Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Bottom-type calls on stocks this past week

The one from Ed Yardeni was not just a bottom-type call, but an explicit call that Monday 3-30 was the Bottom as Yardeni said on CNBC on Thursday, April 2. His target for this year is 7,700. He said the “obvious way out is for the President to declare we have won & get out” and added “that is what he did last night“.

When asked if the tech comeback has legs, Yardeni said “absolutely” and added “tech got cheap, relatively cheap again… Mag 7 PE has gone done from 31 down to 25, actually went down to 22 in the last couple of days; Mag 7 also got relatively cheap“

Than on Saturday, 4th of April, we noticed a clip on YouTube titled “Ed Yardeni: “The Market Bottom Is In” – Now’s The Best Time To Get In Before A Massive 2026 Rally“. This 10-minute clip listed 3 stocks as Mr. Yardeni’s favorites. Those, assuming the clip is an accurate communicator of Yardeni’s opinion, are Micron (MU), Taiwan Semiconductor (TSM) & Microchip (MCHP). This brings us to a suggestion that CNBC should not let a guest leave their show without giving 1-3 favorites. That was the dictum of the late Louis Rukeyser & it served him & his viewers well.

Then we heard HSBC’s Max Kettner come on CNBC On Thursday afternoon to say that “markets are seeing the biggest buy signal since the liberation day sell-off“. But, in clearly what must be our fault, we simply could not pin down what this specific signal was from his statements. For example, we heard:

- “we are seeing that things like survey-based sentiment, things like hedging demand in equities, are very very high; we are seeing things like technicals, relative strength around credit, around commodities, as really, really weak “

These sound like the statements about current conditions instead of a signal. Especially when he added “we haven’t reached the extremes in terms of the bearish positioning, bearish sentiment like we had in April 2025“.

In contrast, the 3rd call we cover is explicitly simple & focused. It is a call on a “woeful under-weight” of investors in “pro-inflation assets“. And it is so when there is a kinda secular change going on. This is the opinion of Rich Bernstein whose firm was purchased by Janus Henderson recently. Bernstein told CNBC’s Santoli that he thinks the US economy and markets are in an environment similar to the mid-1960s where fiscal policy was referred to as Guns & Butter. Guns referred to the buildup for the Vietnam War while Butter referred to a focus on social spending towards buildup to a Great Society. In this environment, Bernstein said dividends become very very important because they are giving you more of your total return upfront. This is also a relative-return bottom call which may prove profitable.

2. Markets This Week

2.1 US Indices:

- VIX down 23.3% to 31.13; Dow up 3%; SPX up 3.4%; RSP up 2.5%; NDX up 4%; SMH up 4.8%; RUT up 3.3%; MDY up 3.1%; XLU up 1.7%;

To begin with:

- Trader Z@angrybear168 – Thu 4-2 – Market is detaching from the negative correlation to oil today.

And the fuel seems ready:

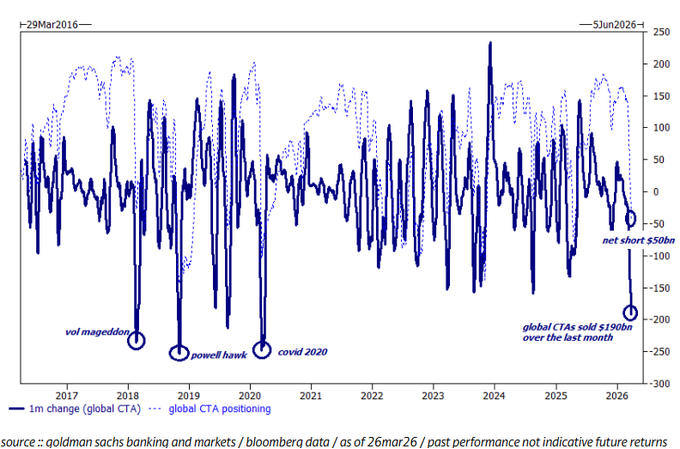

- zerohedge@zerohedge – how short are CTAs

A washout?

Seth Golden@SethCL – 4-4 – Sentiment washout; • Buy Signal Triggered: Extreme pessimism has triggered a rare Optix buy signal ; • High-Probability Setup: When paired with a Composite Washout Model reading ≥ 22%, this setup historically boasts an 87% win rate over a 3-mnth time frame $SPX $XLK $AAPL $SMH $NVDA $MSFT $IGV $PANW $PLTR $QQQ $NDX h/t

@sentimentrader

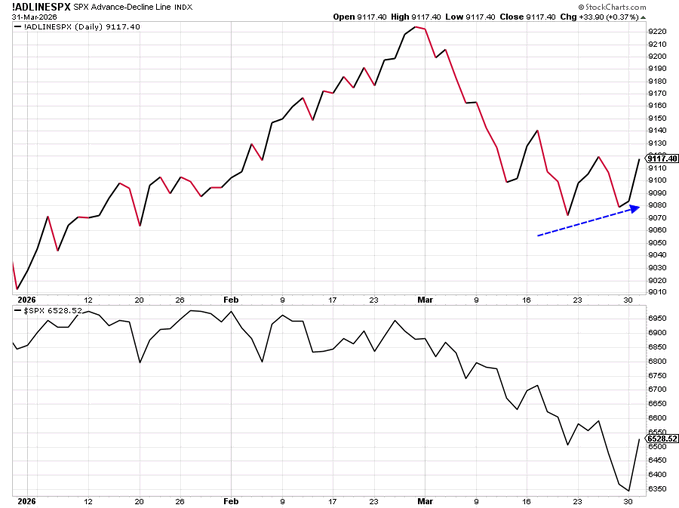

And a positive divergence:

- Ryan Detrick, CMT@RyanDetrick – Breadth didn’t break to new lows with price. Here’s the S&P 500 A/D line sporting a positive divergence with price.

2.2 MAG 7:

- AAPL up 2.9%; AMZN up 5.2%; GOOGL up 7.8%; META up 9.3%; MSFT up 1.8%; NFLX up 3.3%; NVDA up 5.9%; MU up 2.5%;

2.3 Key Financials:

- BAC up 5.1%; C up 7.3%; GS up 7.5%; JPM up 4.2%; KRE up 4.2%; EUFN up 6%; SCHW up 1.5%; APO down 1.3%; BX up 4.6%; KKR up 3.1%; XHB up 1.8%; ITB up 1.5%; NAIL up 3.8%;

2.4 – Dollar & Metals

Dollar was up 7 bps on UUP & down 10 bps on DXY:

- Gold up 4.3%; GDX up 10.3%; Silver up 4.2%; Copper up 3%; CLF up 3.6%; FCX up 9.1%; MOS up 4.7%; Oil up 12%; Brent down 4%; OIH down 4.1%; XLE down 5.3%;

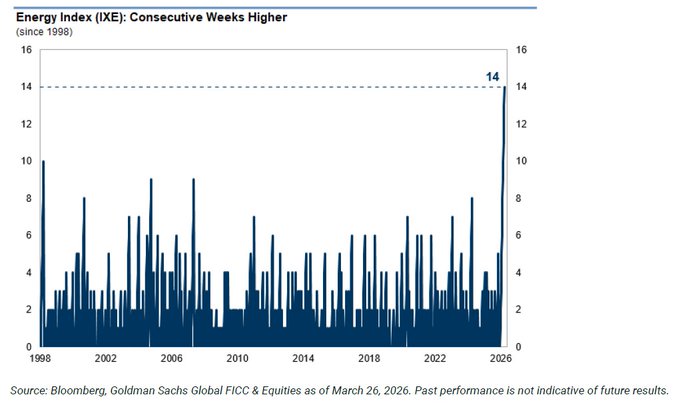

Unheard of?

- zerohedge@zerohedge – The energy index is up 14 weeks in a row. This is unheard of

And,

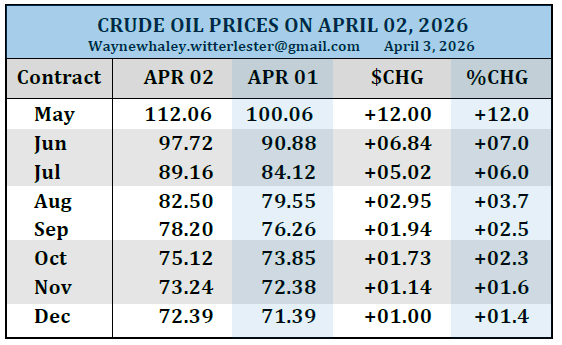

- Wayne Whaley@WayneWhaley1136 – Fri 4-3 – THE CURRENT CRUDE OIL BACKWARDATION & THE S&P

- On April 2, May Crude closed at $112.06, up $12.00/barrel from the prior days 100.06 level, a one day 12% advance.

- Unnoticed by most casual observers, the December contract was much less unnerved by President Trumps negotiation rhetoric the prior night than was the more News sensitive spot contract and closed up only $1.0, closing at $72.39, a more tepid 1.4% advance remaining in the general vicinity at which it began 2026.

- If you review the closing prices on April 2 across the monthly Crude Oil contracts over the remaining year, the trend suggest that traders, recognize that there hasn’t been a strutural change in the supply/demand relationship that contributes to the long term anticipated price of Oil and that for now, we simply have an event driven, short term inability to get some 20% of the Oil in transit each day from the supply points to the demand points in as efficient of a manner as coveted.

- The dramatic backwardation in the data displayed in the table below would suggest that traders aren’t betting on a prolonged 1970’s style Oil crisis or a permanent shift in fundamentals.

- The curvature of the data is essentially saying: Pay up for barrels right now because of the immediate geopolitical risk premium but by mid year or December at the latest, we anticipate Oil will be floating freely across the ocean again and priced back to something closer to a balanced market in the $70s.

- This backwardation in Oil prices is one of the reasons, equity prices, as reflected by the S&P index, have shown much resilience in the first Quarter of 2026 despite the +50% Oil spike with the S&P now only down 3.84% for the year and 5.67% off its Jan 27 High.

- The equity market is reading the same tea leaves as the oil pit, that being one of a message that the energy shock looks to be likely of a transitory nature.

2.5 – International Stocks:

- EEM up 2.5%; FXI up 2%; KWEB up 64 bps; EWZ up 4.7%; EWY up 1.6%; EWG up 4.8%; INDA up 1.8%; INDY up 2.1%; EPI up 2.4%; SMIN up 3.1%;

4.6 Treasuries & Interest Rates:

- 30-year Treasury yield down 6.7 bps on the week; 20-yr yield down 12 bps; 10-yr down 12.9 bps; 7-yr down 12.8 bps; 5-yr down 11.7 bps; 3-yr down 10.4 bps; 2-yr down 10.6 bps; 1-yr down 9.3 bps; (these levels are post-Up surprise of 178K jobs on Friday)

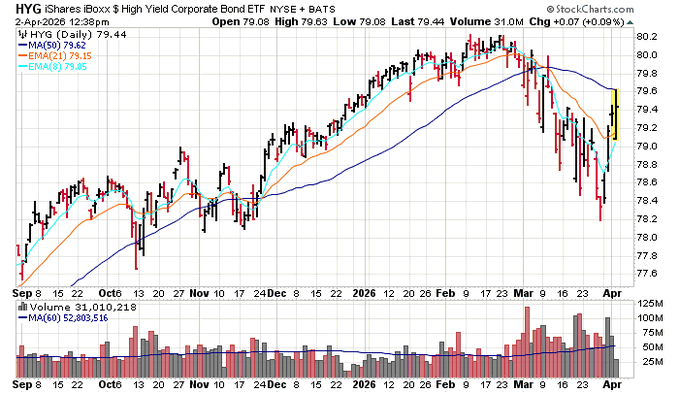

- (as of Thursday close) TLT up 1.3%; EDV up 1.2% ; ZROZ up 1%s; HYG up 1.1%; JNK up 1.1%;

Encouraging?

- Jason Leavitt, LeavittBrothers.com@JasonLeavitt – Apr 2 – I consider it encouraging $JNK and $HYG have bounced so much.

The Jobs number came in on Friday morning at + 178,000 but with revisions. Who better to explain it than the R-man himself?

We heard something on Wednesday, April 1 that we have not heard before. We heard Morgan Stanley’s Ellen Zentner say to Tom Keene “I think the probability of recession here is higher than people think. And I would put it around 40%, which is meaningful. It’s uncomfortable.”

After Zentner, we saw Jeffrey Gundlach tweet “It’s 2007 for Private Credit.“. He may have meant in bearishly but, from an equity perspective, it seems bullish to us. Anyone who sold stocks in April 2007 left quite a bit on the table. The high for that cycle came in October 2007, as we recall.

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on X.