Summary – A top-down review of interesting calls and comments made last week about monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

1. Double Bottom or Draghi/Tepper?

Jim Cramer put it succinctly on his Mad Money show on Friday:

- “A lot of things are going wacky all at once here … we have to respect the bond market because when it takes violent action it can leave tremendous damage in its wake; what we know from the spring of 2013, the velocity of the move is what freaks people out … today’s action seemed a bit ominous;as interest rates moved up dramatically …”

Treasury yields have spiked up as if they were shot out of a mortar. The action is reminiscent of 2013 after Bernanke stunned investors with his taper warning in May 2013. Except for bounce for an hour or so after the Nonfarm Payroll number on last Friday, and a 5-10 minute bounce after this Thursday’s 30-year auction, there has been no bounce in long duration Treasuries, just consistent downward action at varying speeds. It’s almost as if Treasuries have the Ebola virus and everyone is trying to run away from them.

Remember David Rosenberg throwing in the proverbial towel on Thursday, August 28?

- The “new normal” is that U.S. Treasury yields are more tightly linked to market rates in Europe than they are to domestic economic trends”

- “only a fool would now stand now in front of either train, as difficult as it may be to explain how a 2-handle in Treasury yields can possibly coexist with a 2K-handle in the S&P 500.”.

Guess what? Rosie should have doubled down that Thursday instead of blaming fools. Because the 10-year yield is up 27 bps since August 28, TLT is down 5% and the S&P is down 10 handles or 50 bps.

We have heard may explanations for the violent spike in treasury yields, the most common being Draghi-Europe. But that doesn’t fit the data. The week after Draghi’s Jackson Hole speech was great for treasuries & TLT rose 1.4% that week. And Draghi’s stunning QE announcement came 4 days after treasury & bund yields had started rising hard.

The bottom of yields was on Thursday, August 28 with the 30-year closing at 3.076%, the 10-year closing at 2.34% & 10-year Bund yield closing at 88 bps; Yields reversed that Thursday afternoon, went up again a few bps on Friday 8/29 and began spiking up on Tuesday after labor day. We cannot find any reason for the small reversal in yields on Thursday afternoon except to point to the classic double bottom in 10-year yield at 2.34%. That morning looked like a panicky fall in yields and then suddenly it stopped & reversed that afternoon. By the time Draghi stunned investors with his QE on Thursday 9/6, both the 10-year Bund yield & 30-year yield had already rallied 7 bps from Thursday, August 28 to Wednesday, September 5. Clearly, the Bond market, in its collective wisdom, moved first and then the data & fundamentals followed.

What moved decisively on Draghi QE Thursday were the Euro and the U.S. Dollar. The Euro has remained at the same level post Draghi-QE day but the Dollar kept rallying, yields kept rising & commodities kept falling violently post-Draghi.

As we go into next week’s FOMC meeting, the consensus is as intensely committed as we have seen for a long time. If 2013 was a taper tantrum, the past 12 trading days have been a rate-hike storm. Will Yellen be able to calm this storm next week or will her comments covert it to a hurricane? Next week should be something with the Fed & Scotland referendum.

2. Bernanke vs. Greenspan

The 30-year Treasury yield rose 8.7 bps & the 10-year yield rose 6 bps on Friday and TLT decisively broke through support of its channel. Was that due entirely to the strong retail sales number & the sentiment number? Or was there something else? That something was Ben Bernanke speaking at Morgan Stanley according to Keith McCullough of Hedgeye who said the following in his Macro Notebook on Friday morning:

- “My pal Bernanke who was with the boys at Morgan Stanley yesterday started talking about his GDP forecast, … he is highly convicted in his view… that consensus isn’t bullish enough on Q3, Q4 and 2014 GDP growth. and he is also talking up interest rates. … that moved the bond market big time … Mr. Bernanke you just imposed one heck of lot of volatility in the bond market into the Fed meeting and yes we continue to think bond yields go lower not higher in 2014.”

Given the importance of this scoop & the direct style of Keith McCullough, we include the entire youtube clip below:

Who might argue with ex-Chairman Bernanke about the forward GDP growth? How about ex-Chairman Greenspan who said the following to CNBC’s Kelly Evans on Wednesday:

- “It is certainly an indication that the Fed’s secondary impact on the economy after its impact on long term interest rates is now beginning to take hold; how significant it is & whether this is another false dawn remains to be seen; I am a little skeptical that it is more than a short term phenomenon but this is a very difficult type of thing to forecast because we have never seen anything like this before.”

Who will current Chair Yellen side with next week? And will the bond market listen to her or go about in its own convictions? As Greenspan told Kelly Evans:

- “market forces are going to be more fundamental here than Fed’s discretionary actions”.

3. Guru opinions about Yellen & Treasury yields

Gundlach & Rosenberg agreed this week on Yellen and on yields.

- Gundlach on CNBC SOTS – I dont hear Janet Yellen saying that; I hear some of her associates saying that;she seems to be concocting excuses why not to raise rates anytime soon; I don’t think Janet Yellen wants to raise interest rates; I don’t think there is much of a reason to raise interest rates;

- Gundlach on rates on CNBC SOTS – bottom may be in European rates; I do think bottom is in US rates; & if we go to the big picture; the bottom is US rates was back in 2011; us rates are rising; but they are rising very slowly & that’s going to remain the case for a couple more years; … will trade in a range 2.20-2.80%

- Rosenberg on Reuters – there is 100% chance they will change the wording; they changed a lot of it in the previous meeting; but to expect changes that alter expectations of first rate hike being mid 2015, I don’t see that happening at all; big scuttlebutt is they may get rid of considerable period; but as long as they have those words “significant”, “unused capacity” which is really Janet Yellen’s core view = we are not doing anything unless we see sustainable signs we have taken out the slack from the job market

- Rosenberg on rates on Reuters – bond rally has already come to an end; we touched 2.30%, now at 2.5%; cant justify 2.5% 10-yr note when the nominal GDP is 4%;they are usually within basis points of each other; bonds, in my opinion, are more expensive than stocks are right now; 10-yr by year-end will be 2.75%.

Bill Gross seems to be agree, we guess based on:

- Lisa Abramowicz @LisaAbramowicz1 – Pimco’s Bill Gross says it’s a good time to lever up on credit investments. http://bloom.bg/1CWNLri via @BloombergNews

Larry McDonald of NewEdge is a courageous & smart investor who likes to jump into swirling waters as he demonstrated on CNBC Closing Bell on Friday:

- “I think the 10-yr is a screaming buy here … I think next week the slack in the labor force is gonna force Janet Yellen to increase her dovish position; I think US 10s can go back to 2.30% over the next 6 months;”

His segment-mate, Tom Essaye of Kinsale Trading, disagreed completely:

- “bond buying fever of 2014 breaking before our eyes; it is breaking in Europe as the ECB finally targets inflation & growth & it is breaking here in the US; lows are in; everyone seems to agree that rise in yields will be gradual & take time; I would not be surprised if we see 3% on the 10-year may be before end of the year or very early in 2015;”

Based on our empirical observations, the real action in long duration yields & TLT takes place when the 200-day is broken. Those levels are 2.65% & $110 resp.

What about immediate technicals?

- Mark Newton @MarkNewtonCMT – Treasury ylds likely to find at least some resistance here @ 2.61-2-Skeptical we see immediate Followthrough pic.twitter.com/pIgTeqvh6g

4 Equities

Not surprisingly, stocks had a choppy week. But long term & medim term bulls were undeterred:

- Craig Johnson of Piper Jaffrey on Friday on CNBC Closing Bell – made the case of his target of 2,350 on the S&P.

- Tony Dwyer on CNBC FM 1/2 on Tuesday – raised his year-end target to 2230 from 2185 – the change came is from earnings estimates; we have been below the street at $115; we are looking for $117.50; (& 19 PE) … Partying like 1996 – in August 1996, you were following a 34% up year in 1995; you were up more than 8% into August and you closed the year up 20%; … market correlates to the direction of earnings & that is still clearly higher; it should drag in fund flows; I want to be in the financials, I want to be in technology, basically I want to be in anything that is related to capital spending; all the data is showing capital spending is picking up;as long as that takes place, you want to be in people that lend them the money, that get them the money, capital formation; industrials, technology and even some health care;

Then you have bullish gurus who are short term bearish:

- Rosenberg on Reuters – “market has gone ahead of itself; seasonality; internals – lack of breadth, very narrow leadership, lot of technical aspects of the market that are looking very heavy right now; valuations are too high – 5-10% correction, excellent buying opportunity to buy back some quality names; like financials, industrials, technology, capital spending is making a comeback;”

- Jeffrey Saut on Friday – “Plainly, I would feel more comfortable, at least on a trading basis, if the SPX had backed off for a full retracement of its recent rally to the 1965 – 1970 support zone, but they don’t operate the equity markets for my benefit. On a trading basis the D-J Industrials (INDU/17049.00) have now traded into the high end of the typical 17 – 25 session “buying stampede,” leaving them vulnerable in the short run. Additionally, looking at the candlestick charts, yesterday’s action shows a “spinning top” formation. This morning, however, the futures are flat despite new sanctions by the European Union against Russia, the yes/no vote pending from Scotland, France’s tattered budget agreement, 2400 now dead from the Ebola virus, and as the U.S. dollar heads for its best upside run in 17 years”

Speaking of bears, you gotta begin with Marc Faber & his comments on CNBC Futures Now on Thursday:

- “we are in a kind of late stage rally, we are not likely going to get a correction but likely a bear market that will be 20-30% at some point … I think the credit market will weaken first; we are gonna go down on October-November, there will be a rebound & may be no new highs; it would be my view; because if you look at the list of new highs, its been diminishing very rapidly; we are close to an all-time high but number of stocks hitting new highs is very poor at the present time & the number of stocks hitting new 12-month lows is increasing, so the technical picture of the market is not particularly good and the U.S. is the most pricey market compared to other markets in the world“

On the next bearish scale, you have 2007 comparisons:

- Keith McCullough on Hedgeye on Monday – “I haven’t been this bearish since 2007“ – much much different this time is liquidity ; people are not going to able to get out, of small mid-cap stocks, there was a lot more liquidity in 2007 than today in equities

- Chris Kimble of Kimble Charting on Yahoo Finance in Home builders diverging again, similar to 2005-2007 – “The above chart [see below] reflects that the DJ Home Construction Index diverged against the S&P 500 for almost two years (2005-2007) before both of them fell in price together from 2007 to 2008. … The home construction index has now diverged against the S&P 500 for almost a year and a half. Humbly, I believe it is worth investors time to watch this divergence and to be careful should home builders and the broad market break support together.”

5. Gold & Commodities

Gold, Silver & Oil got trashed again this week. But Tom McClellan argues for an “upward phase” in gold in his article Gold – Watch the €1000 Level:

- “Gold is still in a downtrend, if you examine a chart of gold prices measured in dollars. But gold in euros looks much stronger, and that’s actually a bullish condition, eventually. … I have found that when the two plots disagree, it is usually the euro price plot that ends up being right about where both are headed.”

- “Gold is due for a new upward phase now, according to the 13-1/2 month cycle that I addressed here back in July. The ascending phase of a new 13-1/2 month cycle is usually where the big gains are found. But first, gold has to finish up the business of putting in a bottom. “

- “The way I see it, once gold starts upward and breaks up through the €1000 euro level, a “recognition wave” of follow-on buying will occur as euro-based traders recognize that the €1000 level has been breached. Gold is currently at €960/oz, so it does not have far to go to make such a breakout.”

The real question is where does Gold put in its bottom?

- Friday – Joe Kunkle @OptionsHawk – $GLD large monthly bear pennant, below 113 heads back to 95 pic.twitter.com/Cu9swkAsPj

What about Silver?

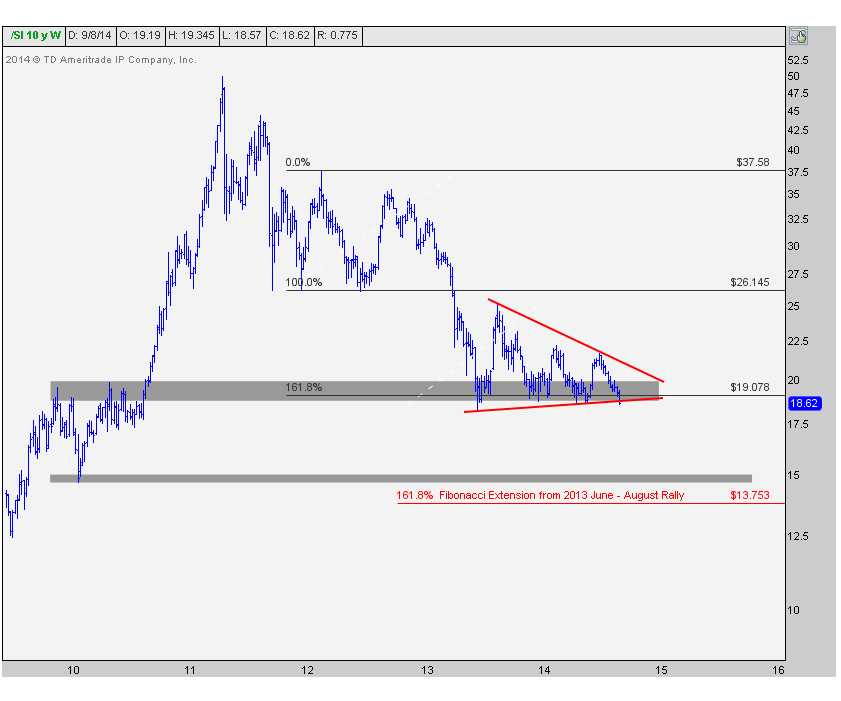

- Thursday – J.C. Parets @allstarcharts – The Downside Target in Silver is Under $15 http://dlvr.it/6tHdgf

In his article, Parets writes “one of the scariest looking charts in the world today has to be Silver” and explains his rationale for his $15 target.

On the other hand,

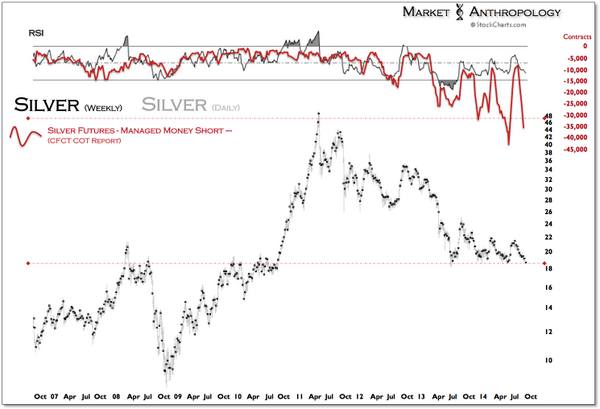

- Thursday – Market Anthropology @MktAnthropology – Silver COT from last week.Expect we see new record MM short after this wk.Back @ LT support w/another bounce on deck pic.twitter.com/MkG3ZvqEy5

What about Oil?

- Thursday – Dana Lyons @JLyonsFundMgmt – From earlier >”Oil Ready To Stop Getting Drilled? $USO hitting support at $34″ Post: http://stks.co/s0lE9 Chart: pic.twitter.com/YFOGW7ks9H

Send your feedback to [email protected] Or @MacroViewpoints on Twitter