Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

1. Black Swan?

What sort of a week would render irrelevant comments by Fed Vice Chair Stanley Fisher & previous Chairman Alan Greenspan? This week, of course. What these two Fed giants said was forgotten by the specter of a Black Swan. The term “black swan” was used by Richard Suttmeier in his article on theStreet.com about China’s devaluation of the Yuan. Frankly, we liked the photo in his article and couldn’t resist using it:

The term is used for extraordinarily rare events.

- Wed – Charlie Bilello, CMT ?@MktOutperform – 16 sigma event in Chinese Yuan ETF, which basically means it should not happen once in the history of the Universe.

But what does it mean?

- Thu – Charlie Bilello, CMT ?@MktOutperform – Yuan at lowest level since 2011. Don’t believe anyone saying they know the ramifications of this. $CNY

When has that stopped anyone? So many talked & wrote about what they thought it meant. Most discussed it in terms of 1998. James Rickards, the man who was at Long Term Capital during that crisis, pointed out on BTV that the 1998 crisis began over an year before its climax with the Thai Baht and that, if this Chinese event becomes a 1998 type event, it would take awhile to get there.

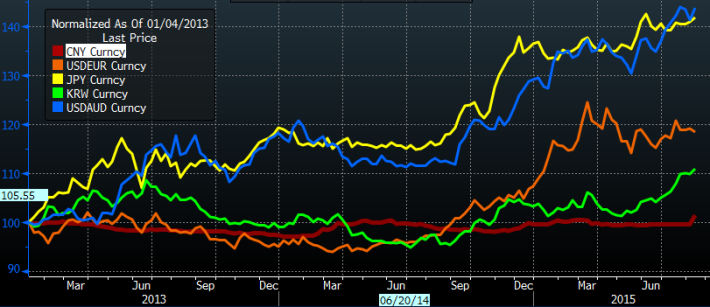

Raoul Pal said on CNBC FM that the first shoe to drop was the devaluation of the Japanese Yen thru QE and now nearly two years later, the second shoe has dropped with the Chinese devaluation of the Yuan. Clearly, the peg with the Dollar had made the Yuan highly uncompetitive vs. Asian Currencies, especially the Yen. This is evident in:

- Forbes ?@Forbes – Understanding why China did what it did with its currency: http://onforb.es/1EsxVU1

In a sense, the stage was set when the IMF postponed the decision about including the Yuan in the SDR to September 2016. That enabled the PBOC to devalue now and hopefully get stability before next year’s decision. Last month’s drop of nearly 10% in exports was stunning and the PBOC had to move. Will China’s exports improve materially with a 5% depreciation in the Yuan? The reality is that an economy that is suffering the simultaneous bust in 3 massive bubbles, Credit, Housing, Stocks, cannot peg its currency to the strongest currency in the world. And they faced a tightening by the Fed in September. Did that trigger this week’s move?

- David Rosenberg – The PBOC cannot cut rates if the U.S. raises them under the prior foreign exchange mechanism, so rather than being a bad thing, yesterday’s moves actually gave the central bank greater leeway to ease policy

But what if the Fed ends up postponing the September Fed hike to December? That would mean the tightening of global liquidity ahead of the Fed hike would recede simultaneously with Chinese devaluation adding liquidity in China. In that case, shouldn’t Chinese stocks rally? That is the conclusion Tom McClellan comes to from a completely different direction in his article Shanghai’s Crash:

- “If it keeps on working into the future (and there is no guarantee of that with these pattern analogs), then the implication is for a rise from here to early September, and then some choppy structure before the start of a really long and ugly decline lasting well into 2016. My other predictive tools are saying that we may not actually see higher highs like the Nasdaq’s year 2000 pattern is hinting at for late September and into October”

We don’t have to wait long to see if such a rally occurs in Shanghai. If it does, it could bring China much needed relief, at least for a short period of time.

2. Fed – Will they or Won’t they?

We keep hearing that the Fed really wants to get off the zero rates policy. We keep hearing that they have to raise rates in September because their credibility is at stake. But what about their credibility if they raise rates and then face a weakening economy, a weakening that makes them eventually lower the rates they raised in September?

Much might depend on the economic data in the next 3-4 weeks and especially on the August Nonfarm Payroll number. Much more might depend on how the S&P 500 behaves in the next few weeks. After all, a strong positive wealth effect was the aim of Fed’s QE. If the US stock market begins to fall and calls into doubt the sustainability of the wealth effect, will this Fed be able to raise rates? This is the same trap in which the Chinese PBOC found itself. We saw how they began dealing with it.

Very little in the US economy suggests a driving need to raise rates next month. Freight volumes are pointing to weaker growth:

- Lance Roberts @LanceRoberts – 3 Things: Freight volumes, Deflation rises, and No Hike In September. #ThingsToThinkAbout http://streettalklive.com/index.php/blog.html?id=2855

- Lawrence McDonald ?@Convertbond – Eurozone disinflation picture looking like the US, except they’re lunching QE, US hiking rates? Via @ZSchneeweiss

3. Treasuries

3. Treasuries

Treasuries were virtually unchanged at the end of this tumultuous week and so was the 30-5 year yield curve. TLT and the 30-year T-Bond remain just below their 200-day moving averages. Will they break through or fade once again?

- Wed – J.C. Parets ?@allstarcharts – this is where 10yr yields bounced in May. Something worth watching. Plus I’ve been getting way too much credit for my long bonds call $TNX

In his discussion of the Chinese devaluation, Marc Faber told CNBC Asia that one asset class he is positive on is US Treasuries.

4. High Yield vs. Stocks

Credit has usually led stocks. That led David Rosenberg to write colorfully on Thursday:

- “If you think the equity market is heading for a spot of trouble here, the high-yield bond market is having a coronary … the average yield is the highest since mid-December and has risen 120 basis points—1.2 percentage points—just since June. Spreads are at 580 basis points, a level hit only twice in the last three years. … In other words, this move in high-yield spreads is on par with what we have seen when we have previously had a 9 percent correction in equities or what would be about the same as the S&P 500 now correcting to 1,910 … Yet the stock market is off just over 2 percent (during the most recent selloff) so either the S&P 500 has more downside from here or spreads are going to have to adjust by tightening back in”

Larry McDonald of SocGen is more concerned about the speed of the move in high yield spreads as he told CNBC on Thursday:

- “When high yield dramatically underperforms in a short period of time, it is a very good warning sign for equities. Since 1996, it has been a correct warning sign about 72% of the time about being a predictive indicator of an equity selloff …. It is the acceleration of the deterioration since April in high yield index, Barclays for example is 55% wider than Treasuries in just like 3 months”

The size of the divergence is bad itself:

- Charlie Bilello, CMT ?@MktOutperform – High Yield credit spreads at multi-year wides: 604 bps. May be largest divergence with equities we’ve ever seen $HYG

The divergence is in merely in the level of stock but in the volatility of stocks as well:

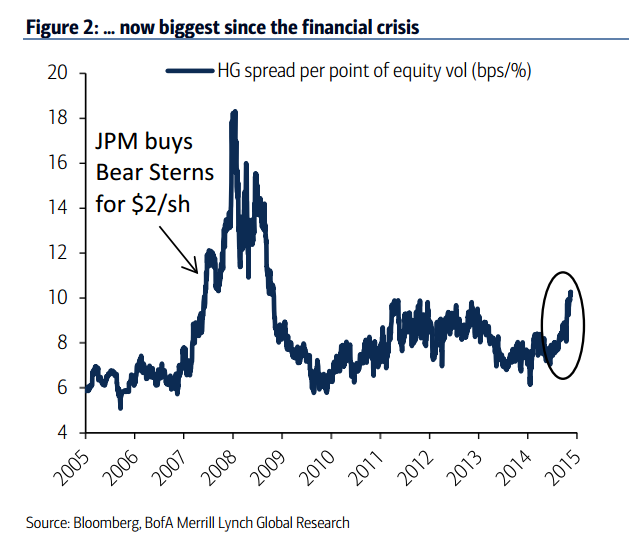

- Tracy Alloway ?@tracyalloway – Credit spread per point of equity volatility rising. BofAML sees shades of early 2008 stock/credit disconnect:

The commentary from BofAML is chilling:

- … 10.26 bps of credit spread per point of equity vol, the level reached on March 6, 2008 – ten days before Bear Stearns was forced to sell itself to JP Morgan for $2/sh. … the upcoming rate hiking cycle appears to concern issuers and investors so much that they have been taking real actions that have repriced our market lower relative to equities to an extent that we have only seen during the financial crisis.”

In other words, this year-long talk about potential tightening by the Fed has resulted in serious damage, far more damage than we would have seen had the Fed raised rates by 25 bps in March instead of talking so much.

Will the above divergence heal itself if the Fed becomes dovish again in the September FOMC meeting or has the damage done – to US credit, Chinese growth, EM currencies – been so severe that Jim Cramer will have scream once more and far more loudly than before that “they don’t know anything“.

Dana Lyons discussed this divergence from the point of view of stocks on Thursday in his article High Yield Bond Rates Indicating Heightened Risk:

- “The bottom line is, this is another red flag for the economy and equity market, even if it hasn’t shown up in the major indicators.”

But this is a risk not a prediction as the graphic in the above article illustrates:

What if the man in the picture recovers his balance and walks proudly to safety? How could that happen in our discussion? The Fed becomes mucho-dovish, interest rates fall, Dollar goes down, oil rallies, the high yield market, dominated by energy companies, rallies & spreads tighten and stocks rally. This could be our multiple single malts speaking but notice the above is a slim athletic man & not a singing fat lady.

5. Stocks

The best tweet award, if we had one, would go this week to:

- Jeff Cooper ?@JeffCooperLive – anyone who thinks they have an edge in this market more than intraday is nuts

With this wisdom in mind, we present the following opinions:

5.1 Bullish

The definition of bullish is the call to arms by Richard Ross on CNBC FM on Wednesday:

- I liked everything that I saw today; exactly as you ordered up if you were bullish; today we break below the 200-day moving average, we are staring into the abyss to a collapse beneath 2040, then we get a heroic textbook reversal that is a classic hammer, you cant draw it any better than this; this set the stage for a late summer surge into the high end of this range, up here around 2130; our contention had been and continues to be that we break out above this range and trade 2180 with upside to 2220; the NDX 100, what’s not to like here? We are talking about the best large cap profitable high quality tech & biotech; that’s exactly where you want to be in this market; a very well-define uptrend channel in contrast to teh sideways channel in the S&P; it is a continuation pattern, it tells you the next move is higher out of this channel; no conversation about the NDX is complete without the big boy here – Apple; at the very least it gets us to the 200-day at 122; I see everything I see here;

A more restrained analysis:

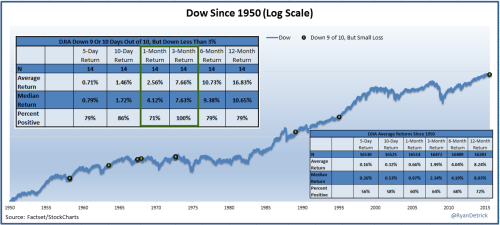

- Ryan Detrick – Thu – Ryan Detrick, CMT ?@RyanDetrick – New Post: $DIA Holding Up Historically Well For Being Down 9 of 10 Days, What’s It Mean? http://stks.co/t2h7L via @YahooFinance

His article states:

- Looking at the 14 other times the Dow was down 9 (or 10) times out of 10 days and it lost less than 3% (like what just happened), the Dow is higher 2.56% a month later and 7.66% the next three months. Both of those results trounce the average returns over the same time frames.

One caveat – 13 of his 14 cases are before 1990; the sole exception being January 1995.

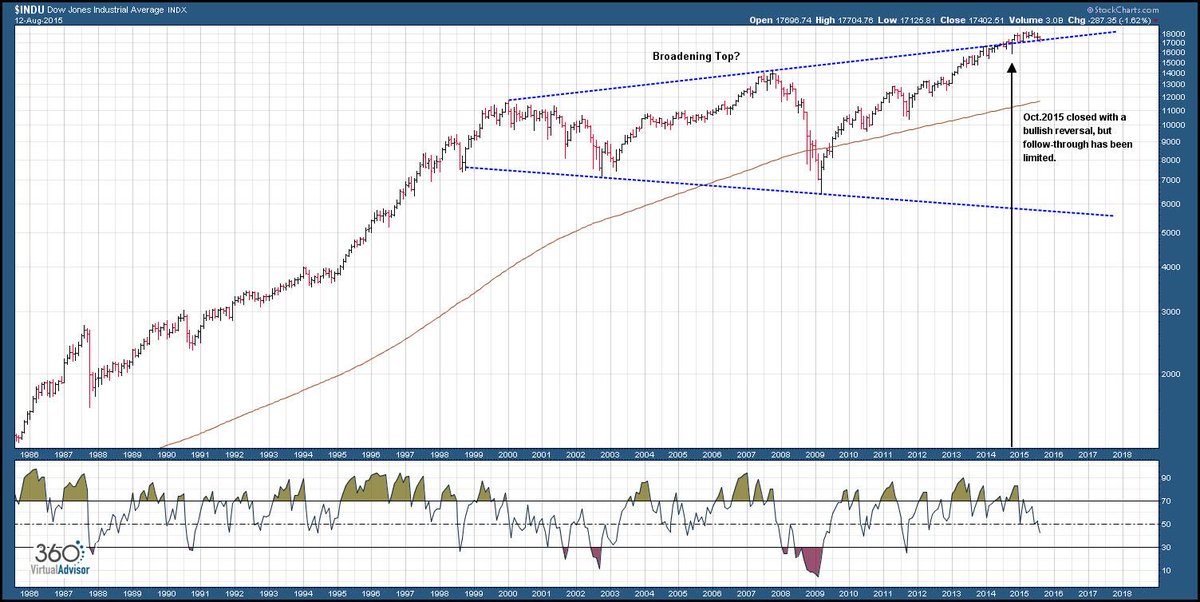

- StockTwits ?@StockTwits – This could be the largest megaphone pattern in history ?? Chart by @hertcapital: http://stks.co/a2OXU $DJIA

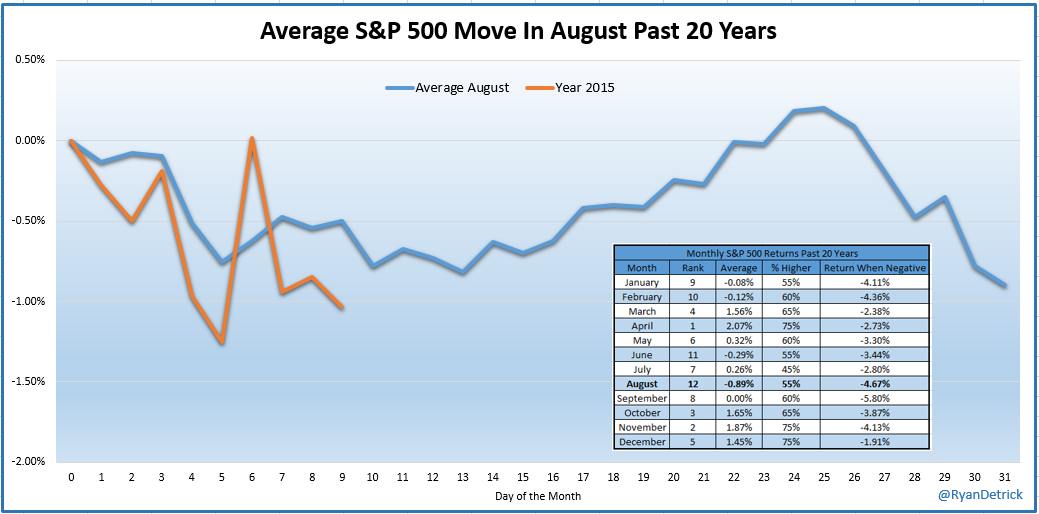

How does this August track so far with others?

- Ryan Detrick, CMT ?@RyanDetrick – $SPX in August is playing out just like the average August the past 20 years so far. $SPY

5.2 Bearish

What happens after a great reversal like the one we saw on Wednesday? We asked and were answered:

- Market Inflections @larryfooter – @MacroViewpoints if memory serves me well, bounce then lower lows except for Oct 2011.

Jeremy Siegel was bearish on the next 5-7 weeks on CNBC on Monday:

- “Dow 20,000 is possible by year-end; next 6-7 weeks would be very rough; Fed hiles in September leads to strong $, weak commodities; thats why earnings in 2015 are flat over 2014; guidance not good for Q3 – end of August & Sept = notoriously weak months historically; very hard to see stock market much higher until Sept ; I do think they hike rates in Sept; coming out of that see a nice rally in Q4″

Can a picture be fractured?

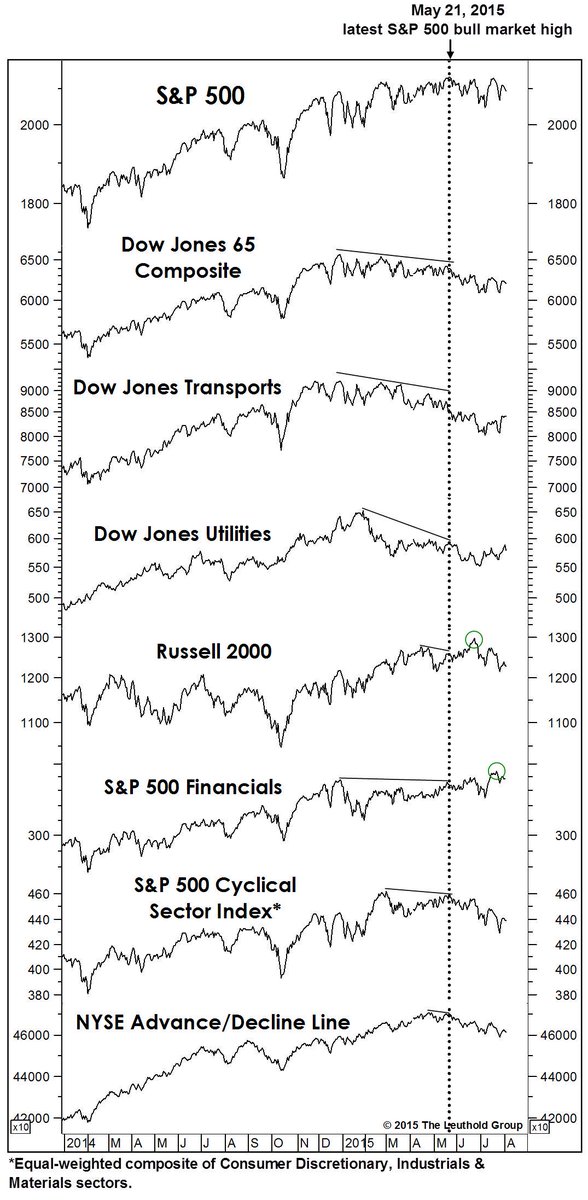

- The Leuthold Group ?@LeutholdGroup – The broad #stock picture is now clearly one of “fracturing.” Next big move should be down

-

Vinny Gambini (@Couzin_Vinny) in his article on The Wilshire 5000 – “Suffice to say the index is forming a rounding top on the daily.”

- Cousin_Vinny ?@Couzin_Vinny – $NYA 50/200 cross “Score Board” 50ma currently (-24.45) below 200ma was +33.55 above a week ago TUES not slowing down

5.3 Emerging Markets

J. C. Parets in his article Are Emerging Markets In Trouble?

- We have broken the uptrend line from the lows in December. Over the past few weeks, prices have now broken support from those December lows. Momentum is hitting oversold conditions which is a characteristic of a downtrend, and therefore confirming everything price is already signaling. Price target-wise, I’m looking at that 33 level which represents the 161.8% Fibonacci extension of that entire December-April rally.

- So how do we execute? Well with that downward sloping 200 day moving average and prices breaking all kinds of support levels, I am definitely in a sell any and all strength mode, especially if we somehow get back up towards 38-39, although I doubt we get up there any time soon. I would only want to be short here tactically if we are below the December lows and more neutral above that level. Target-wise, I would be covering tactical shorts under 33, which is still a long way down from here.

- This is a messy market, both short-term and long-term. The underperformance really stands out, especially with fresh support levels breaking down

6. Gold

The expert commentary we watch began getting bullish two weeks ago and last week they became bullish. How timely was that? Gold & Gold Miners were the only asset class that rallied hard this week with GLD up 2% and GDX, GDXJ up 8.5% & 11% resp.

- Wed – Mark Arbeter ?@MarkArbeter – Everything is $DUST in the wind. Took awhile but this parabolic finally broke down. Beware The Slope! $GLD, $GC_F

And a victory lap:

- Wed – Raj Dhaliwal ?@RSDTrading – Selling all $GDX calls here. Gap fill is completed. Locking in profits

7. Oil

Gold finally rallied for a couple of days. No such luck for Oil. But energy stocks did better than the commodity. Jim Cramer devoted a segment mid-week to technical bullish signals on Exxon, Chevron, Oxidental & EOG.

- Fri – Mike Valletutti, CTA ?@marketmodel – The charts of Energy stocks are positively diverging from Oil price. $HAL $APC $CVX

What about demand though?

- Wed – Mike Valletutti, CTA ?@marketmodel – Oil demand growing at fastest pace in five years, says IEA http://on.wsj.com/1NpJDnq via @WSJ Yes, there is a Demand part of the curve.

On the other hand, Walter Zimmerman of United-ICAP was very bearish on CNBC Futures Now. He pointed out that commodities have a 15-year cycle and the bottom of oil in this cycle will not be reached till the 2nd half of 2016. He expects Oil to trade between $32-$25. Jeff Kilberg of CNBC Futures Now expects Oil to fall to $38.

An interesting way to measure sentiment on Oil:

- Thu – Peter Atwater ?@Peter_Atwater – Am still not seeing anything yet to suggest a capitulation low yet in oil.

And a real honest reaction to the price of Brent:

- Yoda @JediEconomist – Hummmmph, ugh ugh ugh, yesssss. Ouch

8. Our favorite debating duo

In contrast to the usually boring fare on FinTV, the first segment on CNBC Closing Bell often features the two wild & crazy guys below. Invariably , the most entertaining and useful segment of the day.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter