Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

1. Channel for monetary policy

The smart & sensible Tony Crescenzi had made it clear a couple of weeks ago when he said the Fed transmits its monetary policy through four channels including the bond market, the stock market and the Dollar. The Fed has to be frustrated with the bond market’s refusal to price in higher inflation expectations. The Dollar isn’t doing what they wanted. Remember they tried to talk the Dollar down via their “new & improved” Fed minutes released on Wednesday, October 8. That didn’t work so well. That leaves the Fed’s most favorite channel and the key, in their mind, to keeping the economy on the right trajectory – the U.S. stock market.

And how do they manage their transmission via this channel? Recall the “hawkish” Fed statement on September 17. We all know what happened to the stock market in late September & early October. So on Wednesday, October 8, the Fed released minutes of the September 17 meeting that were 180-degree opposite of the Fed statement on September 17. That created the rally but it lasted only one day. Then came the flash crash in Treasury yields on Wednesday, October 15. So, the very next day, they sent James Bullard, St. Louis president, to talk about possibly pausing the taper in the October 29 FOMC meeting. Did that do the trick? The Dow is up 1250 points from the close on pre-Bullard Wednesday, October 15 and the S&P is up 156 handles, in 12 trading days. So the Fed reverted back to their “hawkish” stance in the FOMC statement on October 29, a stance that was 180-degree opposite to the Fed “minutes” released on October 8.

So it should be clear to all. The Fed’s ability to exit QE depended on the stock market behaving itself and the Fed ensured that. The stock market is their preferred channel and the linchpin of their “maintain asset-prices” strategy for economic growth & inflation expectations.

Frankly, their tactics also worked because of the October effect – the absolute requirement to juice up returns for year-end. The entire performance fee industry is based on the dire need to mark up their returns in the last two months of the year. So when Bullard reminded them that the Fed’s put is still married to their portfolios, the gallop began. This is essentially why Paul Richards of UBS told CNBC FM 1/2 that he was “so bullish, that it hurts“.

The role played by Bullard was seconded by Forexlive.com on Friday in their article Years from now people will look at October stock market charts and ask what happened.

“As the market closes after one of the craziest months in years, I have no answers. I can assure you, I was in front of my trading screens for 12 hours a day and I didn’t miss a single headline. … The S&P 500 fell 8% and then rallied 10.85% and the bond and FX markets were equally crazy. … I can offer no coherent explanation for the panic or the incredible recovery in markets. … After all the carnage, one headlines stands out: Bullard saying the Fed could keep QE going…. If I had to wager a guess, I’d still say Bullard changed the psychology of the market and made everyone realize that US growth is in a pretty good spot and cheap oil will help”.

2. “Its like Pebble Beach …”

That was the succinct buy call from investor & CNBC star Kevin O’Leary. His point was simple – just as the Japanese came in to buy highly valued Pebble Beach in 1990, Japan is coming to buy US Stocks now. So people should buy stocks and then sell them to the Japanese. He also put it another way using more acceptable terms like “PE expansion”. The US stock market took that to heart – even sectors that were down despite the Fed on Thursday, like Transports, Semis, rallied strongly on Friday.

If Paulsen wanted a bazooka, Kuroda brought a howitzer. Not only did he raise his QE from 70trillion in JGBs to 80 trillion, the Japanese pension fund doubled its equity allocations for both domestic & overseas stocks from 12% to 25%. All of a sudden, Kuroda became “Mrs. Watanabe”, to use a 2005-2007 term. With dollar soaring against the yen, wouldn’t they buy the safest stocks they can – US stocks of course. This, we believe, was O’Leary’s logic.

Japanese stocks shot up as if they were scalded – unhedged EWJ was up 5%. yen-hedged DXJ was up 6.6% and Small cal DXJS was up 7.20% on Friday. CNBC FM trader Josh Brown has been a fervent fan of Japanese stocks and of DXJS in particular. He took a modest victory lap on Friday and remained bullish arguing “ this is the beginning not the end of the [Japanese] economy getting stronger“.

There is no the slightest question that Friday’s explosion came from Kuroda’s howitzer. Those who want charts & facts should listen to Santelli’s recital on Friday:

.

We don’t get why Scott Wapner decided to question facts so vehemently at the end of this clip. Yen didn’t collapse, Nikkei didn’t explode, global stocks didn’t rally for any other reason except the volley from Kuroda’s howitzer. As Art Cashin said on Friday morning:

- “all the relationships we have been watching have been swept away by the events in Japan”.

Kuroda again taught a lesson we learned last year – that technical charts sink to the bottom when a monetary tsunami washes over them. And so do comments from veterans who tell us that major lows like Thursday, October 16 need to be retested for confirmation. That wisdom is so pre-QE4. We don’t wait for “W” bottoms anymore, we have the “V”s.

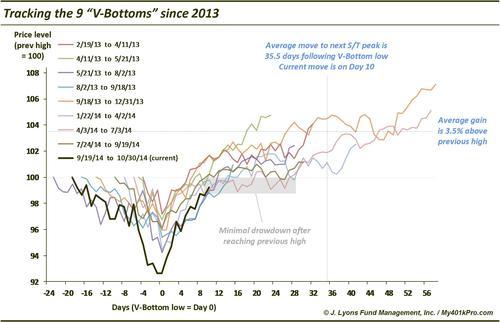

3. Where does this V-bottom take the S&P?

But how do you define a V-bottom? Dana Lyons provides a definition and its target in his article The V-Bottom is STILL in fashion:

- “a 52-week high, a subsequent greater than 3% sell off to at least a 1-month low, a subsequent rally to within 1% of the previous high with at least 7 of 10 days being up and no down days worse than -1%”

Based on this definition, “there have been no less than 9 V-bottoms“, since March 2013. So based on these V-bottoms, what can we expect?

Based on the above, Lyons writes:

- “minimal drawdown (i.e., 1%) from the point the S&P 500 first recovers to within 1% of the previous high (now);”

- “another month of gains: the average rally lasted 35.5 days after the low (today would be day 11);”

- “the S&P 500 at 2080: the average rally has taken the index 3.5% above the previous high (2010)”

Assuming the V-bottom history repeats, there should be another V-bottom 2.2 months after October 16, 2014 – meaning just before Christmas. What could bring about another sell-off in early December? Draghi is expected to announce QE in his December meeting. What if he doesn’t? Art Cashin answered on Friday:

- “the focus next,however, will shift to Mr. Draghi; is he going to get into this game of sweeping cuts and if they don’t produce something that looks like QE, that may take away from what’s happened“.

4. What a week?

The Dow was up 3.5%, the S&P 2.7%, the Nasdaq 3.3% and the Russell 4.9%.

Last week, we wrote:

- “Many people have talked about 2007 but is it possible we see a 1999 type run to the end of the year? The Fed gives a dovish signal, BoJ talks QE on Friday, & Draghi follows up with expectations if not actual buying. The U.S. data comes in OK just like the earnings this week. Republicans take the Senate in November and Ebola becomes less scary. Can we see a stampede into year-end in search of performance?”

This week had a 1999 type feeling to it. What could make this feeling stronger? What if Draghi announces QE or gives strong hints about QE next week? And what if the payroll number comes in just strong enough? Could that trigger a run in November? Don’t the performance managers need such a run for the year-end roses? Paul Richards of UBS argued yes on Thursday on CNBC FM 1/2:

- “the next major macro trade is going to be, if not the hint of QE then at least the start of QE within the next 4-6 weeks; the markets are gonna love that trade; I am equally bullish on stock market & Dollar but on a timing basis, I would take the stock trade because when you look at positioning right now, everybody has had a tough October, they need a new trade, be dragged into this trade in my opinion; so I would go with the stock market first but I would be very quickly following that up by selling the Euro & buying the Dollar; (1.21 – yearend target)”

Remember the low level of active managers early this month flagged by Ryan Detrick last week in the chart below. He had written last week – “The recent reading of 9.97 was the lowest level of equity participation since September 2011. In fact, levels this low have been nice buying opportunities recently.”

:

.

.

If managers were scared before, they became panic stricken after the V-bottom on October 16. This is seen in the big spike in bullishness in the Investors Intelligence survey. But is this a contrary indicator? Not when the market is in an uptrend, according to Tom McClellan in his article on Thursday titled Insights from Investors Intelligence Data:

- “The recent flip back to bullish is a sign of the initiation of a strong new uptrend. … The current market is still arguably in an uptrend, having recovered from a very brief dip below the 200MA. And so the most recent big positive spike in this weekly change indicator should more appropriately be interpreted as a sign of new upward initiation, as opposed to a failing effort during a countertrend rally”

A new strong uptrend from here? That would be something. By the way, MacNeil Curry of BAC-Merrill Lynch gave 2044 & 2080 as his S&P targets in his appearance on CNBC Futures Now on Tuesday. Another interesting target suggestion came from J.C.Parets who combined three patterns – one-year seasonal pattern, 4-year presidential cycle, 10-year decennial pattern – into one composite in his article S&P500 Seasonal Studies Combined. He then gets the following “roadmap”.

One warning sign, at least for the immediate term, could be the extended level of the McClellan Oscillator, the most extended in a year according to McClellan’s chart below:

courtesy of mcoscillator.com

This may be why Lawrence McMillan warned on Friday:

- “In summary, all of the indicators are positive. The only negative is that $SPX has risen so far so fast. So the intermediate-term picture is bullish, but the short-term action could be subject to overbought corrections”

Then you have the following:

- Friday – Hedgeye @Hedgeye EXCERPT: @KeithMcCullough in today’s AM Newsletter

5. Treasuries – the dog that didn’t bark?

A fast emotional, & huge up week in the stock market should lead to treasuries falling in price. Not this week , not in long maturity Treasuries. The 30-year yield rose by a miniscule 2 bps & TLT fell merely by 50 bps this week. The 10-year yield did rise by 10 bps and the 2-5 year yields rose by a smoking 11-12 bps. Meaning the curve flattened dramatically. This flattening has been the relentless trade of 2014, a reminder that the 30-year T-bond market “disagrees with the stock market wholeheartedly” to use a quote of John Lekas on CNBC Futures Now on Thursday.

Rates will remain in range according to Paul Richards & Mohammed El-Erian who define the range as 2.20- 2.60%. Let’s see what the payroll number suggests next week.

- Joe Kunkle @OptionsHawk – $GLD chart posted back in September is playing out….UGLY

- Friday – Charlie Bilello, CMT @MktOutperform – Junior gold miners down -83% from 2011 peak. But don’t expect to hear “value” buyers talking up these names.

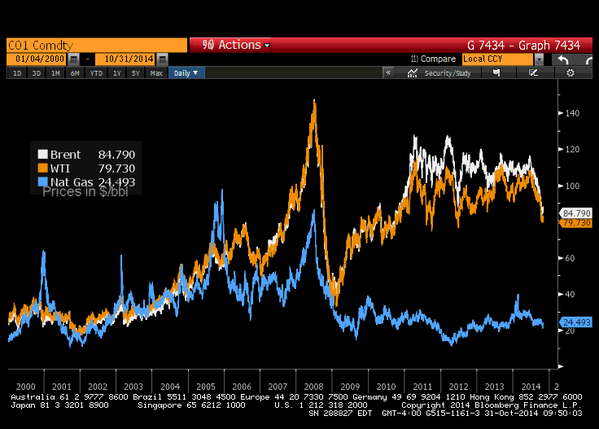

What about Oil?

- Friday – Todd Harrison @todd_Harrison #Crude < $80 is either A) part of the new paradigm (see #Gold) or B) the single greatest heads-up in the history of deflationary heads-ups.

- Friday – Erik Schatzker @ErikSchatzker – What if oil went back to trading in step with natural gas? Uh, that’d be $25 a barrel.