Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.What Timing? What a signal?

A wonderful week was about to end; the Dow was up 230 points at its high intra-day and about to cross over the 2740-2750 resistance; the fear index looked as if it was going to close at its lows of the week. And then boom!

- Kate’s Dad @KASDad –Funny how “news” happens at convenient moments on charts

$SPX futures$ES_H. Some believe, some don’t.$NDX$IWM

The news hit the tape that indictments were going to be announced by Deputy AG Rosenstein in the afternoon and stock indices fell out of bed. The markets recovered some when it became clear that only Russians were to be indicted and not any American with sensitive political connections. Another recovery took place after Rosenstein’s comments. But the reassurance was only about that specific indictment. So how many would go into a three-day weekend with the specter of more announcements hanging over their heads? No wonder the Dow was up only 19 points at the close.

The news hit the tape that indictments were going to be announced by Deputy AG Rosenstein in the afternoon and stock indices fell out of bed. The markets recovered some when it became clear that only Russians were to be indicted and not any American with sensitive political connections. Another recovery took place after Rosenstein’s comments. But the reassurance was only about that specific indictment. So how many would go into a three-day weekend with the specter of more announcements hanging over their heads? No wonder the Dow was up only 19 points at the close.

But that insertion of concern on Friday afternoon cannot take away the superb signal given last week by Fidelity Investments. As we wrote last week:

- “We have to wonder whether Fidelity’s action on Friday to halt “buy orders of three leveraged ETFs “to protect customers from outsized risk during the current market environment,” will end up being described as closing the barn door after the horse has bolted. … We also wonder whether this ban by Fidelity on short VIX instruments will NOW become a signal to do precisely that, meaning short the VIX.”

How great was that signal to buy the newly prohibited inverse-VIX instruments? The SVXY was up 17% on the week and the $VIX fell by 33% on the week. The collapse in near-term VIX futures has been spectacular – from 63.88 on February 2 to 29.06 on February 9 to 17.775 this Friday. Besides, the slope of the VIX Futures curve is now almost flat from 17.775 near term to 17.65 in October.

Looking back is always great but what about next week? Is there more room left for $VIX to fall next week?

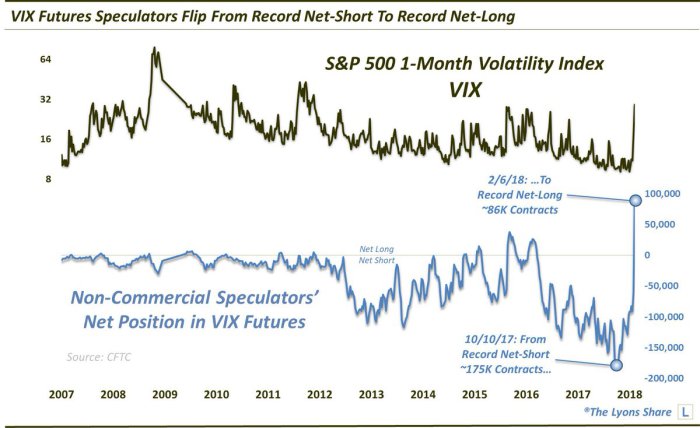

- Dana Lyons @JLyonsFundMgmt ICYMI>ChOTD-2/13/18 After Storm, Volatility Speculators Pull A 180

$VIX$XIV Post: https://lyonssharepro.com/2018/02/after-storm-volatility-speculators-pull-a-180-2/ …

- “With the notoriously “dumb money” speculators (at least at extremes) at their largest net-long position ever, we are left to wonder if they have now gone too far in the other direction. Are they too prepared for continued elevated volatility and is vol liable to settle back down again? “

- “To go from the largest net-short position of all-time to the largest net-long in such a short time gives you an idea of the suddenness of the potential moves here as well as the fragility of this market.”

It is not clear how many of these “record” long positions have been liquidated in the past couple of day. But the mere definition of “record” indicates a further potential for liquidation and hence for $VIX to fall.

Our contention has been that the movement in $VIX is more connected with the movement in SPX than any other indicator. That should continue, we think, until the froth in $VIX positioning is unwound. As Lawrence McMillan of Option Strategist points out in his Friday’s summary:

- “$VIX has given two recent “spike peak” buy signals, and the term structure signals are bullish, too. Despite these buy signals, it should be noted that $VIX is still in an uptrend at least for now. When volatility is in an uptrend, that is not good for stocks.”

Perhaps, an unwinding of the record long positioning described by Dana Lyons will end the volatility uptrend, barring another “news” of course.

What about the other “cause” of the steep fall in stocks since February 2?

2. Interest Rates – the “CA” word?

Remember the 2.9% wage growth rate in the Non-Farm payroll number that scared investors on Friday, February 2? By Tuesday, February 13, a school of thought argued that the reality was not as strong as that number reflected. The hot CPI shook everyone out of their comfort zone on Wednesday, February 14. Not only did rates shoot higher, but look how the hot CPI burnt S&P futures?

- Riva GoldVerified account @GoldRiva – The S&P futures, they don’t like this:

The short end of the Treasury curve exploded & closed up on the day – 5-yr yield up 9 bps; 2-yr yield up 7 bps. In contrast, the 30-year yield only closed up 4.5 bps on the week.

The short end of the Treasury curve exploded & closed up on the day – 5-yr yield up 9 bps; 2-yr yield up 7 bps. In contrast, the 30-year yield only closed up 4.5 bps on the week.

But the real surprise of Wednesday was the V-bottom rally in US stock indices. The Dow closed up 253 points; S&P closed up 36 handles and the real hero of the day was Nasdaq 100 which closed up 121 handles or 1.85%. So a rally fueled by falling VIX was not going to be hampered by Treasury rates going up.

But as the VIX decline fuel runs out, can a fall in Treasury rates serve as new fuel for US Stocks? Perhaps, but who expects Treasury yields to fall in the near term? Actually a few do:

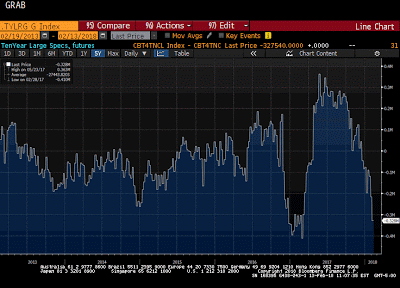

- Marc Chandler @marcmakingsense – Tue Feb 13 – Large specs had record short 10-year note futures position as of Feb 6. The net position is nearly as short as it was a year ago. Vulnerable? http://www.marctomarket.com/20

18/02/great-graphic-bears-very -short-us-10.html …

- “This chart shows the net position, which is a combination of gross longs and gross shorts. The chart shows that the net speculative short position is approaching the record high seen in Q1 17. ”

- “Yet, if anything, the net position conceals an extreme gross position. Specifically, as of last Tuesday, 6 February, the large speculators had a record gross short 10-year Treasury futures position. It stood at 939k contracts. The previous record from a year ago was 882k. “

The 5-year yield has also reached an interesting level:

- Joachim Dressler @TheVolawatcher – Tue Feb 13 –back to positive real returns in UST 5y over 5y5y fwd =financial repression fading =return of the ‘risk free’ rate approaches longterm chart 2002-2018 by

@lisaabramowicz1 thank you !

But was any one ready to utter the Capitulation word, we wondered. Well, some one did on Thursday and on Friday. Larry Mcdonald ( @Convertbond ), the man with a proven Capitulation model, stepped forward & took a pause from his public Bond Bear message to call for a sustainable rally in Treasuries. This rally could last for a month or so, he said. But that is merely a pause before the real rate rise quake hits, McDonald warned.

But was any one ready to utter the Capitulation word, we wondered. Well, some one did on Thursday and on Friday. Larry Mcdonald ( @Convertbond ), the man with a proven Capitulation model, stepped forward & took a pause from his public Bond Bear message to call for a sustainable rally in Treasuries. This rally could last for a month or so, he said. But that is merely a pause before the real rate rise quake hits, McDonald warned.

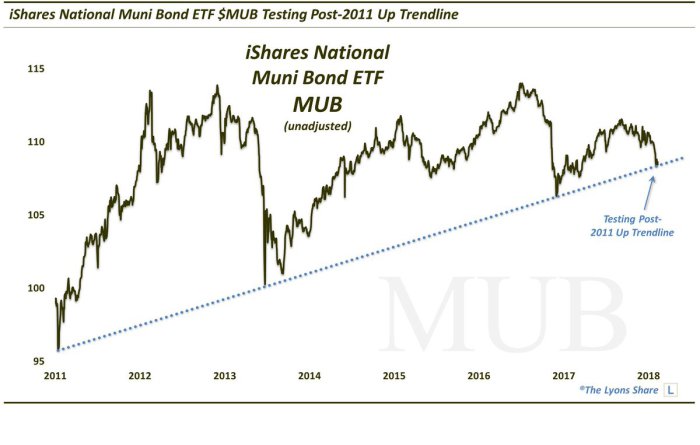

Not only are Treasuries in an interesting spot, so are Municipals:

- Dana Lyons @JLyonsFundMgmt iShares National Muni Bond ETF

$MUB (unadjusted) Testing Post-2011 Up Trendline#TrendlineWednesday

3. Stocks

If $VIX continues to decline and Treasury rates also decline, then wouldn’t that be positive for US Stocks? On the other hand, look where the S&P is at the end of this week:

On Nonfarm payroll report Friday, February 2, the S&P fell through its 20-day moving average. Now after a glorious 6 day rally, the S&P sits just below its 20-day. Even simpletons like us know it has to break above the 20-day line and above the 2800 line from where it dropped. Does it have the fuel to do that? The 2750 level could prove to be a big one and then you have the 2800 level from which the S&P fell vertically. There could be a good deal of congestion at that level.

On Nonfarm payroll report Friday, February 2, the S&P fell through its 20-day moving average. Now after a glorious 6 day rally, the S&P sits just below its 20-day. Even simpletons like us know it has to break above the 20-day line and above the 2800 line from where it dropped. Does it have the fuel to do that? The 2750 level could prove to be a big one and then you have the 2800 level from which the S&P fell vertically. There could be a good deal of congestion at that level.

There has already been one push back at 2750:

- Jeff York, PPT @Pivotal_Pivots – The

$ES_F overnight hit my target for this week at the Wr1 Pivot. When price kept boucing off the WP, was the clue for Wr1@PivotalPivots

Also the S&P has retraced about 61.8% of the decline from the peak. So given the magic of Hemachandra-Fibonacci numbers, this would be a natural level for the S&P to back off.

Also the S&P has retraced about 61.8% of the decline from the peak. So given the magic of Hemachandra-Fibonacci numbers, this would be a natural level for the S&P to back off.

On the other hand, what if people come to the conclusion over this weekend that the Mueller investigation is not going to touch either President Trump or his senior team? That plus a fall in Treasury rates might give a two-handed push to lift the S&P above the resistance.

By the way, Larry McDonald also made a bullish call on Utilities as companion to his bullish call on Treasuries.

What about FANGs? There too, we see a difference in opinion among technicians:

On the other hand,

On the other hand,

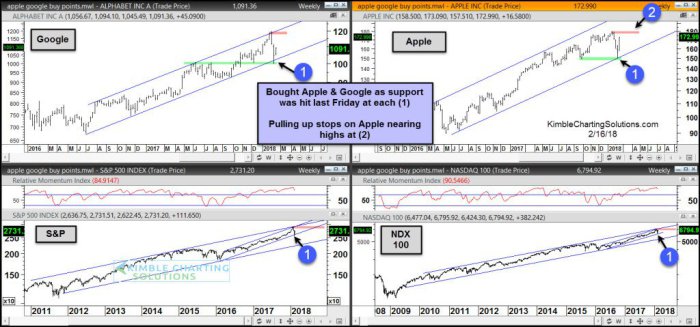

- Chris Kimble @KimbleCharting – Apple & Google Update- Taking some gains here https://kimblechartingsolutions.com/2018/02/apple-google-update-taking-gains/ …

4. Dollar, Commodities

The biggest unspoken & un-understood story in markets is the behavior of the US Dollar. Yes, the Dollar did bounce hard on Friday. But it was down 1.4% on the week. It is hard to speak about commodities without discussing the Dollar. So all we do here is simply share some charts & opinions from experts:

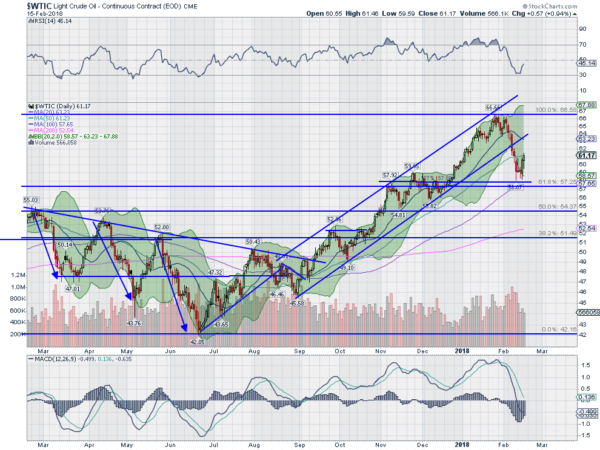

And about Crude as stand-alone trade?

- Greg Harmon, CMTVerified account @harmongreg – Crude Oil, a good spot for a bounce http://dragonflycap.com/crude-

oil-a-good-spot-for-a-bounce/ … $CL_F$USO

-

“If the stock market can reset and then move higher why can’t Oil prices do the same thing? The upside strength now sees potential resistance at the 50 day SMA and the prior support near 62.50 then the recent top at 66.50. A move over that could establish a target price of near 80. Now is a good time to be long Oil as long as it stays above the low of the week.”

“If the stock market can reset and then move higher why can’t Oil prices do the same thing? The upside strength now sees potential resistance at the 50 day SMA and the prior support near 62.50 then the recent top at 66.50. A move over that could establish a target price of near 80. Now is a good time to be long Oil as long as it stays above the low of the week.”

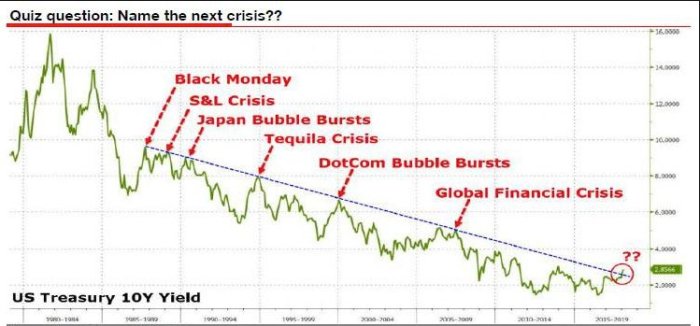

5. Lordy, What a Chart!

- Urban Carmel @ukarlewitz – Wed Feb 14 – Lordy, the GFC, tech boom, S&Ls and the entirety of Japan’s post-war boom all culminated because

$TNX hit a slanty line

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter