Summary – A weekly top-down review of interesting calls and comments made last week about monetary policy, economics, stocks, bonds & commodities.

Editor’s Note: In this series of articles, we include important or interesting tweets, articles, videoclips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

1. Sangfroid?

How else could we describe these financial markets? This week threw just about everything it could at the markets, a slightly more hawkish Yellen, big technology partnership between old & new Tech, major media buyout offer, shooting down an airliner & a Russia-US/EU crisis, an Israeli ground incursion into Gaza – yet, by the end of the week, the markets were mostly unchanged. The major trends of the year continued softly – large cap indices up a bit, small caps down a bit; yield curves flattened a bit more, VIX flat for the week. The market’s sangfroid state was shared by Lawrence McMillan in his Friday summary:

- “In summary, for all the panic in Thursday’s trading, it didn’t really show up in the indicators except for the change in $VIX to a bearish status. So at this time, we have sell signals from breadth, put- call ratios, and $VIX. But what we don’t have — and this is extremely important — is a breakdown below support from $SPX. Hence we are not getting bearish unless support at 1950 is broken.”

But one major streak was broken this week, with S&P moving more than 1% on both Thursday & Friday. Is that important?

- Friday after-market – Ryan Detrick, CMT @RyanDetrick – So we go 62 days without a 1%, then have two in a row. Last time had two consecutive 1% moves was April 9 and 10. $SPX $SPY.

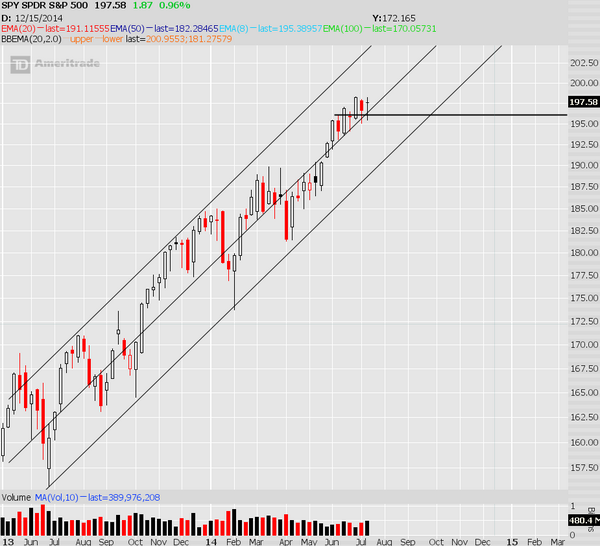

The SPY made broke the 50-day moving average & closed at $181.51 on April 11 and then began the rally that continues. So will the S&P go again on a 9% rally to say $215? Detrick did not say but we noticed the following on Friday afternoon:

- Joe Kunkle @OptionsHawk – $SPY Oct 210 Calls just traded size at $0.19 offers, 15K or so

- Joe Kunkle @OptionsHawk – $SPY – Our channel in play forever projects to around 210 for Oct. for upper rail touch pic.twitter.com/IoMbIlyuoL

And Kunkle did prove correct in his tweet on Thursday:

- Joe Kunkle @OptionsHawk – $IWM next week $114 calls starting to buy in size, 40,000 buying to open

Long duration Treasuries had a better week than stock indices this week with the 30-year yield falling to new 2014 of 3.26%, slightly below the 3.29% close on May 28, 2014. The action on Friday did not detract from the big move of this week. Last week, J.C. Parets had written “I have to stick with the bulls. At least for now“. That worked very well. What did he say this week?

- Friday – J.C. Parets @allstarcharts – long-term rates flat on the day even with stock market flying $TYX – Bonds highest weekly close since May 2013. Still look great $TLT $ZB_F.

The real story in bonds is the drop to 1.16% in the German Bund 10-year yield leading Rick Santelli to say on Thursday:

- “… look at Bunds. this goes to 2011. boy, we are in record territory, I tell you, at 1.16%, anybody think we will not test 1%? it’s drawing it like a magnet.”

With both Treasuries & Bunds falling in yield, surely emerging market debt should be doing well. What does this say about EM equities?

- Friday – Michael A. Gayed,CFA @pensionpartners – If emerging market credit is leading, what does that say about emerging market stocks. pic.twitter.com/pDh129SqBh

Last week, J.C. Parets recommended “Buying Brazil & Selling Germany”. This trade worked well this week with EWZ up 3.7% & EWG up 39 bps.

2. The Fed & the Markets

The Fed ventured into a rarely trodden area this week with comments on valuation & relative valuation of bonds and stocks:

- “The Committee recognizes that low interest rates may provide incentives for some investors to “reach for yield,” and those actions could increase vulnerabilities in the financial system to adverse events. While prices of real estate, equities, and corporate bonds have risen appreciably and valuation metrics have increased, they remain generally in line with historical norms. In some sectors, such as lower-rated corporate debt, valuations appear stretched and issuance has been brisk.”

GaveKal Capital took exception to this analysis in their article Cognitive Dissonance?. They wrote:

- “Over the last five years, the S&P 500 and the spread between high yield bonds and US Treasuries have moved largely in lock-step, with an 82% correlation.”

- “In the last year, the assets have exhibited a 95% correlation. Interestingly, in June, high yield spreads started to back up while the equity market powered ahead. It feels like we have seen this sequence before.”

- “In June 2007, high yield spreads reached a maximum low relative to US Treasuries of 2.48% and stocks peaked four months later only 1% higher. Over the following 18 months, high yield spreads backed up to 20% while stocks fell from 1561 to 666.”

(source – GaveKal)

Stan Druckenmiller compared today’s credit markets to 2007 in his conversation with CNBC’s Joe Kernen in their Delivering Alpha conference on Wednesday:

- “corporate credit is growing at a record rate. far faster than it grew in 2007, and s&p pointed out that 71% of debt issued is a “B” rating. or worse. to put that in perspective, in the ’90s, that number was 31%“.

- “do you remember all the hull la baloo in ’07 about covenant light they did $100 billion in ‘07, loans? and 38% of them were “B” rated. This year, we’re going to do $300 billion. we did $260 billion last year. up from $90 billion a year and 58% of them are “B’ rated. so anybody who says they’re not a bubble, I just don’t agree with it”

But Druckenmiller doesn’t think today’s bubble is a systemic problem, because it “has not infiltrated the banking system” yet.

The above discusses the specifics of this year’s Humphrey-Hawkins testimony by the Fed. But is this testimony itself important as an inflexion point for markets? That is what Todd Harrison suggested via the chart below in his article on Minyanville.com:

3. Apple-IBM partnership & Fox’s offer for Time Warner

By 4:30 pm, Chair Yellen’s congressional testimony was forgotten because of an amazing partnership announced by Apple & IBM, a wow-type visionary merging of old Tech & new Tech, the much-awaited breakthrough for Apple in the enterprise world & an outlet for IBM’s Big Data capability. Both stocks soared in the after market and opened higher on Wednesday morning, a morning made doubly euphoric by Fox’s bid for Time Warner. But,

- Wednesday – Bespoke @bespokeinvest – Apple ($AAPL) opened up nearly $2 on the $IBM partnership and has traded down all day. Now in the red. $IBM still up 2%.

The reason IBM stayed up was because of optimism about next day’s IBM’s earnings which fell flat and $IBM fell.

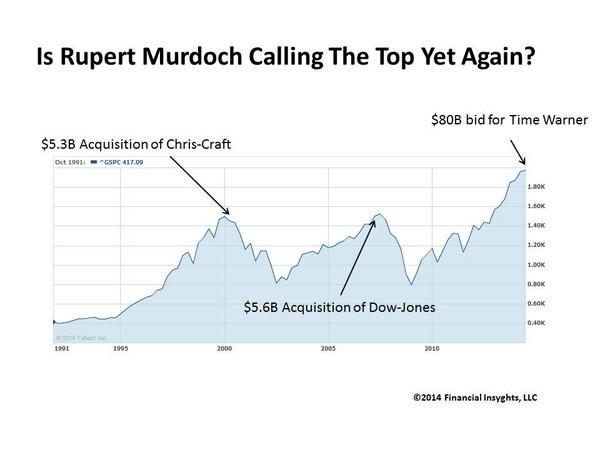

Time Warner ($TWX) shot up on Wednesday morning and actually moved higher, a testimony to Mr. Murdoch’s famous determination and possibility of others stepping in. A more interesting action developed that morning regarding a chart about offers by Mr. Murdoch and the subsequent action of the stock market. The chart was first, to our knowledge, tweeted pre-open by

- Peter Atwater @Peter_Atwater – Murdoch’s bid for Time Warner may be the best bearish contrarian market indicator yet. @Minyanville pic.twitter.com/tlpxXoI47C.

This chart went viral and led to:

- Peter Atwater @Peter_Atwater – Art cashin faxes my chart to @saraeisen who takes a photo of it which she tweets which @m_udland uses for @businessinsider. Just like that.

A detailed discussion of the above chart can be found in Peter Atwater: The Serious Thinking Behind the ‘Dumbest Chart Ever‘ on Minyanville.

4. Delivering Alpha Conference

There is a huge difference between hedge fund managers & non-performance managers like mutual fund managers, advisors & brokers. Only hedge fund managers win or lose big when their investors win or lose big. Generating competitive returns in good markets and not losing money in bad markets is critical to their success or even existence. This makes them similar to individual investors, at least to the basic goal of individual investors. So we always listen when we get a chance to hear successful hedge fund managers.

A best place to hear many such is the annual Delivering Alpha conference of Institutional Investor & CNBC. Since we are deemed “untouchable” in the ultimate caste-system sense by CNBC, we prefer to watch & listen on TV. Below is a quick summary of what CNBC broadcast & posted on their website:

- “we’re right on the border of where we were in ‘1999 – . 93% of IPOs went public and never made a dime. today it’s 80%. the only time in history we’ve approached that. those who say how great ipos are encouraging investment, … it’s myopic. good for employment today but not if all the high-tech firms in ’99,u get a job, laid off or fired or your company goes bust.”

Leon Cooperman think that S&P will hit 2,000 this year but:

- “The markets finally found a fair level, … I expect the rate of appreciation to slow.” He said the market was not yet priced to perfection, noting the market was in a zone of “okay.”

- His stock ideas –

- Growth at reasonable price = Actavis, Citigroup & Thermo Fisher.

- Income & growth = Atlas Energy, Gaming and Leisure Properties, KKR & Nordic American Offshore

- Asset restructure plays = Louis XIII Holdings, Monitise & SandRidge Energy.

Larry Robbins of Glenview Capital Management:

- “Our single best idea is a theme: companies should be levering up now,” he said. Among his specific stock picks were Thermo Fisher Scientific and Monsanto Co.

Mary Callahan Erdoes of JPMorgan Asset Management:

- “People who aren’t as informed are going into the bond market….they don’t understand the effects of duration and convexity and what will happen eventually. That’s the most dangerous part of this,”

- ” … The U.S. economy is on great footing,” she said, noting increased credit card debt and low delinquencies as examples. “The economy looks strong.” When asked if we were in a credit bubble today, Erdoes said no. “It’s not a bubble if we grow into it, it’s a bubble if it stops right now,”

5. Gold

Gold & Silver opened the week with a huge thud on Monday and fell hard again on Tuesday after the Yellen testimony – recovered some of the losses on Wednesday and exploded up on Thursday to give up some of the gains on Friday. On the week, Gold & Silver fell by 2% & 2.7% resp. The miners dropped even more.

So what does the #1 Gold Timer so far of 2014 (according to Times Digest) say? In his article Fishing Around For a Gold Cycle Bottom, Tom McClellan writes:

- “The price bottom associated with gold’s 13-1/2 month cycle is ideally due right now. The problem is that gold does not always bottom exactly when it is supposed to … we should see a price low at the cycle bottom which goes below the December mid-cycle low. That means a dip to below around $1190/oz.

- another feature of some of these cycles … is the tendency to see a late blowoff move just ahead of the final cycle low.

- my interpretation is that the June 2014 pop in gold prices is another example of this late blowoff behavior, and that we still have the final “thud” yet to come. If that final down move arrives before late August, it would still be considered to be a case of the cycle bottom arriving “on time”, given that +/- 1 month tolerance.”

Send your feedback to [email protected] OR @MacroViewpoints on Twitter