Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Why Then?

Friday’s Non Farm payroll report made up for whatever little weakness last month’s NFP showed – 250,000 jobs added, unemployment down to 3.7%, labor participation rate of 62.9% and above all 3.1% yr/yr wage gains. Actually the 3.1% number might be deceptively small:

- David Rosenberg @EconguyRosie – As with employment, the wage growth pick-up is broadening out. As in, a solid 3.4% annualized growth rate in the past three months. No doubt this is on the Fed’s watch list, and arguably just a little more of an influence on the next rates move than a presidential tweet.

With that number, yields had nothing to do but rise hard. The 30-yr yield rose 7 bps on Friday to close at 3.46%, higher than the 3.40% high reached after last NFP number on October 5, a rise of 14 bps on the week. The 10-year & 5-year yields also rose by 7 bps on Friday to close the week up 13 bps & 12 bps resp. at 3.21% & 3.04%, both still below their October 5 peak closes of 3.23% & 3.07%. If this momentum continues, then the 3-year & 2-year yields could soon close over 3% from their Friday closes of 2.98% & 2.91% resp.

But unlike in the first week of October, the stock market took this large rise in Treasury rates in stride. In fact, the stock market hardly noticed what was going on in Treasury yields just like stocks had hardly paid any attention to Treasury rates rising in September. That leads to the obvious question – would the stock market have suffered such a massive selloff in October had Fed Chairman Powell never uttered his loose comment “we may go past neutral … we’re a long way from neutral at this point, probably”?

We don’t think so. The markets took Powell at his word and immediately priced in a 4-handle federal funds rate & therefore priced in the entire Treasury curve with high 4 or even potentially 5-handle rates. That shock plus very heavy long positioning was enough to create fear & then carnage. Not only were absolute declines bad, but “the loss of momentum in the current selloff has been severe” as David Rosenberg put it.

We will see what Chairman Powell says in his FOMC statement this coming Wednesday. How he phrases the Fed’s intentions could prove pivotal.

2. What next?

The year over year wage growth came in at 3.1% . But where did the wage growth come from? From the high wage sector or the low wage sector?

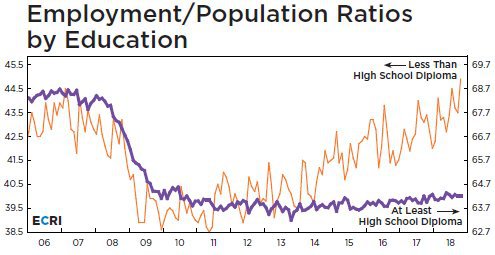

- Lakshman AchuthanVerified account @businesscycle – The least-educated now have more

#jobs than ever, with their employment-population (E/P) ratio soaring to a record high. In sharp contrast, the E/P ratio for more-educated workers continues to languish. See details: https://goo.gl/mpyuL5

So in this case, President Trump has kept the promise he made to the low-education workers. But is that inflationary? Compare the action in the 30-year rate vs. the rest of the curve. The 30-year rate is the only rate that closed above its October 5 close on Friday. And what is the 30-year rate most sensitive to? Inflation. So where is inflation headed?

So in this case, President Trump has kept the promise he made to the low-education workers. But is that inflationary? Compare the action in the 30-year rate vs. the rest of the curve. The 30-year rate is the only rate that closed above its October 5 close on Friday. And what is the 30-year rate most sensitive to? Inflation. So where is inflation headed?

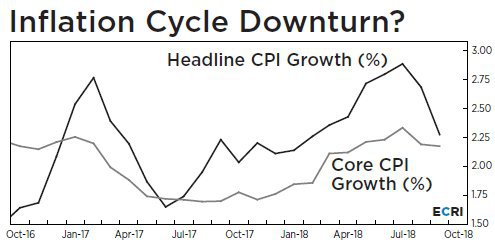

- Lakshman AchuthanVerified account @businesscycle – ECRI’s Future Inflation Gauge began pointing to falling inflation pressures in July.

@barronsonline reported: “That downturn is now a fact, not a forecast.” Today, yoy PCE deflator growth at 7 mo low, just like yoy CPI growth. https://goo.gl/pexf32

This means “ultimately yields should be heading lower, not higher” as Lacy Hunt of Hoisington Management explained in his conversation with Rick Santelli:

This means “ultimately yields should be heading lower, not higher” as Lacy Hunt of Hoisington Management explained in his conversation with Rick Santelli:

.

- “the main determinant of the risk free long Treasury rate is inflationary expectations defined by the Fisher equation and the inflation rate, in our view, has peaked for the year; it is turning down; there has been a major deceleration in bank credit, money supply growth; Fed is draining liquidity from the rest of the world; the $ is basically at an all-time high …. ; this serves as a deflationary pump; we have a synchronized monetary deceleration going on around the world; inflation rate is heading lower and ultimately that means yield will be heading lower, not higher.

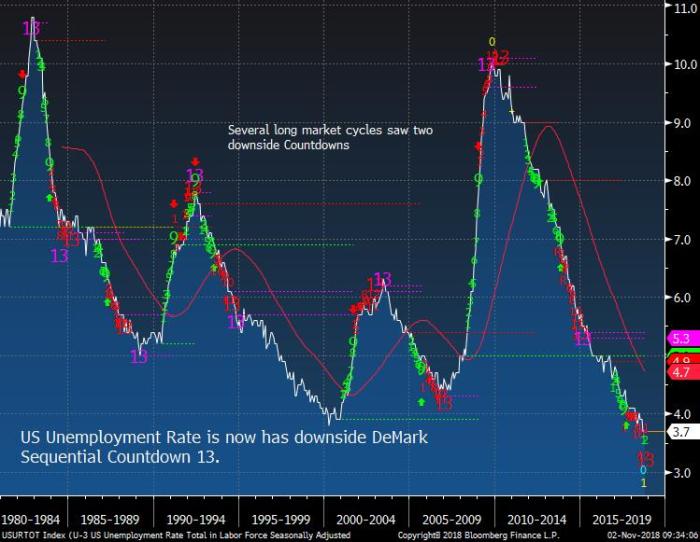

But what about the unemployment rate? Is that likely to halt its steady march too?

- Thomas Thornton @TommyThornton – US Unemployment Rate with rare monthly downside DeMark Sequential Countdown 13. Has been good signal historically. Expect upside move with unemployment rate into 2019. More on Hedge Fund Telemetry Daily Note today.

The last rate increase in the 1994-1995 rate hike campaign came in January-February 1995 and then rates fell during the rest of 1995 as if shot down in a barrel over Niagara Falls. That campaign of Greenspan vanquished the rise of inflation and created a disinflationary boom from 1995 to 1997. Chairman Powell mentioned this example of Greenspan in one of his early speeches. But will he follow Greenspan’s example?

We will see what his statement says on Wednesday.

3. US Stocks

Paul Richards of Medley Global Advisors has consistently warned about a binary outcome from talks between US & China. This week, Larry Fink said it clearly:

- “I was in China a few weeks ago, and I do believe if the path remains the same in the next few weeks, we’re going to have a full-fledged trade war, … Let’s hope I’m wrong.”

We all saw how seriously the US stock market takes this. After a big rally at the open went negative 200 points on the Dow, just one sentence from President Trump created a vertical 100-point rally. Is it likely that President Trump’s comments were intended for the midterm elections on Tuesday? Quite possibly. Yet, his administration could not send a false signal and hence the Kudlow backtrack.

We think protecting American edge & strength over China is an overriding goal of President Trump. He may weave & left & right tactically but strategically we think President Trump is serious. And his goal transcends the stock market.

Apart from China, the uncertainties about the midterms and the FOMC should get clarified next week, leaving Italy-Europe as the other big uncertainty. Just as Larry Fink is worried about US-China, Jamie Dimon is worried about sovereign debt risks from Italy-EU & Brexit. And the action in the DAX is testament to the binary outcome of such concerns:

- J.C. Parets @allstarcharts – German

$DAX is on the mount Rushmore of the most important stock market indexes on earth, as far as I’m concerned. Should we chalk this one up as a major bottom or a major top?

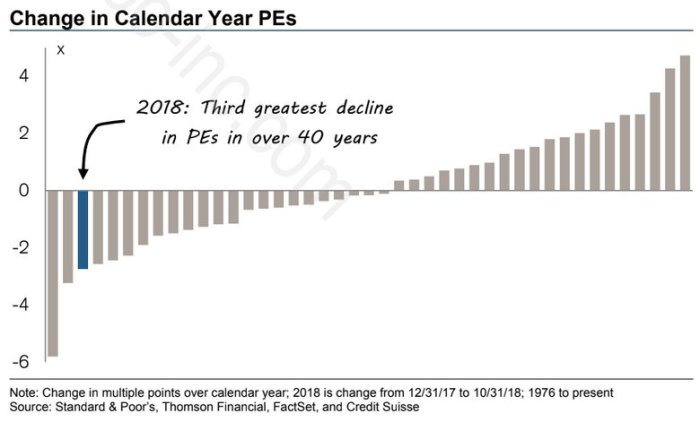

On the other hand, what do we know that is independent of these concerns? First, the improvement in valuations:

On the other hand, what do we know that is independent of these concerns? First, the improvement in valuations:

- Myles Udland @MylesUdland – Multiple contraction, via Credit Suisse

Then,

Then,

- SentimenTraderVerified account @sentimentrader There have been 11 other months when the S&P was down > 7% and consumer confidence was at a 1-year high. Six months later, the S&P was higher every time.

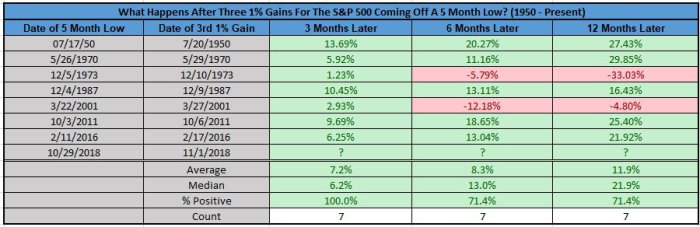

A more detailed table below:

- Ryan Detrick, CMT @RyanDetrick – What just happened is extremely rare, yet historically quite bullish. S&P 500 makes a 5 month low, then up 1% on 3 consecutive days? Since ’50, only happened 7 other times and 3 mos later up another 7.2% on avg and higher every single time. (the 7.2% is after the 3rd 1% gain)

This has been a great week for stocks with all broad indices up big – Dow up 2.4%, S&P up 2.4%, Nasdaq up 2.7%, NDX only up 1.6% thanks to Apple, RUT up 4.3%, Transports up 4%. Actually the rally was even greater on Friday morning, before the reversal late morning & afternoon. The question is how much of the bullish energy was used up?

This has been a great week for stocks with all broad indices up big – Dow up 2.4%, S&P up 2.4%, Nasdaq up 2.7%, NDX only up 1.6% thanks to Apple, RUT up 4.3%, Transports up 4%. Actually the rally was even greater on Friday morning, before the reversal late morning & afternoon. The question is how much of the bullish energy was used up?

- Bob Lang @aztecs99 – with the MC oscillators heated at +130 and +145 earlier today at market highs, buying power was used up. still think this is a possibility.

On the other hand,

On the other hand,

- Urban Carmel @ukarlewitz – A trend following sell signal triggered today. What happens next. New from The Fat Pitch https://fat-pitch.blogspot.com/2018/10/what-todays-trend-following-sell-signal.html …

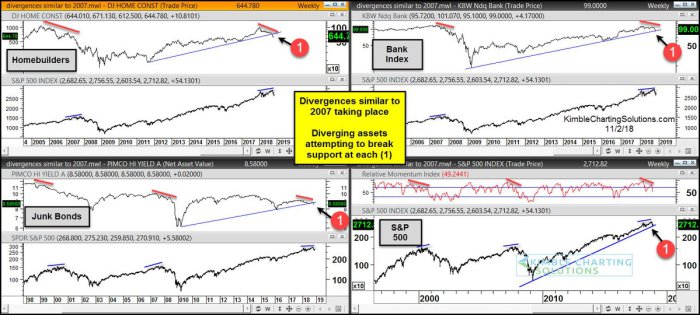

If a simple sell signal is not adequate, then a 2007 reference:

If a simple sell signal is not adequate, then a 2007 reference:

But doesn’t credit have to decline for a 2007 reference to even make sense?

- Jesse Felder @jessefelder It’s the worst October for U.S. junk bonds since 2008. https://www.bloomberg.com/news/articles/2018-10-31/junk-bonds-spooked-by-worst-october-since-2008-as-yields-spike …

We don’t usually discuss individual stocks, but Apple is so much more than an individual stock. And besides earnings, Tim Cook said unit sales don’t matter prompting the tweet below:

We don’t usually discuss individual stocks, but Apple is so much more than an individual stock. And besides earnings, Tim Cook said unit sales don’t matter prompting the tweet below:

- ValueTrap @Valuetrap13 Great Moments in Investing. Bob Nardelli, 2006: “Comps don’t matter.” Eddie Lampert, 2007: “Comps don’t matter.” Tim Cook, 2018: “Units are less relevant to our business.”

Can you talk about apple without mentioning Isaac Newton?

- Peter BrandtVerified account @PeterLBrandt – Will Isaac Newton be proven correct?

$AAPL

4. EM vs. S&P

Emerging markets performed great this week, beating the S&P by over 200 bps. EEM rallied by over 5%, Korea by over 5.7% and even India rallied by 4.5%. This, according to Ruchir Sharma, will be the case when the new bull market begins. Some of his points from his live appearance on CNBC were:

- “US over the rest of the world is the highest it has been since 1930s. While the US economy is 25% of the world economy, the US stock market is over 55% of the world’s market cap. This is simply unsustainable. He also thinks higher interest rates have already started to bite in the US and the demographics are not a positive. So the US economy is likely to catch down to the rest of the world. But the biggest risk is China. If China falls hard, then every market will fall.”

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter