Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. “they are gonna“

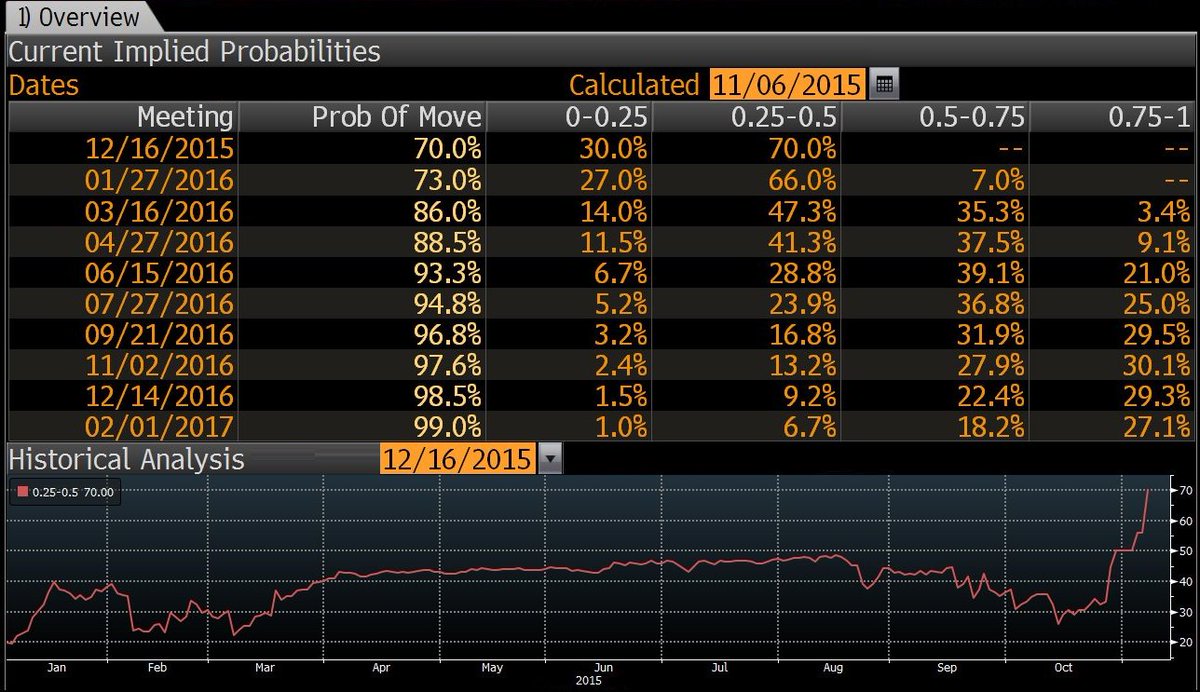

That is the colloquial expression Gary Cohn of Goldman Sachs used earlier this week when asked about the possibility of Fed raising rates in December. Well, the Federal Funds market agreed with him on Friday.

- Antony Filippo @Vconomics – Market now expecting a rate hike (via the Fed Funds Futures)

How could they not? After all, Chair Yellen had virtually promised a rate hike in December in her Congressional testimony. So Friday’s stunning number of 271,000 new jobs removed any doubt any one might have had. It wasn’t just the headline but the details too:

- Ben Casselman @bencasselman – This was the best jobs report of the year — even better than the headline figures suggest. http://53eig.ht/1S2Zvyh

So a 25 bps increase in the Federal Fund rate in December seems a foregone conclusion. But then why didn’t Chair Yellen raise rates on Friday? We wish she had. She could have added all the appropriate sedatives about the path to higher rates being long and shallow. A rate rise on Friday would have eliminated any uncertainty and removed the Damocles sword of a December rate hike from hanging over our heads for the next 5 weeks. Remember, the biggest headache for all markets has been the will-they-won’t-they uncertainty. But why should there be any uncertainty? Think back to October 3, 2015 and the printed NFP number of 142,000. Remember what David Rosenberg tweeted on that day?

- Friday, October 2, 2015 – Gluskin Sheff ?@GluskinSheffInc -Rosenberg: Tack on downward revisions, decline in the workweek, and the “real” payroll number was -265k. You read that right.

- Pantheon Macro @PantheonMacro – “Barring a disaster in November, rates are going to rise in December” @IanShepherdson via @nytimes @NelsonSchwartz http://ow.ly/UkxWB

Why even risk caveats like “Barring a disaster in November“? Why didn’t they act by 11:00 am on Friday? That should have been enough time to gauge the reaction of markets to the NFP number. The reality is that the Fed is terribly scared of their inability to understand markets. That is why they go to absurd lengths to “prepare” the markets. Heck, even they must have realized their “preparation” is more dangerous than any decision could be.

We are in a very uncertain period in the world, especially given the destruction of the Russian charter plane with 224 passengers on board. Not only does it send chills down the spines of anti-terrorism officials in the world, it also raises the specter of a “deadly retaliation” by Putin in the words of a CNN reporter. Why risk any of this or even a violent rally in the Dollar? We do wish Chair Yellen had stepped in Friday late morning and raised rates by 25 bps while categorically taking off the table any more interest rate hikes till 2016 or even until March 2016. Seems so simple to us.

2.It’s all about the Fed.We may hate it and we do. But there is no question that almost every asset class & even rotation within an asset class is turning about to be about the Fed. When the Fed surprised by being dovish in September, commodity stocks, emerging markets, gold & Treasuries rallied. Look the action since the October meeting, totally reverse. This is not entirely due to the Fed but more so about the large positions that are built up and unwound. But the Fed is making this worse by the uncertainty they have fostered. Hopefully, that ended on Friday.

- Joe Deaux @JoeDeaux – HUGE beat on payrolls. Gold falls off a CLIFF

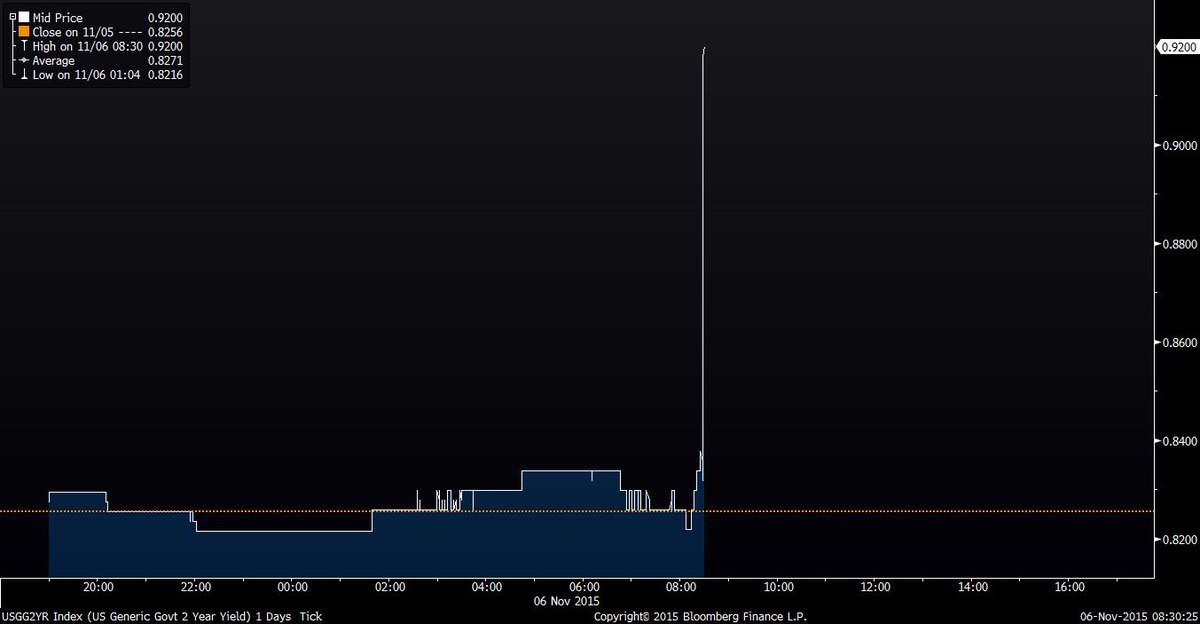

- Tracy Alloway @tracyalloway – And here’s the very large move in the two-year Treasury yield on the back of that payrolls beat

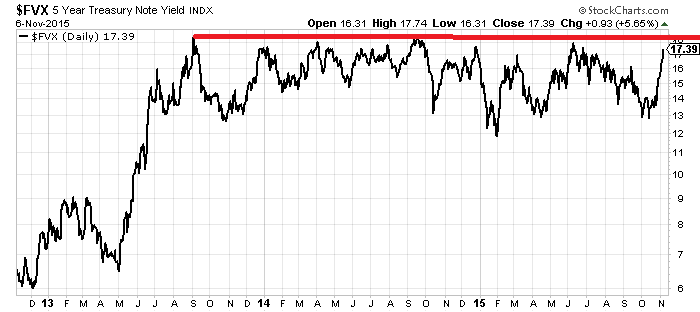

- Helene Meisler @hmeisler – .@mark_dow is this 5 yr yield ever gonna get over 1.80% ???

- Bear Traps Report @BearTrapsReport – Last time 2yr yield this high was 2010, a year that began with rate hike talk and ended with QE2 via @michaellachlan

3. Stocks.By now everyone gets that the Fed looks at only one indicator – the US Stock Market. That’s why we were so convinced that the Fed would be hawkish in the October FOMC meeting. How could they not after the rip roaring rally in October? But the symmetry is indeed interesting. The Fed went dovish in the September FOMC statement and two weeks later the September NFP number proved terribly disappointing on October 2. The Fed reversed and turned hawkish in the October FOMC statement and a week or so later, the October NFP number came in stunningly strong on November 6. Did they get lucky on two successive occasions or are their models so accurate?

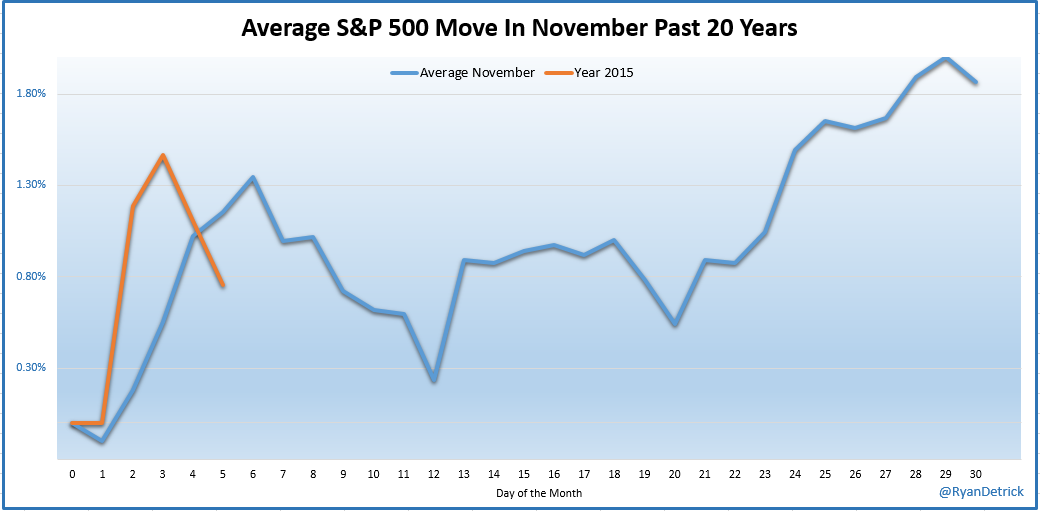

More importantly, will the current rally continue and allow the Fed to raise rates in mid-December or will we see a real correction? Friday’s action was indeed reassuring. After an initial selloff, the stock market regained its composure and the major indices closed positive or nearly unchanged. Was that a reaction to the NFP number or simply an unwillingness to sell in the midst of this Q4 rally? Which performance-fee compensated manager would sell in early November given the track record of November-December?

- Thursday – Ryan Detrick, CMT @RyanDetrick – The avg Nov over the past 20 years tends to start strong (check) and turn weak for the next week or so. $SPY

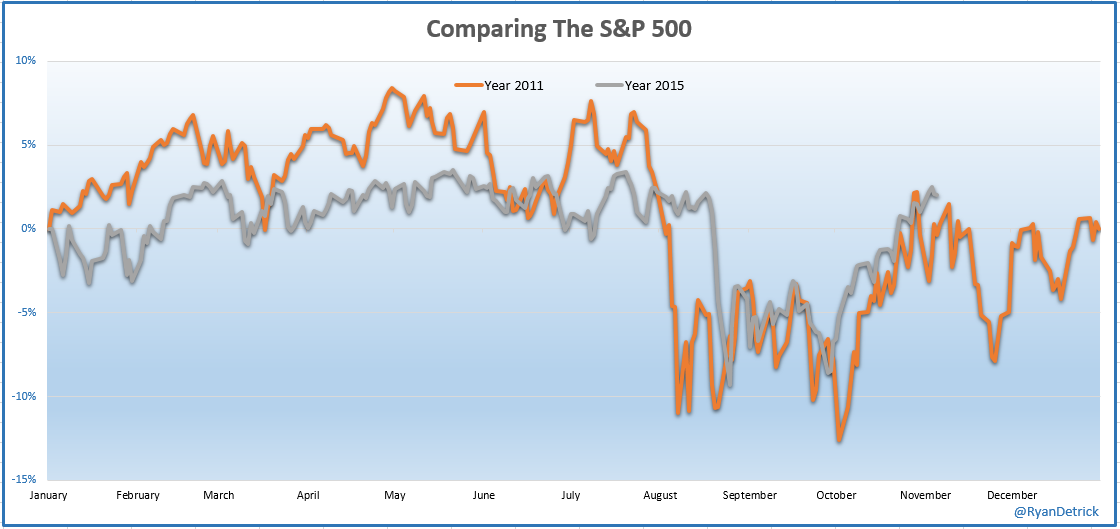

- Ryan Detrick, CMT @RyanDetrick- 2015 continues to track 2011 to a tee. $SPY

- Jason Goepfert @sentimentrader – Good news on top of good news hasn’t been good news for the next few days.

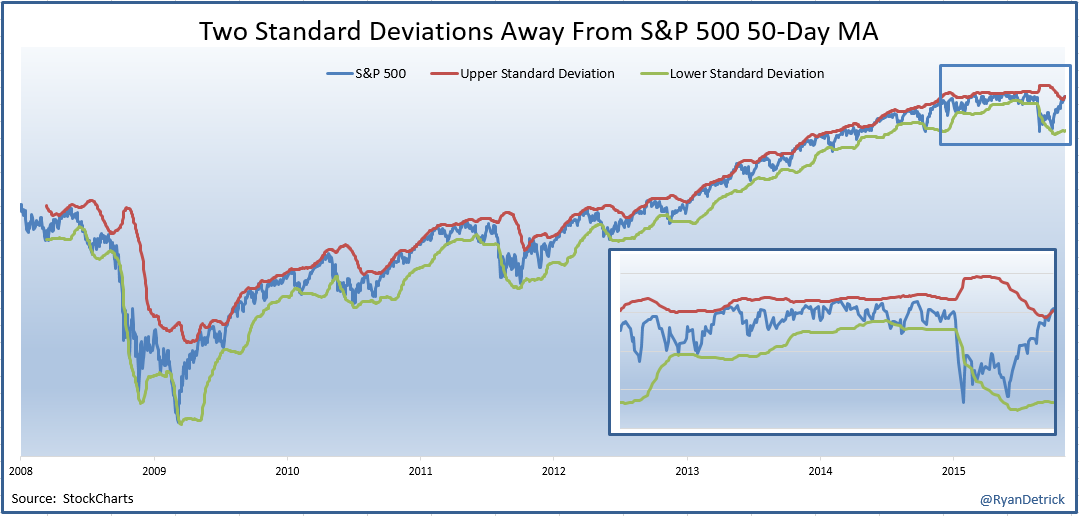

- Thursday – Ryan Detrick, CMT @RyanDetrick – $SPX is 2 standard deviations above 50-day MA for first time since June ’14. $SPY

4. Dollar

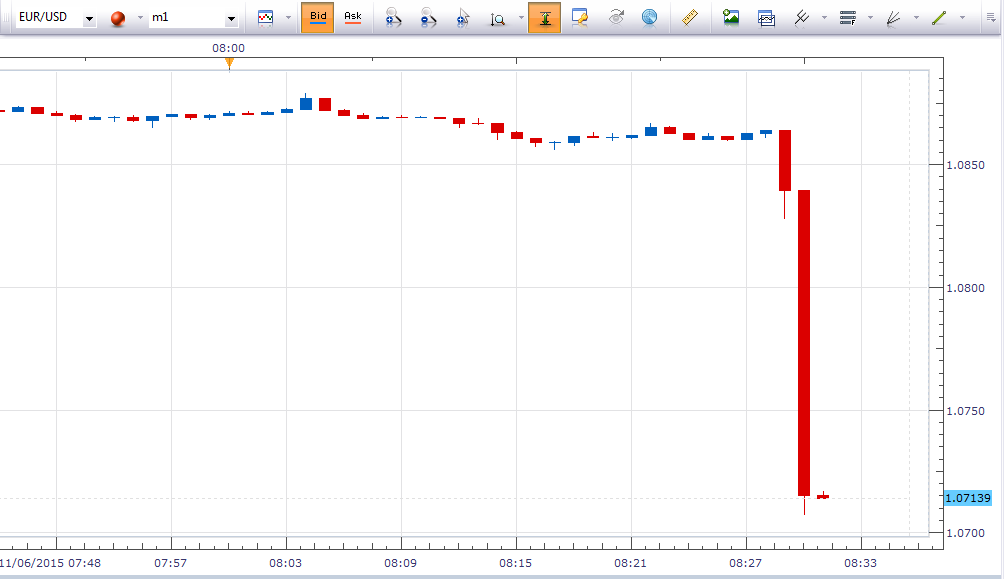

- FXCM @FXCM 51s51 – $EURUSD drops nearly 150 pips after the #NFP release

- Chess @chessNwine – $DXY Monthly. U.S. Dollar Index, aka “Dixie.” Dixie has not looked this threatening since Battle of Chancellorsville