Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. “rate rise here is enormous risk to the Fed“

Who made this succinctly profound point? Art Cashin of course. Does Chair Yellen want the label as the one who pushed the global economy downwards? We don’t think so. As we wrote last week in our FOMC section:

- “If all this, Dollar rally, commodities breakdown, and yield curve flattening, continues next week, then will Chair Yellen send the same hawkish signal on July 29th she did this week? We doubt it. So why did she sound so hawkish this week? The Fed is a political animal and Chair Yellen knew the Congress wanted her to sound hawkish. And she did sound so just right.”

Commodities & EM currencies broke down to multi-year lows this week, the yield curve flattened hard all week and for once the US stock market took a hard drive. The last factor stunned even veteran market watchers especially after the rocket propulsion by Netflix & Google last week:

- Friday – Scott Redler @RedDogT3 – So they gun the market from 2044 to 2130 with no real time to get comfortably long— & squeeze the shorts relentlessly to highs– then this

And what is “this“?

- Friday – Helyn Bolanis @helynbolanis – Yikes! He’s down for the count today.

Recall that the conditions today for Chair Yellen are very similar to the ones that prevailed just before the FOMC meeting on March 18, 2015. The 30-5 year & 30-10 yr spreads were 113 bps & 59 bps on Tuesday March 17 & the levels for GLD, GDX, GDXJ, USO, BNO were $110.20, $17.86, $21.60, $15.77, $19.88 resp.

Guess what happened when Chair Yellen went dovish on Wednesday, March 18? Gold rallied by 2% while Gold Miners and Oil ETFs exploded up by 5%+. The 5-year yield fell by 16.6 bps on that day and the 30-5 & 30-10 yr spreads flattened by 8 & 4 bps resp.

These moves continued at least until Tuesday, April 28, the day before the April 2015 FOMC meeting. From Tuesday 3/18 to Tuesday 4/28 – GLD rallied by 6%, GDX by 15%, GDXJ by 19%, USO by 24% & BNO by 18%. The 30-5 & 30-10 yr spreads flattened by 16 bps & 11 bps to 129 bps & 70 bps resp.

What would happen if Chair Yellen takes out the September rate hike possibility next Wednesday? That would depend on the positioning of the big guys, of course. But we did get a glimpse on Friday afternoon when some one “inadvertently” leaked dovish interest rate projections for 2015 & 2016 intra-day.

The 2-year yield fell hard and

- ForexLive @ForexLive – Gold rips more than $20 from the lows http://news.forexlive.com/!/gold-rips-20-from-the-lows-20150724

2. Pre-FOMC positioning

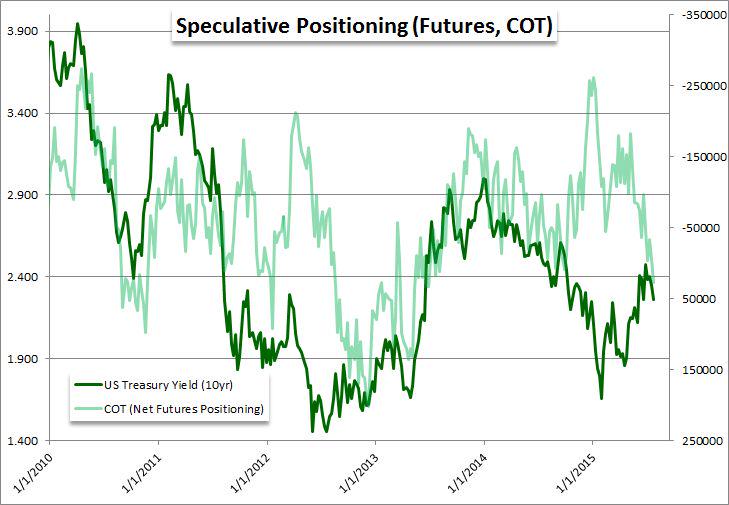

- Friday – John Kicklighter @JohnKicklighter – Speculative futures traders are the most net long Treasuries in two years (July 2013). Fed outlook diverging:

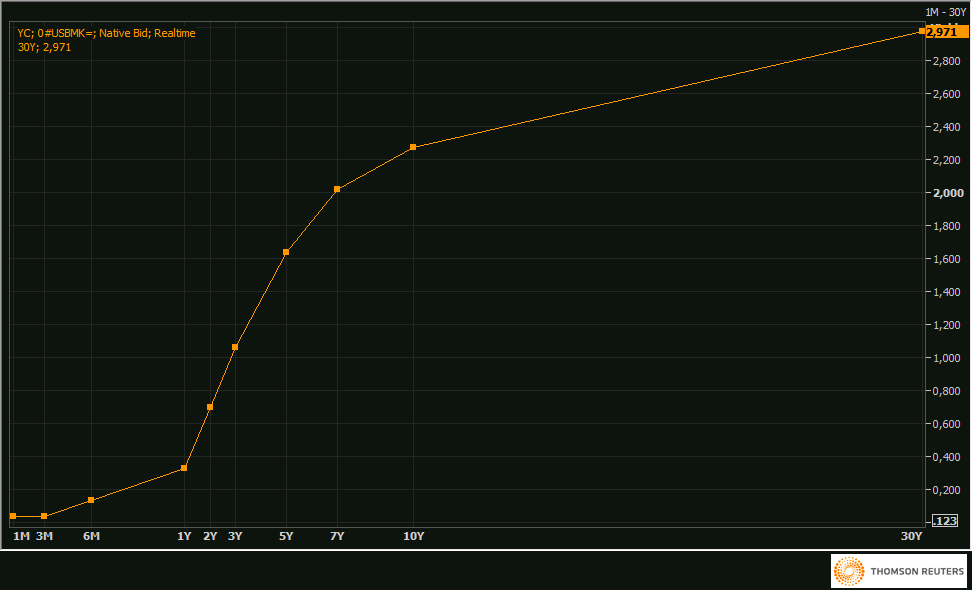

- Thursday – Holger Zschaepitz @Schuldensuehner – US Treasury yield curve flattest in nearly 2 months as 10y yields drop to 2.268% while 1y at 0.32%, 2y near 0.7%.

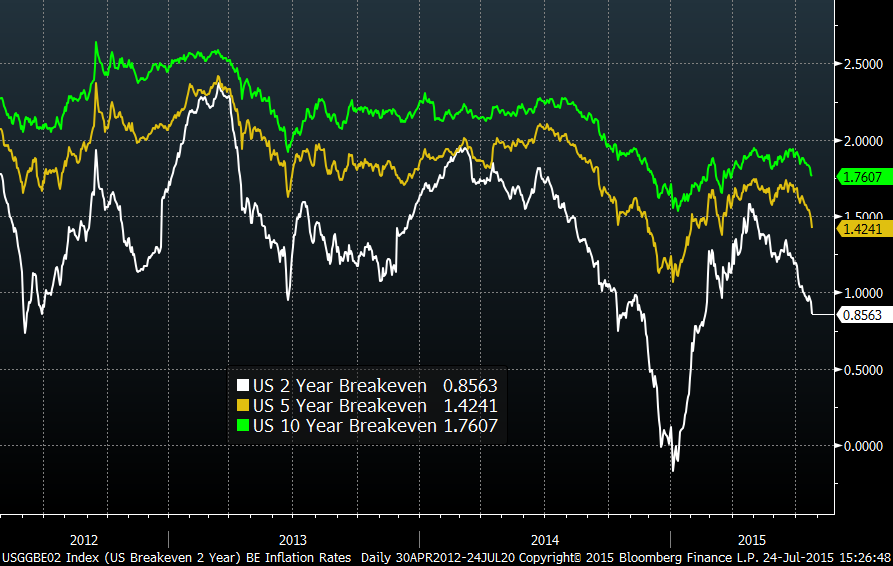

- Friday – Charlie Bilello, CMT @MktOutperform – US Breakeven Inflation rates falling hard this month. $TIP

- Friday – Jason Goepfert @sentimentrader – Large commercial traders are now the least-hedged against a decline in metals in more than a decade.

- Friday – Bloomberg Business @business – Hedge funds hold first ever net-short position in gold http://bloom.bg/1SGmpuM

- Friday – Mark Arbeter @MarkArbeter – This chart looks even worse than it did when I posted it on Monday. $DUST, $GLD. Look out below!

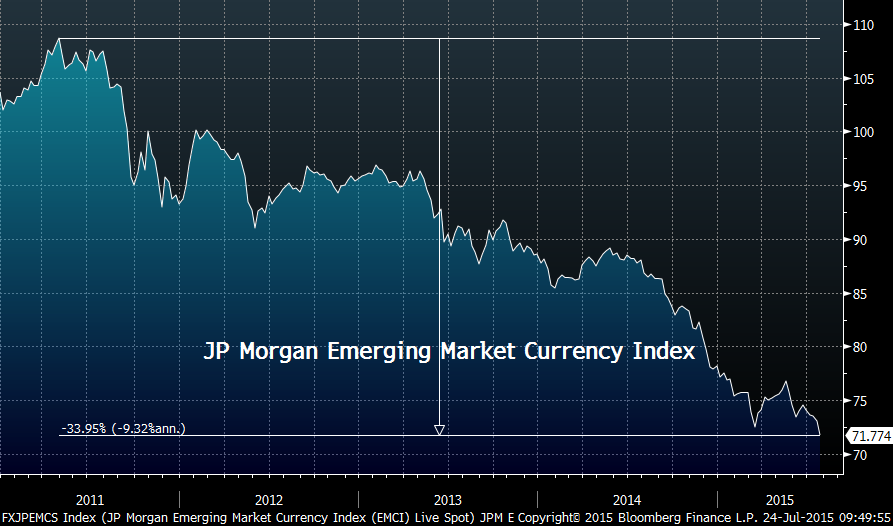

- Friday – Charlie Bilello, CMT @MktOutperform – New multi-year lows again for EM currencies…

- Friday – Jess Delaney @jdelaney_NYC – US companies reducing economic exposure to emerging markets

Even assuming the leak on Friday was really inadvertent, would Chair Yellen allow a hawkish statement next Wednesday, a statement that seals in a September rate hike? We doubt it because, as Art Cashin said, it could pose an enormous risk for the Fed.

3. China – “now no safe places to invest“

When the founder of the largest hedge fund in the world says “now no safe places to invest“, it makes an impact. The text of Dalio’s letter, as reported by Institutional Investor, is even bleaker:

- “While we would ordinarily consider the impact of the stock market bubble bursting to be a rather small net negative because the percentage of the population that is invested in the stock market and the percentage of household savings are both small, it appears that the repurcussions of the stock market’s declines will probably be greater, ” the letter goes on state “Because the forces on growth are coming from debt restructurings, economic restructurings and real estate and stock market bubbles bursting at the same time, we are now seeing mutually reinforcing negative forces on growth“

Not that any one cares but we concur. We have been in Marc Faber’s camp of maximum 4% growth this year. We have been in the camp of Michael Pettis that the transition to consumer-spending economy will necessarily mean a few slow growth years. But that was before the recent asininely stupid attempts by the Government to hold up the Chinese stock market by prohibiting investors from selling their stocks. The only way it can work if the Chinese Govt begins buying stocks in the exchanges and keeps buying until confidence of Chinese investors in the absolute infallibility of the Government returns. But isn’t this possible only if they have unlimited money and unlimited time? Not in any other country which gets Gambler’s Ruin. But China. May be they could do it and that is what they mean by belief.

The Chinese government may feel obligated to buy stocks held by their citizen investors. but they are not obligated at all to keep buying stuff from other emerging markets or from EU. And that may be the greatest risk to growth in Europe.

Once again, can next week’s FOMC statement lean hawkish towards a September rate hike or will it lean dovish? That might be more relevant in the short term than the slowdown in China, that is if Chinese markets maintain at least the illusion of stability.

4. Next Week

The moves this week have been fast & furious. The 30-year Treasury bond rallied hard in both weeks and real assets fell very hard in both weeks. This in itself is scary:

- David Schawel @DavidSchawel – Long end of the UST curve is confusing/scaring a lot of people right now

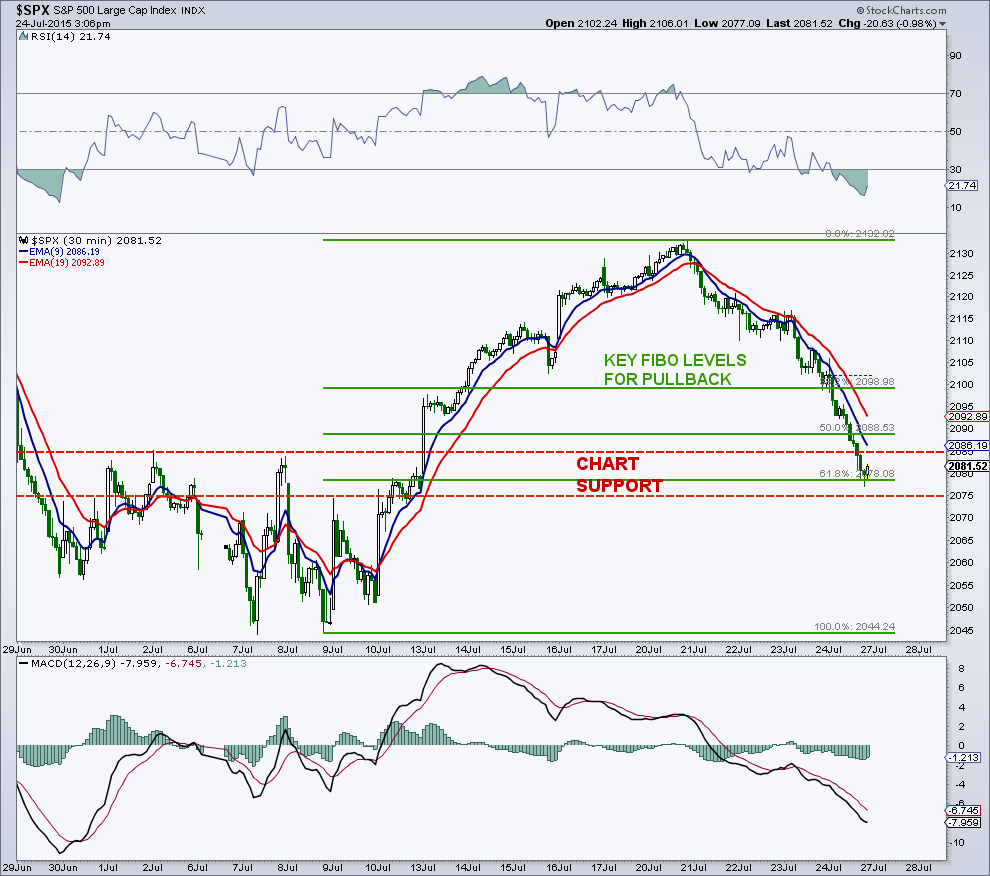

But stocks rallied very hard last week and fell very hard this week giving up all the post-Greece gains. There was no bounce from the first Hemachandra-Fibonacci retracement level, only a straight fall to the second level:

- Thursday afternoon – Dana Lyons @JLyonsFundMgmt – 38.2% Fibonacci Retracement of July S&P 500 rally now $SPY $SPX

- Friday afternoon – Dana Lyons @JLyonsFundMgmt – Commented on StockTwits: ~61.8% Fibonacci Retracement of July S&P 500 rally now $SPY $SPX http://stks.co/c2HEt

What if this level doesn’t hold?

- Friday – Mark Arbeter @MarkArbeter – $SPY, $SPX right down to chart support and 61.8% retracement. Really don’t want to see another round trip to 2,040.

It is not just the S&P:

- Friday – Dana Lyons @JLyonsFundMgmt – S&P400 MidCap $MID & MidCap SPDR $MDY treading their 200-Day SMA…one would think they’d at least temporarily hold their 1st touch of 2015.

On the other hand,

- Friday – Cam Hui, CFA @HumbleStudent – Too far too fast. Covering all shorts & going to cash. Will re-evaluate. Have a nice weekend

- Friday – Cam Hui, CFA @HumbleStudent – Nearing $SPY $SPX bounce zone here

Similarly:

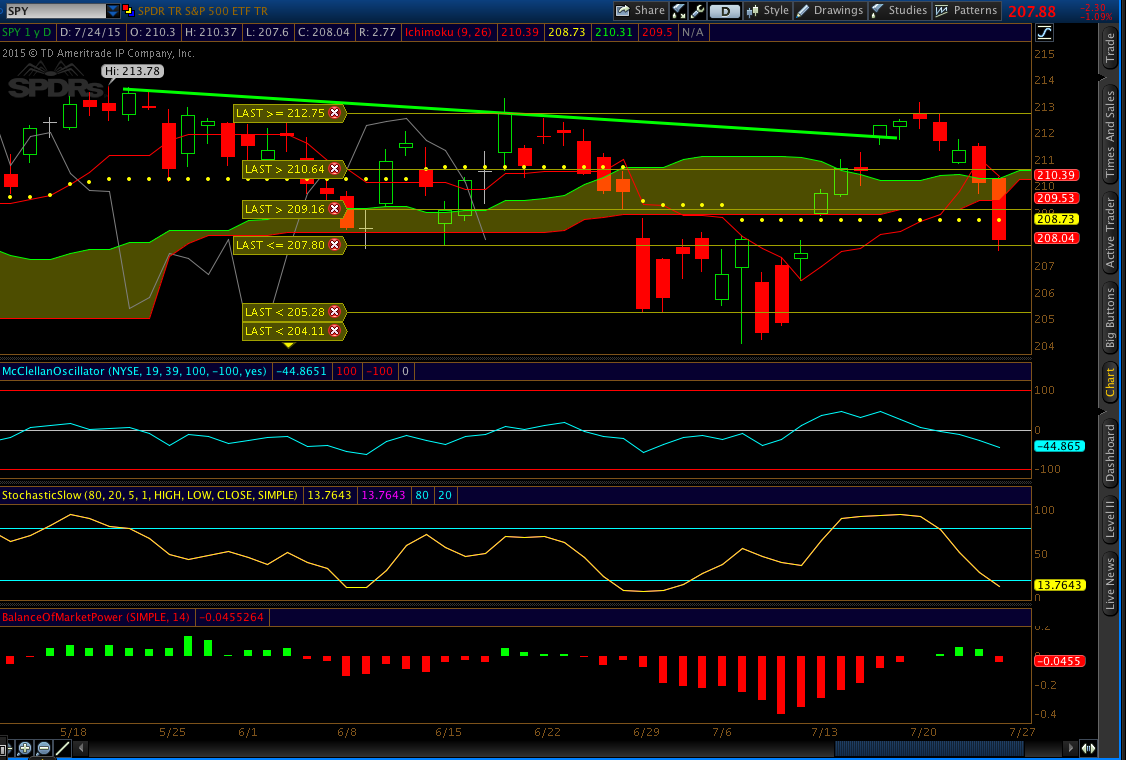

- Cousin_Vinny @Couzin_Vinny – $SPY presently holding the previous pivot at 207.80 (6/15) just to the right of 207.80 LAST Alert – overshot a bit

5. Intermediate Term

Tony Dwyer reaffirmed his bullish out look on CNBC FM 1/2 on Monday with a 2334 target for year end 2015. he has been right so far and may well prove right this time as well.

On the other hand, Tom McClellan suggests the possibility of a major top in August 2015 in his article RASI Shows Bull Market Waning:

- “My leading indication from the eurodollar COT data says that we should expect a major top in August 2015, and so there is not all that much time left for the RASI to get back up above +500. An upturn from this oversold condition should be able to produce a marginally higher price high, but if it cannot produce a RASI reading above +500, then we will know that the end has arrived for the bull market“

This week’s action with serious slowdowns in China & Europe does suggest the possibility of something ominous that is lurking, something that is finally spooking the stock market. The action of the 30-year Treasury Bond is disconcerting even to those who own it. If you share even a few of our worries, take a look at the article titled Totality from NorthmanTrader.com. There are too many charts for us to highlight and so we will merely include some excerpts. Read the article and look at the charts if the excerpts below are of interest to you.

- “What I want to do today is outline the totality of all the different factors that make me extremely cautious here. You know some of these as I have been talking about them, but I want to put them all together on one page to show the total picture. And I’m not talking about a 3%-5% pullback here. I’m talking about something much larger.”

- “On an annual basis we are looking at a market that hasn’t corrected in years, but maintains a steady up trend, but is vastly disconnected from its annual 5EMA … History plainly suggests that runs like this end up with at least a 5EMA tag eventually and that is 300 handles lower no matter what chart scale you look at. Currently that tag sits near the October 2014 lows.”

- “Yet while $SPX and $COMPQ have maintained their structural integrity so far others have not. Mainly the $NYSE: …. And the $WLSH is very close to breaking:”

- “The strongest index, the $NDX just put in place a divergence virtually identical to the one placed at its peak in 2000: It made a new high in price while it made a lower high in the BPCOMPQ:”

{kind=link}

- “In other words: There is a broad based weakening taking place in the overall structure of the market. And this weakening has been building over several months.”

- “Yet in recent days we are seeing an acceleration of this broad based weakness. While we see certain individual stocks racing to make new highs day after day, i.e. in $GOOGL and other high tech fliers we see others getting absolutely hammered, i.e. $IBM.”

- “The immediate consequence of this action is we are seeing an imminent and drastic divergence in the cumulative $NYAD versus stocks:”

- And yet, even though financials and tech are rocking to highs the $DJIA, which includes big time financials, just placed a weekly double top as part of a right shoulder:

- So I see big time risk everywhere, yet I don’t see it being priced in by the market. Which makes me either very contrarian wrong or very contrarian right.

- From a trading perspective this totality of data forces me into patience and discipline mode. My basic view remains to want to sell strength and be very patience about the outcome as I sense that the market’s behavior has changed dramatically versus the past 6 years

- But I’m also cognizant of the fact that we may even make new highs into the 2175-2200 $SPX zone first.

6. Gold

- Friday – Jason Goepfert @sentimentrader – Returns when $GLD gaps down to a yr low, then closes up. Tiny sample size and all the usual caveats. $gold $GC_F

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter