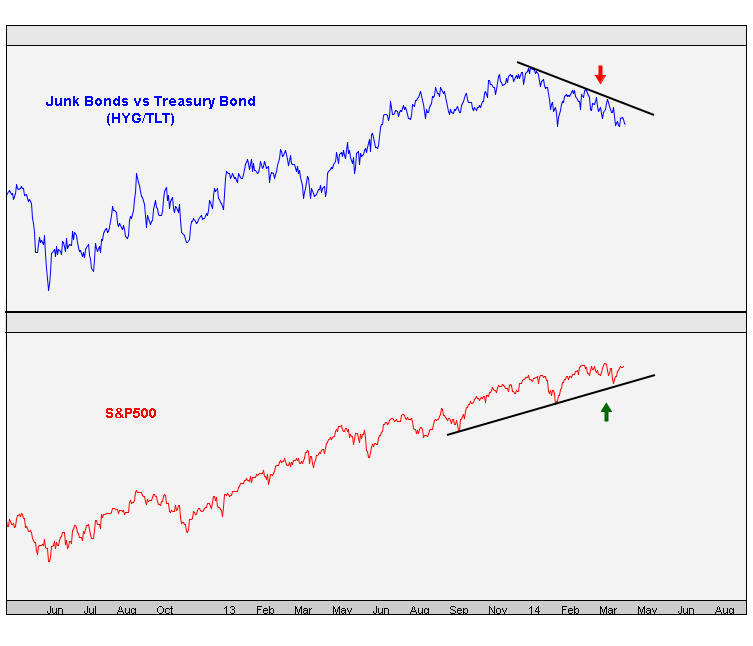

What about the divergence between the bond market & the stock market?

- J.C. Parets @allstarcharts – Bond Market Not Confirming the Stock Market in 2014 http://dlvr.it/5V0QJm

The Parets article is a good read and centered around his chart below. His bottom line:

- “I would look for a break to new lows in the HYG/TLT spread to confirm a new downtrend …. lower lows are likely in store for this bond spread. That’s not good for stocks.”

5. U.S. Equities

The most short term bullish call came from Jim Paulsen:

- “I really think the economy might be growing close to 4% here in the second quarter. and if it is anywhere as close to that. that is what is ultimately going to bring a bid back to Wall Street and push it towards 2,000.”

- “I think before the year’s out, we’re going to bring the Fed back into the equation in a big way. and i think what’s going to do that is economic growth. I think if the economy’s probably going to grow about 3.5% this year, far more than people expected. and that initially is going to push stocks higher. good news is good news for the stock market. but I also think it’s going to start to push bond yields higher. and at some point, good news may become bad news for stocks. and part of that equation will be people may come to the opinion that the Fed’s behind the curve. and we may — we may have a mini overheat panic in the second half with the fed playing center stage on that in terms of how fast if they have to accelerate their tapering program”

If Paulsen is at 2,000 Jeff Kilburg of CNBC Futures Now is at:

- “feels like computers are locked & laser-focused on printing 1900; one thing no one is really talking about is the lack of inflation over in Europe; so will ECB come with a trillion dollar QE?; that will certainly push us above 1900 but feels a little fatigued up here so I am a little cautious I do think we will see a new high – but 1900 prints in my mind 1800 could certainly print one month later”

The difference is that Kilburg is a trader and Paulsen is an investor of other people’s money. So Paulsen is “long term” without stops & Kilburg could turn around next week.

Was the sell-off on Friday due to Ukraine or due to margin calls? Rick Santelli pooh-poohed the Ukraine impact as marginal and Steve Grasso of CNBC FM argued that it was mainly margin.

5.1 U.S. Equities – Margin

The first should surprise no one:

- Elliott Wave Int’l @elliottwaveintl – This chart shows that investors have gone from optimistic to overoptimistic to a near frenzy http://bit.ly/1k4gErV pic.twitter.com/IqKG00RNz1

The article and video in their article What Happens When Borrowed Money Buys $178 Billion in Stocks?

elaborate on the point made succinctly in their chart below:

The second comes from Jeff Copper & Minyanville via Are Margin Debt Levels Pointing to a Peak in the S&P 500? He writes:

- “The point is that there is beaucoup leverage today, and it is among the professionals and corporations. ..My friend, a fellow trader, made an important point: “Given the market

has shown distribution over recent weeks, we should keep watch for a

change in direction of margin balances. A significant drop would be

confirmation that a top may be in for the year“

Cooper also looks at margin debt as a % of GDP and shows an interesting comparison:

So is Cooper definitely bearish? No because,

- “I can’t help but think that one of the reasons why risk continues to be

skewed to the upside in the US equity market in spite of the mountain of

debt shown above is that the investment community has a Sherpa called

the Federal Reserve Bank“

Well, the Sherpas of Nepal went on strike this week. And Cooper’s Sherpa speaks next week in the FOMC statement. This Sherpa is slowly going on strike by tapering by $10B at every meeting. But that shouldn’t worry anyone because tapering is not tightening, right? The big difference between the two Sherpas is that several Nepali Sherpas died this past week on Everest while the Fed Sherpas are killing American incomes.

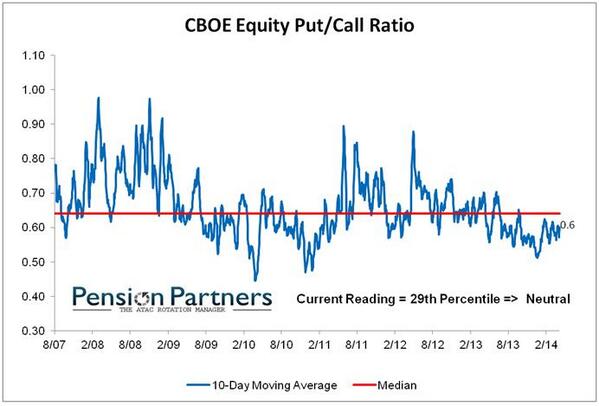

5.2 U.S. Equities – Sentiment

The first again from:

- Elliott Wave Int’l @elliottwaveintl – This proven stock market indicator is sending a SCREAMING message http://bit.ly/1nEVUIf pic.twitter.com/H0Xzkx4S1P

The chart below is from their article:

.

.

When else did we see this before?

- Urban Carmel @ukarlewitz – Hmm. A 7-mo high in II bears. From a 27-year low in Dec. That also happened in July ’11. And June ’98. And others. Context

Does a low in bear-count suggest complacency?

- Charlie Bilello, CMT @MktOutperform – Biggest headwind for US equities here is same headwind we saw on Jan 1, just massive complacency out there. #putcall pic.twitter.com/vl17DXVBgP.

and from,

- Jeff Cooper @JeffCooperLive – Is $NDX setting up for a snap of double bottoms (3400) and 200 dma next week. Crashes come from complacency not excessive bullishness #VIX14

5.3 U.S. Equities – Short Term Market Direction

From veteran trader Lawrence Altman:

- traderxaspen @traderxaspen – 14 day moving avg has crossed below 30,50 ma and all sloping down in Sp nasd and Russ negative on charts

- traderxaspen @traderxaspen – The mkt looks very vulnerable !! Yesterday’s higher open and sell off all the stocks with good earnings lower accept Appl

and from,

- Scott Redler @RedDogT3Live – $QQQ could be forming right shoulder of macro Head & Shoulders pattern. Weak reaction to strong earnings also bearish http://ow.ly/i/5mB5F

Redler explains in his chart (best viewed in original):

and,

- Charlie Bilello, CMT @MktOutperform – If this is a lower high here, the long-awaited test of the 200-day may not be far off. $SPX pic.twitter.com/jScDrnzNRI

again, his chart tells the story:

But what about seasonality of April-May?

- Urban Carmel @ukarlewitz – Next week: April typically ends strong + May begins strong. After that, May is weak. FOMC + GDP Weds and NFP Fri pic.twitter.com/g6ms0o2sls

5.4 U.S. Equities – Sectors: Small Caps, IPOs & BioTech

Richard Bernstein argues that U.S. small caps are in a secular bull market. The market has not concurred for a few weeks and neither do the following:

- Retweeted by Michael A. Gayed, CFA – SJD10304 @SJD10304 – To quote @pensionpartners…”smaller caps” weakness is looking like 2011. A sharp, fast, violent correction on deck? pic.twitter.com/MPQtQhx3Ab

- Ryan Detrick, CMT @RyanDetrick – $RUT is up 7 quarters in a row for the first time ever. That doji on a monthly chart last month looks potentially ominous to me. $IWM

- J.C. Parets @allstarcharts – So the Russell2000 is looking at 10-month closing lows versus the S&P500. Another feather in the hat for the bears #WeightOfTheEveidence

If we recall correctly, Jeff Chmielewski tweeted a timely tweet about buying $IWM puts this week. On Friday he tweeted:

- Jeff Chmielewski @JeffCNYC – Even if $IWM drops 20 points it will still be overvalued.

- Jeff Chmielewski @JeffCNYC – @DollaScholar Forward P/E on S&P around 15.xx, Russell close to 20… Can make a case $IWM should be sub-90.

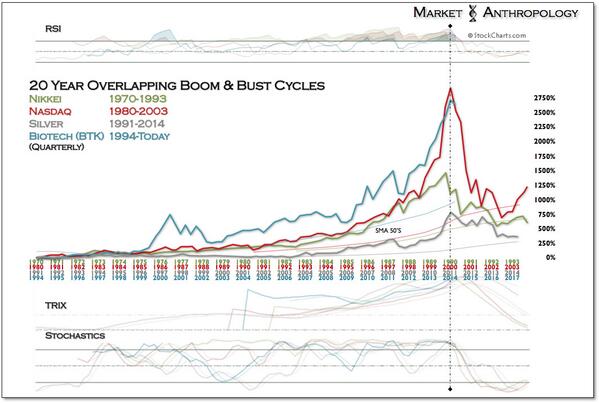

- Market Anthropology @MktAnthropology – 20 yr overlapping boom&bust cycles – from: www.marketanthropology.com/2014/04/whats-up-with-silver-gold.html … pic.twitter.com/himvhNWBG3

- Ryan Detrick, CMT @RyanDetrick – Commented on StockTwits: +1 “@KimbleCharting: Party like its 1999? Losing IPO’s hitting 1999 record levels again!… http://stks.co/c0Toj

- Ryan Detrick, CMT @RyanDetrick – Big spike in $GDX late vs. $GLD not doing much. Not 100% sure what it means, but I am long $GDX

- “One of the largest suppliers of gold, and of course platinum, is Russia,” said George Gero, precious metals strategist at RBC Capital Markets. “And if they’re going to be involved in sanctions, and more problems with Ukraine, and deliveries are curtailed—and there is already a problem in South Africa between the miners of platinum, palladium and the mining companies—all of that could somehow explode on the upside and curtail deliveries, meaning higher prices.”

- “You have option expiration tonight on the Comex, and options, when in-the-money, become futures contracts,” Gero said. “And we have more puts than calls that could be in-the-money if the price goes lower from here. And that means there will be large short positions to be covered, or very large margin calls.”

- Elliott Wave Int’l @elliottwaveintl – “Gold is at or near end of its upward run” Get our forecast for Gold & other markets we follow bit.ly/1hlqcdC pic.twitter.com/qPf9bqThEN

-

Weekly flows show bond inflows ($3.3bn) outpace equity inflows ($2.9bn)

-

Second straight week of outflows from floating-rate funds (longest outflow streak since Jun’12); HY and IG bond funds still catching a bid

- EM: 4 straight weeks of inflows (albeit small $0.4bn)

- Europe: 43 straight weeks of inflows

- Japan: modest $0.3bn inflows

- US: $0.5bn outflows (all via LO funds)

- By sector/style, rotation from healthcare to energy and from growth to value funds (Chart 1)

- Long-term uptrend support lines — In the February issue, we identified 11 emerging markets that were testing long-term uptrend support lines. All 11 have since rallied from lows in the first quarter of 2014.

- Infotech sector outperformance — In the March Asian-Pacific Finanical Forecast, we showed how Infotech had led the MSCI Emerging Markets Asia sector indexes since the 2011 lows.

- Extreme negative sentiment — In the new issue, we show you how short interest for a popular ETF tracking Chinese companies listed in Hong Kong hit a record high of 29% of outstanding shares even as underlying valuations hit 12-year lows. That’s fear at work.

- Blood in the streets — Anecdotally, the 2013 and 2014 lows in emerging markets generated negative mass social events that were comparable in magnitude to those we saw at significant stock lows in the past. (The April Asian-Pacific Financial Forecast gives you two fresh examples.)

< /ul>

Earlier in the week, we saw a few tweets & charts arguing about a rally to new highs. Clearly they were proven wrong by the end of the week. Similarly many of the above tweets could be proven wrong next week perhaps due to the wickedness of markets, economic data and/or the Fed. So Caveat Reader is our message in the strongest possible manner.

Biotechs have been a hot sector this year at least until very recently. How hot? Intensely so according to the following tweet & chart:

But what about Hot IPOs as a sector?

Haven’t you heard the old saying about many many charts lying at the bottom of the ocean? Well, we might see that next week with many of the charts above if the alternating up-down weeks pattern described by Ryan Detrick above holds next week.

After all, Chair Yellen could surprise positively, the payroll number could come in at 250K or higher and/or Putin might throw in the towel and go take a vacation at the Black Sea ports he just acquired. A strong rally would essentially make many of the above charts invalid and so, once again, Caveat Reader.

6. Gold

Like the actions of some people precious to us, we can’t make any sense of the action in precious metals. Apparently, we are not the only ones:

But Friday’s rally came as George Gero told viewers of CNBC Futures Now on Thursday afternoon:

And predictably the opposite view:

7. Rotation all over again?

According to this week’s report from Michael Hartnett,

And the breakdown of equity inflows?

Hartnett adds:

His chart 1 is expressive:

Source: BofA Merrill Lynch Global Investment Strategy, EPFR Global

But Carter Worth of Stern Agee & CNBC Options Action was unimpressed. He called the rotation from growth to value as “epic” but added that when value succumbs (his tone implied it would) then growth would not recover & then the S&P will go lower as an index. Of course, the webmasters at CNBC.com deleted this comment from their videoclips. So the above is our recollection subject to the vagaries of our memory.

The inflows into EM fit with the rare bullish call that we saw from Elliott Wave International in their article Emerging Markets To Begin a New Uptrend? The chart & the excerpts below are from this article:

“The past few issues of our monthly Asian-Pacific Financial Forecast have detailed important evidence supporting a low in emerging markets:

Now, such negative fundamentals and sentiments provide a classic contrarian backdrop.”

This seems to be a directional call and not a relative EM-S&P outperformance call. Historically, EM markets have needed S&P to behave itself and Elliot Wave is screamingly negative on the U.S. stock market (see 5.1 & 5.2 above).

Another way of saying Caveat Reader is a la Sgt. Esterhaus of Hill Street Blues “Let’s Be Careful Out There next week” (exit line introduced years ago in his daily by Dennis Gartman).

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter