Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Engine expertise vs. Transmission experience

Rebuilding trannies is a very difficult job. We found that out the hard way a long time ago as a poor graduate student with a used car. You can have the greatest engine in the world but your car wouldn’t do a thing if your transmission refuses to cooperate. The economists at the Fed are like experts in the engine of the economy – they manage the starting ability, the optimal horsepower of the economy, they decide how hard they should press the accelerator or how softly they take the foot of the accelerator. But they, as Bernanke proved in 2013 and as Yellen is proving now, don’t have a clue how the transmission of the economy works. By that, we mean the interest rates market, the yield curve. It is the interest rates market that has the job of transmitting the stimulus delivered by the Fed to the economy.

Greenspan semi-honestly called his ignorance of how long treasuries trade a “conundrum“. Bernanke was utterly arrogant and, throughout 2013, he stuck to his egoistical belief that he could speak to the bond market and the market would follow his guidance. The result was the disaster now termed the Taper Tantrum of 2013.

Chair Yellen seems be the opposite. She is utterly afraid of provoking another tantrum in the Treasury market. That is why she sounded so dovish this Wednesday in her presser. Read what William Lee of Citigroup said on CNBC FM on Thursday:

- “… the one thing the Fed is much worried about is taper tantrum; the Fed anxiously wants to get rates off zero; They are tring to reassure everybody that they are going nice and slow, nice and gradual, we are going to have nice smooth increase in interest rates … will the bond market be able to give them a smooth ride or will it bumpier than they think it is going to be … I think the bounces are going to be very severe … what did we learn from taper tantrum? people want to get ahead of any rate increases … “

Read what Stanley Druckenmiller said on CNBC on Tuesday, March 5, 2013:

- “Do you know what guys like me are going to do when they sell the first bond out of 4 trillion? … what do you think the markets are going to do when they figure out the exit?”

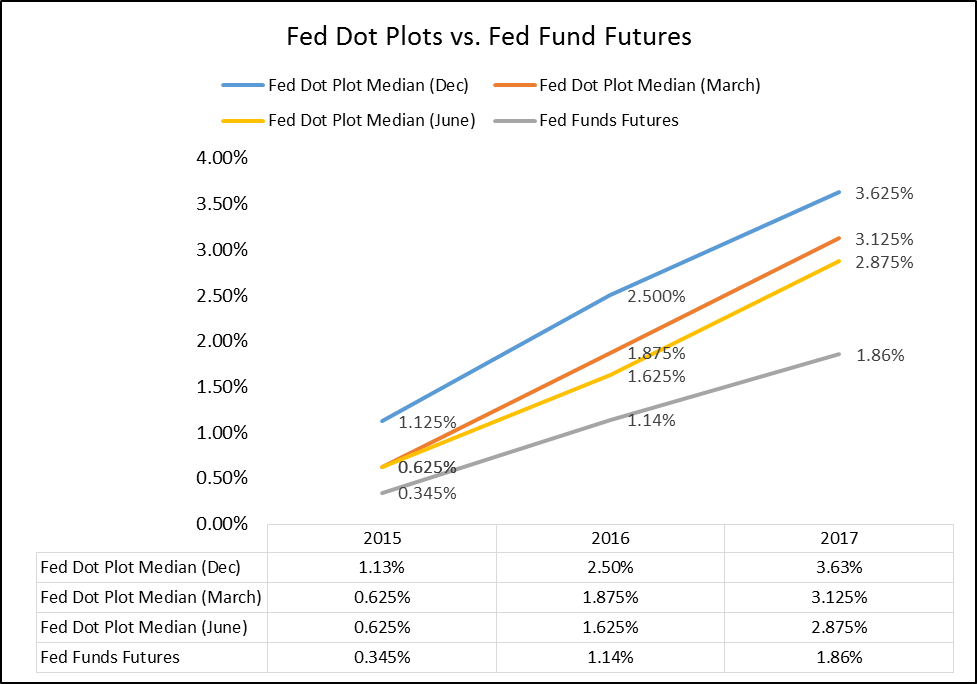

Chair Yellen has now made the same mistake Bernancke made in 2013 – she did not raise rates when the data supported her and when the bond market was receptive to a rate hike. Just as Bernanke did not taper in mid-2013 when the bond market was ready for it. Instead, he tried to guide the bond market and the uncertainty & fear of what he might do caused serious overshooting of interest rates. By the time Chair Yellen begins to raise rates it might be more dangerous to the economy. Read what James Paulsen of Wells Capital Management said on CNBC on Friday:

- “Our concern is not that by waiting so long, the Fed is behind the curve (although that also is possible). Rather, by waiting too long to start the process, the Fed has allowed its traditional exit ramp (i.e., raising interest rates against strong gains in corporate profits) to expire… Consequently, the Fed is now about to begin the process of raising interest rates without its traditional buffer of recovering profitability … Although profits are likely to continue growing in the next few years, even under the most optimistic assumptions, earnings growth will not be as dramatic as it was earlier in this recovery … The Fed’s exit ramp, which normally buffers the impact of its early tightening moves, has already expired.”

Similar views prompted Rick Santelli to restate his conviction that the Fed will not raise rates in 2015. The consensus on Thursday seemed to be that December would be the first hike and not September.

- Wednesday – Charlie Bilello, CMT ?@MktOutperform – Fed Dots move closer to market but they stand firm in 2015. Fed wants to move but market doesn’t believe it yet.

Read what Danielle DiMartin Booth, until recently an advisor to the Dallas Fed, said on BTV on Thursday about the Fed honchos:

- “From the perspective of somebody who looks at the world through the prism of the financial markets, I don’t think they are given enough credence in the decision making process at the Fed … there need to be more who understand the financial markets who have been, who have actually worked inside the markets, who understand the fixed income markets, especially the currency markets; people who have been on the street … ”

This is we publicly urged the appointment of a Bond Trader as the Fed Chairman or Vice Chairman on June 22, 2013. Our point was simple – for Fed to successfully drive the economy, they need equal expertise in the stimulus engine AND in the transmission mechanism of the interest rates market. Our choice at that time was either Stanely Druckenmiller or Bill Gross.

2. Greece

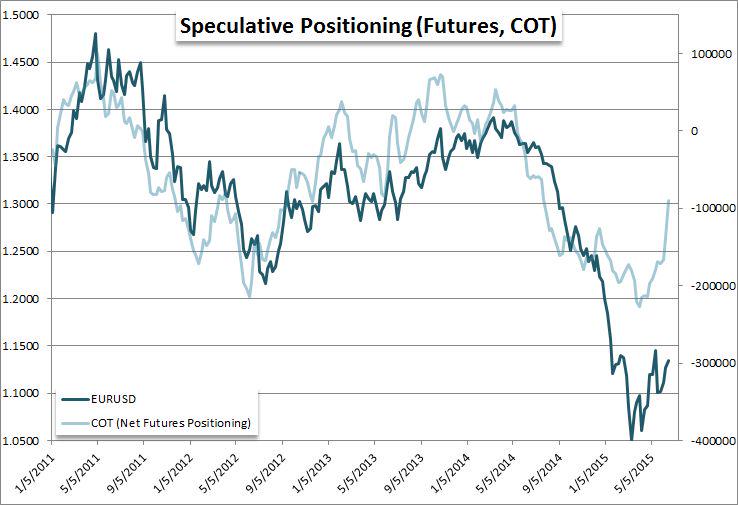

Now that the Fed is behind us, the biggest question mark is Greece. There is clearly nervousness in the markets, but the overall feeling seems to be what Paul Richards of UBS articulated on CNBC FM 1/2 on Thursday:

- ” … they need a deal but they are ready to wait another 2 weeks … just at the last minute someone blinks & they are going to blink; Draghi is owed 3.5 billion on July 20th and he wants his money back; Merkel is going to be the key in my opinion; stay long the Euro; market is short; I think its going to 116.5… “

The large speculators seem to be leaning in that direction:

- Friday – John Kicklighter ?@JohnKicklighter – Speculative futures traders cut their net short Euro position this past week by the most in 3 years ($EURUSD)

Another school of thought argues that a Grexit would actually be a positive because a Europe without Greece would be stronger. This is a “Lehman Bankruptcy would be good” argument. Now let us be clear – A Lehman dissolution that preserved Lehman Bonds but let the Lehman stock go to zero might have been OK because the big difference between Lehman & Fannie-Freedie was that Fannie-Freddie bonds were held safe.

Similarly, a Greek end that preserves Greek Banks might be a safer “exit” than just letting them go. After all, what was the biggest difference between 2008 & 1930s – TARP which protected US Banks while the Fed let the banks go in the 1930s. As Charles Dallara, previous managing director of the Institute for International Finance, said on CNBC On Friday:

- “The dilemma there is how to mange the Greek banking system, because the Greek banking system is on a lifeline right now from the ECB“

On the other hand, the biggest obstacle is the sanctity of the Euro. They could create a la petit eurochma or simply a Guro that is struck cheaper than the Euro for a few years. That spread could be made to contract as Greece gets back on its feet. But that would take time. And they don’t have the time unless they punt right now. Only Merkel can get Greece a safety net for now and she might because:

- Tuesday – Richard Bernstein ?@RBAdvisors – Remember #Germany needs #Greece more than Greece needs Germany. http://icont.ac/2Yfqs

What happens if Grexit becomes a mess? Charles Dallara said on Friday:

- “I am somewhat concerned that investors are looking at this and thinking the Germans, the IMF, the Greeks, they’re all rational players at the end of the day, and we can all hope that they will be; But right now it looks to me as if the markets are not prepared for a default and this could be a bloody bath if it happens.”

3. Treasuries

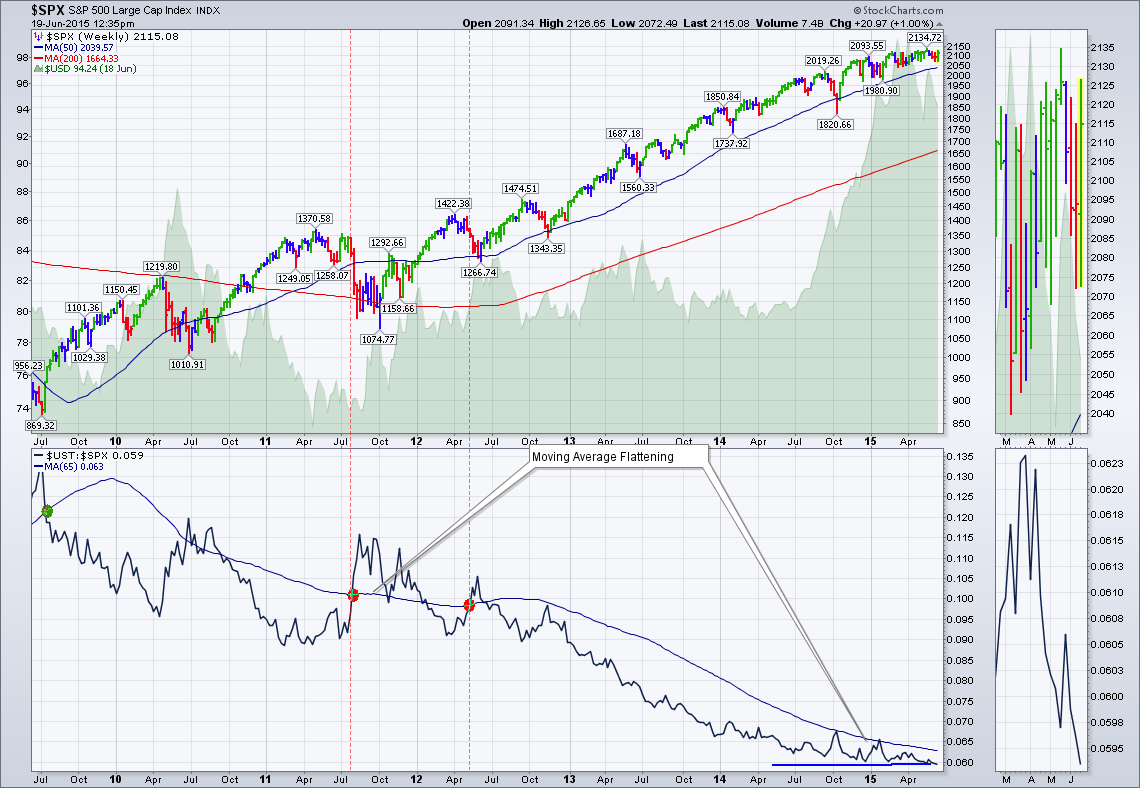

Are Fund flows a reverse indicator? An old debate may be revived soon

- Friday Sara Eisen ?@SaraEisen – Biggest week of bond outflows in 2 years, 8th week of outflows for Treasuries http://reut.rs/1GWJJSI

This was trumpeted by Michael Hartnett of BAC-Merrill Lynch as evidence of a new avatar of the “great rotation” from bonds to stocks. Will this prove a contrary indicator?

- Friday – Cousin_Vinny ?@Couzin_Vinny – $UST $SPX BOND STOCK RATIO – been 3 years since this indicator has crossed. Interesting no? $SPY $SPX $TLT

- Friday – Keith McCullough ?@KeithMcCullough – UST 10yr Yield = 2.27%, down -12bps on the wk and -27bps from last week’s “breakout” highs

The entire Treasury curve rallied this week. And, as evidence of a dovish Fed, the 30-5 year curve steepened by 12 bps and the 5-year yield fell by 16 bps with the 3-2 year yields down by 14 & 10 bps. The sentiment remains awful:

- Friday – J.C. Parets ?@allstarcharts – sentiment has been so obnoxiously bearish bonds (bullish rates) lately…..I’ve never seen anything like it….. $TLT $TNX $ZB_F

4. Equities

Is this week’s performance due to the Fed or due to Greece? The Fed is now a tailwind unless the incoming data stuns on the upside. So the next two weeks might hinge on Greece. If they punt on Greece and avoid the near term turmoil, then stocks should rally. Actually the S&P should break out of its long rut and decisively go to new highs. But if it break out and then fades again, will that be a failed breakout? Or will they then punt until earnings for the real breakout?

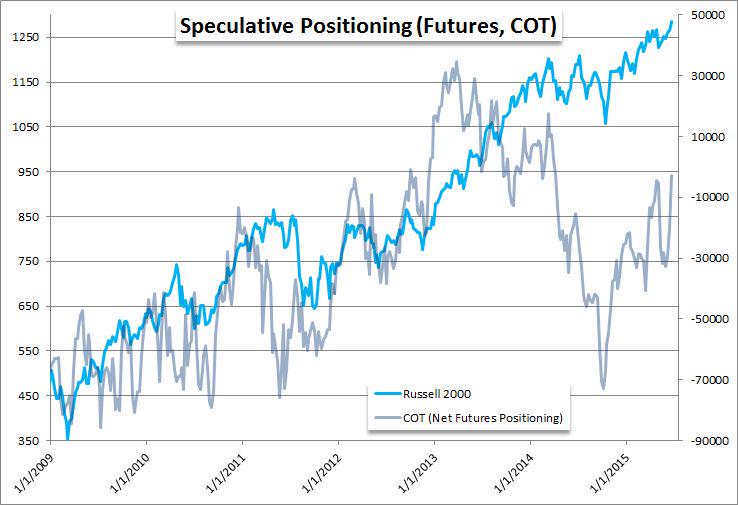

So far, the Russell 2000 seems to have been the safety trade:

- Friday – John Kicklighter ?@JohnKicklighter – Fighting the current is tough. Net long futures spec positioning on the Russell 2000 jumps most since May 2012:

The rally on Thursday was something:

- Thursday – Joe Kunkle ?@OptionsHawk – The amount of stocks breaking key resistance levels today has my head spinning

- Thursday – Urban Carmel ?@ukarlewitz – $SPY: first higher high on the weekly chart since the week of May 18

- Thursday J.C. Parets ?@allstarcharts – a ton of upside alerts going off for me in U.S stock sectors this morning….

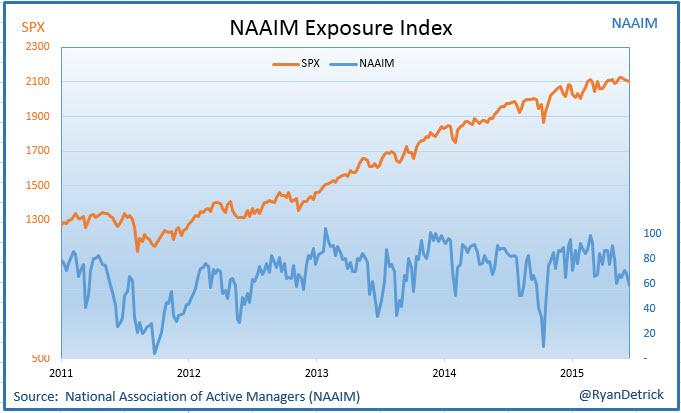

The sentiment seems to be playing along too:

- Thursday – Ryan Detrick, CMT ?@RyanDetrick – NAAIM Exposure down to a new calendar year low. With $COMP and $RUT making new highs, this is so rare and bullish.

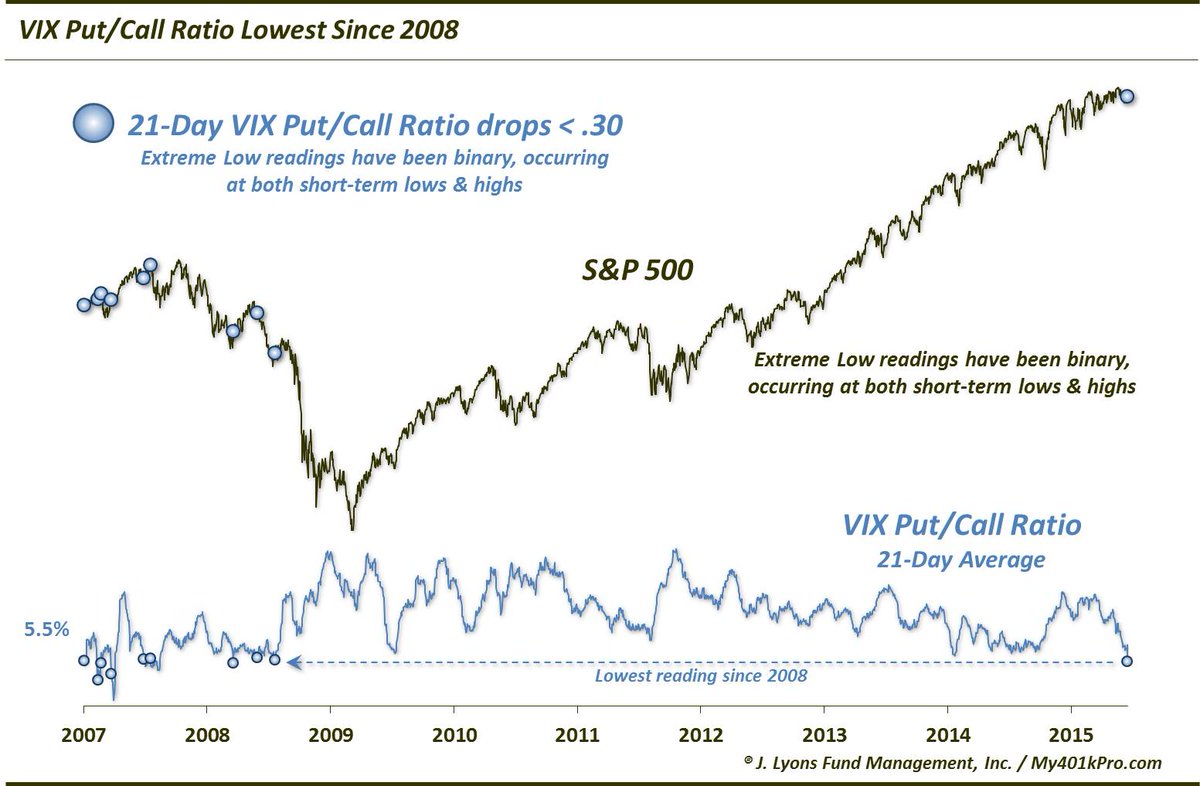

But what about VIX?

- Friday – Dana Lyons ?@JLyonsFundMgmt – ChOTD-6/19/15 $VIX Put/Call Ratio Lowest Since 2008 $SPY

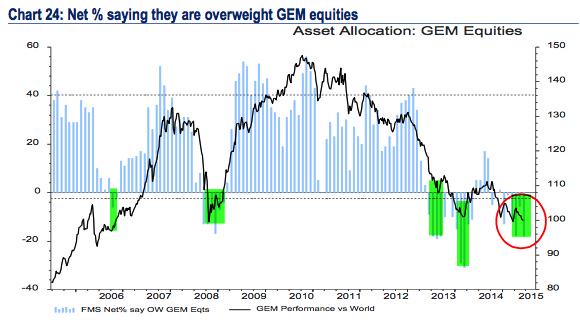

Is the Merrill Lynch survey a contrary indicator?

- Tuesday – Urban Carmel ?@ukarlewitz – BAML: the biggest change was in cutting emerging markets exposure to a 2-yr low $EEM

We had not heard of a Cat/Man formation until we saw this chart:

- Tuesday – Katie Martin ?@katie_martin_fx – Weird cat/man formation, S+P returns. Bullish

And we have no idea what to do with the following except trade at night:

- Tuesday -Eric Scott Hunsader ?@nanexllc – Buy at midnight, sell at 4am – most of the gain, none of the pain (hindsight is everything): $ES_F

5. Gold

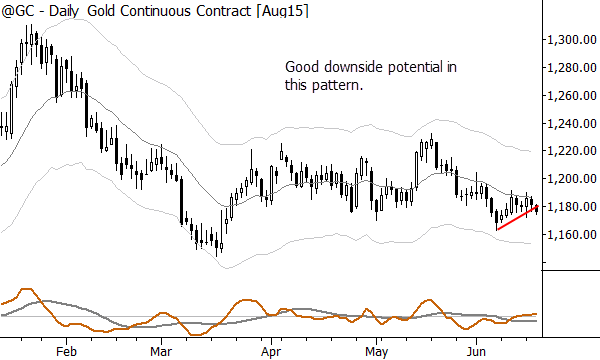

If Gold cannot rally with a dovish Fed, when can it rally? May be with a weaker Dollar and falling interest rates? In a week in which Gold rallied by 1.8% & Miners rallied by 2-3%, we couldn’t find bullish comments on Gold. What we found was:

- Wednesday – Adam Grimes ?@AdamHGrimes – could be downside potential in a breakdown from this bear flag in #gold $gld $study $gc_f

and

- Wednesday – GenX Investor ?@GenXxInvester – $GDXJ has major downside potential compared to $GDX

Is this a contrary signal in itself?

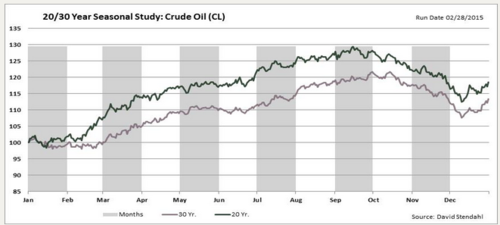

6. Oil

Carter Worth, resident technician on CNBC Options Action, was negative on Energy stocks (XLE) on Friday evening. On the other hand, the following chart makes a seasonal bullish case for oil.

.