Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.”Deep State” has no clothes – Sessions & Powell redux

What former Fed ViceChairman Dudley wrote did this week is stunning in its bold arrogant simplicity. He disrobed the Fed’s assumed garb & revealed to the world what it is really is – the quintessential Deep State machinery in America; the ONLY Deep State machinery that is uncontrolled & virtually unanswerable to anybody. Any one who thought the sidelining of AG Sessions by the Department of Justice machinery was the height of deep state power learnt that the DoJ is merely a weak sister compared to the Fed.

Since last December 2018 we have been comparing former AG Jeff Sessions to current Fed Chairman Powell. We never thought Mr. Powell himself was a committed anti-Trump activist. But, based on his December 2018 presser, we felt Mr. Powell was being dominated by a more educated & much more committed Fed bureaucracy. He simply did not have the academic & personal stature of either Greenspan or Bernankeneeded to dominate the Fed’s army of hundreds of Ph.D.s.

We felt it was exceeding dangerous to have such a man at the head of the most independent & powerful agency in America. That is why we contrasted him & his Fed to the US Military & its then head General Jim Mattis. General Mattis resigned on his own, partly because he could have been fired by President Trump. But Mr. Powell contemptuously declared publicly that he would not resign even if President Trump asked him to. Now we see he was not being merely arrogant but he was carrying out the wishes of the Deep State within the Fed.

We thought this was so outrageously undemocratic that we wrote an article on December 22, 2018 titled Mattis vs. Powell – Tyranny of the Unelected. Interestingly, former Treasury Secretary Larry Summers used the same military vs. the Fed analogy in his public comments condemning Dudley’s comments that rivaled the anti-Trump derangement of Bill Maher. Dr. Summers also said,

- “… it is not the job of non-elected appointed officials to technocratic rile to decide how they can act to constrain & influence the President of the United States & the behavior of the rest of the government of the United States …”

But isn’t that the basic definition of “Deep State”, Dr. Summers? Why didn’t the CNBC anchor ask this basic question? Because the anchor, Sara Eisen, is herself a committed anti-Trumper?

Actually, Dudley may have made a big mistake by publicly asking the Fed to exceed their mandate.

- Jim Bianco@biancoresearch– – Jay, Without a good explanation, Dudley’s opinion piece, combined with comments made by Harkin (Philly) and Mester (Cleveland) can be interpreted as the Fed is violating its congressional mandate and attempting to “screw” Trump. Please address (3/3)

Bianco added:

-

Jim Bianco@biancoresearch – This is what Dudley accomplished … Republicans, that are currently hiding from Trump’s attacks on the Fed, will slowly come out and side with Trump against the Fed. Powell has to come out and blast Dudley. Having a spokesman do it is not enough.

But this Dudley episode & it’s condemnation by many may have done what tweets from President Trump have not done so far, as was pointed out by Cannacord’s Tony Dwyer:

- “… Dudley right there gave the Fed the flexibility to become aggressively accommodative … now they have to prove they are not biased against President Trump “

It may have done more than that. It may have given President Trump & his campaign a real & believable ammunition to put the blame for a recession on the Fed. Witness:

- Lawrence McDonaldVerified account @Convertbond – Fed Playing Politics Here? Rate Hikes 2018: 4 2017: 3 2016: 1* 2015: 1 2014: 0 2013: 0 2012: 0 2011: 0 2010: 0 Fed Balance Sheet 2019: $3.8T 2018: $4.3T 2017: $4.5T 2016: $4.5T* 2015: $4.5T 2014: $3.7T 2013: $3.1T 2012: $2.8T *$1.7T of quantitative easing pre-election

President Trump always had data like this. Now President Trump has a former Vice Chairman of the Fed, a long time veteran, proving the Fed’s “enemy of Trump” stance with his own words.

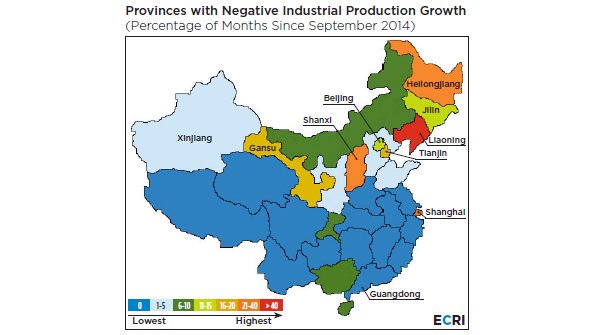

2. China & “the mother of all charts”

Clearly President Trump was unsettled by the sell off on Friday, August 23 from the angry exchange between China & him. So he pivoted & crossover-dribbled to a different “second thoughts” comment. He gave up nothing and gained a big rally on Monday. Then China gave an assist & the Dow rallied by 3%.

For his part, President Xi seems to have quelled a nascent revolt & the Party gave him a title that only Mao had before. So he also can talk tensions down a bit while he established his order in Hong Kong.

But what is really going on in China? Below is a chart from Lakshman Achuthan of ECRI that BTV’s Tom Keene called “the mother of all charts”:

- “The prime mover of the “Chinese miracle” has been its industrial sector, so declining industrial production in multiple rust belt provinces is a serious matter. This weakness in recent years has been exacerbated by the current global industrial slowdown that predated the trade war, which is also hurting global growth. ”

- “In Q1 2019, there was much hype around China’s trillion-dollar stimulus supporting the global economy. But a big part of that stimulus went to shoring up state owned enterprises in an effort to minimize job losses and keep zombie companies open.”

Achuthan’s conclusion?

- “As a result, Chinese overcapacity is pushing waves of deflation around the globe. And it’s not over.”

Those who think President Trump & the US is playing with a weaker hand should also look at Beijing’s reaction to US warships going through the South China Sea. In this connection, look how George Friedman compared the trade dispute with Japan in 1980s with the current trade dispute with China:

- “Japan’s geographical position proved vital to the U.S. defense of the Pacific. In addition to its proximity to Korea, Japan’s geography blocked the Soviets’ open access to the Pacific from Vladivostok. The latter was a fundamental interest of U.S. strategy, and therefore, the resurrection of Japan as a prosperous industrial power became vital to American power.”

But China is very different, as Dr. Friedman points out:

- “The United States cannot tolerate the possibility of China marshaling manpower, raw material and technology to protect its access to global sea lanes because guaranteeing that access would require the United States to retreat from the far Western Pacific. …. The Chinese cannot tolerate the United States being in a position to blockade China and savage its economy, potentially weakening Chinese unity.”

And technology is going to be the vital factor in future conflicts, far more than it has been in past wars. So what is America’s hammer in trade negotiations with China? Look what Hany Nada, co-founder of Acme Capital said on CNBC:

- “… I think the tariffs are doing some harm in near term …. but the longer term impact is much more detrimental to China than it is to us; US is the best on the planet at moving science to technology to product; we are cornering the market … tech companies are moving supply chains out of China to Vietnam, Malaysia, even Mexico … over time tech companies are going to adapt … China is going to be losing jobs, manufacturing capacity & that’s where the big impact is; that’s our hammer in these trade negotiations …”

Having said all that, we believe we will see the same a step forward, a step backward dance between USA & China all through 2020. This dispute is essentially unsolvable & both Presidents have other battles to fight, the most important being 2020 for President Trump and 2021 for President Xi. And those battles will need directing the attention from trade wars to matters of interest rates & stimulus.

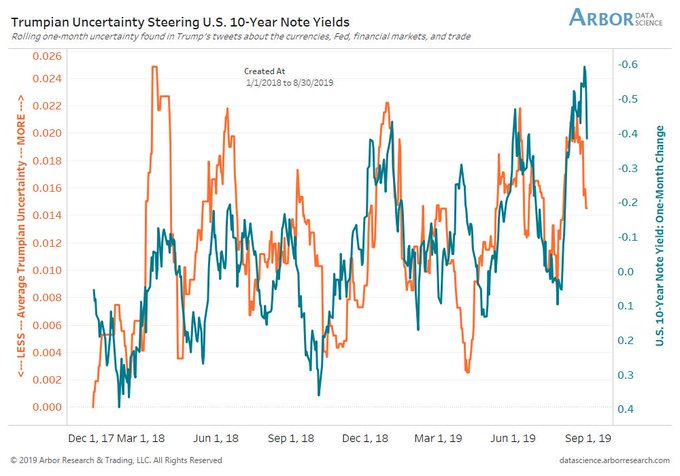

What the equity market is fearful is about a big rupture but not about the status quo. So if both leaders simply allow the status quo to continue, equity markets would be content, we think. Look, – “Trumpian Uncertainty” is actually falling:

- Ben Breitholtz @benbreitholtz – Trumpian uncertainty measured via tweets (NLP) is surprisingly falling, leading short-end Treasury volatility and 10-year yields lower.

That leads to:

3. Treasury Rates & the Fed

First the dog that did not bark. This was a week in which Dow Jones rallied 3% or 774 points & all averages rallied hard with even moneycenter banks like BAC & C rallying 4%. Even the failing transports rallied by 4%. If there was ever a week in which Treasury rates should have gone up & the curve should have steepened, it was this one.

But look what happened – the entire 30-2 year Treasury curve fell in yield & the curve actually flattened with 30-year yield falling by 5 bps, 10-year yield falling by 2.2 bps & the 5-2 year curve falling by only 1.5 bps. And this is in a week in which the Treasury Secretary tried mightily to steepen the curve by talking about issuing a 50-year T-bond. So what is going on?

Priya Misra of TD Securities answered this question in her conversation with BTV’s Jon Ferro on Thursday morning:

- .. the Treasury’s view is that the only reason curve is flat is because of the demand for the long end & the supply doesn’t exist; … I think the curve is flat because the market is saying the Fed is ineffective or not doing enough to get inflation expectations higher …

Lakshman Achuthan said to CNBC’s Kelly Evans that afternoon:

- … the Fed is wrongfooted cyclically & structurally …the moment to take the recession risk off the table has passed...”

Achuthan explained in a little more detail on Friday to BTV’s Tom Keene:

- “… the longer a slowdown becomes, we begin to move towards a recessionary window of vulnerability … a shock that was not a recession shock a quarter or two ago becomes a recessionary shock; that’s the key thing to watch …”

David Rosenberg was more direct:

- David Rosenberg @EconguyRosie – We now have had three months of a 3-mo/10-yr yield curve inversion. The track record this has had in predicting recessions: 100%.

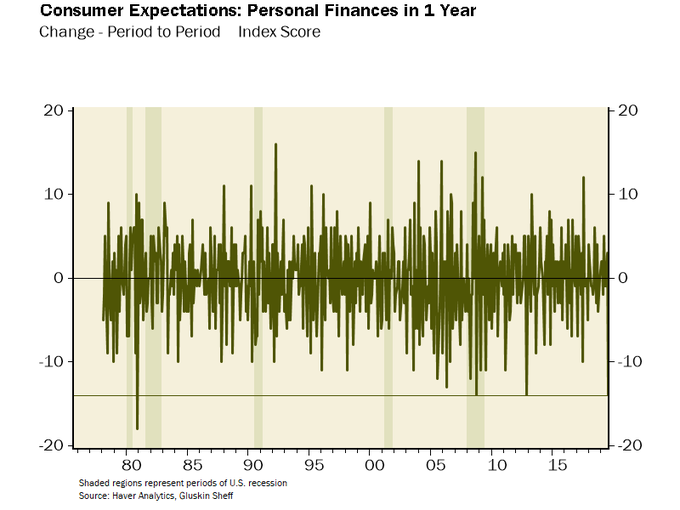

And what about the vaunted consumer?

- David Rosenberg @EconguyRosie– Household expectations of their personal finances plunged 14 points in August, tied for the second steepest slide since 1978. Guess where the savings rate is going from here?

With all this, next Friday becomes very interesting. What if the payroll report comes in stronger than expected? Would the Treasury curve steepen with the higher growth? Or will the Treasury curve flatten because such a report might prevent the Fed from easing rates aggressively?

With all this, next Friday becomes very interesting. What if the payroll report comes in stronger than expected? Would the Treasury curve steepen with the higher growth? Or will the Treasury curve flatten because such a report might prevent the Fed from easing rates aggressively?

The people who worry & the bond market are saying that the global slowdown will infect US growth & the Manufacturing slowdown will affect Services as it has done in Germany. The confident ones say the US is a closed economy & the US consumer is strong.

This is a sharp & verbally violent debate and such debates are resolved sharply & violently to use words of technician Carter Worth from his clip below.

4. Stocks – Good vs. Bad September

Since we quoted Mr. Worth above, we will begin with his descriptive “wake me up when September ends” directive. He said on Friday on CNBC Fast Money that the S&P is mired in sharp indecision & that is usually resolved sharply, lower in this case. He thinks the downside is to 2720. Hear him directly:

On the other hand, the legendary trader Larry Williams says, per Jim Cramer, that he sees a big rally in September beginning before labor day that should be sold at the end of September. Watch Jim Cramer communicate the case of Larry Williams:

Who makes a better case? We leave to readers. Who will prove to be right? We will find out by September end. But, to his credit, Jim Cramer said the above on Tuesday, August 27 evening. Since then the Dow has already rallied by 625 points & the S&P has rallied by 57 handles in the remaining three days of this week.

What about the legendary yield curve inversion? One factual tweet says:

- Lawrence McDonald@Convertbond – SPX Equity Market Drawdowns during periods of Yield Curve Inversion Dec 65 – Dec 69 -22% -17% -10% Mar 73 – Nov 73 -14% -10% -9% Aug 78 – Jan 80 -13% -10% Sep 80 – Jul 81 -10% Dec 88 – Jul 90 -11% -9% May 98 – Mar 01 -30% -22% -13% Dec 05 – Dec 07 -11% -11% -8%

But what about the immediate aftermath of an inversion? Isn’t there a rally first? Yes, a 15% rally on average said Tony Dwyer on CNBC Fast Money this past Wednesday.

What about sentiment?

- Urban Carmel@ukarlewitz – AAII 4-wk spread is now -19%. It’s been this low only twice since March 2009: early Feb 2016 and late Dec 2018 $spx

And a surprise in the last two days?

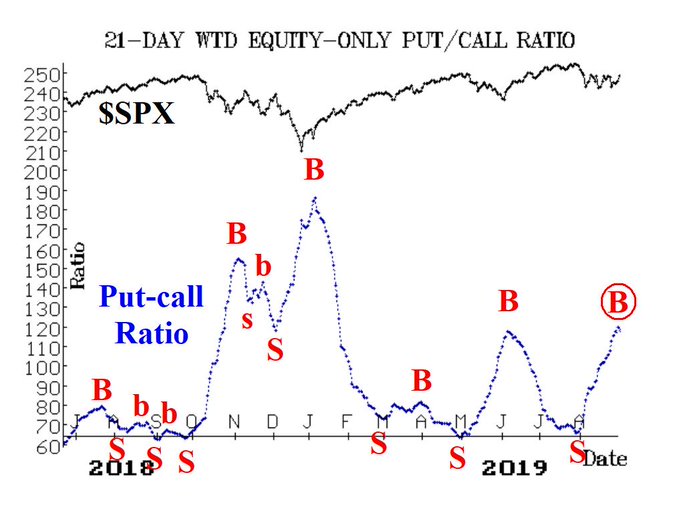

- Lawrence G. McMillan@optstrategist – In a somewhat major new development, both equity-only put-call ratios have rolled over to buy signals in the last two days. optionstrategist.com/blog/2019/08/w

But there is a caveat in his Friday summary:

But there is a caveat in his Friday summary:

- “In summary, the indicators have improved. But experience has taught us that there are times when nearly all other indicators are on buy signals, but the $SPX chart must confirm them, else the market will retreat once again. So, with $SPX near the top of its trading range, we are remaining negative in line with the $SPX chart, but would reverse that position on a close above 2950 by $SPX.”

5. Everything Up?

The Dollar was up 1.2% on the week, But did it break out to a new 2-year high? Depends on which Dollar index you use & how much Euro weighting it has.

- Mark Newton@MarkNewtonCMT -A couple key developments today- US Dollar- per Bloomberg Dollar index broke out to the highest level in 2 years.. ( Only 32% vs Euro vs 63% vs DXY)– DXY has not accomplished this yet given its heavy EURO component newtonadvisor.com

Regardless of this Dollar strength, Silver rallied up 5%, Oil rallied 2% & even Copper rallied 28 bps. Gold was marginally lower by 36 bps but the Gold Miners ETF (GDX) was up 78 bps.

And EM equities were up big – EEM up 2.8%, EWZ up 3.7%, EWY up 3% & even India up 1.8%. Heck, even EM Debt, EMB, was up 78 bps.

Why can’t all weeks be like this one?

6. People-politics

This week we heard about Treasury’s ideas to use the monies collected from Trade Tariffs to give a tax cut to people. Our earlier suggestion was to set up a Strategic Food Reserve by using trade tariffs money to buy food from US farmers that China would have bought and then use it for targeted hunger relief for needy Americans. But targeted tax cuts for needy American citizens might be simpler and better.

Targeted spending was a tactic used by PM Modi in India. His programs to build toilets across rural India paid off enormously in his 2019 re-election. The poor, a huge voting bloc, identified him as a leader who does things for them while others merely talk. Of course, toilets are one of the many programs introduced by PM Modi.

This week, he did something very smart. He cut the price of sanitary napkins sold in “people’s medicines stores” who cater to the needy & the poor. The new price of oxo-biodegradable napkins will be Rs. 1 or 1.4 cents (at 71 Rs to a Dollar), a 60% cut in the price of sanitary napkins, according to India Today.

This is a great pro-people program & a brilliant political one. Building toilets is fine but approx. 300 million people in India do not have access to running water. Women walk a couple of miles to get pots of water from a river and carry it home. That water is too precious & too scarce. So women have little choice but to sit in an outhouse type area during menstrual periods in villages, especially women from families who can’t afford regularly priced sanitary napkins.

This is a classic Modi program – designed to significantly improve women’s hygiene, provide a higher quality of life at a far reduced cost & save a highly precious resource like water. And it doesn’t hurt that poor women are the largest & most dedicated voting bloc in Indian elections.

7. Women scorned? Do they win later?

We have all heard the phrase about “women scorned”. But isn’t that to be expected more & more in our era of gender equality? Actually smart confident women have never been afraid of being scorned and they usually have the final win. Below are two who were scorned publicly & won in the end.

First from Tombstone (1993) – Doc Holliday telling Wyatt Earp – “I stand corrected Wyatt; you are an Oak“.(minute 1:40 to 2:00).

The other one from 1958, literally another era before the China-India war of 1962 – watch from minute 3;35 to 4: 10.

Both women show the anger & pain at being so clearly rejected. But both are confident enough to ignore the rejection. They both get their men at the end.

8. Will the Lady Scorn us again this year?

Unlike the two spectacular women above, we have been scorned every year by that cruel woman named Lady Luck. We have no doubt she will scorn us again on the Saturday before Thanksgiving if not earlier. But the journey is magical & full of hope. Michigan is again ranked high at No. 7 while that evil is ranked No. 5. But Urban Meyer has retired & so do we dare hope that Michigan will finally beat Ohio State?

Yes. The magical journey called College Football has begun. Enough Said.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter