Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Blue Shocked the World & Markets!

The last great memory we had of UofM campus was the 1989 stunning win of Michigan over Seton Hall. Glenn Rice torched Seton Hall with his 3-point shooting scoring 31 points while Rumeal Robinson played the entire game & sank the last 2 free throws for the Championship.

Those can now remain as happy memories after the Best Michigan College Team Ever won a great game over UConn this past Monday. Did this victory have something to do with the market’s rally this week? That’s what us believers think!

Now to the more mundane things!

2. Markets This Week

2.1 US Indices:

- VIX down 19% to 19.23; Dow up 3%; SPX up 3.6%; RSP up 1.8%; NDX up 4.5%; SMH up 11.4%; SOXL up 44.8%; RUT up 4%; MDY up 3.3%; XLU up 1.3%;

- Seth Golden@SethCL – 4-10 – I’m not in the business of betting against the INSIDERS. As evidenced by the chart, this is the highest level of Tech Insider buying we’ve seen in the last 15 years. That seems like a pretty powerful signal juxtaposed with highest Tech sector Y/Y EPS growth since 2021. They know their earnings potential better than anyone! $SPX $XLK $AAPL $NVDA $MU $AVGO $PLTR $MSFT $IGV $SPY $QQQ $NDX h/t @jaykaeppel

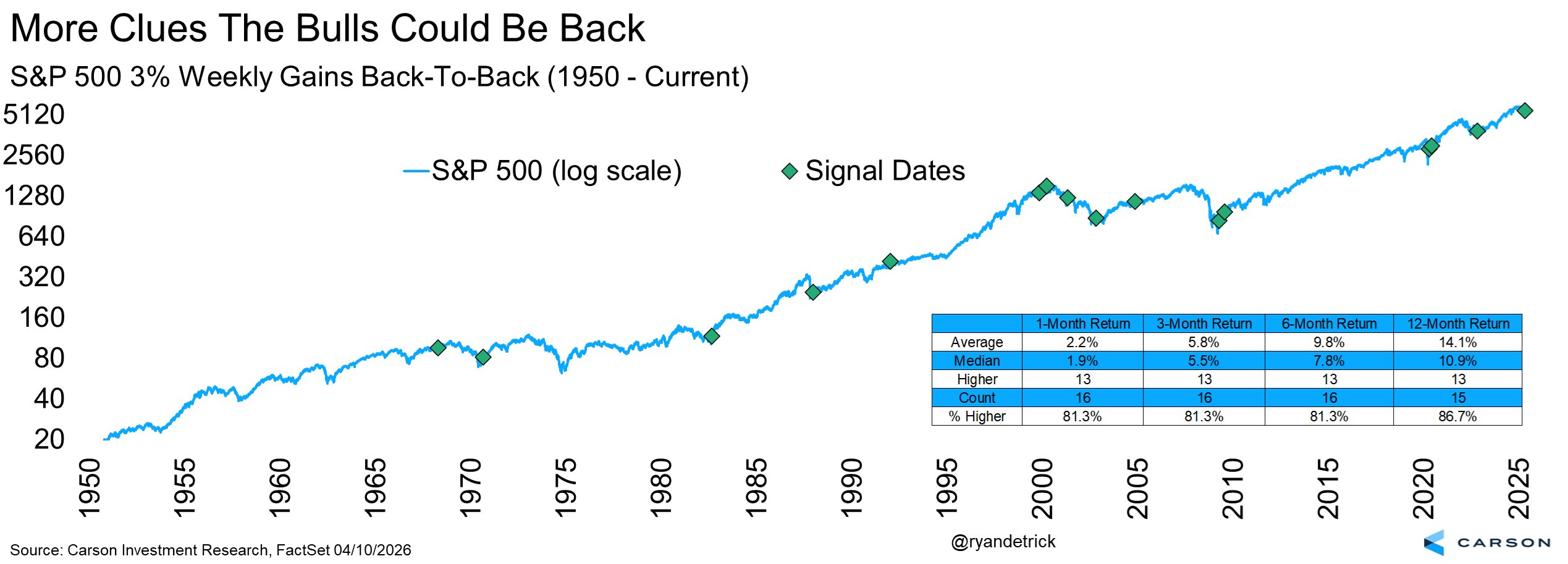

- Ryan Detrick, CMT@RyanDetrick – 4-10 – More good news for the bulls. S&P 500 up >3% back to back weeks is historically quite bullish. Above average returns across the board and higher a year later 86.7% of the time.

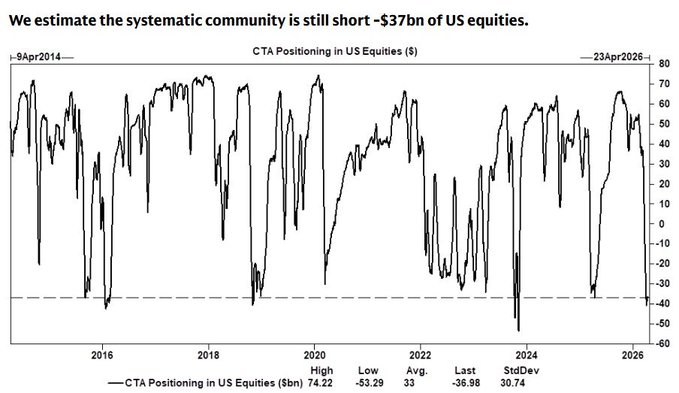

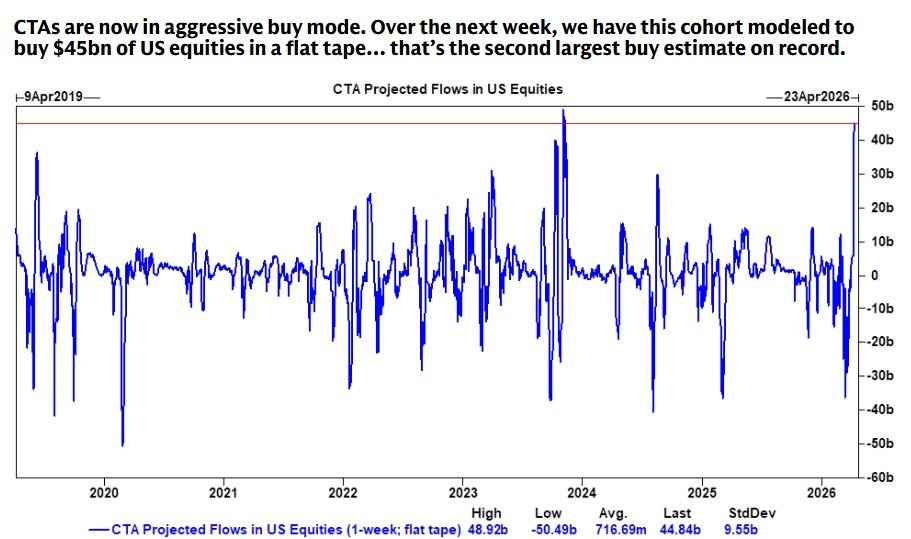

And 3 charts that suggest a lot:

- Macro Charts@MacroCharts (via Detrick) – 4-10 – stunning charts from GS — big extremes here:

2.2 MAG 7:

- AAPL up 1.8%; AMZN up 13.6%; GOOGL up 7.3%; META up 9.6%; MSFT down 69 bps; NFLX up 4.5%; NVDA up 6.3%; MU up 14.8%;

Dan Niles covered NVDA & Semis with AI & META, MSFT on Tuesday April 7 with CNBC’s Mike Santoli:

A quick summary below:

- “THIS LULL, I THINK YOU’VE SEEN IN CHIP STOCKS, I THINK YOU’RE GOING TO SEE THEM GET A LOT STRONGER. … YOU’RE GOING TO HAVE TO BE SELECTIVE. BUT I THINK YOU’RE GOING TO SEE THEM GET A LOT STRONGER AS YOU GO THROUGH THE REST OF THIS YEAR. BECAUSE OF THAT MOVE TO AGENTIC AND THE MASSIVE INCREASE IN COMPUTE THAT THAT TAKES”.

- I’VE TALKED ABOUT CISCO IN 1997 AND 98 HOW IT WAS DOWN 37 TO 38% INTRA YEAR BOTH OF THOSE YEARS. AND IT FINISHED THOSE YEARS UP 31 AND UP 150%. AND I THINK NVIDIA SORT OF IN THE SAME CATEGORY … THIS MOVE WITH AGENTIC REQUIRING A

LOT MORE TOKENS, MEANS THAT I THINK NVIDIA ENDS THE YEAR HIGHER THAN WHERE IT IS TODAY

2.3 Key Financials:

- BAC up 6.4%; C up 7.9%; GS up 7.5%; JPM up 5.2%; KRE up 4.5%; EUFN up 5.9%; SCHW up 1.1%; APO down 2.8%; BX up 1.6%; KKR down 1 bps; XHB up 5.7%; ITB up 4.5%; NAIL up 12.9%;

John Kolovos of Macro Risk Advisers told Mike Santoli on Tuesday:

- “I am actually very bullish on the market of stocks warming up to the stock market; … tech ex-software is doing pretty decent; same with financials… if you look at the advance-decline lines of those two groups, they are actually near new highs … Banks is what is different & biotech is quite interesting as well”

We will find about Banks next week.

2.4 – Dollar & Metals

Dollar was down 1.5% on UUP & down 1.3% on DXY:

- Gold up 1.8%; GDX up 5.1%; Silver up 5%; Copper up 4.3%; CLF up 7.6%; FCX up 10.5%; MOS down 5.4%; Oil down 13.6%; Brent down 12.9%; OIH up 2.7%; XLE down 3.9%;

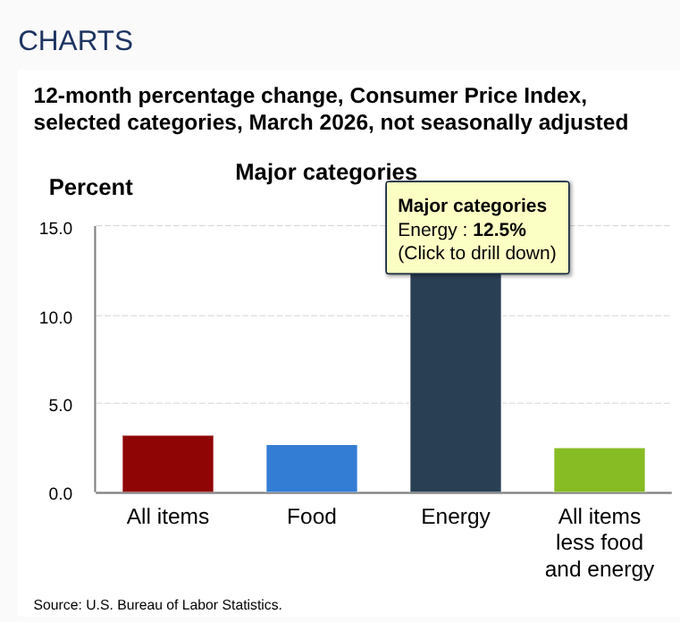

- Markets & Mayhem@Mayhem4Markets – Energy costs stand out, rising 12.5% year-over-year as oil surged to triple digit territory in March.

2.5 – International Stocks:

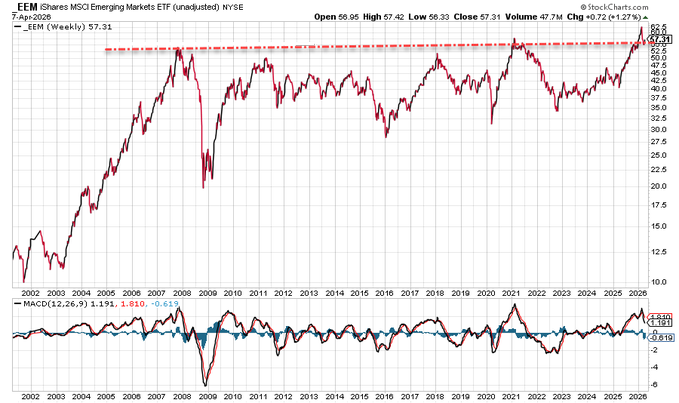

- EEM up 7%; FXI up 1.9%; KWEB up 2.2%; EWZ up 7.8%; EWY up 12.9%; EWG up 4.3%; INDA up 5.8%; INDY up 4.9%; EPI up 5.3%; SMIN up 7.3%;

What are the smart guys saying?

- Ryan Detrick, CMT@RyanDetrick – Most important chart in the world? Emerging markets broke out and tested their peak from 2007. So far, this important area is holding. Again, bullish action for the bull market we are in right now.

Any market in particular?

- The Market Ear@themarketear – 4-8 – Brazil is ripping… and you’re probably not in.

Well, we don’t know who the “you” above refers to. We know that Stephanie Link of Hightower has been in & hopefully those who heard her on CNBC are also in.

2.6 Treasuries & Interest Rates:

- 30-year Treasury yield up 0.2 bps on the week; 20-yr yield up 1.9 bps; 10-yr up 1.4 bps; 7-yr down 0.4 bps; 5-yr down 0.2 bps; 3-yr up 0.2 bps; 2-yr up 0.6 bps; 1-yr up 3.3 bps;

- (as of Thursday close) TLT down 35 bps; EDV down 65 bps ; ZROZ down 74 bps; HYG up 50 bps; JNK up 54 bps;

What are the CTAs doing, you ask!

- zerohedge@zerohedge -4-8- CTAs Are Max Short Treasuries,As Goldman Warns Of Overshoot Risk

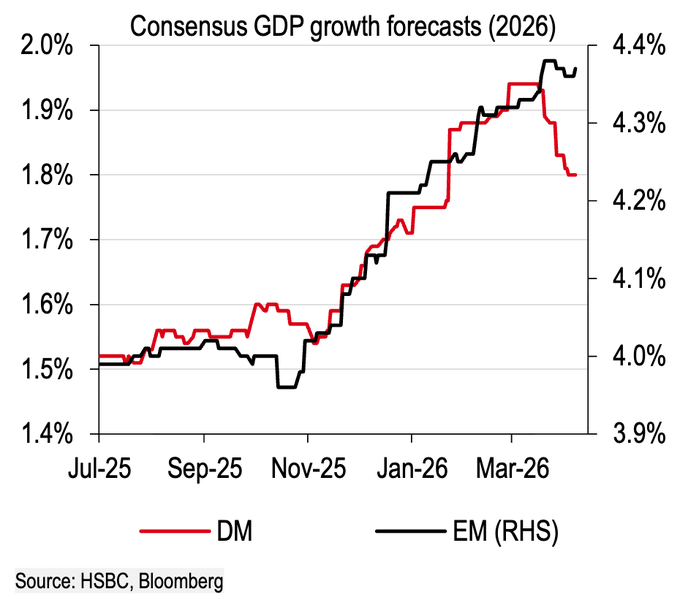

What about growth, you ask?

- (((The Daily Shot)))@SoberLook 4-10 – Growth expectations have rolled over for developed markets, but have held up for EM. Source: @HSBC

Meaning buy US Treasuries & EM Stocks or EM-exposure stocks!

3. Pig Stays inside Python for years? – Software & Private Credit

The analogy came from Bruce Richards of Marathon Asset Management who has been extremely smart to avoid direct lending to software companies while others have been doing so with 8,9,10 turns of leverage.

In his analogy, the pig will remain inside the python for next many years, the pig being direct loans to the software sector. In his words, ” the BDCs are … trading at 25-30% discount to NAV … because all the exposure there is to software“.

He added,

- “the valuation of 20 times that PE paid for a lot of these software companies allowed the private credit manager to justify somehow they can lend at 10 times on that business; its too much leverage & companies can’t sustain that“

And one reason the pig is still early inside the python is that

- “valuations just got reset in the last quarter; the maturities aren’t happening until 27 or 28. And the price to get out is a very, very low price … some in the sixties, some in the fifties, & some in the forties“.

When asked “do you just stay away from software“?, Bruce Richards said:

- “the reason you have to stay away is the default rate is going to go .. 15% in software specifically …. and it won’t be 15% one year; it will be double digit default rates for 3 straight years. “

- “And with very simple terms, the defaults are going to be massive“

Kudos to Bloomberg TV for covering this topic & allowing Mr. Richards the floor for 10 minutes to explain the above to simple folks like us.

The above clip was posted by Bloomberg on Tuesday, April 7. Now, just for the heck of it, pull back the 5-day chart of $IGV and notice the steep drop from Wednesday April 8 to Friday April 10. Did investors happen to view the above clip or others like it and reduce their exposure to software & perhaps move that money to SMH?

But some smart minds saw a positive divergence by the end of the week!

- Ryan Detrick, CMT@RyanDetrick – Nice one from @FrankCappelleri in his note this AM. Software is back to the late February lows, but positive divergence with RSI.

4. Second worldwide event eclipses the First

Readers might recall our coverage of the fantastic film Dhu-Run-Dhar that began on December 28, 2025. It has been a humongous success, that too for a “real, raw & violent“ film. Until then, we did not believe that Indians would make such a stunningly raw, violent film. As we wrote then, we watched it on the big screen at AMC 25 in Times Square, NY on 3 separate times & loved it more every time. Then we watched it twice on Netflix & loved it there too. We wrote then that Dhurandhar “will be for a long time the symbol of New India, a confident, aggressive India that responds violently to every attack on India“.

Watching Dhurandhar became a smart & necessary act for major North American & European political leaders interested in Indian politics & business. Watch Canadian PM Carney & the Finland President Stubb bring up Dhurandhar during their recent jog in Hyde Park, London:

When asked how was his event in India, Carney said “it was huge after I said I watched Dhurandhar“. Then watch the Finland President say that his son asked him to watch Dhurandhar & he did. Hear him yourself above.

A few days ago, we watched Dhurandhar again on Netflix. It wasn’t the same though. Yes, the film was great & we liked it, of course. But this time, the film felt softish even a but gentle and actually a bit slow.

Then it struck us that this time we had watched Dhurandhar AFTER we watched its sequel Dhurandhar 2 – The Revenge at AMC 25. And the first Dhurandhar pales before the raw reality, violence, passion & speed of Dhurandhar 2.

First & foremost, the “Revenge” depicted is that of the horrific, inhuman attack on 26 November 2008 by Napaki govt- sponsored terrorists on Mumbai & their mass murder of Hindu, Jewish citizens of Mumbai. And this Revenge is depicted as sheer real, raw, violent in a fast way we have never seen in any film, Indian or otherwise. It is the true of representation of a confident, aggressive India that responds violently to an attack on India.

The Dhurandhar Revenge film is 3 hours & 50 minutes long, about an hour longer than Dhurandhar 1. And you don’t feel the time even a little bit. Not only is the film great, its reception by the Indian people has been mind-blowing. In a mere 3-4 weeks, Dhurandhar 2 has blown past the revenue record that Dhurandhar had collected.

And this Dhurandhar 2 has gone global. We all know that Israel has been busy with its own harrowing experience. But during that harrowing time, Israel reached out & requested that Dhurandhar 2 be screened in theaters & movie screens across Israel. And, as usual, Dhurandhar 2 is also drawing huge illegal views in Napakistan despite the Napaki government’s ban on the film.

The biggest surprise is how the Gen Z generation has become fans of Dhurandhar 2. The ones who missed the first Dhurandhar found it a bit difficult to connect with Dhurandhar 2. So guess what the Gen Z crowd in Hong Kong did. They demanded that both films be shown one after another for a mega experience – 7 hours of non-stop Dhurandhar action in one seating. In Hong Kong? Who would have thunk it?

And, by the way, Dhurandhar: The Revenge has entered the list of the world’s top 10 highest-grossing films of 2026, marking a significant milestone for Indian cinema. Led by Ranveer Singh and directed by sensational Aditya Dhar (pronounced Aaditya), the film has crossed $175 million globally, outperforming several major international releases. This is despite the fact that it takes 93 Rupees to make 1 Dollar.

Predictably, the anti-Hindu establishment has not liked it even a bit. They prefer Hindus to be pathetically weak beggars of help from the white liberal crowd. So led by the Economist, they mounted a campaign against the film. Naturally that led to more people watching Dhurandhar 2 and showing contempt of the Economist. But to their credit, CNN-India (CNN-News 18) derided the stupidity & racism of the Economist. Watch it & decide for yourselves.

Why can CNN-News 18 be a real fighting channel while CNBC-TV 18 is so afraid of its own shadow? By the way, a couple of days ago, the best coverage of the US-Iran talks in Napakistan was on this CNN-News 18 show with the same anchor. And they were able to seamlessly incorporate a fresh CNN-US interview by Ms. Erin Burnett in their show in India.

5. Now What?

Obviously, we refer to the breakdown of the US-Iran negotiations last night. We are not smart enough to figure out the whys or wherefores, but we are grateful to this interlude because it enabled the beautiful equity rally of the last two weeks. And a continued rally or at least a stable stock market is what benefits the US & President Trump both generally & in these circumstances.

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on X.