Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Markets Last Week

1.1 US Indices:

- VIX up 41 bps to 17.06; Dow up 22 bps; SPX up 2.3%; RSP up 63 bps; NDX up 5.5%; ; RUT up 1.7%; MDY up 1.6%; XLU down 3.9%; SMH up 11.1%; SOXL up 35.7%

What about this month?

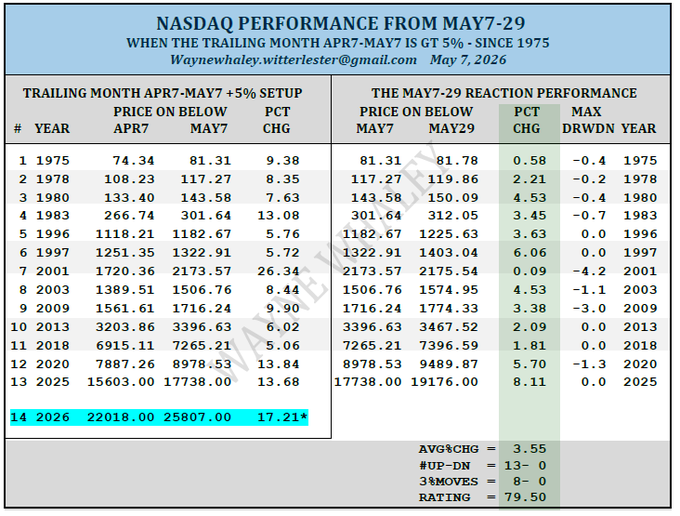

- Seth Golden@SethCL – In the 13 prior years in which the Nasdaq was up at least 5% from Apr 7-May 7, the following May 7-29 time frame was 13-0 for an average gain of +3.55%. Rally-on Garth, Rally-on Wayne Whaley! $SPX $ES_F $SPY $QQQ $AAPL $SMH $NVDA $AMZN $TSLA $IBIT $ETH $SMU $CRWD $HACK $VIX

And,

- Ryan Detrick, CMT@RyanDetrick – May 7 – We continue to see clear signs to be overweight equities here and this from @granthawkridge is another reason. High beta stocks are breaking out relative to the S&P 500, while low volatility is breaking down.

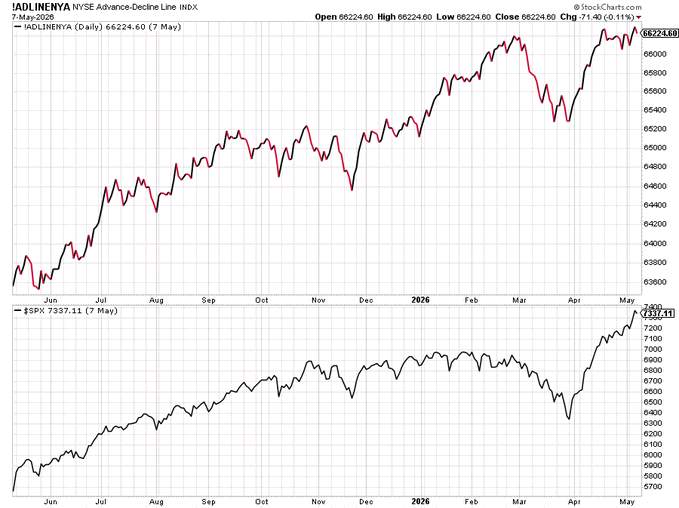

A message from the A/D line:

- Ryan Detrick, CMT@RyanDetrick – A lot of talk again how only a few stocks are going up. This isn’t true, much like it hasn’t been true for years. NYSE A/D line hit a new ATH on Wednesday. Hard to think this happens if only a couple stocks were going up.

On the other hand:

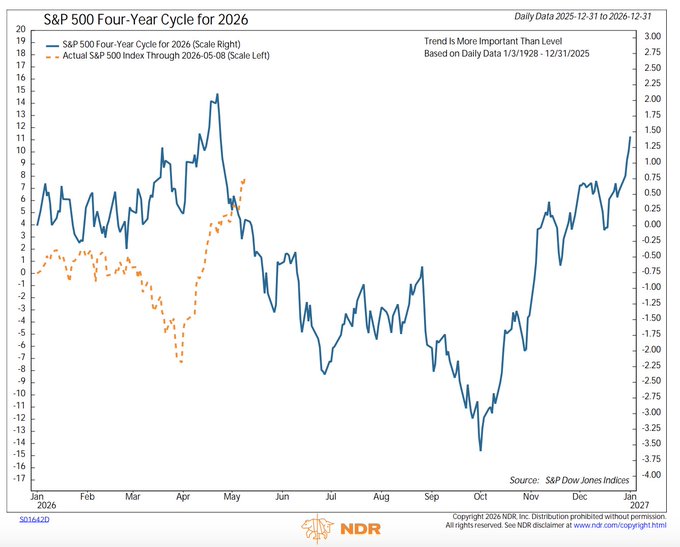

- Seth Golden@SethCL – When Midterm-Cycle 2026 got off track w/average Midterm yr performance I warned bears and alerted bulls of the more probable mean reversion coming. Now with 2026 outperforming, and where a mid-year correction usually occurs, price action may prove sloppy for next few months, at worst, Barring exogeny/endogeny!

Along that line,

- Trader Z@angrybear168 – Bullish divergence on both the $VIX and $VVIX, maybe we could get a temporary news shock next week to spike fear? Not a signal to short but hopefully the market pulls back to offer everyone a better risk to reward entry.

And,

- @TheMarketEar – SOX weekly RSI at the highest levels since March 2000.

2.2 MAG 7:

- AAPL up 4.7%; AMZN up 1.7%; GOOGL up 3.9%; META up 14 bps; MSFT up 16 bps; NFLX down 5%; NVDA up 8.4%; MU up 37.7%;

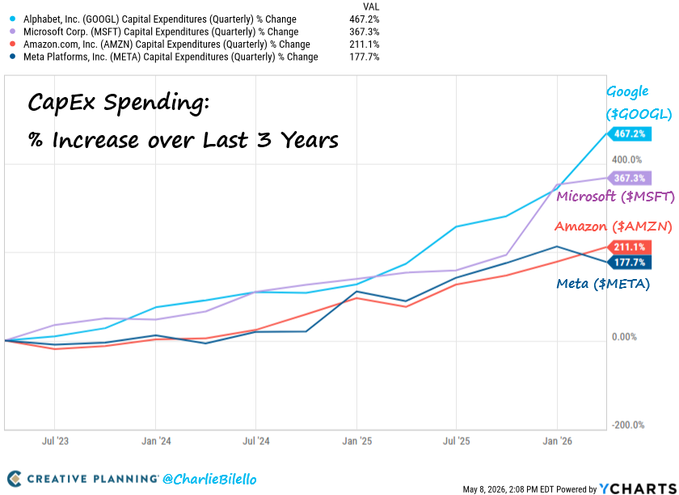

The fundamentals behind the Mag 7 move are & remain the same.

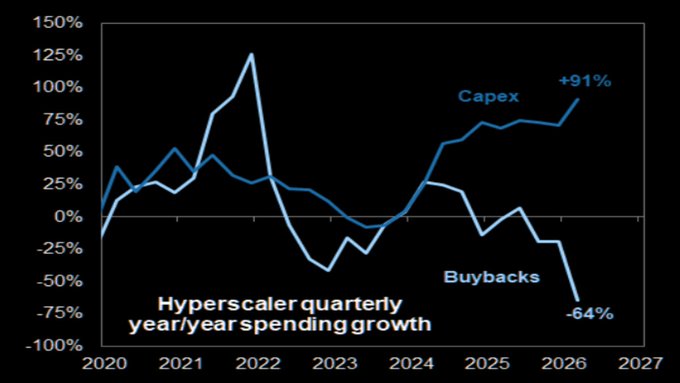

- Charlie Bilello@charliebilello – Increase in CapEx spending over the last 3 years… -Google$GOOGL: +467%; Microsoft$MSFT: +367%; Amazon$AMZN: +211%; Meta$META:+178%

And looking forward,

- zerohedge@zerohedge – 5-4 – Hyperscaler Capex Expected To Hit $1.1 Trillion In 2027, Up From $800BN This Year

In a sense, the 8% plus move in $NVDA may be interesting.

John Kolovos of Macro Risk Advisors made interesting comments to CNBC’s Mike Santoli on Thursday after the close. Remember Thursday afternoon showed a “bit of a candle-reversal“. Regarding $NVDA, he said:

- “so what I am telling clients is hang on loosely; … rotating back to $NVDA might actually save the top here; … you have a market with RSI of 83 (in $QQQ), very very high …. but NVDA is not; it has middling momentum & we look to NVDAs of the World to save the the top from completely falling… “

More broadly, he sees the S&P at 7,500 before we roll over for the summer in his opinion.

2.3 Key Financials:

- BAC down 3.6%; C down 1.5%; GS up 1.4%; JPM down 3.3%; KRE up 4 bps; EUFN up 1.1%; SCHW down 3.2%; APO up 2.1%; BX down 2%; KKR down 1.1%; XHB down 2.5%; ITB down 1.9%; NAIL down 6.9%; IGV up 5.2%; CRM down 1.1%; PANW up 14.8%

Since corporate credit is a major issue in this sector, take a look at a broad & diverse discussion about the economy & credit in Section 2.6 below.

2.4 – Dollar & Metals

Dollar was down 26 bps on UUP & down 35 bps on DXY:

- Gold up 2.4%; GDX up 8.6%; Silver up 6.8%; Copper up 5.5%; CLF up 4.9%; FCX up 9%; MOS down 4.2%; Oil down 7%; Brent down 7.2%; OIH down 5.4%; XLE down 5.4%;

First metals:

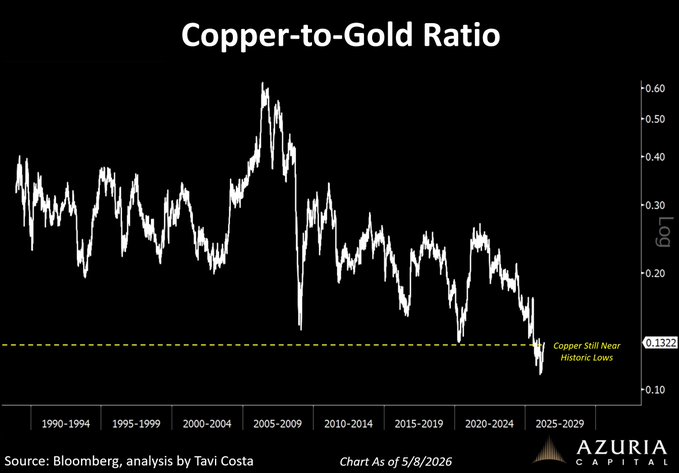

- Otavio (Tavi) Costa@TaviCosta – It’s wild to see copper hitting record highs while still trading near historical lows when priced in gold terms. The copper-to-gold ratio remains nearly 80% below its 2006 peak. More importantly: Periods where copper became this cheap relative to gold have historically not lasted very long. https://tavicosta.substack.com/p/copper-at-record-highs

And,

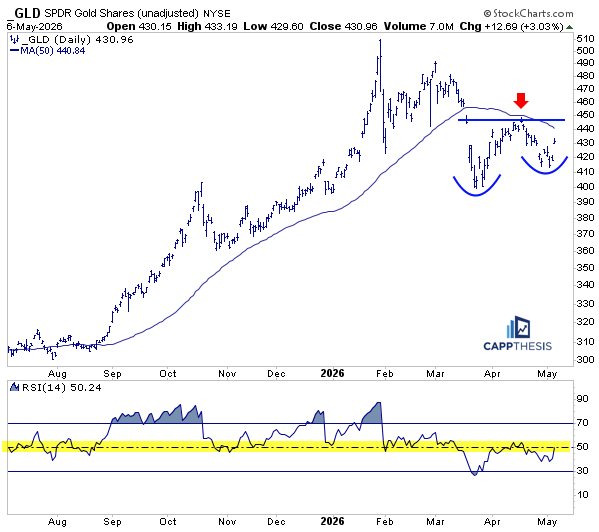

- Ryan Detrick, CMT@RyanDetrick – May 7 – A lot of bears on gold it feels like, but @FrankCappelleri noted a potential positive pattern in his note this morning. 🥇

Now to the most important commodity of them all, at least at this time:

John Kolovos said to Mike Santoli on Thursday:

- “Oil right now is sideways; … long term I think Oil is in a secular advance; goes to $150-$200 over the next couple of years … but right now it is consolidating, moving sideways“

Time is running short as experts say & as even simple folks like us think. After all, it reportedly takes about 3 months for oil to start flowing in a gush AFTER a deal is reached. Below are two expert opinions:

First Jeff Currie, previous Head of Commodities at Goldman Sachs & now at Carlyle, who says “US Oil Storage Tanks to Run Empty Around July 4“:

Then a more kinda provocative & even semi-humorous at times clip from Amos Hochstein, Former Middle East Senior Advisor, who says “We’re Going Towards a Cliff on Oil“

2.5 – International Stocks:

- EEM up 5.9%; FXI up 1.2%; KWEB up 2.7%; EWZ down 79 bps; EWY up 17.4%; EWG up 76 bps; INDA up 1.5%; INDY up 32 bps; EPI up 92 bps; SMIN up 4.2%;

The most important & clearly the most visible international event this week is the Trump-Xi meeting in Beijing. Look how Danny Russel, Former Assistant Secretary of State for East Asia, positioned it in this morning’s hot off Bloomberg Servers clip

- The overhang from the Iran, mess is immense when it comes to the, Trump Xi summit. You know, when you think about it, Donald Trump had intended to arrive in Beijing as the conquering hero with decisive victory over Iran under his belt. And instead, what the Chinese are seeing, as as your correspondent Wendy pointed out, is a picture of American vulnerability, American overstretched, you know, tactical military brilliance, but strategic incompetence, frankly. And look. The you know, the Chinese are good at math. It’s not only Iran. It’s Iran plus the legal rulings against the tariffs, plus the soaring gas prices, you know, plus the declining poll numbers in an election year so that all this adds up to leverage for Beijing.

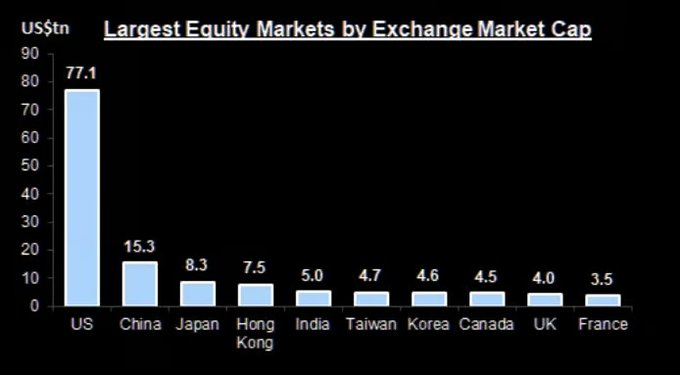

Now change your focus from “largest equity markets” to more geopolitical impact and observe how Japan, India, Taiwan, Korea ( & now Vietnam) are increasing coming closer in their fear of & opposition to China. And that is assuming this bloc doesn’t get closer to US.

2.6 Treasuries & Interest Rates:

- 30-year Treasury yield down 2.1 bps on the week; 20-yr yield down 2.5 bps; 10-yr down 1.4 bps; 7-yr down 1.5 bps; 5-yr down 0.8 bps; 3-yr up 0.5 bps; 2-yr up 0.5 bps; 1-yr up 2.5 bps;

- TLT up 55 bps; EDV up 74 bps ; ZROZ up 83 bps; HYG up 10 bps; JNK up 12 bps;

What gives? Treasury yields fell on 3 of the 5 market days this week, mainly on concerns about the economy & of the Lower K of people. As David Rosenberg wrote in this recap:

- ” … the consumer is cracking in plain sight. Disney reported a rare decline in theme park attendance — a real-time bellwether for consumer confidence — even as gasoline prices have climbed +53% since the war began. The stock market doesn’t seem to care: the Philadelphia Semiconductor Index just posted its largest 25-day rally since the dot-com bubble peak in March 2000.”

- “The question remains: how long can a market carried by AI capex and chips mania ignore an economy where 72% of GDP is contracting?“

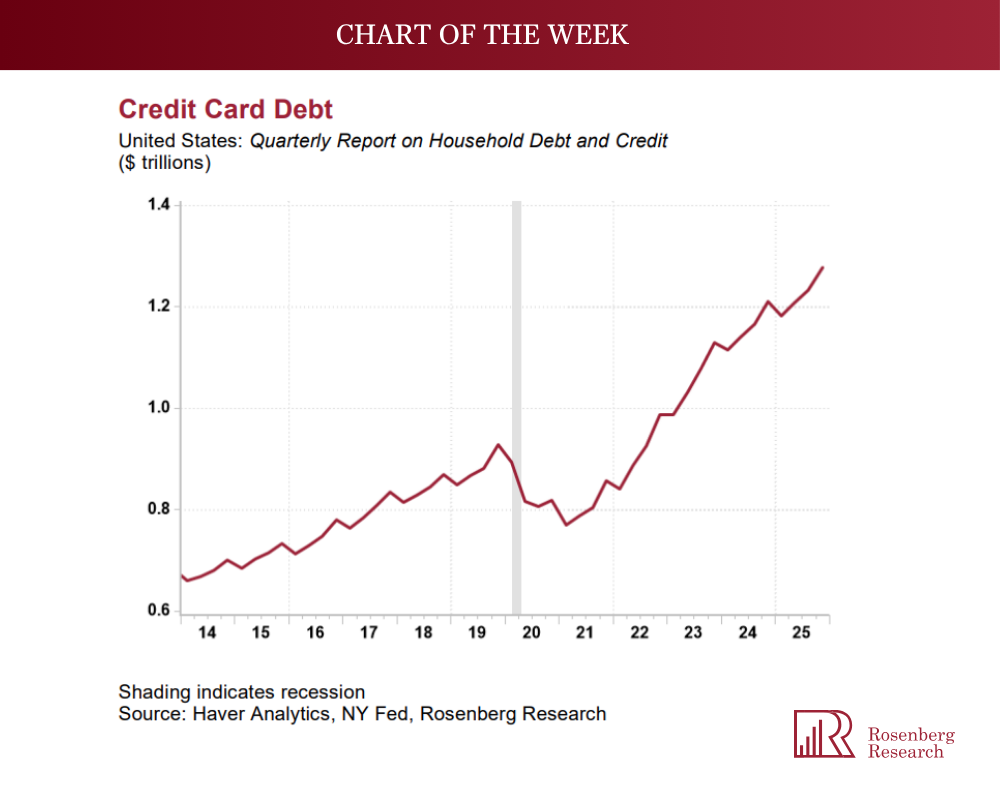

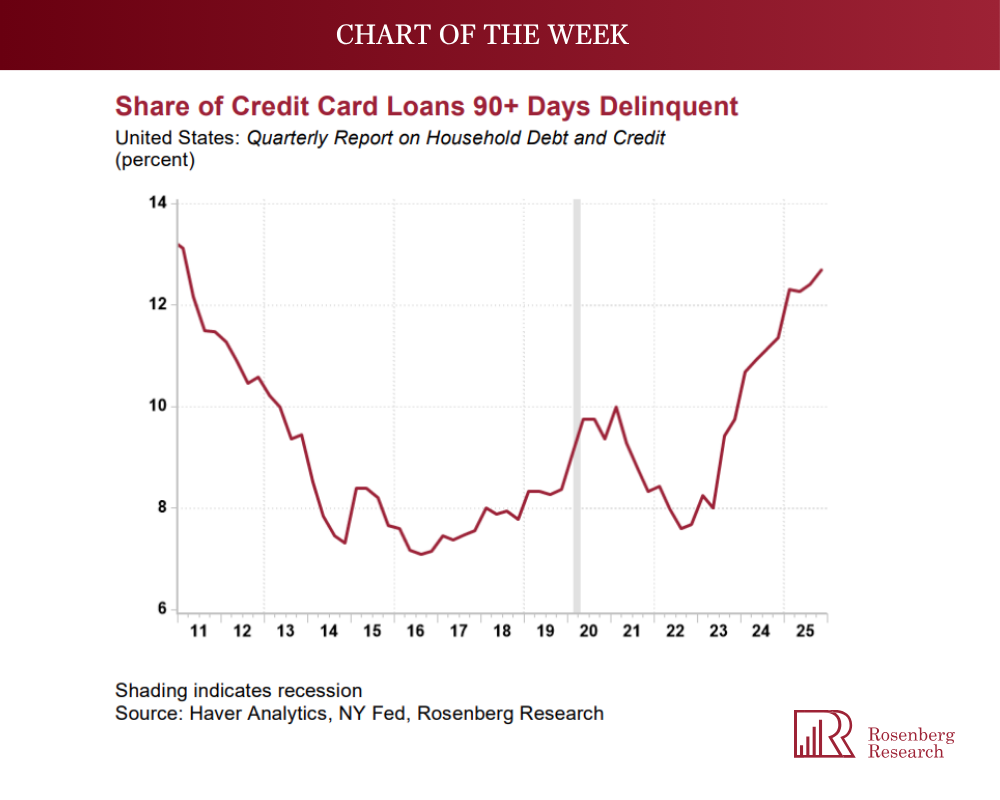

And Rosenberg posted two charts regarding the financing available to the Lower K:

What is his summary you ask? Allow us to suggest that you have a swallow of whatever beverage you reach for when you are feeling kinda depressed & then read his summary:

- “Besides the weather and the AI spending binge, the primary source of stimulus for the U.S. economy over the past year has been the sharp decline in the personal savings rate from over 5.0% to 3.6%. Barring that effect, real consumer spending would be running flat right now instead of +2% on a YoY basis. The reasons? The equity bull market rally, which has made the high-end feel richer and more willing to spend more out of their after-tax income; and for the low-end, the ability to continue to tap their credit cards to stay intact, even though the delinquency rate on this form of household debt has soared to a fifteen-year high of 12.7% from 11.4% a year ago and 9.7% two years back. It really says a whole lot about the fragility beneath the surface when credit card default rates are higher today than they were in the third quarter of 2008 (9.5%) when Lehman collapsed, and the Great Financial Crisis entered a new and sinister chapter.“

May we repeat the question we have asked for years without getting an answer? Who in Heaven’s Name, gave him a nickname analogous to Rosy?

Can we mention “credit” above without at least touching on “private credit”? Yes, we saw high-branded funds cutting the valuations of their portfolio by a non-trivial amount. For those who care, allow us to insert here a clip of the man who first introduced CNBC viewers to the state of Private Credit a few months ago. The same man spoke at length on Bloomberg Podcasts this week. Even if you pooh-pooh the warnings of such “smart” folks, listening to the clip below might be helpful. We won’t say “Enjoy” but do repeat the smarts of sipping your favorite drink as you listen:

Gundlach suggests that the US Government might actually cut the Coupons on existing Treasuries to about 1% & thereby save a humongous amount of money. Gundlach believes that the prices of Long Maturity Treasuries would plummet. On the other hand, David Rosenberg is on record saying the yields on long maturity Treasuries would first collapse. So listen to both & choose your poison.

But there is another smart mind who says weird but comforting stuff that actually will make you smile. Allow us to list some of his quotes before we reveal his name & post his clip for all readers to watch & listen:

- “The difference in the technicals and the equity market and the bond market are as diverse as you can as imagine.”

-

“we don’t create enough stocks. We’re you know, the buyback relative to the issuance of equities. People talk to the IPO market. It’s tiny relative to the buyback market. We don’t create enough equities, and there’s a huge amount of cash out there. So you just get this continued buying, and then there’s no stock. … In bonds, we’re getting 520,000,000,000 a week of trade of gross supply of treasuries. “

- “The other is we’re witnessing a growth paradigm that is unbelievable. That is I mean, I think this year, you can grow 6% nominal GDP after a number of years of significantly positive nominal growth. And then you see this in the earnings numbers that are coming out. I’ve been pretty blown away by not just that you have top line revenue that’s impressive, but you have pricing power. Pricing power is the worst thing you can have for the bond market because, obviously, what it means from inflation side. So I think it can persist…. equities have a whole lot more upside than the than quite frankly interest rates do today“

- ” the strength that we’re still seeing through … in corporate earnings when it comes to equities, I mean, I have to imagine that translates to the performance of the credits as well. …. So, I mean, it’s pretty hard and people say, you know, I don’t like these spreads at these levels. That being said, the yield fits portfolios, not just our portfolios, but with your pension fund, life insurance company, any insurance company, etcetera. The yields are very attractive because the risk free rate is high because central banks are keeping it there for inflation. So those yields are interesting. It keeps demand at a pretty at a at a great pace.”

- People talk about private credit. They’re stressed in private credit. When the economy’s growing at 6% nominal or let’s say I’m wrong and it grows at low to mid fives, it’s pretty hard to have a default cycle of any significance. I’ve learned over my career, cash flow makes up for a lot of mistakes. And as long as you have that sort of backbone of cash flow growth, you’re not gonna have any significant default cycle.

But what about the economy?

- “Is that the the issue? …. I’ve I’ve been pretty adamant about this. You have a lot of The US economy. It’s actually in recession. Yeah. And part of why I’ve been a believer that even if you grow this fast, Fed can cut rates. The reason why I think they can is because what is rate sensitive in the economy today is actually in recession. So you think about traditional manufacturing, you think about housing, you think about where young people, low income people that are struggling, and that’s where the interest rate tool is effective.”

- “… you have two parts of the engine that are steaming ahead. …. Certainly, on a short term basis, it’s huge. And then you’ve got consumption that’s coming from the higher income cohort …. That’s keeping it up. So you’ve got an economy that’s doing extremely well “.

- “And then, by the way, for a lot of people in the country Yeah, It’s actually not going so well. And so …. I think you’ll see a Fed that will cut rates because of that part that’s really going.”

- “.… this AI, the technology boom, is we’re gonna see a productivity revolution that nobody’s ever seen before. I mean, many companies including yesterday are announcing growth, CapEx spend, and we don’t need as many people. Part of why I’m not that worked up about inflation over the over the intermediate term. Certainly, over the near term, we’ve got a transmission from a variety of things, fuel being the number one. But I think productivity and employment are gonna change, and I I worry about and I’ve not heard anybody give me a good reason why in the short term, the transition in terms of employment is not a difficult one.”

Then he went to where we have been living for about a year & half – the need to have a forward-looking brain & mind-set & not the traditional Fed-backward-looking brain & mindset. He used the Gretzsky analogy for focus & simplicity.

- “The one thing that I think will be different in terms of Fed perspective Yeah. I think you have to be more prospective about where the puck is going Right. Versus where we’ve been historic and the historic analogs don’t really work in what is a new era. …. I think the transition we’re talking about a it’s certainly a couple of years. I mean, it’s pretty hard to project how the the world changes, industries that grow relative to this. But for the next couple of years, some big industries, I always talk about driving and some others that employ a lot of people. Mhmm. That transition, that retraining is gonna be and the size that it’s happening and the speed it’s happening at will be dislocating certainly for a couple of years. By the way, I would argue at the same time, we have a debt burden in the country that that is compounding higher. …. I think this Fed will do a great job. But I think the key is gonna be, are they prospective about where we’re going and about what the new challenges are versus the analogs from history that aren’t as relevant.”

- “The Fed’s objective is to create full employment and price stability. It’s not to make sure the markets feel good about what you’re doing at every meeting. And I actually think having a a lower level of forward guidance, particularly when you’re easing. When you’re easing to tell the world, like, we may go 25 every six weeks, I don’t think is actually that robust. If you if you kept your cards to your vest and said, okay. Now I gotta shock the system because I’m trying to execute change. I’m trying to get financial velocity moving. I actually think lower and, you know, is do the markets feel like, gosh, it’s a little bit more uncertain and the increased vol volatility and so on? Maybe at the margin. But as long as you’re effective on communication as to the metrics you’re looking at, this is what we’re pivoting off of so the markets understand.”

- “The long end of the yield curve, interesting. I’m getting my long curated assets through equities or a lot of people are doing that, and my other portfolios are doing a ton of that. And say, gosh, I don’t need the thrill of the back end of the curve moving around. Yeah. So I’d rather stay in the front of the belly of the yield curve. …. I will say people don’t realize that 89% of the treasury’s debts in the zero to two year part of the curve. Don’t actually have that much debt when you take what’s net of the Fed’s balance sheet.”

- “So the reason why people get in the steepener trades and I actually think fundamentally the curve could steepen. The technicals are actually keep that from happening. So listen. I think if you said to me, where are we going in six months, a year from now, we have to get the mortgage rate down in this country. And do I think the back end can stay contained? I think so. My view is, like, putting on steepeners and flatteners, hard to make money on that to your point. But listen. I think the ten year is gonna get down to 4%.”

- “I think what will be the catalyzing influence is when you start to see real motivation around the mortgage rate coming down and some and by the way, I think there’s some fiscal initiatives that can bring rate down and mortgage rates down. But once you start to see that, then I think it’s gonna be then it’s in place where we start to go out the yield curve. I will say we run optimizers on our portfolios. These real rates out the curve … are pretty attractive. I just think today, you’ve got some inflation coursing its way through the system. You’ve got a more … an alternative asset, i.e.. Equities. It’s a better long curated asset. But my sense is that we’ll get a chance over the next few months to to start to to start to go out the curve more aggressively.”

3. India-USA-SEAsia

Something big & unprecedented happened in India this week. And it can realistically by termed as politically “Dhurandar”. BJP, the ruling party in India, won a huge victory in a state that it has never won before. Not just any state, but the first state that accepted control of the British East India Company in 1757. It was the state that was broken into two by the British before exiting India. It was the state that led to the breakup of NaPakistan in 1971 & then kept becoming a radically violent Muslim state. A state, whose Hindu majority which, despite all of that, refused to blend in to India wholeheartedly.

This state of Bengal in a huge wave joined the BJP wave in India & delivered a spectacular victory to PM Modi. It was a landmark victory that will prove more everlasting than the 1971 victory. And PM Modi in true humble & Indian style performed a Dand-Vat to the crowd that had come to hear his victory speech. Watch his vandan (reverance) for the people of Bengal in true Indian tradition (between 30 & 39 seconds of the clip below).

This was so huge that anti-Hindu media BBC, NY Times, Washington Post, Guardian praised this victory of PM Modi.

Now look why this victory is of geo-economic significance for India.

Between the Indian State of Bengal and the states of North-East India lies (in white) Bangla-Desh, the Muslim “country” which was liberated by the Indian Army in 1971 from Pakistan which had killed 5 million Bangladeshis then. Bangladesh remains destitute with desperately poor 177 million Muslims.

Now with Bengal becoming 100% Indian, the risk from BanglaDesh is reduced substantially and you will see the North-Eastern states become much more integrated via roads & rail. This is critical because the North-Eastern states border Chinese-occupied Tibet & Myanmar.

At the same time, the southern state of Tamil Nadu (green in the map above with Chennai as its capital) , the 2nd state taken by the British East India Company, also overthrew its anti-Hindu local party, so anti-Hindu that its Chief Minister had changed his name to Stalin (yes, the Russian dictator) to publicize his anti-Hindu conviction. Frankly, he had done well for the State but that was not enough. A new young leader won the largest number of votes in a 3-party contest.

Tamil Nadu is the closest state to the Malacca Straits and NE-India backed by Bengal is adjacent to Eastern Tibet, Myanmar. Now India’s neighbors know that the border states of India are 100% Indian & that changes their “power”-perspective of India.

Now go back to Section 3.2, titled Enter South Korea, Japan & Germany, of our article dated April 26, 2026. That section covered the 1st ever visit by South Korea’s President to India for a detailed, ambitious & long-term industrial-military relationship with India. It also covered the beginning of a new industrial-defense relationship initiated by PM Takaichi-San of Japan.

Now look at the map below. With a beginning of a nascent defense relationship with Japan & a defense-relationship with South Korea, India has now begun a naval presence in the Sea of Japan.

As you enter South China Sea from above, you see Philippines on one side and Vietnam on the other. Well, Philippines has been an early buyer of Brahmos missiles from India for its naval defense. That’s good but what about Vietnam, a state with a military reputation and a successful defender of a Chinese attack in 1979.

Since you bring it up, we must report that Vietnamese President and General Secretary To Lam visited New Delhi this past week (May 5- May 7). It was treated with due pomp & respect by the Indian Government. It seems that, apart from normal trade discussion, the underlying reason was naval defense of Vietnam. It seems, according to the 9-minute clip below, that purchase of Brahmos missiles by Vietnam was a core underlying reason for the trip.

We could be wrong but the above does relate to the US-China meeting scheduled for this week. Defense of South China Sea is a major US goal and that too in co-operation with US allies like Japan, South Korea Philippines. In that context, a strong & beneficial defense relationship between these US Allies & India is a positive for America.

That brings us to America-India relationship. But doesn’t US prefer private ventures instead of Govt-to-Govt deals? Indeed & that brings us to this week’s launch of the world’s 1st ever OptoSar 196 lb. satellite by a Benguluru-based startup named Galaxye .

- OptoSAR is the world’s first hybrid satellite technology combining Synthetic Aperture Radar (SAR) and Optical (multispectral) sensors on a single platform, launched by Indian startup GalaxEye Space on May 3, 2026, via SpaceX.

And, as of May 8, Galaxeye announced that OptoSAR satellite ‘Drishti’ is alive and kicking in orbit. The linked article provides a detailed description of the capabilities of the satellite. Galaxeye has plans to launch a constellation of 8 more OptoSar satellites to cover all of India.

Think an Indian graduate of IIT-Madras & his team designed the 1st ever OptoSar satellite, got the financing to build it themselves & then launch it successfully using the world’s largest launcher of SpaceX. Listen to the young CEO Suyash Sen speaking to NDTV before the launch:

This sector is not only the preserve of IIT graduates. Check out Skyroot Aerospace, the startup founded by two former scientists and engineers from Indian Space Research Organisation (ISRO), Pawan Kumar Chandana and Naga Bharath Daka:

- Skyroot Aerospace, the Hyderabad-based space startup, has raised nearly $60 million in fresh funding just weeks before the launch of Vikram-1, the country’s first privately developed orbital rocket, and has now become India’s first space-tech unicorn, reaching a valuation of around $1.1 billion.

That’s all fine & dandy. But if India has so much money, how about investing that in America? Guess what we found out this week from US Ambassador Sergio Gor?

- “Indian companies are planning to invest $20.5 billion in the US, spanning sectors like tech, manufacturing and pharma. The update, shared by Sergio Gor, includes $1.1 billion already announced by 12 firms. The move signals growing momentum in India–US business ties, as both countries aim to scale trade to $500 billion by 2030.”

By the way, the above is all this week’s news. If that doesn’t indicate the trajectory of US-India business relationship, what would?

The above also answers the question why India-ETFs which trade in the USA are performing so weakly. Look at portfolio holdings of $INDY, the huge BlackRock ETF that tracks the Nifty 50 index. About 50% of the Fund is in companies like HDFC Bank, ICICI Bank, State Bank of India, Reliance Industries, Larsen & Toubro. These are mature companies that are subject to the wrong factors. Not even large companies in high growth sectors are in these ETFs. Not even Adani Ports, the stock that is up 20% in a month because of their giant new MegaShipment port that has 100 ships waiting to enter for delivering mega-size cargo containers. Not even HAL, the military manufacturer of fighter planes & other large defense equipment that is being delivered to Asian countries.

Why can’t BlackRock or other such entities launch ETFs that focus in high-growth Indian companies in Technology, Communications, Defense Equipment & other high growth areas?

Going back to our core theme, what happened in Bengal this week was pure “Dhurandhar”. Not necessarily the film but the enormous waking up in Indians that was first portrayed in the film Dhurandhar. That us the same waking up that led to PM Modi’s unprecedented victory in Bengal.

And guess what? The film Dhurandhar is now going to Japan.

Seriously TV & Media executives – Ban all your reporters, correspondents from saying or writing even a syllable about India without watching both Dhurandhar 1 & Dhurandhar 2. Without that, they would remain totally Brit-servile & utterly ignorant.

What’s the difference between Dhurandhar 1 & Dhurandhar 2? Watch the early song from each & figure it out yourselves:

Got it?

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on X.