Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Reaction to horrors

How do people react to horrors? They recoil for sure but do they change how they feel or what they do? The reaction to last year’s horror at San Bernadino was swift and clear. But the reaction to the more horrific Orlando is still not clear. There is uniform revulsion & ice cold anger against the killer. But the horror is still being mentally assimilated. People are trying to come to grips with the why of that unimaginable horror. So we have no idea whether the American people will make a major change in how they think or maintain their previous attitudes.

Compared to Orlando, the shooting-murder of Jill Cox, a member of UK parliament was small in scale. But its impact in UK has been huge. It was reportedly a domestic homicide by a man shouting “Britain first”. The shock was so great that both sides of the Brexit campaign decided to suspend their campaigns for two days. But next week’s vote was not cancelled.

The financial markets have concluded that the horrific shooting-murder will force voters to veer towards staying within the Euro to express solidarity with the slain member of parliament.

- Holger Zschaepitz

@Schuldensuehner – Another sign that#Brexit probability has fallen: Hedge Funds have cut their bearish Pound positions by 45%.

Jeffery Gundlach has not changed his position on Brexit. As he reiterated on Friday on CNBC, he believes British people will vote to remain in the Euro mainly because the undecideds usually decide in favor of the status quo.

- Jesse Felder

@jessefelder – Brexit Stress Mounts in Funding Markets as Dollars Become Scarce http://www.bloomberg.com/news/articles/2016-06-16/brexit-stress-mounts-in-funding-markets-as-dollars-become-scarce …

“There is a scarcity, similar to what happened during the Lehman event and European crisis, of dollars,” said Priya Misra, global head of interest-rate strategy at TD Securities (USA) LLC in New York.

We do realize that the referendum is non-binding and the British Parliament may choose to disregard it or delay it with endless debates & negotiations to the point that it becomes meaningless. But we fail to see how Prime Minister Cameron can continue as the head of the Government & his party after suffering a defeat on such a momentous issues.

Regardless of what happens on Thursday, the first three days of next week should be volatile unless we wake up Monday morning with a clear & decisive momentum towards Brexremain.

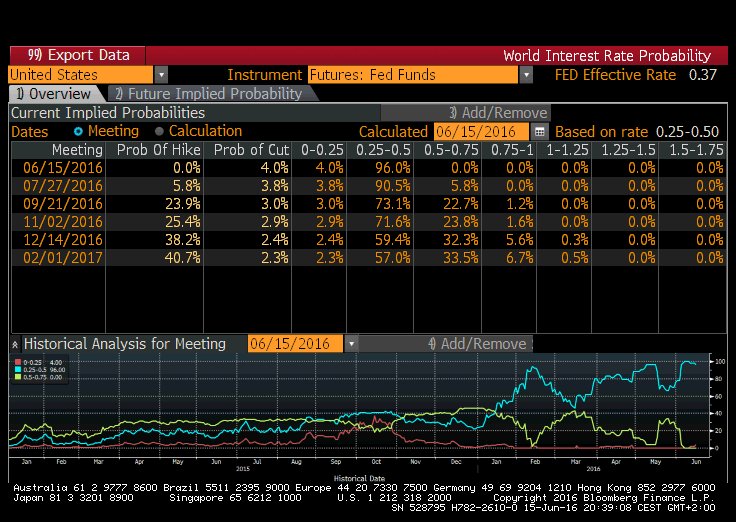

2. Capitulation – “0 before 50 bps” or Waiting for Godot?

- Holger Zschaepitz @Schuldensuehner – June 15 – #Fed‘s Yellen: Mixed data justifies cautious approach. Mkts have repriced rate hike expectations. No hike in 2016.

Some on FinTV have already begun waiting for monetary Godot, meaning a rate hike by this Fed. We have been advocating the “0 before 50 bps” chant meaning the next move by the Fed will be a cut back to zero. This week, we got some illustrious company. Jim Grant said he expects the next Fed move to be a rate cut on CNBC on Thursday. Jeffrey Gundlach did not go so far but said he doesn’t expect the Fed to raise rates this year. Kudos to ECRI for venturing into a rate cut the day before the FOMC meeting.

- Lakshman Achuthan

@businesscycle Main points from Reuters interview, and how next move by#Fed may end up being rate cut. https://goo.gl/6vRx0h

But all this brings up an important question.

3. Did the World change so much in one month?

Remember the afternoon of Wednesday, May 18, 2016? The afternoon the minutes of the prior FOMC were released – minutes that instantly changed the possibility of a rate hike in June-July into a near certainty. So how did the FOMC turn from a near certainty of a rate hike on May 18 to removal of further rate hikes on June 15?

- Decline in Treasury yields – 22 bps from 2.64 to 2.42 in 30-year; 24 bps from 1.85 to 1.61 in 10-year; 27 bps from 1.38 to 1.11 in 5-year; 23 bps from 1.06 to 0.83 in 3-year; 19 bps from 88 bps to 69 bps in 2-year – so a large but nearly parallel fall in the yield curve

- Move in Currencies – Dollar down 1.2%; Euro up 70 bps and Yen up 5.5%.

- Rally in Gold-Silver – GLD up 3.5%, GDX up 7.8%, GDXJ up 11%, SLV up 6%.

- Rally in Stock Indices – Dow up 1.4%, S&P up 1.5%, COMP up 1.9%, RUT up 4.6%. EEM up 4.2%, Goldman down 6% & BAC down 8%

- High Yield – HYG up 31 bps, JNK flat

The first four moves above are not just massive but logically consistent. They tell us two things, in our opinion:

- The markets concluded that the overly strident hawkish tone of the May 18 Fed minutes was wrong and began fading that message from Friday May 20.

- Secondly, most of the fade was already concluded by the time Chair Yellen spoke in her presser on Wednesday, June 15. That is why the semi-climactic rally in Treasuries & Gold-Silver on Thursday, June 16 morning reversed almost from the open. Gold & gold miners reversed viciously on Thursday and long duration Treasuries reversed hard on Friday morning.

Now that the FOMC has gone from stridently hawkish to capitulative dovish in one month, what does Chair Yellen say next week?

4. Economy

- Jesse Felder

@jessefelder – The World Economy Looks a Bit Like It’s the 1930s http://www.bloomberg.com/news/articles/2016-06-16/world-economy-flashes-hint-of-1937-38-redux-says-morgan-

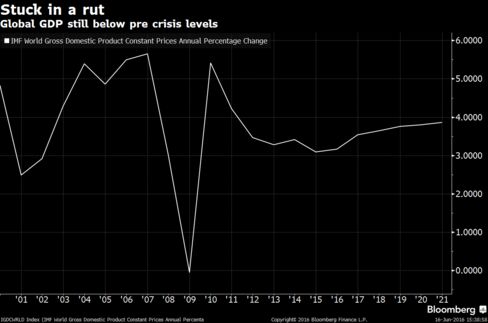

The article quotes Morgan Stanley economist team:

- “We think that the current macroeconomic environment has a number of significant similarities with the 1930s, and the experiences then are particularly relevant for today,” they wrote. “The critical similarity between the 1930s and the 2008 cycle is that the financial shock and the relatively high levels of indebtedness changed the risk attitudes of the private sector and triggered them to repair their balance sheets.”

Will Brexit spell “financial shock” or is something else ahead of us? Something from China perhaps?

- Charlie Bilello, CMT @MktOutperform – Chinese Yuan hit its lowest level in over 5 years vs. the US Dollar this week…

Will it take a financial shock to get to the prediction below?

- Raoul Pal @RaoulGMI – US 10 Year bonds – The world clearest trend. Going to 0.5% yields and lower…

5. The real determinant

Are low interest rates, the lowest in known history, bullish for stocks? Dividend Discount Models (DDMs) preach an absolute yes. But that wasn’t true in 2007-2008. The stock markets collapsed at that time after the rates had declined. The real answer to this question depends, in our opinion, on the direction of the credit cycle. If the credit cycle is trending up or stable, then low interest rates act as an impetus to stocks & DDMs rule.

But, as we found out in 2007-2008, when credit cycle trends down decisively, low rates act as a signal of deep problems. One argument postulates that the inexorable decline in yields all around the world is signalling a steep fall in the credit cycle. Look at the performance of asset classes from May 18 to June 17 in Section 3 above. In that period, TLT rallied by 4.8% and yields fell by 20 bps+ across the yield curve while HYG & JNK severely underperformed. And,

- Holger Zschaepitz

@Schuldensuehner – Jun 16 – This chart shatter the view investors would stop buying at 0%.#Japan bonds headed for best half year in 2 decades.

And what should underperform in a down credit cycle?

- Raoul Pal

@RaoulGMI –$EEM Emerging markets look set to break. Something has changed everywhere in last few days…

Raoul Pal may be right. If Emerging markets don’t rally in an environment of low Treasury rates, low global rates & weaker Dollar, something else is going on.

6. US Stocks

All this negative stuff does suggest a rally if for no other reason but pure contrary spite. And even 2007 featured a big rally into July, right? And there are other reasons both statistical & positioning driven:

- Ryan Detrick, CMT @RyanDetrick – Jun 16 – The last 2 times the S&P 500 dropped 5 straight days were 2/11/16 and 9/28/15. Five days later it was up 4.8% and 5.6%.

And five days later would be after the Brexit results, right? And,

- Urban Carmel @ukarlewitz – Jun 14 – BAML: fund manager cash at 14 yr high, equity allocation at 4 yr low. Bond allocation at 3.5 yr high $spy

So we wouldn’t be surprised to get a rally if Brits vote to remain, especially given that the rate hike scare is behind us. And double especially if the June payroll report shows a bounce from last month’s lousy 38,000 number. It would be important for such a rally, assuming we get one, to decisively break to a new high. Else,

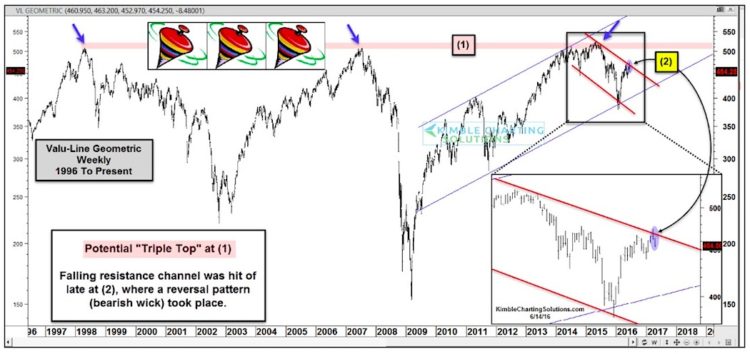

- See It Market

@seeitmarket – New Post – Stock Market Triple Top? Watch This Broad Index! http://www.seeitmarket.com/stock-market-triple-top-perhaps-broad-index-15789/ … by@KimbleCharting$SPX$VALUG

If you do want to play for a Brexremain rally, what should you buy as a trade. and only as a trade, according to Jeffrey Gundlach? European Banks!

- Dana Lyons

@JLyonsFundMgmt – ICYMI>ChOTD-6/16/16 European Bank Stocks On The Ledge$EUFN$DB$CS Post: http://jlfmi.tumblr.com/post/146029103975/european-bank-stocks-on-the-ledge …

Lyons writes:

- “It goes without saying that European banks have been mercilessly taken to the woodshed. However, we would caution one from getting too eager to catch the falling knife just because it is down “a lot”. The reality is that the cycle decline may be as close to the beginning (i.e., July 2015) as it is to the end. So, this is not a recommendation, but if I owned these assets, I would be praying for a 5%-10% bounce that challenged the broken post-February Up trendline – so I could dump them“.

7. Gold & Silver

Negative rates around the world are a basic trigger for owning Gold. And now US real rates are negative as well:

- SoberLook.com

@SoberLook – Chart: US 5yr real rate –

That may be why:

- Raoul Pal

@RaoulGMI –#Gold Inverse Head and Shoulders gone – Long $’s and long gold looks to be the right trade

If Gold is rallying, can Silver be far behind? Not according to Carter Worth of CNBC Options Action who said Buy SLV on Friday.

On the other hand,

- Chris Kimble

@KimbleCharting – Largest bearish reversal patterns in a couple of years, says Joe Friday$SLV$GLDhttp://blog.kimblechartingsolutions.com/2016/06/gold-silver-biggest-reversal-patterns-in-years-says-joe-friday/ …

and

8. Momentum or Reversal?

You know what we are talking about! You know who has the momentum & who has to reverse it! Brexit can wait. Who exits on Sunday night comes first:

photo courtesy of tweet by Jordan Zirm – @clevzrim

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter