Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Economy & markets – Clarida & Greenspan

What a super day was Friday! The S&P closed above 2,900 thanks to China, JP Morgan, Disney & Chevron. Fed’s Vice Chairman Clarida told us that the U.S. Economy was in a good place.

If U.S. Economy is in a good place, the Chinese economy must be in heaven. At least that’s how the Chinese consumers seem to think:

- Babak@TN China’s consumer confidence, measure of general #sentiment, is in the stratosphere… & yet, beware of hindsight bias! blue boxes added to Tavi’s original chart points to many times in the past one would have (falsely) drawn the same conclusion chart via@TaviCosta

What is the source of this confidence?

- Lisa AbramowiczVerified account@lisaabramowicz1 – China’s economic resurgence is being fueled (yet again) by a huge growth in leverage.

Her accompanying article details how much leverage or, to be more polite, credit growth:

- Aggregate financing was 2.86 trillion yuan ($426 billion) last month, compared with about 700 billion yuan in February, the People’s Bank of China said Friday. The median estimate was 1.85 trillion yuan in a Bloomberg survey.

- Financial institutions offered 1.69 trillion yuan of new loans in the month, versus a projected 1.25 trillion yuan

- Broad M2 money supply increased 8.6 percent, the fastest pace since February 2018

Clearly, the U.S. Fed is Uncle Scrooge in comparison. But the U.S. market is doing very well and just a stone’s throw from a new all-time high. All this because as Fed Vice Chair Clarida said to CNBC’s Sara Eisen:

- “markets are reflecting the fact the underlying momentum in the economy is good; we think the economy is in good place & we guess markets do see that“

In other words, the U.S. economy drives markets and the Fed determines policies that determine the economy & so they deserve the credit for the stock market rally. How did David Rosenberg describe this attitude of the Fed, more specifically the attitude he found in the Fed minutes released this week?

- David Rosenberg @EconguyRosie – What a confident group. If the Fed is adept at anything, it’s being completely flat-footed at inflection points — as history clearly proves.

We are simple folks who think simply. So instead of us commenting on Clarida’s claim of credit, we quote what Alan Greenspan, the Fed Chairman with almost two decades of Fed tenure, said on the same day:

- ” … what we don’t recognize is that Real GDP change is very largely a function of stock price change; a 10% increase in stock prices, say S&P 500, gives you a 1% increase in GDP over a quarter lag; … so there is a bit of a stock market aura about the current economy …”

In other words, the stock market rally leads to rise in GDP that influencesFed policy instead of the other way around as Clarida claimed.

Dr. Greenspan was not alone in expressing this sentiment. Ruchir Sharma, the Morgan Stanley strategist, said on CNBC Closing Bell that the “market drives what’s happening in the economy & the policies“. And Doug Ramsay, the CIO of Leuthold Group said the “stock market has become a fundamental“. Does all this answer the question implicit in the tweet below?

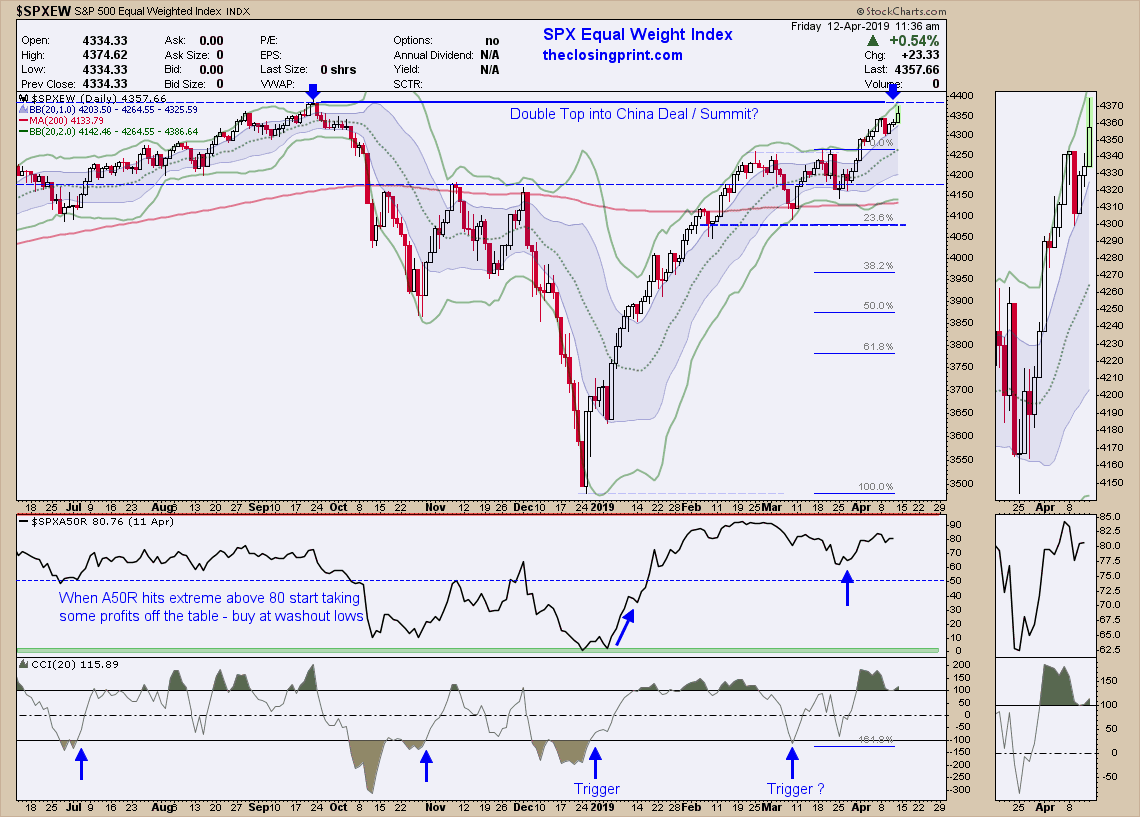

- Cousin_Vinny@Couzin_Vinny – $SPX potential 2x top or breakout – thinking 2nd half earnings would be better if China deal. Could also sell off. So, watching price $SPXEW

This poses another problem, a problem with interest rates. The rally in the US stock market led to a breakout in Treasury rates on Thursday & Friday. The 10-year yield closed above Santelli’s critical level of 2.55%-2.56%. So if this week is really a breakout of the S&P 500, then Treasury rates would also breakout. And that might, once again, damage the rate-sensitive sectors of the U.S. economy.

As Dr. Greenspan said, “the stock market rally to-date has already built-in a significant rise in GDP in the current period“. So a further rally to new all-time highs & beyond would further lead to a higher GDP later this quarter and in the third quarter. That might lead to Treasury rates rising back to challenge the Q4 2018 levels and put the Fed back into the “behind the curve” box, where they were in September 2018.

This situation reminds us somewhat of the mid-August to October 2007 period when Bernanke’s dovish posture lead to a big & fast risk-on rally & a new all-time high in October 2007. Perhaps because of that robust rally, Bernanke postponed lowering rates or even sounding more dovish till the late October FOMC meeting. By that time, it was too late and, as the experts announced later, a recession began in November 2007.

We have been worried about this prospect since the beginning of 2019. But now, after Greenspan’s analysis that the current economic strength has a stock market aura, we are getting even more concerned that the Fed is possibly going to repeat that mistake in 2019.

Vice Chair Clarida was radiating confidence when he told Sara Eisen that they are content to stay on hold. To us, that level of smug confidence either suggests arrogance or real unexpressed fear.

- David Rosenberg@EconguyRosie – This is not your 1986, 1995 or 2003 Fed, willing to take an insurance policy out on the economy. These guys aim to be reactive, not proactive, as they were back then.

Perhaps this is because acting proactively would send a message that they know they made a mistake in raising rates in December. And they would never admit that even if that means causing economic damage to America. Look what Clarida said to Sara Eisen:

- “I don’t think it [December rate hike] was a mistake; I voted for it at that time; if we rewind it, I wouldn’t change that view“

Look what the recent quarterly review of Hoisington Management wrote about the focus of the Fed on the stock market & coincident indicators, what they called “one fatal similarity” between previous Fed mistakes & the current Fed:

- ” … the Fed appears to have a high sensitivity to coincident or contemporaneous indicators of economic activity, however the economic variables (i.e. money and interest rates) over which they have influence are slow-moving and have enormous lags.”

What did that review say about the December rate hike?

- “In the most recent episode, in the last half of 2018, the Federal Reserve raised rates two times, by a total of 50 basis points, in reaction to the strong mid-year GDP numbers. These actions were done despite the fact that the results of their previous rate hike sand monetary deceleration were beginning to show their impact of actually slowing economic growth. The M2 (money) growth rate was half of what it was two years earlier, signs of diminished liquidity were appearing and there had been a multi-quarter deterioration in the interest rate sensitive sectors of autos, housing and capital spending.”

And the concluding sentence from that review?

- “It appears that history be being repeated – too tight for too long, slower growth, lower rates.”

Fed Chairman Greenspan was proud of the fact that no one understood what he was saying. In contrast, ex-Fed-Chair Greenspan was as clear as possible in this clip below:

After watching the above Greenspan clip, watch the detailed interview with Fed Vice Chair Clarida:

Kudos to CNBC’s Sara Eisen for two excellent detailed interviews and kudos to CNBC for putting the entire conversations on their website. Somehow we will all be referring to these two clips in the months ahead, we think.

2. Dumbo flies

Didn’t you & don’t you still get a thrill when Dumbo flew for the first time? You would if you still have even a little bit of a kid in you.

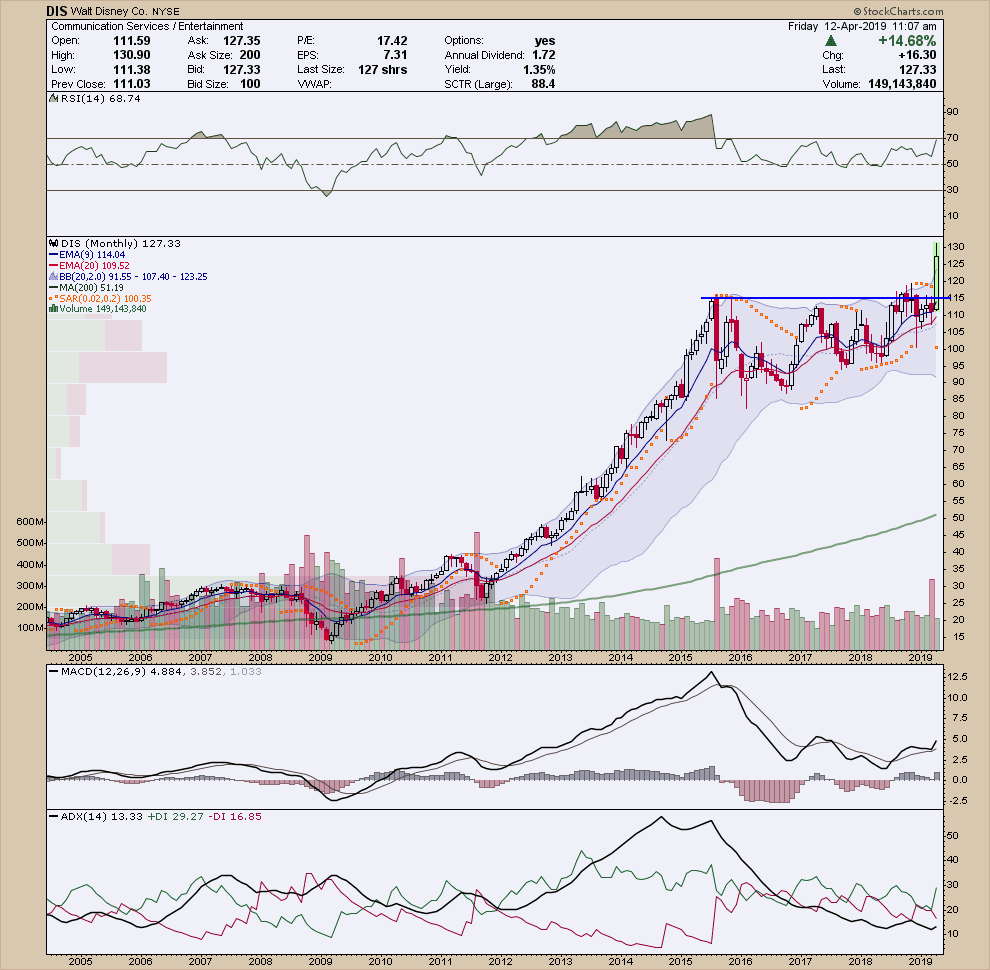

Investors reacted to the Disney announcement about their Netflix type product in the same joyous manner. The stock broke out in the same manner too.

- Cousin_Vinny @Couzin_Vinny – $DIS multi-yr breakout; looking at this swing same way as $LLY last year when it was trading 90/share. No chasing. Will setup first b4 entry

But we don’t think this Disney product will have any material impact on Netflix & its customer base. What we watch on Netflix, we won’t get on Disney & vice versa. So we thought the decline in $NFLX and rise in $DIS after the open was excessive. But by the end of the day, those levels were recaptured.

We missed the $LLY breakout but we do recall the Easterbrook-triggered break out of McDonald’s above $100. So this breakout in $DIS could be very real. After all, Eiger has re-engineered the company around this product.

But what about Netflix? Either because of Friday’s action or the upcoming earnings on Tuesday, Carter Worth of CNBC Options Action put a sell on it.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter