Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.September Seasonality

On one hand, Sentimentrader.com wrote on Thursday,

- “Stocks have rolled right over every possible negative in 2021, and seasonality is a tertiary factor anyway. That said, the S&P 500’s returns after it closes the month of August at an all-time high was a sea of red, with positive returns over the next month only 20% of the time.“

Add a caveat & you see the other hand,

- Ryan Detrick, CMT@RyanDetrick – As we all know by now, September is the worst month of the year for the S&P 500. Down 0.5% on average since 1950. But if it makes a new ATH at any point during the month, the average return jumps to 1.4%, with a median return of 2.2%. Made a new high today.

What does it say when even one who argues that “minor top is actually due right now, and then a dip is due just after it” is actually bullish for September? Tom McClellan wrote on Thursday:

- “September has a bad reputation as a awful month for the stock market. This year, that bad stuff is likely to wrap itself up early in the month, and then surprise a bunch of analysts by bringing a rising stock market for the rest of the month of September“.

How about a really bullish view of September seasonality?

- From The Market Ear – “Still not a believer in the SPX seasonality? The 1995 pattern continues to trade rock solid. Time to get ready for the real melt up? SPX 1995 vs now needs little additional comments.”

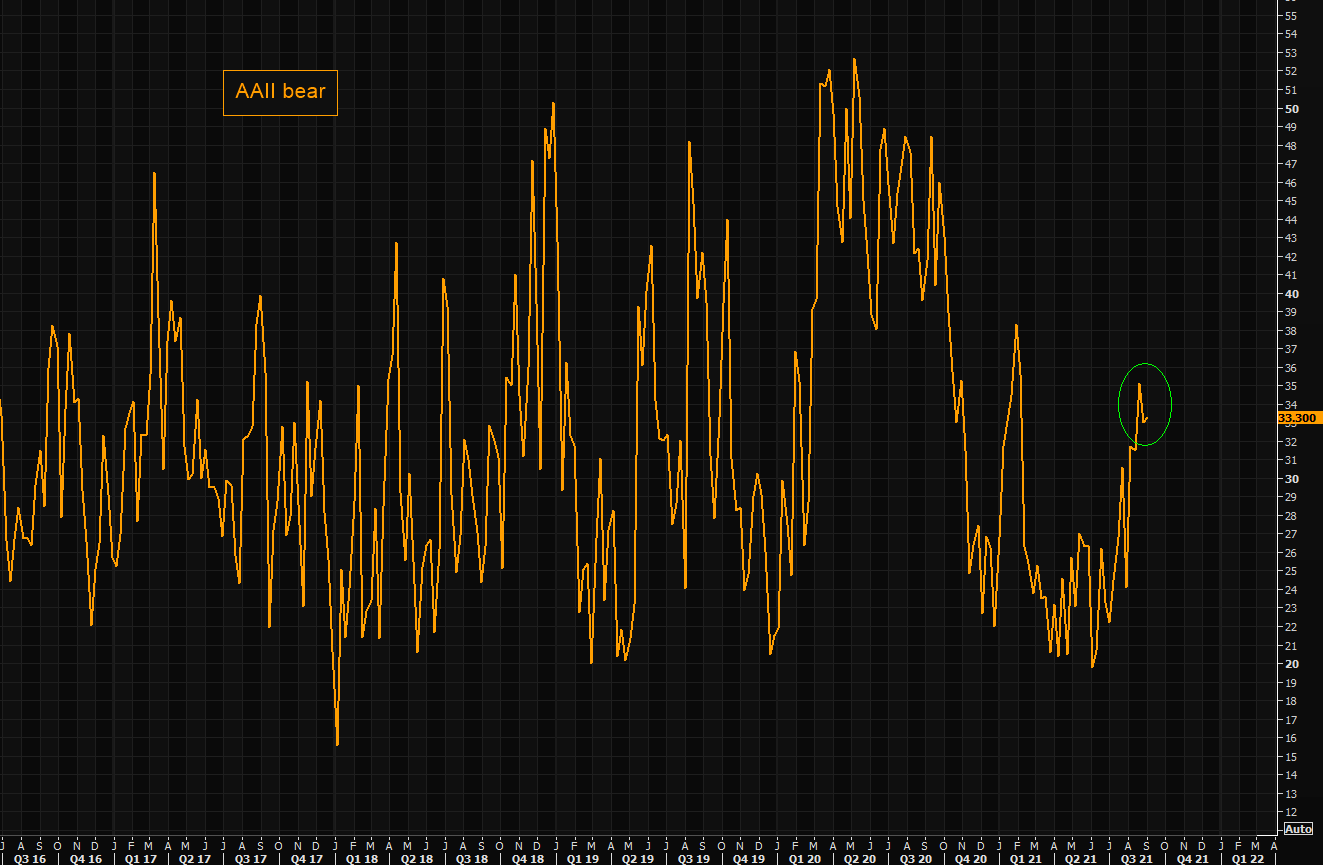

What about the Bears? Haven’t they disappeared? Not quite, according to some:

- The Market Ear – The problem with this market… …is that bears remain at elevated levels. Latest AAII sentiment shows bears refuse giving up. Therefore, the upside remains the main force…

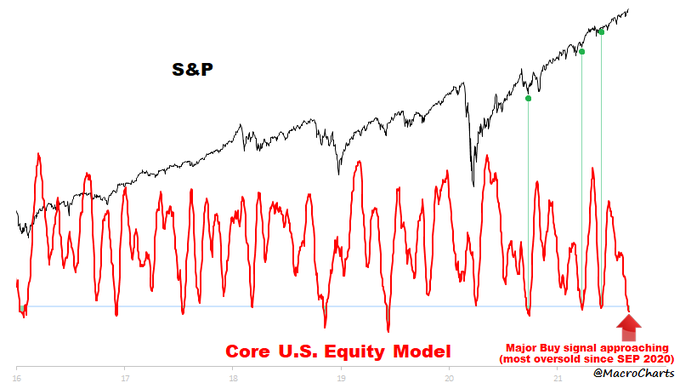

Does that mean a major buy signal is due soon?

- Macro Charts@MacroCharts – My most important Equity Models are oversold *again* – and could turn UP soon. Previous Buy signals led to big rally extensions – despite broad pessimism (see April blog). Once more – don’t underestimate how far this rally could go. A textbook Bull Market – follow the trend.

And what is a buy?

- Richard Bernstein@RBAdvisors –#Bloomberg Chart of the Day points out #smallcaps cheapest since…well…the last big #tech bubble.

Then you have the Tom Lee perspective:

2. Catalyst for global rally?

DXY, a U.S. Dollar ETF, was down every day of this past week. UUP, the other Dollar ETF, was down the past 3 days after being flat the first two days of the past week. What might this say for EM?

- Macro Charts@MacroCharts – EM Equity Flows. At the start of 2021, everyone thought EM would be the “trade of the year”. I warned in January: similar speculative euphoria led to big losses for EM investors. Today, no one wants EM. This is how big opportunities are made – be prepared for a Major change.

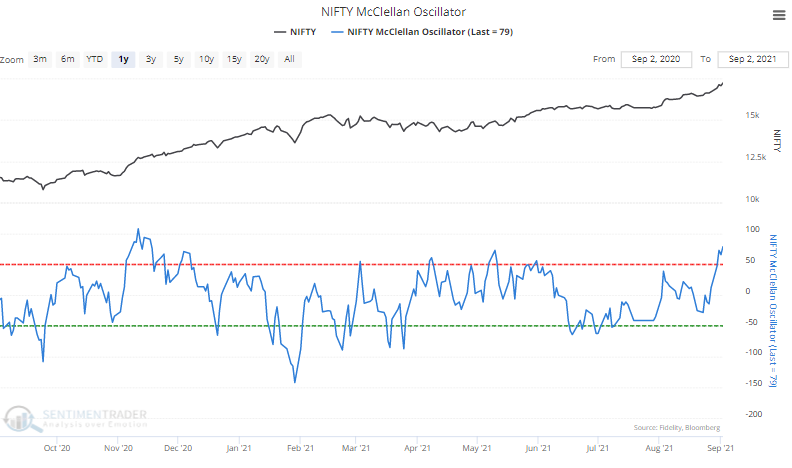

At least one EM market is not unwanted. Far from it according to Sentimentrader.com:

- Nifty rally. The Nifty 50 index of Indian stocks has shown incredible momentum of late, and the McClellan Oscillator – a measure of internal breadth momentum – is at its 2nd-highest level in a year.

As Larry McDonald of Bear Traps Report pointed out on August 31 on BNN Bloomberg, India was at the nadir of Covid 3-4 months ago and now jet fuel is at a record high in India with travel coming back.

Speaking more generally, he said succinctly “Covid is slipping away“. Meaning focus on $64 Trillion of non-US GDP instead of $20-22 trillion GDP in USA.

3. Treasuries, Bonds & “never seen in my career” condition

The Non Farm Payroll number came in steeply lower than expectations at 235K. But after an initial dip long duration rates went up and stayed up.

- Lisa Abramowicz@lisaabramowicz1 – This is what people are looking at: the upward revision in July to more than a million jobs created. Weaker August data is largely being seen as a blip due to Covid.

The other factor, in fact a rare one:

- Lawrence McDonald@Convertbond – Inflation expectations are higher with a 500k jobs miss, you don´t that every day.

On the week, the 30-yr yield was up 4 bps to 1.946%; 20-yr up 3.3 bps & 10-yr up 2 bps to 1.324%. Will the 30-yr cross back above 2%? It should if the target below is realized:

- Thomas Thornton@TommyThornton – US 10 year yield.

Frankly, we fervently wish for the consummation projected by Mr. Thornton. Besides our personal wish, our rational basis is Rick Rieder’s admission that “we are in a period of time like I have never seen in my career“. This master of trillions at BlackRock said so on Bloomberg Open post-NFP on Friday September 3 (at minute 17:10):

- “there is actually something really important that people don’t focus enough on; if you got additional supply, market can absorb it quite well; we are in a period of time like I have never seen in my career; it is demand for yielding assets particularly quality assets that is extra-ordinary; very absorbable by the market;”

Earlier in the show (at minute 9:50), Mr. Rieder pooh-poohed the concern about Fed’s tapering:

- “the amount of focus on Fed taper of $10-$15 billion a month!! you got net supply of $250 billion Treasuries a month; $100 billion of investment grade credit; $30 billion of loan supply; $30 billion of high yield supply and we are debating $10-$15 billion of Treasuries leaving the system!!“

So is it likely that Tom McClellan is right? That a dip in the next 2 weeks will be met by “a rising stock market for the rest of the month of September“?

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on Twitter