Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Price of Oil

Last week we used a caricature of the Devil to focus on what we think is the biggest risk to the world – explosion in the price of oil. But the steps taken by the White House (statement of Karoline Leavitt) & the declaration by Treasury Secretary Bessent on Friday, March 6, of sanctions removed on purchase of Russian oil by India helped lower the price of oil on Monday. As Bloomberg reported, Indian Refiners snapped up 30 million barrels of oil.

But oil resumed its upward move on Wednesday and things looked bleak. Then a new topic became center-stage – a phone call from President Trump to President Putin. And that brought forth the hypothesis that the two Presidents would discuss both the conflicts – Ukraine & Iran. In other words, Trump-Putin would act to finish off the Ukraine war before or at the same time Putin-Trump act to finish off the Iran war.

For a cleaned-up, politely discussed & more formal 10:53 minute discussion of this by Scott Ritter with Glenn Tiesen was published on You Tube by Strategic Dialogue Today on March 14, 2026.

With respect, we found the above as insipid as the proverbial heck. Because we had heard the honest discussion with critical details (who met whom, where, why – 25 minutes long) by Scott Ritter on The Jimmy Dore Show on Thursday, March 12, afternoon.

We think President Trump is smart when he is not angry & now we may be seeing a hint of a sign that he might be inching back to the Deal-Maker Trump. And if we do get what we fervently hope Trump-Putin deliver, then (OMG! We can’t believe we are saying this), we might possibly see a Nobel Peace Prize a la 1978 Begin-Sadat.

And oil will fall hard, thereby sending the Devil to wherever his abode might be.

2. Markets Last Week:

2.1 US Indices:

- VIX down 7.1% to 27.39; Dow down 2%; SPX down 1.6%; RSP down 2.3%; NDX down 1.1%; SMH up 1.8 %; RUT down 1.8%; MDY down 1.9%; XLU up 47 bps;

“Go with who brung you” is the colloquial wisdom, right? Hopefully @Subu Trade is right again!

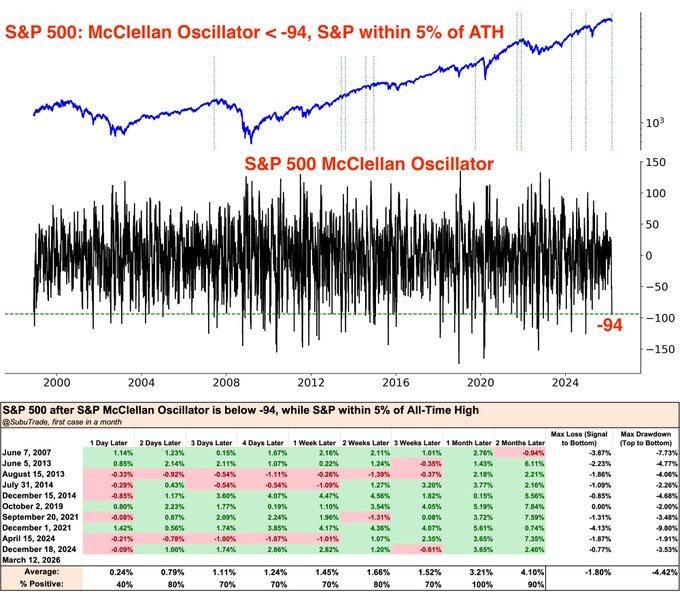

- Subu Trade@SubuTrade – Mar 13 – Despite being within 5% an all-time high, the $SPX McClellan Oscillator is extremely oversold. This setup has occurred 10 times previously, and $SPX was higher every single time 1 month later.

What does the $VIX (weekly) suggest?

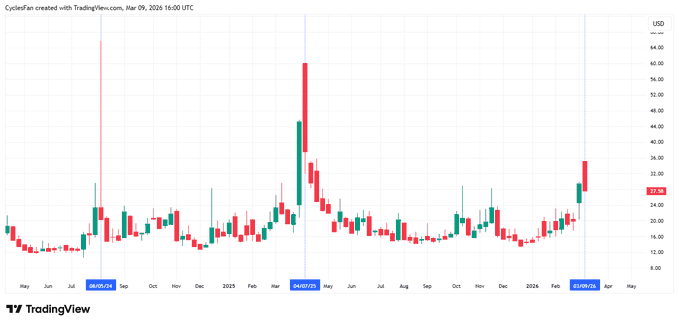

- CyclesFan@CyclesFan Mon – 3/9 – $VIX weekly – When did we see it pop above 30 on Monday, then sell off for the rest of the week before? That’s right. August 2024 and April 2025.

Guess that translates into cost of protection?

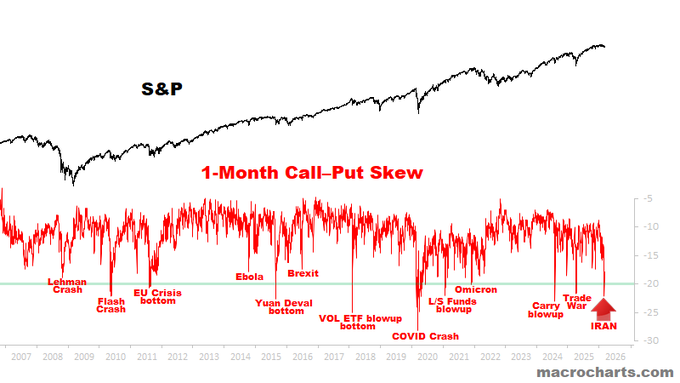

- Macro Charts@MacroCharts – 3-12 – The cost of protection is near the most expensive levels in history. *Is it sustainable? / What happens next?

And,

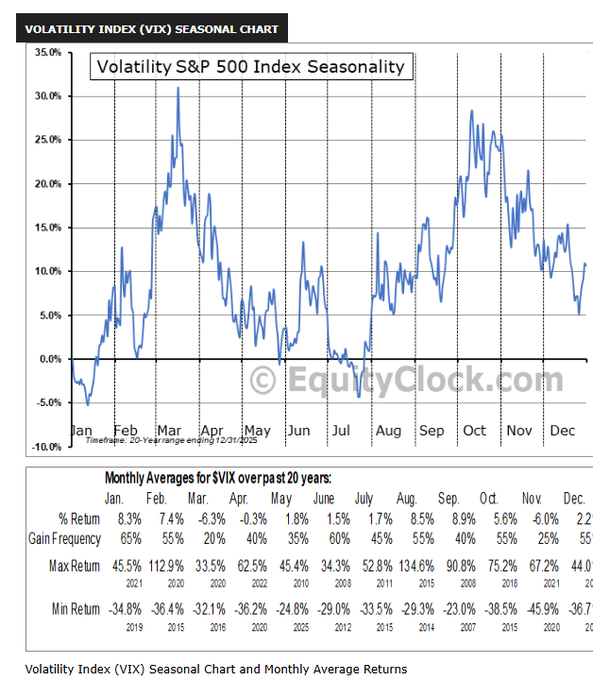

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – 3-15 – Beware the Ides of March… and spikey $VIX.. Volatility has historically fallen hard through April. @equityclock

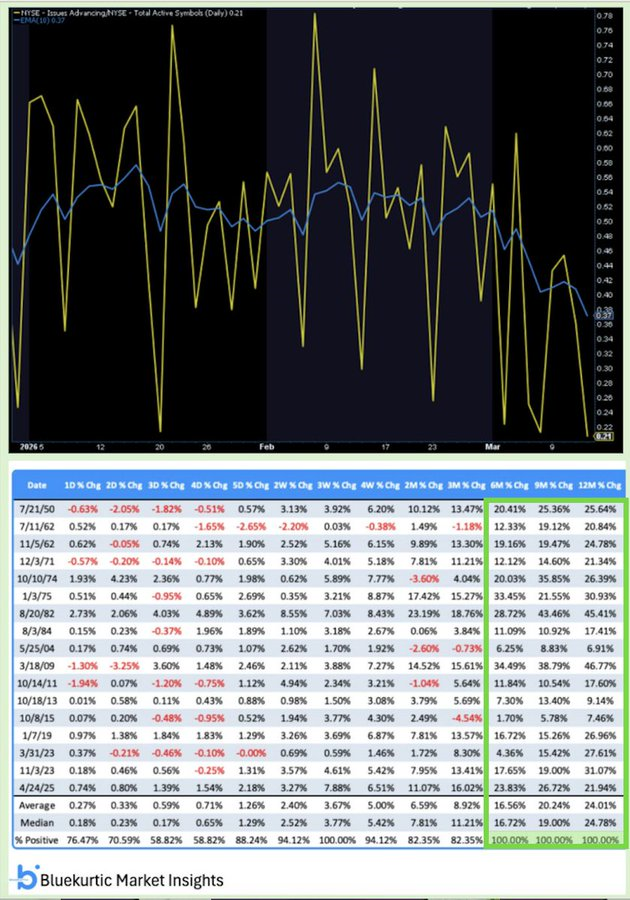

Can such a section be complete without at least one Zweig mention?

- Seth Golden@SethCL – 3-13 – 🚨On ALERT – “Down leg” of a potential Zweig Breadth Thrust achieved Thursday (.40 for 10-EMA) If within 10-trading days, 10-EMA then rises to .615, ZBT will trigger; If ZBT triggers, 6, 9, 12 months forward return positivity rate is 100%, never a negative return in 17 events (Most down legs do not achieve up leg requirement; ZBTs are rare historically) $SPX $ES_F $SPY $QQQ $NYA $IWM $AAPL $NVDA $SMH $VOO $VIX $NDX h/t

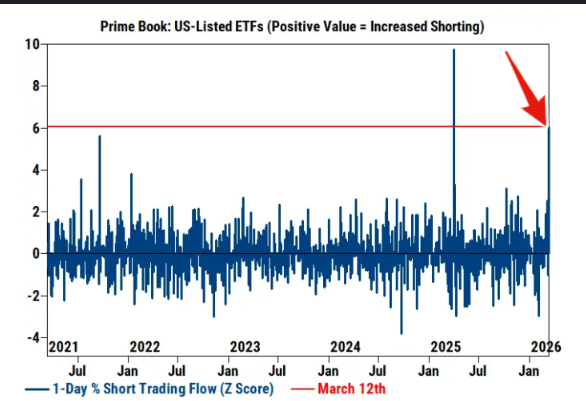

On the other hand, one should not dismiss the Market-Demons! Good to know they are loaded for bear, but who knows, that wait might prove fruitless.

- Markets & Mayhem@Mayhem4Markets – 3-14 – Insane. Hedge funds haven’t been shorting US ETFs this aggressively since the Anti-Tremendous Trade War of 2025. More evidence of a well-hedged market. All the big players are loaded up on insurance. Makes it harder for the market to go down too far/fast. Chart: Goldman Sachs

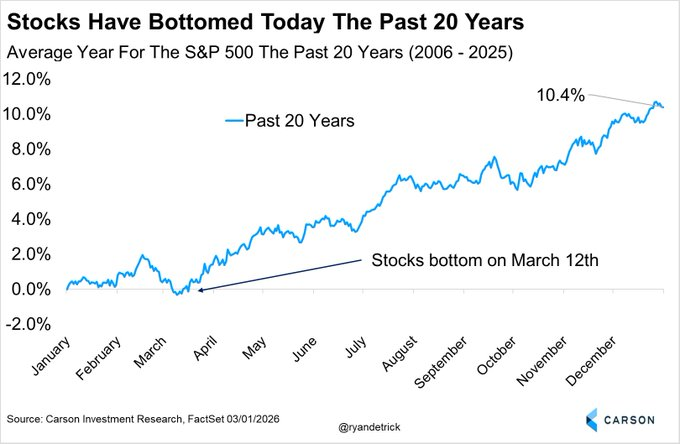

Finally, the type that sound lucky but work out more often than not!

- Ryan Detrick, CMT@RyanDetrick – 3-12- Over the past past 20 years, the S&P 500 has bottomed for the year on March 12th. Today is March 12.

2.2 MAG 7:

- AAPL down 2.9%; AMZN down 2.6%; GOOGL up 1.3%; META down 4.8%; MSFT down 3.3%; NFLX down 3.8%; NVDA up 1.4%; MU up 15.1%;

2.3 Key Financials:

- BAC down 4%; C down 79 bps; GS down 4.8%; JPM down 2.1%; KRE down 2.8%; EUFN down 3.5%; SCHW down 2.3%; APO down 3.9%; BX down 3.3%; KKR down 5.9%; XHB down 4.8%; ITB down 5.4%; NAIL down 15.9%;

The most important sector for 2026, in our opinion. The conditions in the economy, the ego of the financials & our attention to Private Credit (full credit to Gundlach for his very early detailed warning post-Fed in 2025) have been the main impetus in our 3 reductions in the Macro Viewpoints Over-Night Rate, the most recent one being on February 9. To put it shortly, last year’s setup reminded us of 2007. If the last 30 day have not reminded you of Q1 2008, then you must be either a who-cares mega-billionaire or TV anchors who only read from street-exes.

Kudos to Signor Hartnett of Merrill for his 2008 alert. From what we have heard, he is on the right track but still not fearful enough. Guess who is on the absolute right track to repeat their institutional & almost criminal negligence of 2008? The Fed. They came out on Friday, we believe and said they are postponing the 2 rate cuts they had discussed for 2026. Reminds us what a genius level professor had engrained in us in grad school that a backward-intelligence is the greatest risk to sound judgement in a highly analytical field.

We think Chair Powell is a good man, a gentleman in the traditional definition of the term. But he is the MOST Backward-Intelligence person we have ever seen. Check out:

And,

- Jeffrey Gundlach@TruthGundlach – 3-12 – “A Private Credit Fund of Funds in 2026 seems to rather closely resemble a CDO-squared in early 2007“.

What does this Sunday March 15 and upcoming Monday March 16, 26 remind you of?

- “Bear Stearns officially collapsed and was sold to JPMorgan Chase in a government-backed deal over the weekend of March 15-16, 2008“.

More importantly, recall what happened after that? Two well-known financial investors-traders went around asking investors to buy Brokerage Firm corporate bonds. It was an excellent trade for awhile & collapsed when the Treasury & Fed allowed the Fannie & Freddie preferreds to fail on September 7, 2008. It was a disastrous decision because Lehman collapsed one week later on September 15, 2008.

The 2008 Fed DID NOT CUT interest rates for four months after the Bear Stearns “rescue” on March 16, 2008. In fact, they doubled their focus on inflation & the rise in Oil price (which peaked on July 11, 2008) and then began falling.

That Bernanke Fed had cut rates by 25 bps on April 30, 2008. Then the Bernanke Fed focused on the rapid rise in Oil & ignored the increasing softness in the US economy. They allowed the collapse in FNMA & Freddie Mac; they did NOT act when Lehman collapsed on September 15, 2008. They waited till October 8, 2008 to cut rates by 50 bps and then, in a panic, cut 50 bps again on October 29, 2008 & then by 100 bps on December 16, 2008. (see https://www.forbes.com/advisor/investing/fed-funds-rate-history/)

We think the recent explosion in Oil prices is NOT an inflationary warning. In fact, as in 2008, we think this explosive rise in Oil is nearly guaranteed to scare the middle-low income & result in intense deflationary pressure.

But the 2026 Fed is showing they are far more interested in focusing on this oil price increase & showing their utter contempt of middle-lower income America. We hope we are completely wrong but we may not be.

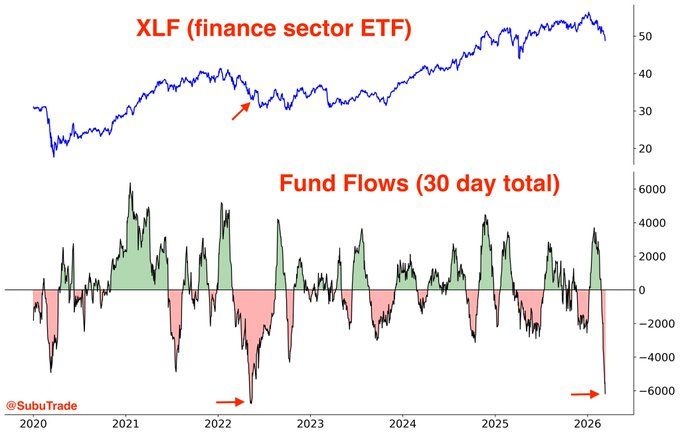

Why this recollection of late March 2008? Because we remember the rally in Financials in April 2008! Why is that relevant? Because smart folks see a rally coming in financials after the drubbing of recent weeks. After all if the CDO-Squareds of 2008 rallied in April-July 2008, then why can’t firms with ownership of Private Credit rally in the next few weeks?

After all, as a smart guy points out:

Then came the below on Sunday morning:

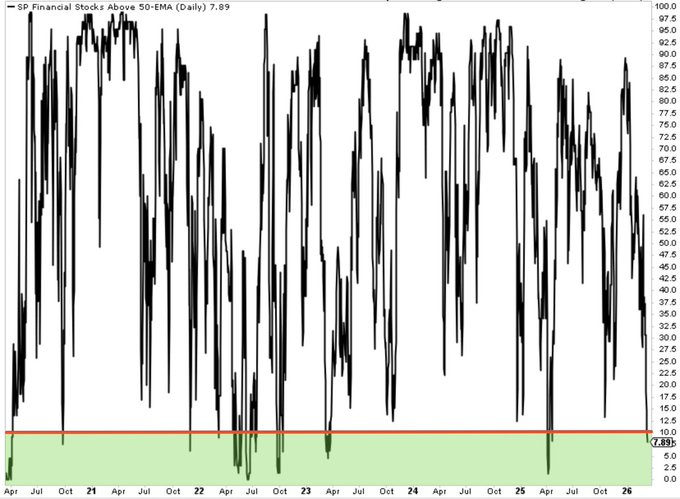

- Seth Golden@SethCL – 3-15 – Critical Oversold Condition; There are now fewer than 8% of Financial stocks trading above their 50-EMA; Financials are the 2nd heaviest weighted sector in the S&P 500. Rarely get such an oversold condition in a bull market without a significant bounce near-term. $SPX $SPY $XLF $JPM $GS $BAC $C $KRE $SOFI $SCHW $DPST

3.4 Dollar & Commodities

Dollar was up 1.6% on UUP & up 1.7% on DXY:

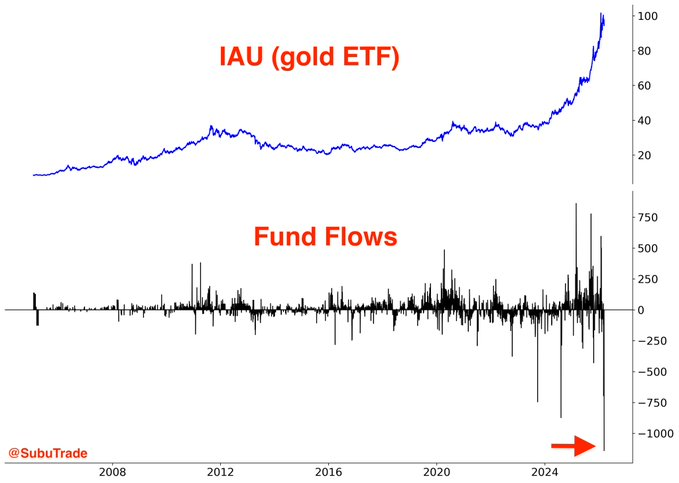

- Gold down 2.9%; GDX down 8%; Silver down 4.7%; Copper down 2.4%; CLF down 14%; FCX down 5%; MOS up 11.4%; Oil up 8.8%; Brent up 11.7%; OIH down 59 bps; XLE up 2%;

- Subu Trade@SubuTrade – 3-14 – Gold ETF $IAU just saw record outflows

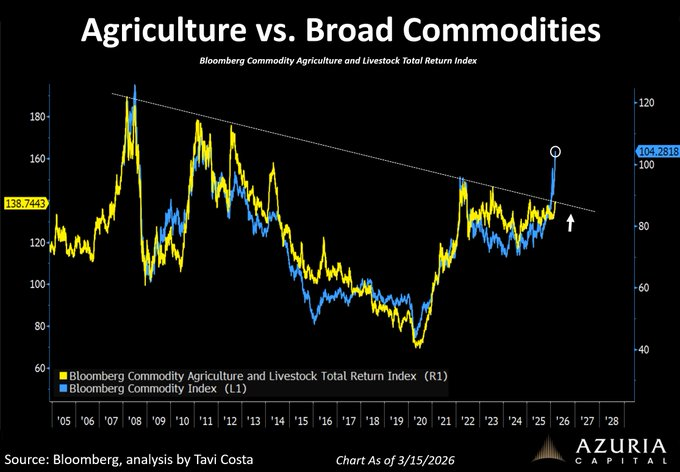

Remember the focus on Canadian company Potash & the explosive rally in mid 2008? Do Agricultural commodities offer an opportunity now?

- Otavio (Tavi) Costa@TaviCosta – 3-15 – This is one of the most compelling setups for agricultural commodities I have seen. Broad commodities appear to be leading the move, while agricultural commodities remain just below a major historical resistance level. A breakout could be the next step. Here is where I elaborate further on this topic: https://substack.com/@tavicosta/p-190883016

3.5 – International Stocks:

- EEM down 91bps; FXI up 1.2%; KWEB up 1.5%; EWZ down 2.2%; EWY down 2%; EWG down 2.4%; INDA down 3.9%; INDY down 4.4%; EPI down 3.3%; SMIN down 3.2%;

2.5 Treasuries & Interest Rates:

- 30-year Treasury yield up 14 bps on the week; 20-yr yield up 16 bps; 10-yr up 14 bps; 7-yr up 14 bps; 5-yr up 14 bps; 3-yr up 16 bps; 2-yr up 17 bps; 1-yr up 10 bps;

- TLT down 2.2%; EDV down 3.3%; ZROZ down 3.5%; HYG down 61 bps; JNK down 72 bps;

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on X.