Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Relief & Exultation

What happens when investors feel both? Best week of the year for broad stock indices. First the French election threw up the ideal result and then cyclicals reported terrific earnings dispelling fears about the economy. Dow rallied by almost 400 points; S&P and Nasdaq rose 1.5% and NDX jumped 2.6% thanks to spectacular earnings from the champion stocks.

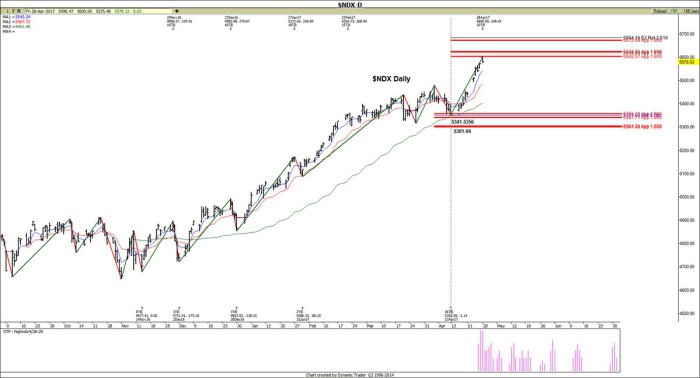

Last week, Carolyn Boroden @fibonacciqueen had placed her potential target for QQQ at $134.32. QQQ blew past that target to close just a penny shy of $136. What does she say now?

- Carolyn Boroden @Fibonacciqueen –

$NDX there is time/price resistance to the recent rally here…great time to ratchet up stops on longs!!!

Despite a 400 point rally, despite the best week of the year for Dow, despite a big rally for EM stocks, the 10-year Treasury yield could not stay above 2.30%. Is this failure to regain the 2.30%-2.60% range good or bad?

- J.C. Parets @allstarcharts you guys notice how 10s have not been able to hold above that 2.3%. That’s missing link to this stock market rally imo. thoughts?

@RaoulGMI

That is the normal view, a view that risk parity funds would embrace. And that view has been demonstrated empirically. But when have declining interest rates proved negative for stocks? When rates decline because of declining high yield credit.

2. Sell High Yield Credit or Stay Long?

This week we heard the first clear-cut Sell High Yield call. Better to hear it directly from Peter Tchir of Brean Capital & Rick Santelli:

- I definitely want to sell high yield, especially index based products.. spreads have compressed a lot, very little upside.. oil which has been a big supporter of high yield is rolling over … I am definitely bearish on stocks; we are almost done with this phase of the rally; we might sell off; credit might lead the way; the 1st hit will be Russell 2000 which is most correlated with high yield & work its way up to Nasdaq & S&P.

Tom McClellan sees it differently in his article High-Yield Bond A-D Line even though he agrees that “junk bonds are the canaries in the stock market’s coal mine“:

- “Just recently, the overall NYSE A-D Line moved to a new all-time high, saying that liquidity is plentiful and it should lift the overall stock market. The same message comes from this High Yield Bond A-D Line, which has also pushed ahead to a new all-time high. The message is that liquidity is so plentiful that even junk bonds can go higher. And history shows that such plentiful liquidity is also beneficial for the overall stock market.”

Both HYG & JNK closed up about 68 bps handily outperforming TLT which was down 1%.

3. US Stocks

First a bold forecast, not in direction but in scale of the next move:

- J.C. Parets @allstarcharts – weekly Bollinger Band width down to 4.47%, the narrowest in history of Russell2000 (back to ‘78) Expecting a violent move coming soon! $IWM

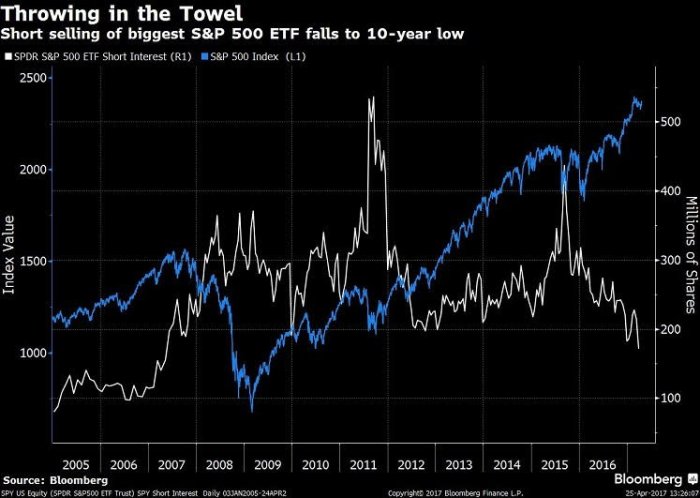

What does positioning look like?

- Babak @TN S&P 500 ETF

$SPY short interest (in nominal shares) falls to lowest level since 2007$SPX source: Maley of Miller Tabak via@TheOneDave

What about seasonality?

- Ryan Detrick, CMT @RyanDetrick – Interesting,

#SPX in May-Oct period has never been lower (4 for 4) when Nov-Apr is up >10% and it is post-election year. Bode well for ’17?

and

- Ryan Detrick, CMT @RyanDetrick – Sell in May based on Prez cycle? Yr 1 has been strongest.

#SPX returns May-Oct since ’50: Yr 1 +2.0% Yr 2 +0.1% Yr 3 +1.7% Yr 4 +1.7%

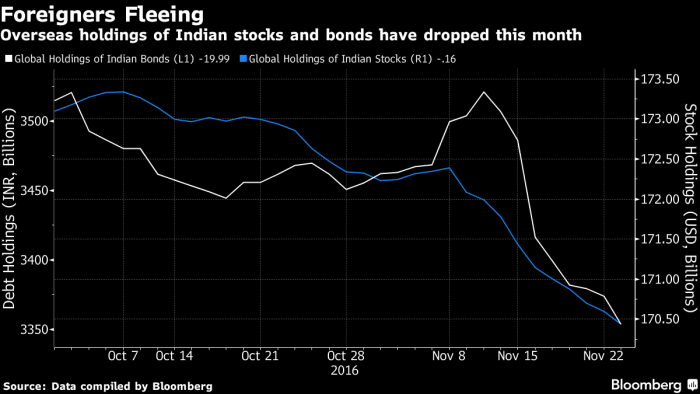

4. Indian Stocks

The Indian stock market has an empirical practice of being a great buy when it is hated and being a sell or an avoid when it is showered with love.

Remember the chart about foreigners fleeing around November 26, 2016 after the Indian stock market had fallen by 6% in two weeks after the monetization announcement. What a buying opportunity that was?

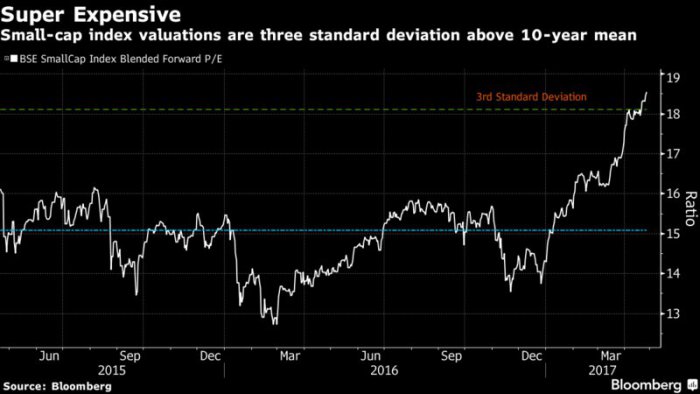

Today, the Indian stock market is loved. We don’t just mean the stock market. The Amazon press release put their success in India right at the top. So is there a chart that demonstrates the love just as the above chart from November 2016 captured the fear?

- Babak @TN – Indian small caps 18.5 fwd P/E +3 std dev above historical trend (asset manager closes fund “to remain rational”) https://www.bloomberg.com/news/articles/2017-04-27/-irrational-indian-mid-cap-market-makes-fund-refuse-new-money …

5. Gold & Silver

Another bad week for Gold, Silver and miners with Gold down 1.3% and GDX, GDXJ down by 5.7% & 6.2%. But,

- Michele Schneider @marketminute – Apr 25 – $GLD–note how holding above 200 DMA while other metals sink-this is worth paying attention to-120 good line in sand

The $120 line did hold all week. If GLD holds, will miners bounce?

- Chris Kimble @KimbleCharting – Largest outflows in history took place at this rising support line test. Panic?

$GDX$GDXJ https://www.kimblechartingsolutions.com/2017/04/gold-miners-largest-outflows-history-bullish-says-joe-friday/ …

What about GDXJ/GDX ratio?

- Chris Kimble @KimbleCharting – Potential bullish wick taking place at dual support this week, after falling hard. $GDX $GDXJ $GLD $SLV

Silver is close to setting a record. Will it bounce if gold does?

- Charlie BilelloVerified account @charliebilello – Silver ETF declines for the 9th straight day, one short of the record set in 2015.

$SLV

6. Oil

- Igor Schatz @Copernicus2013 There is a continued bullish divergence in

#oil curve vs spot, which tells me that we are likely to rally out of here

7. AMD, India & the first “trillion pixel film”

This weekend, the world’s first “trillion pixel film” and a unique VR experience is being launched. The VentureBeat article titled AMD debuts a VR experience around big India movie release describes how Raja Koduri, senior vice president and chief architect of AMD’s Radeon Technologies Group, got involved in this film. The clip below titled Meet the Creators of Baahubali 2 – The Conclusion describes how the VR experience was developed.

[embedyt] http://www.youtube.com/watch?v=HAgSfY8Tn6c[/embedyt]

Our July 2015 review of the first Baahubali film was titled Grand Magnificence, An Eternal Story, A Must Must Watch Breakout Film. The title was actually understated given what the film achieved. The ending left every one wanting to know why & now the Baahubali – The Conclusion is here. It promises to be even better & more magnificent than the first.

Watch how Baahubali climbs the mountain in the first film to reach the Mahish-mati kingdom to meet the woman whose mask had fallen down the waterfall.

[embedyt] http://www.youtube.com/watch?v=F67EVY_sg4E[/embedyt]

If that was the first film, what would the Conclusion with the new AMD chip & the VR experience look like?

Go watch this film this weekend in AMC Times Square (for NYC folks) and all over New Jersey for proud residents of that state. For others, just look up where Baahubali 2 is playing in your city.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter