Editor’s Note: In this series of articles, we include important or interesting videoclips with our comments. This is an article that expresses our personal opinions about comments made on Television and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. What a difference one day makes!

The morning of Thursday, January 10 was bright and cheerful thanks to a “back to 1997 economy” type number in the Challenger layoffs report. Read the conversation between John Challenger & CNBC’s Steve Liesman:

- Liesman – “these are mid-1990s employment numbers here..”

- Challenger – “if I were a Keynesian, I could be telling the government and the Fed to get its foot off the gas pedal right now, not go into 2014 with a sense we’re still going to keep stimulus going, hoping that unemployment will go down even further. this engine is really rolling. …. there are many sectors of the economy right now that are adding jobs.”

David Rosenberg tweeted his own delight a few hours later:

- Gluskin Sheff @GluskinSheffInc – David Rosenberg: “Challenger layoffs down to 13-year low…imagine if a hiring cycle ever takes hold!”

The only folks who thought differently were the buyers of the 30-year auction on Thursday. Santelli gave it an A- rating and yields across the Treasury curve fell a bit on Thursday afternoon. They must have thrown a party on Friday evening.

Because the mood on Friday morning was dramatically different. The Non-farm payroll number printed at 74,000 much lower than the lowest prediction of 100K on the street. A puzzled & worried El-Erian said to BTV’s Betty Liu:

- “It is very surprising. It is somewhere between puzzling and worrisome. Puzzling because it is such a strange number – the 74,000 jobs that were created — even if you add in the revisions from last month. It is still half of what consensus was, and it is inconsistent with lots of other data. But it is also worrisome and I think we have to remember that. Because if you look within the report, you get some pretty worrisome things in terms of what is happening to labor participation. We’re back to levels that we haven’t seen since February ’78. Long-term unemployment still stuck 37%. So we’re going to learn a lot more about what is the impact of the weather, how much of this is real, how much of this is temporary. It is a shocker, to put it mildly“

Larry McDonald had a different take when he spoke on CNBC Closing Bell on Friday afternoon:

- “the worst thing that’s going on, France’s labor force participation rate is 55.9. we’re on a collision course with France. it’s really a perfect storm. you have got technology, you’ve got an aging population, and you’ve got big government. That perfect storm is putting this labor force participation rate on a collision course with France”

His tweet from Friday morning tells the story better:

- Lawrence McDonald @Convertbond – The Road to France– pic.twitter.com/QOYnSZbJEn

2. Questions about Taper again?

There we go again…. a subject that markets had thought was closed seemed not so closed after the jobs number. The market had priced in at least $10 billion of further taper at each Fed meetings and the final end to QE by the end of 2014. Both Greg Ip and Jon Hilsenrath opined that this one weak number would not force the Fed to refrain from reducing QE by another $10 billion in the January 28 FOMC meeting. BlackRock’s Rick Rieder also agreed. So did Paul Richards of UBS who said on CNBC FM 1/2:

- “I don’t think one number makes a trend. the Fed does nothing. they continue to do what they did. they started tapering. They do another 10 billion. steady as she goes; this is a consistent Fed.”

Larry McDonald was one exception. His view is that the Fed will extend its QE into 2015. We don’t have his exact quote because CNBC webmasters in their infinitely sound judgements usually cut off his comments from their clips. May be, because McDonald is usually negative?

The markets seemed to concur with Larry McDonald. Everything that should rally on the expectations of a slower taper rallied – EM was up 1.5%-3% big outperformance vs 23bps in S&P; Gold & Sliver were up 1.5% & 2.75%. Treasury yields fell dramatically and Muni closed end funds roared. Even the US indices rallied after an initial decline to close modestly up.

But CNBC Fast Money gang gave up a big thumbs down to these moves suggesting Shorting EM, Shorting Gold and shorting any prospect of a smaller taper. The sole exception was Guy Adami who pointed to terrible numbers from retail companies and spoke of a chasm between real economy & the stock market.

3. The number stays the number until the next number?

The jobs number was such an outlier that it was dismissed by many economists & traders. But BlackRock’s Rick Rieder made the following empirical observation on CNBC FM 1/2:

- “I think you have to reflect though the fact that the number was weaker. For the next month the number is going to be [the number] until we get to the next number. it’s a weaker number.”

The same point was made via a chart on Friday morning:

- Vconomics @Vconomics – Market direction usually gets decided post-NFP (white arrows signify a continuation of an uptrend or a bottom) $SPY pic.twitter.com/395jL20sew

4. Treasury Yield Curve

Since the taper talk began in May 2013, the action in the Treasury market has been asymmetric, to use a Rick Santelli expression. The rise in Treasury yields on strong data was much greater than the fall in Treasury yields on weak data. Has this pattern reversed?

- The Treasury market was hit with two surprises this week – a much stronger than expected ADP report of +238K on Wednesday and a much weaker than expected jobs number of +74K on Friday. On Wednesday, the 5-year yield jumped by 9.4bps & on Friday, the 5-year yield fell by 13bps. On Wednesday, the 30-year yield rose by 2bps & on Friday, the 30-year yield fell by 8.3bps.

James Rickards told BTV’s Market Makers that the “Fed was tapering into a weakening economy”. The market isn’t saying anything as explicit but its new asymmetric action does veer towards this non-consensus viewpoint.

The action in the yield curve is asymmetric as well. On strong data, the yield curve tends to flatten more than it steepens on weak data. This fits what Ken Volpert of Vanguard said on CNBC Street Signs on Wednesday:

- “I think the 10-year is actually in a pretty good spot; you have got a real interest rate of about 70bps right now; where I think there is real vulnerability is actually at the shorter end of the curve ; probably between 2 & 5 years; if the numbers continue to come in stronger, it will push closer concern about Fed raising interest rates & the shorter end will probably take a hit more; the intermediate part will probably weaken as well; but 70bps when you have an economy still growing at a fairly slow rate is a reasonable interest rate already; I don’t think 10 years have a lot further to go;”

David Rosenberg also focused on the yield curve in his conversation with CNBC’s Brian Sullivan:

- “question isn’t interest rates, question is the yield curve .. it is actually the interplay between the short term and long term rates that matter for the economic activity and stock markets… it is really about the yield curve… a steepening yield curve is usually commensurate with stronger growth, robust liquidity conditions & a stronger stock market.. it is really when you start getting short term interest rates rising more than the long term interest rates and the yield curve flattens that you go into trouble…. go back to 1994,… decent year for the economy but a flat year for the stock market… and that is because the Fed flattened the yield curve … so short term rates under Janet Yellen are not gonna go up for a long period of time; long term rates will ebb and flow with how the economy does; I expect we will probably have even a further steepening of the yield curve going forward “

That is not how 2014 is playing out. The curve is getting flatter not steeper. Of course, 10 days don’t make a real trend. But Chairwoman Yellen is just as aware of the negatives of a flatter yield curve. So if this trend continues for awhile, her FOMC meetings will become more interesting.

David Rosenberg‘s predictions for 2014 are really a must read in our opinion. His three points are:

- Wage Inflation – “… to me, one of the big surprises for 2014 is going to be that we’re going to get some organic wage growth that will help underpin consumer spending.”

- Higher Bond Yields – “By the end of the year, the 10-year note yield will probably up to around 3.5%. … the secular 30-year bull market in Treasuries ended in July 2012. … In the next couple of years, we’ll be talking more like 5% Treasury note yields as opposed to even 3%. “

- Cap-ex cycling starting – “The decline of productivity growth to the extent now that it’s vanished is going to spur on the corporate sector to do something they haven’t done this cycle, which is to rebuild the capital stock. I think one of the surprises of the upcoming year is going to be that capital spending is going to accelerate.”

Veteran Ex-Merrill technician Walter Murphy tweeted after the close on Friday:

-

Walter Murphy @waltergmurphy –Nice reversal in yields

today. It broke the uptrend from the October low and may well also

indicate lower stock prices over the near term.

Bob Doll of Nuveen on Treasury yields & Munis:

- if we get 3% real growth, inflation of 1.5% perhaps heading towards 2%, we’re looking at 5% nominal growth. That is not consistent with Fed funds at zero. So I do think the debate between, if you will, the markets and the Fed will soon, may be not till second-half, come to how can you keep rates at zero for the foreseeable future.

- we think interest rates drift higher, but within that that Munis outperform Treasuries. Headlines on Puerto Rico and Detroit. Most states & local fundamentals are improving. It suggests to us that the spread, which is very wide, between Muni yieds on an after tax basis and Taxables will narrow.

Closed-end muni funds, our favorite asset class, has done very well this year. Our tracking basket of BlackRock, Nuveen & Pimco funds yields approx. 6.5% after all taxes & still trades at a discount to NAV.

5. U.S. Equities

We begin our survey with comments from one who was correctly bullish all through 2013, Bob Doll of Nuveen on CNBC Closing Bell:

- “markets have been easy; 2013 was straight up; that’s not normal; having a pullback of roughly 10% is a very normal occurrence in the context of a good year; my point to suggest this is going to be a very normal year, bumpier than last year.”

- I would argue short term the market does feel a little tired. … the advance decline line, the new high, new low list if I can be a technician for a minute and my guess is that could be part of the seeds that sow some sort of pull back of note.

David Rosenberg on CNBC Talking Numbers:

- “so rising bond yields by themselves are not by themselves negative for the stock market; the stock market is having problems now because it is technically overbought; you have over 60% bulls in the latest Intelligence Investor survey 40% bears – it is a sentiment valuation obstacles right now; until you start seeing the yield curve flatten, the stock market is going to have more of a tendency to go up than down“

Tom McClellan in his article Presidential Cycle Inverting?

- “On average, the SP500 peaks in July of the first year of a presidential term, and then spends the next 16 months chopping sideways to downward until the mid-term election. But the current market is ignoring instructions and just continuing higher, presumably in response to the Fed continuing its money-pumping into the banking system. What is the problem?”

- “More than just zigging upward when it is supposed to be zagging down, the market seems to be doing precisely the opposite of what the Presidential Cycle Pattern (PCP) says it should.”

- “I have seen the market make tops and bottoms early or late by a few days compared to the PCP, but I cannot recall seeing a complete inversion like what appears to be happening. In other words, we have a wholly irregular market right now that is not following the normal rules. It is instead following some other set of rules, and so extra caution is in order.”

Lawrence McMillan in his Friday summary:

- “Stocks have been fairly dull so far in 2014, but some movement is probably setting up soon. In summary, there are some overbought conditions (although no confirmed sell signals), but unless $SPX breaks down below support at 1810, and $VIX climbs above 14.50, this will remain a bull market“

An interesting tweet that caught our eye on Friday:

- Robert Kelley @robertknyc – This count on $IWM is working. I expect up toward 116.70 in wave (v) to put in a top, probably mid-week. pic.twitter.com/EUxWIJwbf1

6. Flows lead markets now?

Conventional wisdom says that individuals are idiots and their flows are to be taken as contrary indicator. But look what happened this week. According to Michael Hartnett of BAC-Merrill Lynch:

- Bond funds halt 5-week outflow streak with biggest inflows in 35 weeks

This was before Friday’s rally in bonds. The breakdown, per Hartnett, is as below:

- largest inflows to IG bond funds since May 2013

- largest inflows to Govie/Tsy in 18 weeks

- 3 straight weeks of inflows to HY bond funds

- 81 straight weeks of inflows to floating rate debt

- 34 straight weeks of outflows from MBS

- 15 straight weeks of outflows from Munis

- 15 straight weeks of outflows from EM debt;

He adds:

- 11 straight weeks of EM equity redemptions = longest outflow streak in 11 years! But note that EM outflows while persistent have not been deep, which explains why our EM Flow Trading Rule remains firmly in neutral territory, too soon for a contrarian “buy” signal.

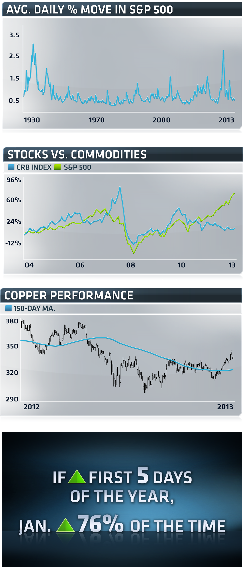

7. A chart for 2014

Carter Worth of CNBC Options Action had an interesting prediction for 2014 on 31st December 2013:

- so it’s the spread between a major asset class equities and commodities. you know commodities spike well above equities. now we have this equally impressive spike in terms of equities above commodities. The presumption is this cannot last. here’s the tell. the most important commodity all, copper, has all the hallmarks of an important head and shoulders bottom. here’s the neckline. this looks like it’s going meaningfully higher. what that suggests is that commodities actually outperform equities in 2014.

Another prediction is that volatility will be higher in 2014. The charts below are from the articles charts you need to see now on CNBC.om

8. Two gorgeous photos

This has no bearing on investing. But the photo is so lovely that we have to include it. It is a view from above of the highest point on earth – Everest. We found it being re-tweeted several times & have no idea where it originated.

Having posted one, why not a second – a reminder of this past week’s arctic chill

INCREDIBLE PHOTO: The American side of the Niagara Falls has frozen over today. @ChicagoPhotoSho pic.twitter.com/9Mm9oPjQJd

Send your feedback to [email protected] Or @MacroViewpoints on Twitter.