Editor’s Note: In this series of articles, we include important or interesting tweets, articles, videoclips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

1. The Draghi Reality.

Back on May 10, we thought Mario Draghi had served notice. The markets certainly read his notice and acted on it as we described last week in The Draghi Effect. Next week Draghi comes to play. Will he throw a deep ball, run just enough to get the next series of downs or punt?

Mark Grant of Southwest Securities to Rick Santelli on Friday:

- “it could be as benign as lowering interest rates, going negative on short rates, or it could actually be quantitative easing. I think it’s very up in the air, but you can bet their going to do something“

John Brynjolfsson of Armored Wolf on CNBC SOTS on Friday:

- “Expect ECB to act more forcefully“

Rick Rieder of BlackRock to BTV’s Tom Keene on Thursday:

- “Draghi & the ECB are going to be incredibly aggressive going forward driving in European bond yields … Draghi is going down the road of negative deposit rates and I think ultimately he is going to talk about other forms of loose quantitative easing, asset backed purchases … I think this time it is different because the Bundesbank is, from everything they have described publicly, understands that there is more firepower that has to go“

We are also inclined to expect something from Draghi because of a very different reason. We think the results of the European elections have served notice to the European elite in Brussels that the European people are fed up & ready to ditch the European Union. And the only one among them who can act unilaterally is Draghi. So we expect there is serious pressure on him to create some growth. And what does that mean to a central banker – Reduce rates, Add Stimulus, and Weaken the currency.

But what if Draghi only delivers verbal stimulus or acts minimally?

- Art Cashin on Friday – “If Mario Draghi does not do anything of significance next week, then I think the market is going to have a serious reaction“

- Rick Santelli on Friday – “that will be negative for equities and positive for fixed income” [as we recall – cnbc webmasters deleted this concluding remark of Santelli from the clip on cnbc.com in their infinite stupidity]

Assuming Draghi does something, how should investors react?

- Tim Seymour of CNBC FM on Friday –“it’s been priced in. there’s definitely a setup that could be disappointing. I think they will cut the refi by 15 points which will get the deposit rate into negative territory. they have been trying to get the banks to lend; they have structural issues we know in Europe they still can’t really be doing the asset backed buying and the QE like we did here. if you think it’s game on for more stimulus, markets could trade higher”

- Steve Grasso also of CNBC FM – “to Tim’s point, if it is priced in, then does that mean you sell the news? is that a sell the news — that’s what it sounds like. I agree with that. We are really at a pinnacle – overbought level is 1923 that got hit today”.

The next week is going to be a big one – China PMI over the weekend, US PMI next week and employment numbers on Wednesday & Friday with ECB meeting on Thursday. Which is the most important?

- Rick Santelli on Friday – “pay very close attention Thursday to the ECB meeting. I think it will trump Friday and Wednesday’s employment data because when a central bank is giving so much attention to the fact that we need new stimulus, after such a crisis, after 2013 was all about European stabilization, I think there’s a bit of worry beads that need to come out at this point”

To our simple mind, Draghi has been the main extractor of volatility from financial markets since August 2012. And volatility is now virtually moribund. Will it arise & shoot up like the old faithful it used to be? The conditions are in place:

- Thursday afternoon – Kristian Kerr @KKerrFX – VIX DSI at 8% Bulls

2. U.S. Treasuries

How awesome was the rally in Treasuries on Thursday morning? In the words of CNBC’s David Faber – “takes your breath away if you are a Bond Nerd“. The entire 5-30 year yield curve fell by about 7 bps on Thursday morning.

Then Rick Santelli came on at about 945 am to say “something has changed”:

- “something has changed. Bunds to 10 yr treasuries in my opinion, started giving you clues that something wasn’t quite right in the global economy. or at least the manipulation of rates in Europe as the boom made its adjustment. look what’s happened. that distance right around tax day, was 121 basis points between our 10s and their 10s – 9 and half year wide. it’s now into 108. this is something you want to pay attention to. maybe it will mean rates will stop going down. we want to watch this. in terms of the euro “.

Back on Thursday, May 8, long treasuries reversed sharply after the 30-year auction on that day. And this Thursday, long maturity Treasuries reversed their morning gains at 1 pm after the tepid 7-year auction as the chart below depicts.

Or perhaps TLT had simply reached the top of the channel, the channel Helene Meisler had been tweeting for three consecutive weeks:.

- Helene Meisler @hmeisler – The line is still in play cc: @Hooper_Quant pic.twitter.com/8sHQKUxqz7

Last Thursday, this lower line of this channel provided a buying opportunity in TLT; this Thursday it provided a selling opportunity. What will next Thursday bring? Yes, that is the Draghi Thursday.

Some like Rick Santelli would argue that a weekly close for the 10-year yield below 2.50% is significant. Some use 2.47%:

- Thursday Karl Snyder, CMT @snyder_karl – $TNX on weekly chart some support 2.39-2.40 so a possible bounce / hesitation but longer under 2.47 opens door 2.37 & potentially 2.32

Larry McDonald of NewEdge reiterated his argument that the action in long treasuries is simply capitulation by the shorts:

- Friday – Lawrence McDonald @Convertbond – US 10 Year Treasury Feels like we just hit the short term bottom on bond yields, nice 7bps bounce off 2.40% #Capitulation

A more serious up turn in yields was predicted back on May 19 by Elliot Wave:

- “Preferred Elliott Wave view suggests US 10 year yields have completed a cycle from ( B ) high i.e. (2.748%). As it was a corrective drop so we have labelled it as wave “W” and treating the current bounce as wave “X”. Yields are showing just 1 swing up from the low and corrections run in 3, 7 or 11 swings so while above 2.473% low, expecting another push higher to complete wave “X” before the declines. Levels to watch on the upside are (( c )) = (( a )) = 2.544, (( c )) = 1.236 x (( a )) = 2.555 and (( c )) = 1.618 x (( a )) = 2.574%. This view is valid as far as pivot at blue ( B ) i.e. 2.748% high remains intact.”

Despite the reversal on Thursday, 30-year & 10-year yields fell by 7 bps & 6 bps this week while the 5-year yield rose by 1 bp thus flattening the curve. What happens next week will depend on next week’s ECB meeting and the payroll data.

3. Bonds vs. Equities

Last week we discussed the possibility of both stocks & treasuries correcting in price simultaneously. The tweet below is along the same lines:

- Tsachy Mishal @CapitalObserver – I am now in the camp Tepper used to be in. In order for the stock market to get hit rates need to rise first $TLT

As we recall, Keith McCullough of HedgEye had remarked earlier that TLT, the 20-year Treasury ETF, should be considered the inverse of IWM, the Russell 2000 ETF. This point was made graphically this week in:

- Thursday – Helene Meisler @hmeisler – Everyone, me included, been watching TLT:SPY when it’s TLT:RUT we should watch. I feel ike the quick brown fox. pic.twitter.com/mcoAXC6yt2

A flattening in the 30-10 year yield curve has not been positive for equities according to:

- Charlie Bilello, CMT @MktOutperform – Learned the hard way over the years that most divergences don’t matter. Here’s one that does. papers.ssrn.com/sol3/papers.cfm?abstract_id=2431022 … pic.twitter.com/o0tQGM3dPv

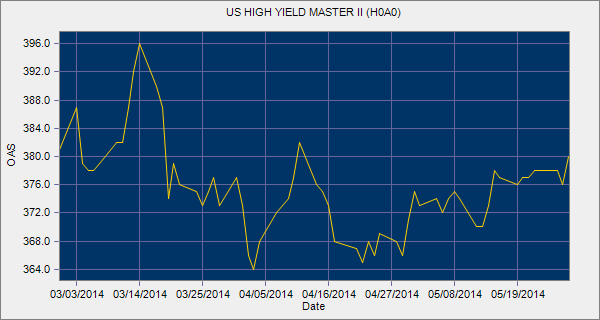

What about High Yield credit and Stocks?

- Thursday – Charlie Bilello, CMT @MktOutperform – $SPX at new all-time highs but credit spreads slowly widening. This is different behavior from what we’ve seen. pic.twitter.com/p5RhyEq5EF

GaveKal made the same point in their article Canary in a Coal Mine? on Wednesday:

- “High-yield (junk) bonds historically have had a high correlation with stocks, and for this reason, they often serve as an early warning indicator for equity investors. In the chart below, we show 15 years of history of junk bond spreads alongside stocks. Junk bond spreads have a history of widening before stocks turn down. Junk spreads peaked in May 1999 and June 2007, preceding the end of the bull market in stocks by months. Widening spreads also preceded the correction in 2011.”

- “We bring up this relationship because junk spreads appear to be in the early stages of widening. Spreads reached a maximum compression of 2.45% in April 2014 and have since been widening, recently reaching 2.64%. Spreads are separating from the equity market, and historically this is a canary in a coal mine for equity investors to rotate into a more defensive posture.”

4. U.S. Equities

The Dow and the S&P closed at yet another new all-time high on Friday. The action impressed many smart folks:

Je

ffrey Saut of Raymond James:

- “my view that the SPX is going to extend into the 1950 – 1975 zone before becoming more vulnerable to a 10%+ drawdown”

Lawrence McMillan of Option Strategist:

- “The broad market, as measured by the Standard & Poors 500 Index ($SPX) and other indices, has broken out to new all-time highs again. This time, the breakout quickly extended with a strong second day, and today added even more distance. This has turned the $SPX chart bullish”

- “In summary, the outlook is now solidly bullish, although the overbought conditions — especially the low volatility indices — indicate that a sharp, but likely short-lived correction is possible at any time“

Tom McClellan in Equity Options vs. Index Options:

- “10-day moving average of the daily ratio of total equity options volume versus index option volume as traded on the CBOE. It sums together the puts and the calls in each category. The range of values tends to wander a bit over time, and so I have also added 50-1 Bollinger Bands (50-day MA, and bands are set 1 standard deviation above and below). When this indicator goes up above the upper 50-1 band, it can indicate a topping condition for prices, and the opposite meaning comes from dips below the lower band”.

- “this indicator has just dipped below the lower band. It is an unusual condition to see the indicator this low while prices are making higher highs, but it has nevertheless happened before. The meaning is still bullish even at a higher price high. The implication is that the breakout move in the SP500 should be able to continue higher because of the sentiment message revealed by this indicator”

Back on May 10, the closest we could find to a bull was the tweet below:

- Minyanville @Minyanville Todd Harrison: Keep in Mind the Bull Case for the S&P 500 www.minyanville.com/special-features/from-the-buzz-banter/articles/Todd-Harrison253A-Keep-in-Mind-the/5/7/2014/id/54886 … pic.twitter.com/U1BcMyS6cx

He proved to be spectacularly right. What did he tweet on this Friday, May 30?

- Minyanville @Minyanville – Todd Harrison on what to watch as we slink into summer 2014: shar.es/V8j77 @todd_harrison pic.twitter.com/q4nQZNTCqe

His reverse head & shoulders formation point to 1975, it seems.

The overbought condition bothered some bulls & suggested a pinnacle (to borrow the word above of Steve Grasso) to some others:

- Thursday – Vconomics @Vconomics – I continue to be bullish but I would pare back (or hedge). The S&P is approaching major resistance. $SPX $SPY -> pic.twitter.com/0CN8NbaQgD

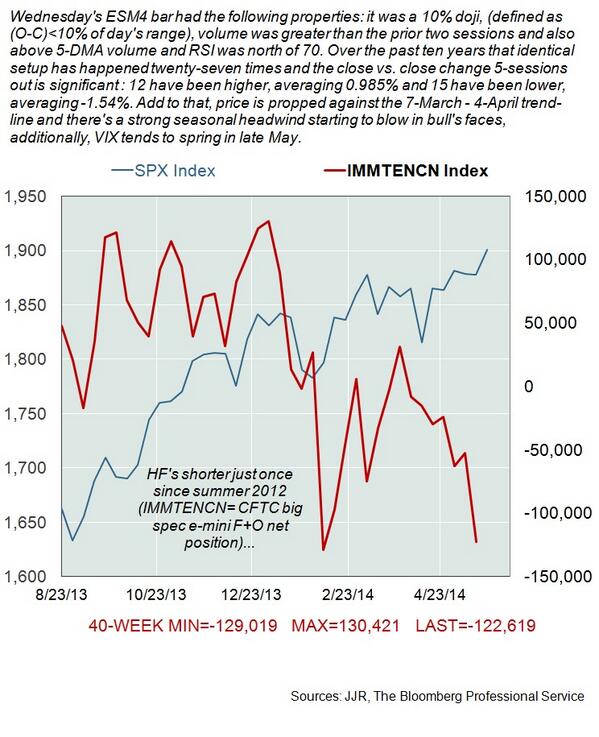

- Thursday – Jack Rodeghier @glarustrading – SPX: heightened indecision, O/B RSI at key resistance. HF’s shorter just once over past 2-yrs. Seasonal pivot near? pic.twitter.com/3BdFQVfNZ3

Walter Murphy seems to be in the market is wrong category based on his article Has S&P Missed the Message?

- “We have regularly pointed out that there has historically been an inter-market relationship between the S&P, yields, the euro, and select commodities. With that in mind, it seems important to note that 10-year yields, the euro, and gold have all recently broken down through important support trend lines. These breakdowns, along with price counts and weak momentum, suggest that lower lows are likely for these assets.Nonetheless, and despite these inter-market pressures, the S&P has continued higher to all-time highs.”

- “So the question is: Who missed the message? Was it the “500” or the other three asset classes? Given the equity market’s overbought momentum and sentiment indicators, as well as fragile seasonal considerations, it would seem that the S&P it the one listening to the wrong message“

And an outright sell signal came from:

- Friday – RR Trades @rr_trades – $QQQ daily Demark sell setup. Poss double top (from March peak). pic.twitter.com/hPriE5Tc2a

5. Emerging Markets

The emerging markets underperformed the S&P 500 this week. Was it simply a correction of a class that has been trading very well since the first week of February as Tim Seymour of CNBC FM seemed to suggest on Friday:

- “Emerging markets had their fourth up month, first time they have done this since ’09. Emerging markets are trading better.”

Or did something change on Tuesday?

-

Tuesday – J.C. Parets – @allstarcharts Chart of the Day: Emerging Market Currencies Break Down http://dlvr.it/5nyVx2

He explains in his article:

- “This is a daily ratio chart where Emerging Market Currencies ($CEW) represent the numerator and US Dollars are the denominator ($UUP). We can see the nice rally from the beginning of the year that kick started the recent strength we’ve seen in emerging market stocks. But now we’re running into former resistance as momentum rolls over and uptrend lines are breaking”

Of course, all this can change next week with the Draghi meeting & US data.

6. Gold & Silver

For metals that are called precious and look glowingly attractive, the action in these metals & their ETFs was uglier than any adjective we can think of. The traditional relationship between Gold and Silver was highlighted in:

- Tuesday 5/27 – J.C. Parets @allstarcharts – If there was any real risk appetite for metals, silver would be outperforming gold, not underperforming stks.co/c0b0r $GLD $SLV

He got more bearish & more direct by Friday:

- Friday – J.C. Parets @allstarcharts – I see every bounce from this support rolling over at lower & lower prices, which tells me sellers getting more & more impatient $SI_F $SLV

- Friday – J.C. Parets @allstarcharts – Look at Silver right now. If I went into the weekend long $SI_F or $SLV I would not be able to sleep stks.co/b0bst

- Friday – Market Anthropology @MktAnthropology – Anyone who thinks silver is breaking down is lost and staring at the trees in a really big forest.

- “Considering the strong technical framework that gold typically trades in we expect the divergence will resolve when gold completes the balance of the pattern. While the breadth of the move has been unusually massive, the prospective inverse head and shoulders pattern is a more typical technical reversal for gold to complete”

Assuming the action in gold has something to do with the action in EURUSD, below is what these two think of that pair:

- J.C. Parets @allstarcharts – nice solid bearish engulfing monthly candle in Euro as we head into next week’s ECB pow wow $EURUSD stks.co/d0bnW

- Market Anthropology – “Although we understand Draghi’s contractual agreements with jawboning the currency lower when he can, the truth is its effects are short-lived and the eventual breakout – should it come, more severe as the short-base grows increasingly entrenched. … Conditions are ripe for disappointment for euro bears and dollar bulls as the currency pair sets sail into next week with a record cargo of short positions.”

Thankfully, Draghi is not Godot. So we only have to wait until next Thursday.

7. A Truer Statement was hardly ever made

You decide if we are right:

- Captain Crom ☠ @theagilepirate – Genius at #xp2014 lightning talks. No further comment needed pic.twitter.com/PSXXK9rYOx

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter