Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. L’Audace, L’Audace, Toujour L’Audace!

Two weeks ago, we wrote it’s all about Greece. That’s where we are today. This was never really an economic game. It is all political that is unfortunately being handled by economic we-know-it-all morons in EU. Add a big component of anti-Greek contempt and that brings us to today. The only reason the deal is so close is due to Chancellor Merkel who gets it better than any of her minions. The Greek side is run by politicians who know exactly what is at stake – their own and their party’s political future.

So having taken it as far as he could, Prime Minister Tsipras is now letting it all hang out by calling for a referendum. They may not lose either way. On the other hand, the EU bureaucracy stands to lose a great deal. Remember, the entire EU mechanism was designed to create a supra-authority in Brussels of the EU elites. They genuinely believe that people, masses of people, are clueless and they need to be run by the EU elites for the greater good of Europe.

Regardless of what happens afterwards, a Greek referendum will set a precedent for the rest of Non-German-bloc in Europe. So when Spain, Ireland, Portugal, Italy or even France get into a mess, a referendum may be called by their leaders. That cannot be allowed to happen. The EU elites know they will lose every single referendum on EU & its austerity and that will be the death of the Euro experiment.

That is why the referendum call by Tsipras is an act of war against the EU elites in Brussels. That is why EU is now saying take the offer now & cancel the referendum Or lose the offer by holding the referendum.

This is becoming like 1914, the war no one wanted but one that everyone stumbled into. Will the EU make an example of Greece by letting Greek banks go under & lead to riots in the street? Or will they try to manage the exit? Monday morning will be interesting.

Tsipras & his colleagues have followed the dictum of Germany’s Frederick – Audacity, Audacity, Always Audacity. Will their decision prove smart or suicidal?

2. Binary?

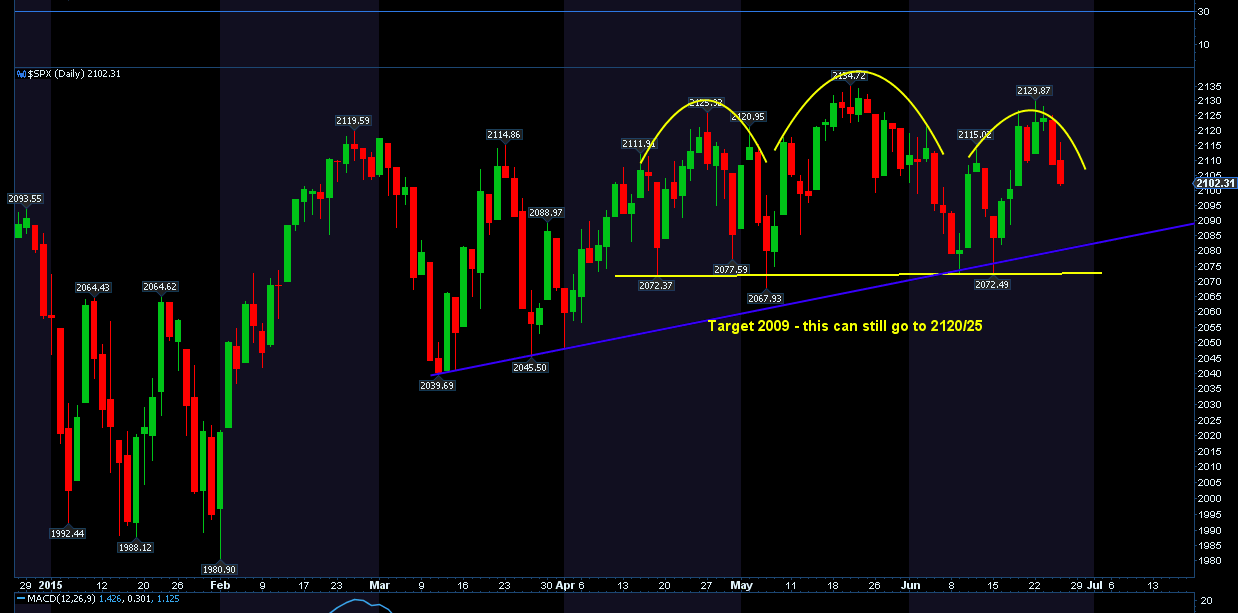

Since it seems all about Greece and the referendum, what to do? Even the stock market seems to be giving two looks to the same formation as shown in Technical Charts by NorthmanTrader:

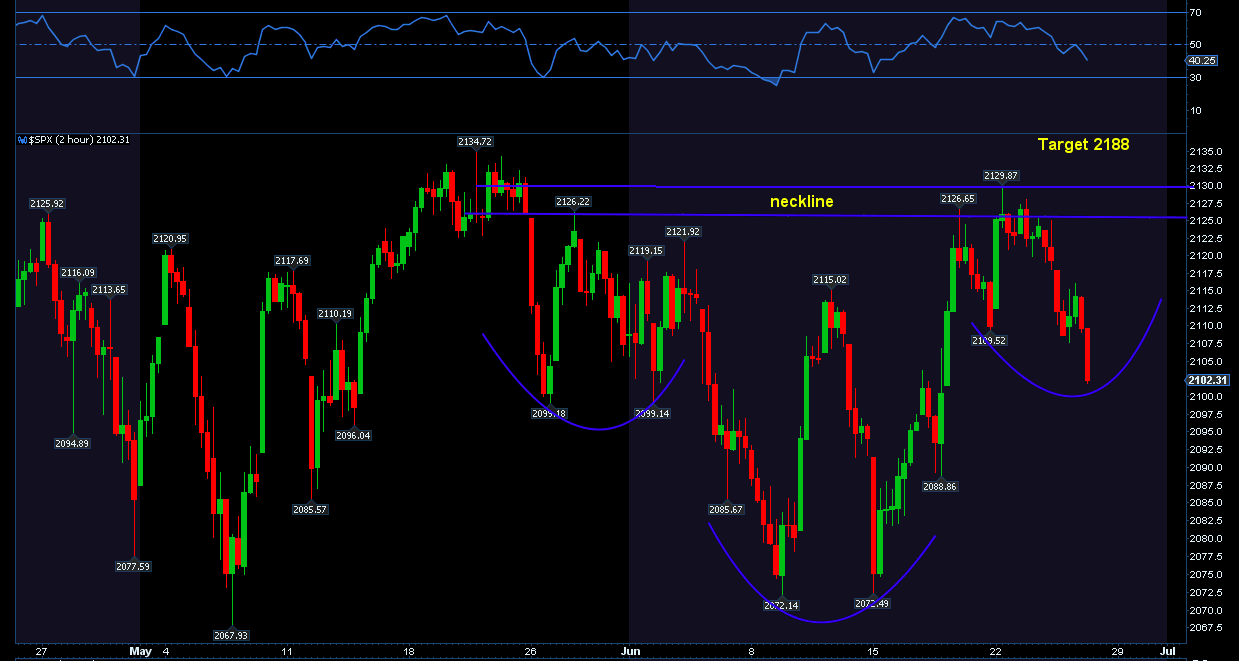

- On the $SPX this pattern also shows up cleanly as Mella_TA’s chart shows:

- YET, and this is critical, an alternate pattern is also emerging, that of a clearly defined inverse:

- “Which one will play out? Unclear as of yet and we’re keeping an open mind, but the outcome regarding Greece may have a large impact on this.”

Andrew Nyquist used a macro-factor approach to express the same feeling – Confusion Reigns. In this article, he provides the same number of reasons to be bullish & bearish. It is an interesting read.

3. Bonds leading from behind?

There was no uncertainty here. Yields shot up this week in a definitive manner. Another clarity was that Bond is following the Bund- The 30-year Treasury yield rose by 18.5 bps this week, a big number unless compared to the 30-year Bund yield which rose by 25 bps off a much smaller level.

- Friday – Holger Zschaepitz ?@Schuldensuehner – Bond rout returns. 10y Bund yields jump by 7bps, Strong correlation w/ US Treasury yields continues.

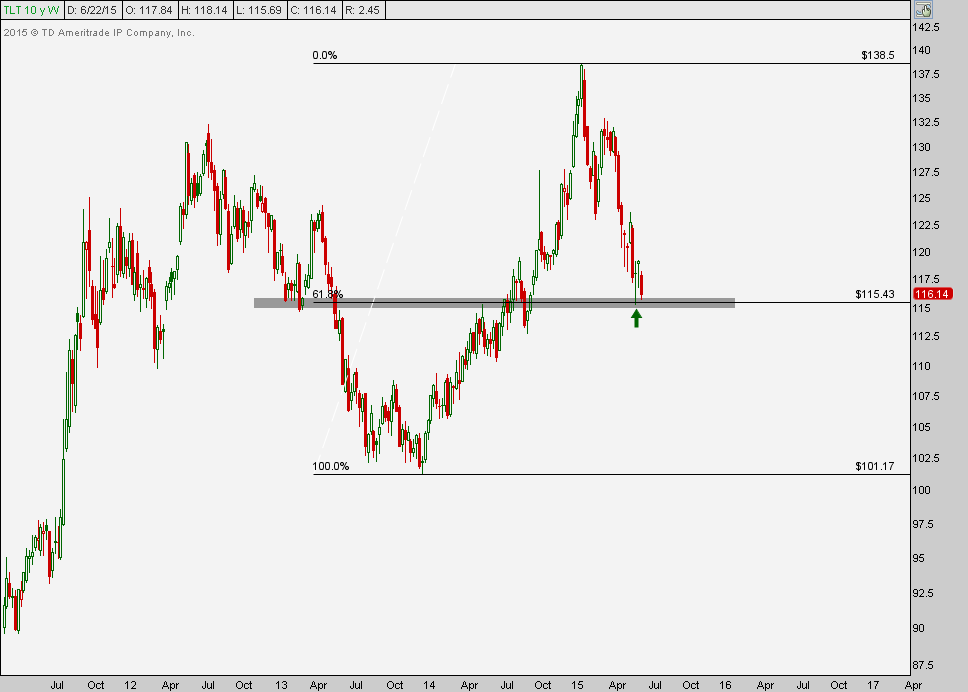

The entire Treasury yield curve rose in yield to close near its 2015 highs except the 30-year yield which did close at a new 2015 high. Some think 2.50% on the 10-year yield is big. Rick Santelli said the big level is 2.62% which we will see soon. If we break that, then you have open skies to 3%. Another view, via TLT, is:

- Tuesday – J.C. Parets ?@allstarcharts – This seems to be the big level in bonds that we want to watch from a more structural perspective $TLT

But could we be near the end of the Bundshock?

- Fri – MacroPru retweeted – Nick ?@NickatFP – “Bond liquidity” story count on Bloomberg

And a brave, lone voice:

- Tues – Sara Eisen ?@SaraEisen – Sri Kumar goes against consensus: “Treasuries are a buy, Fed won’t raise in 2015, and Greece will default and exit the euro“@SriKGlobal

3. Stocks.

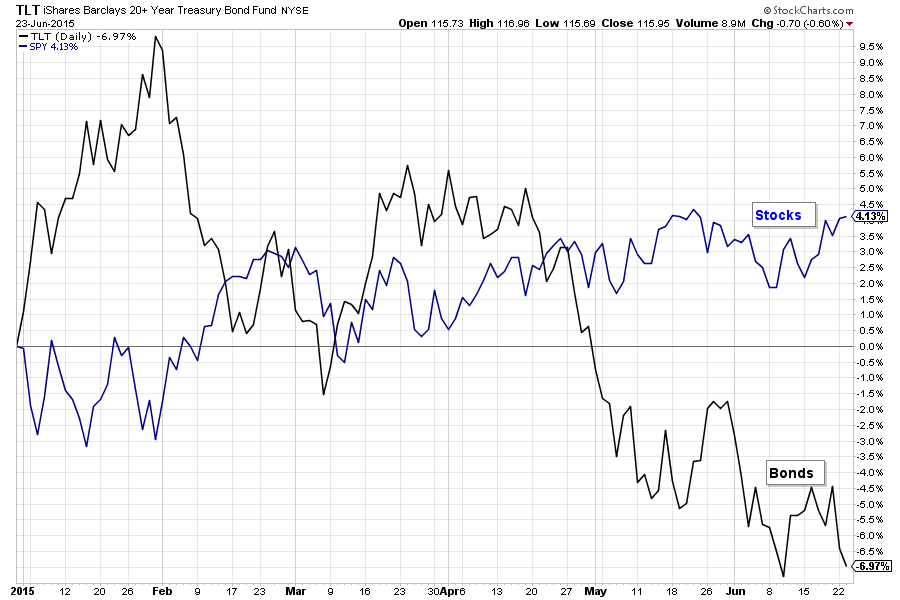

Perhaps, in the “Jill came tumbling after” refrain,

- Wednesday – StockTwits ?@StockTwits – This updated chart is a must-see each day. It shows $SPY (stocks) vs. $TLT (bonds) in 2015 http://stks.co/p2MYz

When nothing seems clear, look at seasonality?

- Thursday – Urban Carmel ?@ukarlewitz – July starts next week, and the first half is typically very bullish. Overall, July is a strongest month of summer

On the other hand,

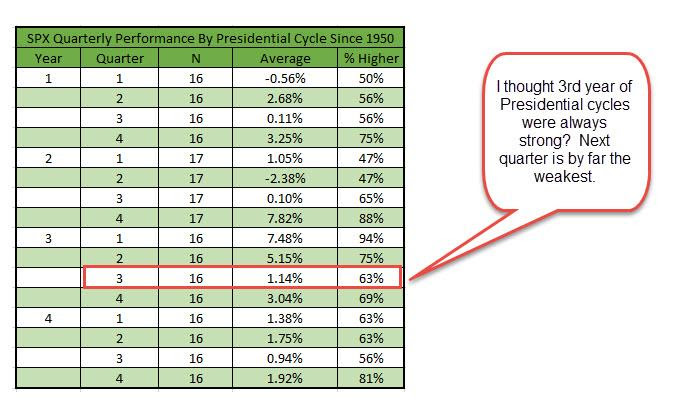

- Wednesday – Ryan Detrick, CMT ?@RyanDetrick – Next quarter is by far the worst quarter during the 3rd yr of the Prez Cycle. Since ’50, up just 1.14% on avg.

4. Warnings from gurus

The last couple of years have been Carl Icahn’s years. People who listened to him or better followed him into Netflix or Apple have been extremely smart and lucky. That makes his dire warnings of this week worrisome:

- t”he market is “extremely overheated—especially high-yield bonds. … I think the public is walking into a trap again as they did in 2007, … I think it’s almost the duty of well-respected investors, like myself I hope, to warn people, to tell people, that really you are making errors.”

- “I do think you are going to have a dramatic pullback, certain things may happen”

Then you have Governor Rajan (pronounced Raajan), a widely respected monetary expert, warn of 1930s like conditions at a conference organized by AQR Asset Management Institute this week:

- “But I do worry that we are slowly slipping into the kind of problems that we had in the thirties in attempts to activate growth. And, I think it’s a problem for the world. … It’s not just a problem for the industrial countries or emerging markets, now it’s a broader game. … The question is are we now moving into the territory in trying to produce growth out of nowhere we are in fact shifting growth from each other, rather than creating growth. … Of course, there is past history of this during the Great Depression when we got into competitive devaluation”

. .

Send your feedback to editor@macroviewpoints.com OR @MacroViewpoints on Twitter